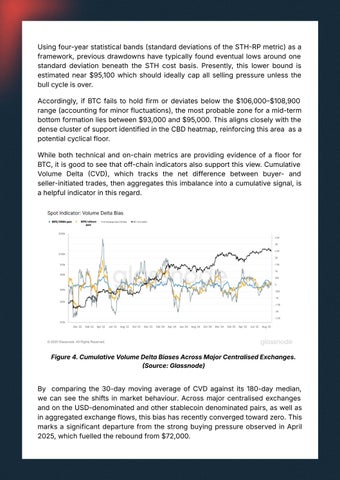

Using four-year statistical bands (standard deviations of the STHRP metric) as a framework, previous drawdowns have typically found eventual lows around one standard deviation beneath the STH cost basis. Presently, this lower bound is estimated near $95,100 which should ideally cap all selling pressure unless the bull cycle is over. Accordingly, if BTC fails to hold firm or deviates below the $106,000$108,900 range (accounting for minor fluctuations), the most probable zone for a mid-term bottom formation lies between $93,000 and $95,000. This aligns closely with the dense cluster of support identified in the CBD heatmap, reinforcing this area as a potential cyclical floor. While both technical and on-chain metrics are providing evidence of a floor for BTC, it is good to see that off-chain indicators also support this view. Cumulative Volume Delta CVD, which tracks the net difference between buyer- and seller-initiated trades, then aggregates this imbalance into a cumulative signal, is a helpful indicator in this regard.

Figure 4. Cumulative Volume Delta Biases Across Major Centralised Exchanges. Source: Glassnode)

By comparing the 30-day moving average of CVD against its 180-day median, we can see the shifts in market behaviour. Across major centralised exchanges and on the USD-denominated and other stablecoin denominated pairs, as well as in aggregated exchange flows, this bias has recently converged toward zero. This marks a significant departure from the strong buying pressure observed in April 2025, which fuelled the rebound from $72,000.