> Otaviano Canuto on Central Banks and Climate Change:

Turning Black Swans Into Green

There are three possible motivations for the engagement by central banks with climate change: financial risks, macro-economic impacts, and mitigation/adaptation policies.

R

egardless of the extent to which individual central banks incorporate the three prongs of motivations, they can no longer ignore the issue.

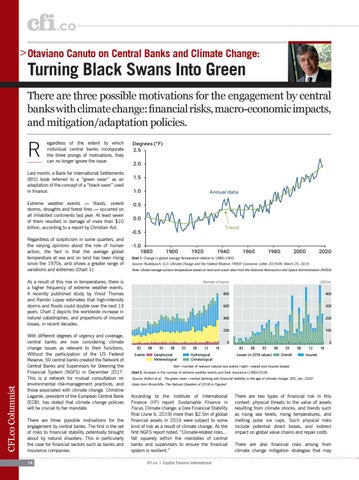

Last month, a Bank for International Settlements (BIS) book referred to a “green swan” as an adaptation of the concept of a “black swan” used in finance. Extreme weather events — floods, violent storms, droughts and forest fires — occurred on all inhabited continents last year. At least seven of them resulted in damage of more than $10 billion, according to a report by Christian Aid. Regardless of scepticism in some quarters, and the varying opinions about the role of human action, the fact is that the average global temperature at sea and on land has been rising since the 1970s, and shows a greater range of variations and extremes (Chart 1).

Chart 1: Change in global average temperature relative to 1880–1900.

Source: Rudebusch, G.D. Climate Change and the Federal Reserve, FRBSF Economic Letter 2019-09, March 25, 2019. Note: Global average surface temperature based on land and ocean data from the National Aeronautics and Space Administration (NASA)

CFI.co Columnist

As a result of this rise in temperatures, there is a higher frequency of extreme weather events. A recently published study by Vinod Thomas and Ramón Lopez estimates that high-intensity storms and floods could double over the next 13 years. Chart 2 depicts the worldwide increase in natural catastrophes, and proportions of insured losses, in recent decades. With different degrees of urgency and coverage, central banks are now considering climate change issues as relevant to their functions. Without the participation of the US Federal Reserve, 50 central banks created the Network of Central Banks and Supervisors for Greening the Financial System (NGFS) in December 2017. This is a network for mutual consultation on environmental risk-management practices, and those associated with climate change. Christine Lagarde, president of the European Central Bank (ECB), has stated that climate change policies will be crucial to her mandate. There are three possible motivations for the engagement by central banks. The first is the set of risks to financial stability potentially brought about by natural disasters. This is particularly the case for financial sectors such as banks and insurance companies. 14

(left - number of relevant natural loss events | right - overall and insured losses) Chart 2: Increase in the number of extreme weather events and their insurance (1980-2018).

Source: Bolton et al, The green swan - central banking and financial stability in the age of climate change, BIS, Jan. 2020 (data from MunichRe, The Natural Disasters of 2018 in Figures)

According to the Institute of International Finance (IIF) report Sustainable Finance in Focus, Climate change: a Core Financial Stability Risk (June 6, 2019) more than $2.5tn of global financial assets in 2016 were subject to some kind of risk as a result of climate change. As the first NGFS report noted: “Climate-related risks… fall squarely within the mandates of central banks and supervisors to ensure the financial system is resilient.” CFI.co | Capital Finance International

There are two types of financial risk in this context: physical threats to the value of assets resulting from climate shocks, and trends such as rising sea levels, rising temperatures, and melting polar ice caps. Such physical risks include potential direct losses, and indirect impact on global value chains and repair costs. There are also financial risks arising from climate change mitigation strategies that may