> CBRE:

Approaching Shadows of Data Opacity and Risk From Flexible Office Market By David Casas Alarcón CBRE Property Management Accounting Lead

We live in a world that offers and value tailored convenience. We are accustomed to the smartphone, the internet, transit options and retail offerings delivering more flexibility than ever before.

N

ew business models cater for people’s preferences, disrupting retail and hospitality sectors. Office space has its own catalyst for change — one that addresses companies’ desire for more flexibility while putting the focus on the human experience of the workplace. Flexible space solutions mean lease agreements that can be procured quickly, with variable terms, and little capital improvement required. This brings profound implications for occupiers and investors, challenging many aspects of the established office leasing model. SUB-LEASING OFFICE SPACE Co-working is the category that has shown the biggest growth over the past four years. Operators lease office space to the landlord, and sub-lease it to individuals, providing shared areas with the equipment and services of a state-of-the-art corporate workplace.

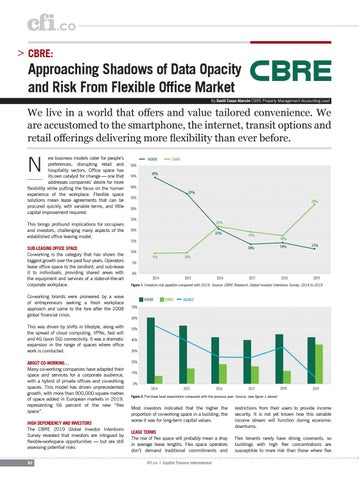

Figure 1: Investors risk appetite compared with 2019. Source: CBRE Research, Global Investor Intentions Survey, 2014 to 2019.

Co-working brands were pioneered by a wave of entrepreneurs seeking a fresh workplace approach and came to the fore after the 2008 global financial crisis. This was driven by shifts in lifestyle, along with the spread of cloud computing, VPNs, fast wifi and 4G (soon 5G) connectivity. It was a dramatic expansion in the range of spaces where office work is conducted. ABOUT CO-WORKING… Many co-working companies have adapted their space and services for a corporate audience, with a hybrid of private offices and co-working spaces. This model has driven unprecedented growth, with more than 900,000 square metres of space added in European markets in 2019, representing 56 percent of the new “flex space”. HIGH DEPENDENCY AND INVESTORS The CBRE 2019 Global Investor Intentions Survey revealed that investors are intrigued by flexible-workspace opportunities — but are still assessing potential risks. 82

Figure 2: Purchase level expectation compared with the previous year. Source: (see figure 1 above)

Most investors indicated that the higher the proportion of co-working space in a building, the worse it was for long-term capital values. LEASE TERMS The rise of flex space will probably mean a drop in average lease lengths. Flex space operators don’t demand traditional commitments and CFI.co | Capital Finance International

restrictions from their users to provide income security. It is not yet known how this variable income stream will function during economic downturns. Flex tenants rarely have strong covenants, so buildings with high flex concentrations are susceptible to more risk than those where flex