INTERNATIONALTRADE

The MINT countries Fact or Fiction? With the arrival of a new acronym for potential markets the British Chamber of Commerce has a handy “Market Snapshot” on their Export Britain website which will help you make up your own mind. This edition we take a look at Indonesia. http://exportbritain.org.uk/international-directory/#ms

Indonesia

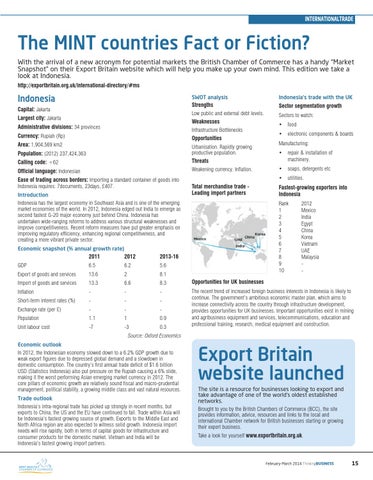

SWOT analysis Strengths Low public and external debt levels. Weaknesses Infrastructure Bottlenecks Opportunities Urbanisation. Rapidly growing productive population. Threats Weakening currency. Inflation.

Capital: Jakarta Largest city: Jakarta Administrative divisions: 34 provinces Currency: Rupiah (Rp) Area: 1,904,569 km2 Population: (2012) 237,424,363 Calling code: +62 Official language: Indonesian Ease of trading across borders: Importing a standard container of goods into Indonesia requires: 7documents, 23days, £407. Introduction Indonesia has the largest economy in Southeast Asia and is one of the emerging market economies of the world. In 2012, Indonesia edged out India to emerge as second fastest G-20 major economy just behind China. Indonesia has undertaken wide-ranging reforms to address various structural weaknesses and improve competitiveness. Recent reform measures have put greater emphasis on improving regulatory efficiency, enhancing regional competitiveness, and creating a more vibrant private sector. Economic snapshot (% annual growth rate) 2011 2012

2013-16

GDP

5.6

6.5

6.2

Indonesia’s trade with the UK Sector segmentation growth Sectors to watch: • food • electronic components & boards Manufacturing: • repair & installation of machinery, • soaps, detergents etc • utilities.

Total merchandise trade Leading import partners

Fastest-growing exporters into Indonesia Rank 1 2 3 4 5 6 7 8 9 10

2012 Mexico India Egypt China Korea Vietnam UAE Malaysia -

Export of goods and services

13.6

2

8.1

Import of goods and services

13.3

6.6

8.3

Opportunities for UK businesses

Inflation

-

-

-

Short-term interest rates (%)

-

-

-

The recent trend of increased foreign business interests in Indonesia is likely to continue. The government’s ambitious economic master plan, which aims to increase connectivity across the country through infrastructure development, provides opportunities for UK businesses. Important opportunities exist in mining and agribusiness equipment and services, telecommunications, education and professional training, research, medical equipment and construction.

Exchange rate (per £)

-

-

-

Population

1.1

1

0.9

Unit labour cost

-7

-3

0.3

Source: Oxford Economics Economic outlook In 2012, the Indonesian economy slowed down to a 6.2% GDP growth due to weak export figures due to depressed global demand and a slowdown in domestic consumption. The country’s first annual trade deficit of $1.6 billion USD (Statistics Indonesia) also put pressure on the Rupiah causing a 6% slide, making it the worst performing Asian emerging market currency in 2012. The core pillars of economic growth are relatively sound fiscal and macro-prudential management, political stability, a growing middle class and vast natural resources. Trade outlook Indonesia’s intra-regional trade has picked up strongly in recent months, but exports to China, the US and the EU have continued to fall. Trade within Asia will be Indonesia’s fastest growing source of growth. Exports to the Middle East and North Africa region are also expected to witness solid growth. Indonesia import needs will rise rapidly, both in terms of capital goods for infrastructure and consumer products for the domestic market. Vietnam and India will be Indonesia’s fastest growing import partners.

Export Britain website launched The site is a resource for businesses looking to export and take advantage of one of the world’s oldest established networks. Brought to you by the British Chambers of Commerce (BCC), the site provides information, advice, resources and links to the local and international Chamber network for British businesses starting or growing their export business. Take a look for yourself www.exportbritain.org.uk.

February-March 2014 ThinkingBUSINESS

15