6 minute read

DANT & R.USSELL, Inc.

for protection against the invasion of lumber markets by competitive materials; and, second, so that wood can be used as an alternate for more of the materials in short supply.

In any discussion of construction materials, it should be noted that the next session of Congress is likely to approve some sort of expanded highway program. E,nactment of a more liberal federal-aid-to-education program, including subsidies for school construction, is another possibility. Once enacted, both these programs would be competing against other classes of construction for available materials, further tightening the supply and creating ne\\' opportunities for the use of lumber.

The U.S. Forest Service's preliminary report on its recently completed Timber Resource Review contains many encouraging facts that promise an abundance of wood for present needs and for the years ahead. This abundance of wood further underscores the need for developing new markets through research and trade promotion.

Unfortunately, the USFS, in its advance press statements relative to the TRR, has seen fit to ignore or play down certain facts brought out by the review. This "scarism" technique is a continuation of the dire forecasts of a timber famine that have all too freguently been issued by the USFS in past years. (See Page 64.) In commenting onthe Timber Resource Review, the Forest Service tells us: "The nation's timber requirements are expected to be so high by the end of the century that timber growth t'ill need to be from 7O to I20/o greater then than it no'w is. Improved forest management at recent

PAtrIFIG COAST Fcl REST PRODUGTS

FRESNO OFFICE

P. H. (PAT) IYNAN

IU'UTBER DIVISION O DOUGLAS FIR PONDEROSA PINE

.

FIR-TEX DIVISION

. FIR.TEX TIIE.PIANK-BOARD

FIR-IEX ACOUSTICAL TIIE

FIR.TEX HARDBOARD

FIR.TEX ROOFDEK

FIR-TEX SHEATHING

. DOUGLAS FIR PTYWOOD HARDBOARD OVERTAY

FRESNO 9-49s9

SACRAIIENTO OFFTCE

HUGH CRABB

HUnter 2-O52O rates of progress appears unequal to providing a balance between cut and growth at the year 2000 "

Based on the record of lumber's use in the last half century, the product development of our competitors and other factors, there is nothing to indicate any such total imbalance by the year 2C00. Such misleading government statements do nothing to encourage the use of lumber and other forest products. Here are a few facts from the Timber Resource Review that cannot be ignored:

The TRR shows 489 million acres of commercial forest land, against 461 million acres in 1945;2,094 billion board feet of sawtimber, against 1,6O1 billion feet in 1945 ; cubic volume growth of all timber 32/o greater than the cut, against an approximate balance of cut and growth in 1945; sawtimber growth and cut about in balance, against a growth deficit ot 5o/o in 1945.

Private forestry enterprise is meeting today's needs and will meet the needs of the future if the law of supply and demand is permitted to operate-and if our consumers aren't frightened away from the use of wood by unfounded predictions of timber shortages.

Flere are some of the many other factors that influence lumber prospects for the coming year: l. Do-it-yourself enthusiasts bought a significant volume of lumber and wood products during 1955 and there is every reason to believe that this market will continue to grow in the year ahead.

2. It is still too early to predict with certainty the full effects of the higher minimum wage voted by the first session of the 84th Congress. There are indications, however, that the increase will cause some dislocation of production. A number of the smaller, marginal operators in our industry may be forced to close down when the higher minimum becomes effective on March l. cerand

3. Military lumber purchases by the Corps of Engineers are expected to increase in the months ahead. Corps officials figure that they purchased about 430 million board feet of lumber and wood products for the military services during fiscal 1955 which ended last June 30. For fiscal 1956, the Corps expects its military purchases to tetal approxim.ately 510 million board feet--€O million more than in fiscal 1955.

4. With farm income down, this segment of the economy must be expected to spend less for building and maintenance work. It should be remembered, however, that lumber has always been the most popular building material among farmers and, with farm income off, lumber's economy will give it an ever greater edge in farm building plans that are carried out.

Bolstering the general confidence of U.S. business and industry are the prospects of a balanced budget and tax reduction in the near future. The outlook for a balanced budget is especially welcome at this time. Certainly, if a country cannot operate on a balanced budget in times of relative prosperity, there is little hope of avoiding deficit financing in a less active period.

When all the factors that make for prosperity and a level of business activity are collectively considered, tainly there is just cause for optimism about the future the year ahead for the lumber industry.

Notionol Assn. of Home Builders Tokes Shorp lssue Wirh Government's Tightened Credir Restrictions

Studies by the federal government rvhich have recently become available on vacancies, household formation, and consumer housing arrangements and buying plans support the proposition that 1955's housing volume is in line with both the market and population trends.

The studies also indicate the strong likelihood that we are improving the total quality of our housing by removing poorer housing fromthe existing supply at a far faster rate than had previously been assumed.

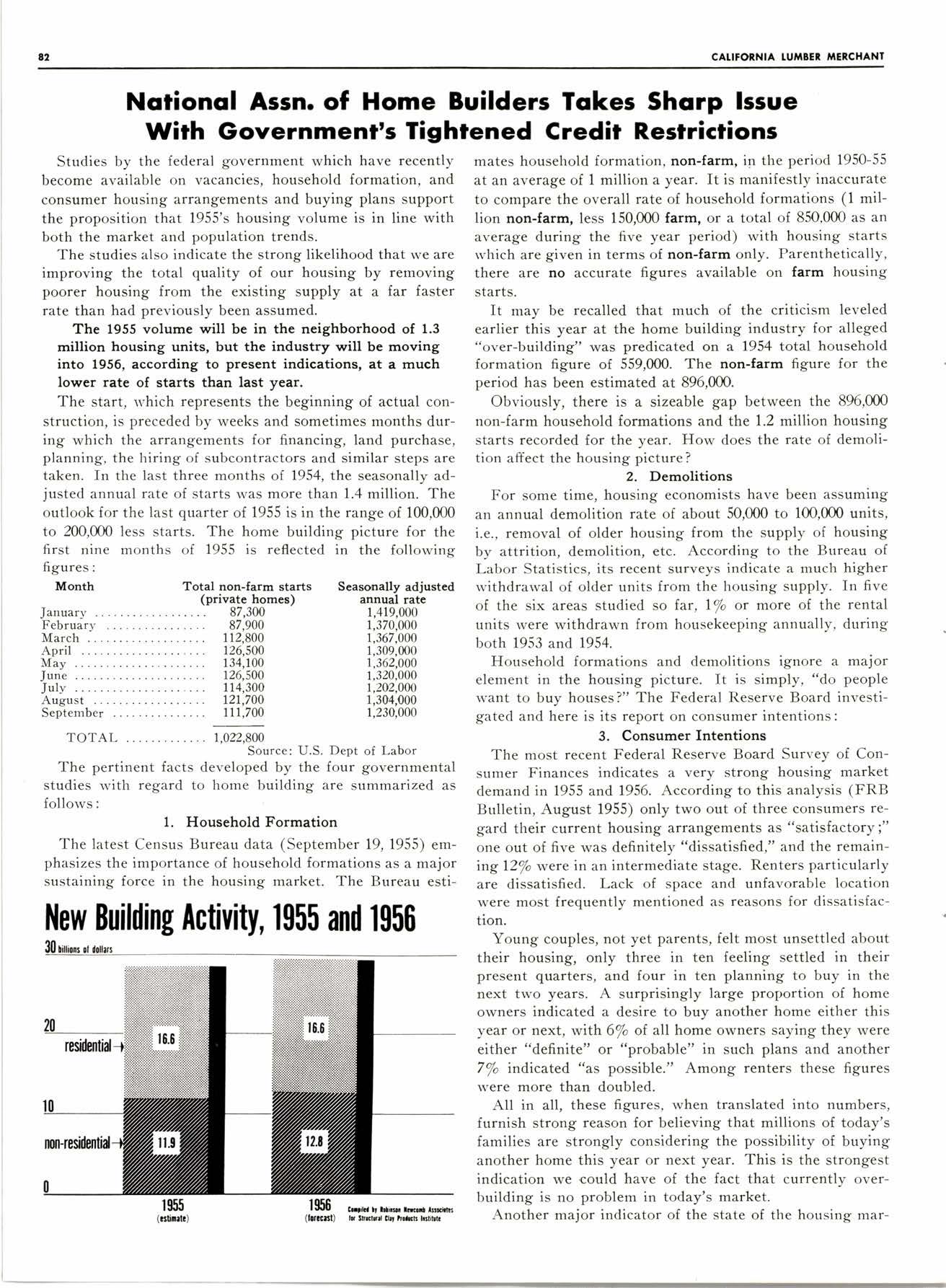

The 1955 volume will be in the neighborhood of 1.3 million housing units, but the industry will be moving into 1956, according to present indications, at a much lower rate of starts than last year.

The start, lvhich represents the beginning of actual construction, is preceded by weeks and sometimes months during which the arrangements for financing, land purchase, planning, the hiring of subcontractors and similar steps are taken. In the last three months of 1954, the seasonally adjusted annual rate of starts was more than 1.4 million. The outlook for the last quarter of 1955 is in the range of 100,000 to 200,000 less starts. The home building picture for the first nine months of 1955 is reflected in the following figures: mates household formation, non-farm, in the period 1950-55 at an average of 1 million a year. It is manifestly inaccurate to compare the overall rate of household formations (1 million non-farm, less 150,000 farm, or a total of 850,000 as an average during the five year period) with housing starts rvhich are given in terms of non-farm only. Parenthetically, there are no accurate figures available onfarm housing starts.

It may be recalled that much of the criticism leveled earlier this year at the home building industry for alleged "over-building" was predicated on a 1954 total household formation figure of 559,000. The non-farm figure for the period has been estimated at 896,000.

Obviously, there isa sizeable gap between the 896,000 non-farm household formations and the 1.2 million housing starts recorded for the year. How does the rate of demolition affect the housing picture ?

2. Demolitions

For some time, housing economists have been assuming an annual demolition rate of about 50,000 to 100,000 units, i.e., removal of older housing from the supply of housing by attrition, demolition, etc. According to the Bureau of Labor Statistics, its recent surveys indicate a much higher withdrawal of older units from the housing supply. In five of the six areas studied so far, l/o or more of the rental units were withdrawn from housekeeping annually, during both 1953 and 1954.

Household formations and demolitions ignore a major element in the housing picture. It is simply, "do people want to buy houses?" The Federal Reserve Board investigated and here is its report on consumer intentions:

3. Consumer Intentions

The pertinent facts developed by the four governmental studies with regard to home building are summarized as follows:

1. Household Formation

The latest Census Bureau data (September 19, 1955) emphasizes the importance of household formations as a major sustaining force in the housing market. The Bureau esti-

The most recent Federal Reserve Board Survey of Consumer Finances indicates a very strong housing market demand in 1955 and 1956. According to this analysis (FRB Bulletin, August 1955) only two out of three consumers regard their current housing arrangements as "satisfactory;" one out of five was definitely "dissatisfied," and the remaining l2/o were in an intermediate stage. Renters particularly are dissatisfied. Lack of space and unfavorable location were most frequently mentioned as reasons for dissatisfaction.

Young couples, not yet parents, felt most unsettled about their housing, only three in ten feeling settled in their present quarters, and four in ten planning to buy in the next two years. A surprisingly large proportion of home owners indicated a desire to buy another home either this year or next, with 6/o ot all home owners saying they were either "definite" or "probable" in such plans and another 7/o indicated "as possible." Among renters these figures were more than doubled.

All in all, these figures, when translated into numbers, furnish strong reason for believing that millions of today's families are strongly considering the possibility of buying another home this year or next year. This is the strongest indication we ,could have of the fact that currently overbuilding is no problem in today's market.

Another major indicator of the state of the housing mar-