3 minute read

Cost of Building Materials Holding Level Movement, Government Survey Shows

Calling attention to predictions made in these columns in November that the upward movement of the cost of building materials would be checked by the end of the year, Southern California Homes Foundation cites the Labor Department's Index of Wholesale Prices for the week ending February 1 as evidence that costs have moved on a level for the past month.

The wholesale index of prices for building materials, the Foundation points out, was 99.5 for the week ending February 1, compared with 99.6 for the week ending December 28. Lumber showed a wholesale price decrease of .7 point for the week ending January 25. Among 22 irol,portant commodities listed, only three had a greater price decrease than lumber.

"Progressive local dealers in building materials have in. dividually made every effort to keep retail prices down despite their own mounting costs," declares C. W. Pinkerton, chairmal of Southern California Homes Foundation. "This has been a simple matter of good business, to protect the home-building market by keeping the small home of today easy to own and more house for the money. The confidence of the public has been won by the building industry on this proposition, and it shall not be lost. We have every reason to believe that the level movement of building-materials prices will continue.

"Meanwhile the building industry's services to the consumer are being expanded month by month. Home-financing costs are lower than in 1939 and no higher than in 1940. There is more ready money for home loans. New types of building materials and home equipment and improved methods of construction make savings for the family building a home.

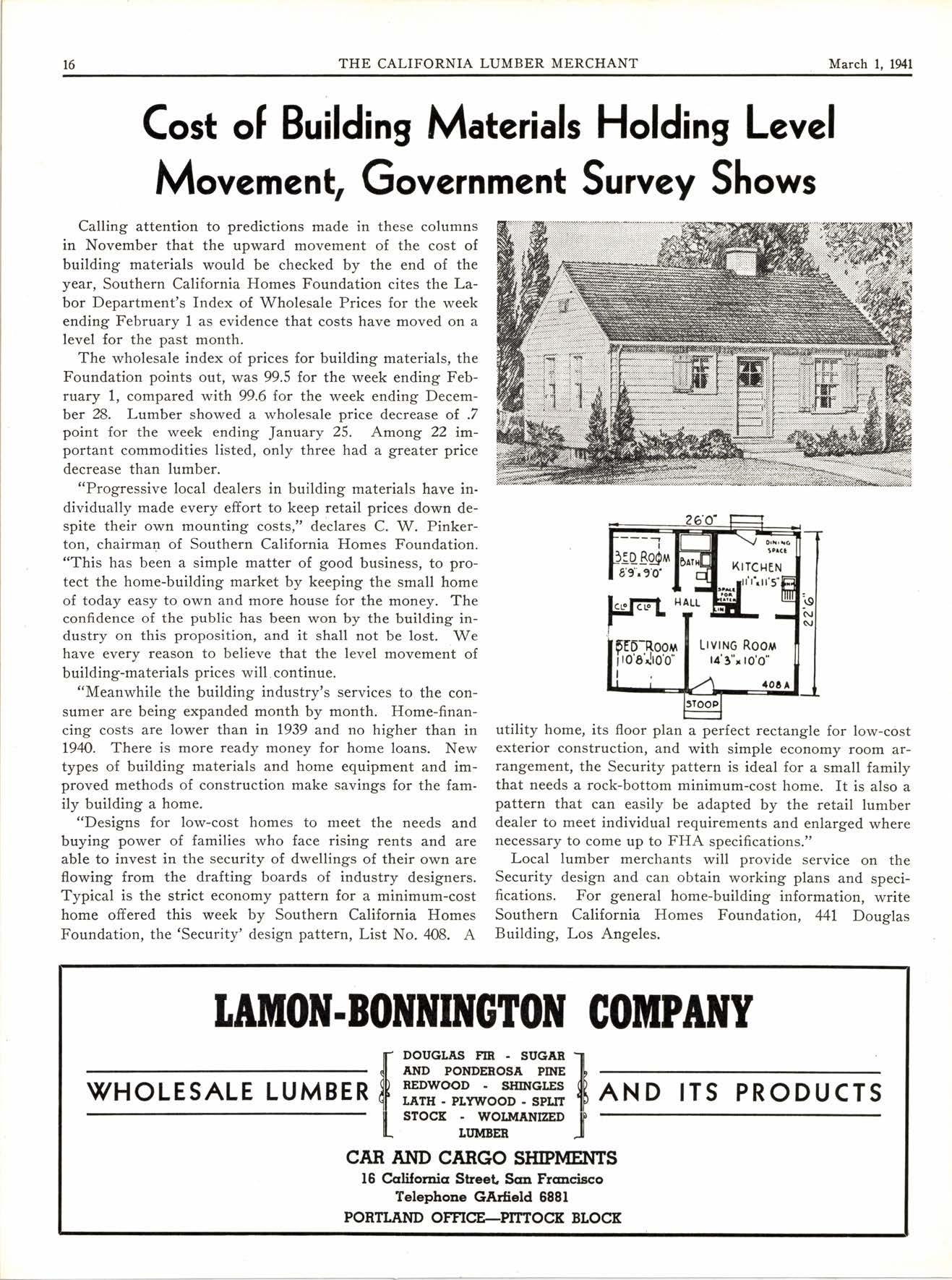

"Desigls for low-cost homes to meet the needs and buying power of families who face rising rents and are able to invest in the security of dwellings of their own are flowing {rom the drafting boards of industry designers. Typical is the strict economy pattern for a minimum-cost home offered this week by Southern California Homes Foundation, the'Security' design pattern, List No. 4OB. A utility home, its floor plan a perfect rectangle for low-cost exterior construction, and with simple economy room arrangement, the Security pattern is ideal for a small family that needs a rock-bottom minimum-cost home. It is also a pattern that can easily be adapted by the retail lumber dealer to meet individual requirements and enlarged where necessary to come up to FHA specifications."

Local lumber merchants will provide service on the Security design and can obtain working plans and specifications. For general home-building information, write Southern California Homes Foundation, 441 Douglas Building, Los Angeles.

Home Building in Northern Californir Shows 45% Gainin January

Home building in Northern California soared to record heights with the dawn of a new year, it was revealed by D. C. McGinness, district director of the Federal Housing Administration, whose January report shows a gain of 45 percent in the number of newly-constructed homes on which mortgages were accepted for insurance over the first month last year.

Construction was commenced on an average of almost 55 new homes, being built in this district under FHA inspection and requirements, every business day during January, Mr. McGinness declared, and the total investment in homes financed under the insured mortgage system averaged, $D2,7I2 a day throughout the month. This was said to include only the 46 counties of the Northern California district.

"It is interesting to note that the home buying public is appreciative of the long repayment period, and the resultant reduction in the amount of monthly payments, permitted under the FHA plan," said the housing director. "An everincreasing number of investors are extending the mortgage term over the maximum period of years.

"This is sound business judgment, because by doing so they not only are reducing home ownership to a less-thanrent basis, but family budgets of the future thus are provided every possible protection."

Citing the fact that an FHA-insured mortgage may be paid off at any time the borrower's finances permit, regardless of the number of years for which the mortgage originally was written, Mr. McGinness said this provision definitely is to the benefit of the home owner.

"Let's assume that a $4000 mortgage is insured f'or a maximum term of 25 years, the payments on principal, 4l percent interest and mortgage insurance would averag'e $26.25 a month," explained the housing official. "IJnder present FHA regulations the borrower is permitted to pay, in addition to monthly installments, as much as 15 percent of the face amount of the loan in any one year, without a prepayment premium.

"On a $4000 insured mortgage this amounts to an additional payment on principal of $600 a year, and on that basis the entire indebtedness could be comrpletely wiped out in about six years, although the mortgage originally might have been written for 25 years. It can be repaid in full at any time with a prepayment premium of one percent, which in this case would amount to only $4O.

On the other hand, if some unforeseen circumstance should slash serious inroads into income at any time during this period, the home owner's investment is thoroughly protected and the entire transaction kept in good standing by merely meeting the minimum payments of less than a dollar a day."

As evidence of the increasing popularity of long-term home financing, Mr. McGinness called attention to the fact that of all mortgages on newly-constructed homes insured last year by the Federal Housing Administration, g2 percent were written for terms ranging from 20 to 25 years.