12 minute read

We don't need a winner. Why a single shipping company won't turn the tide of the fuel market – but the industry at large can (if it only wants to, with the help of policies and other sectors)

by Ewa Kochańska

Wärtsilä’s Sustainable fuels for shipping by 2050 – the 3 key elements of success report outlines what actions are needed to ensure that green fuels become mainstream in the maritime sector within the next three decades. “The future is in our hands,” states the report, pointing to decisive policies, industry-wide and multi-sector collaboration, and individual action as necessary for positive outcomes in decarbonising maritime transport. The report underscores that even though future fuel timelines can be provided – based on data collected and careful analysis – the outcomes will be most influenced by action or lack thereof today.

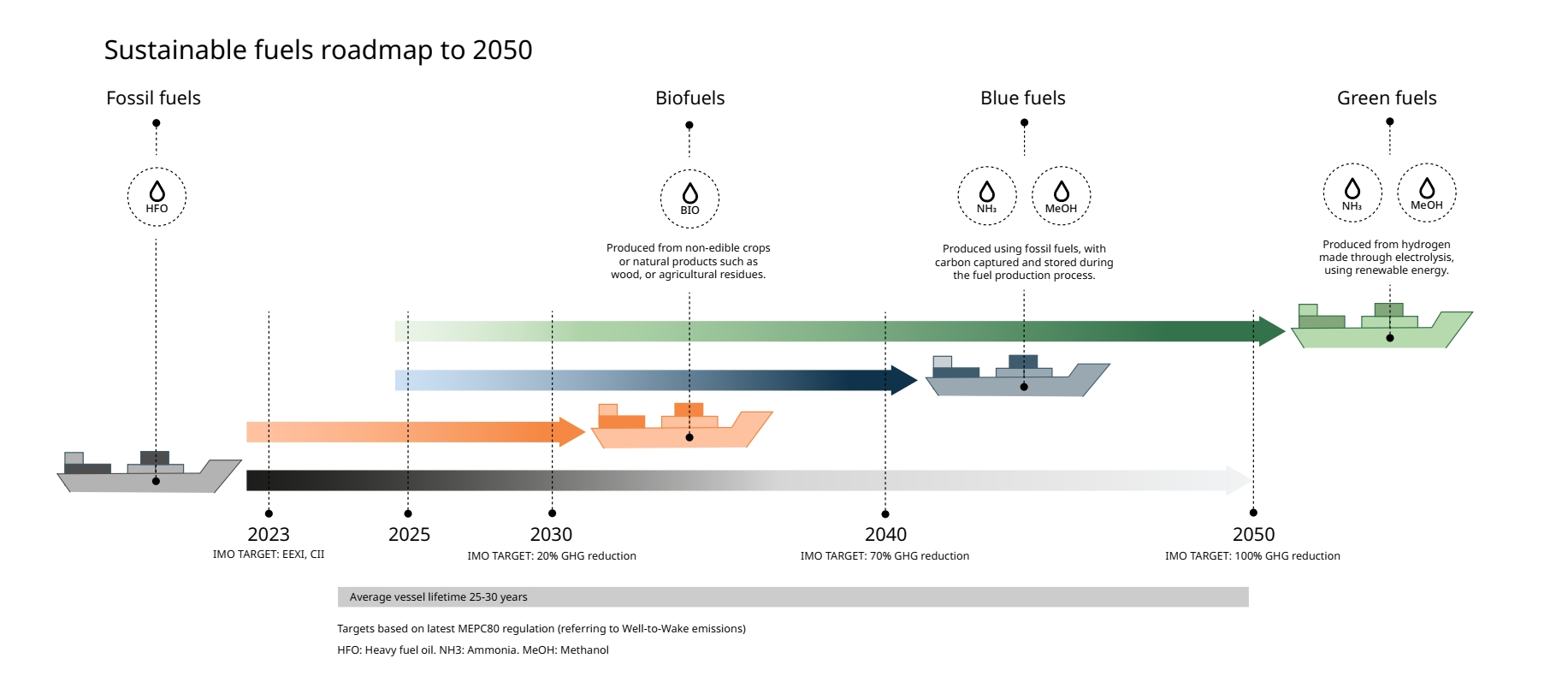

Presently, most vessels are powered by heavy fuel oil (HFO) or marine gas oil. A 2020 study by the International Maritime Organization (IMO) estimated that, without intervention, CO 2 emissions from shipping could rise by over 45% by 2050. On the other hand, achieving net-zero emissions by that year would require about $5 trillion in investments for fleet renewal and equipment upgrades. It is clear that full electrification is not a viable solution for all maritime transport, as long-distance travel would require a lot of energy without refuelling options. While measures like reducing vessel speed by 30% and maximising energy efficiency could cut energy demand by 15-27%, the sector cannot completely decarbonise without transitioning to sustainable fuels.

Viable fuels and their cost

According to the market analysis conducted for the report, biofuels (derived from inedible plants, organic materials like wood, or leftover agricultural products) are first in availability and are expected to see substantial expansion by the 2030s. This category includes biofuels similar to diesel, biomethanol and biomethane (as well as bioethanol, which is already produced in large quantities, particularly in Brazil and the US). For biofuels to remain environmentally friendly, they must be derived from sustainable biomass sources such as waste fats, oils, and greases, ensuring they do not compromise food security or land availability.

Following are blue fuels, such as blue ammonia, emerging as transitional options due to their easier scalability compared to zero-carbon alternatives. These are made using fossil fuels, but the carbon generated during production is captured and stored. Blue fuels are fit for the existing infrastructure and resources of the oil and gas industry.

Last will be green synthetic fuels, which are expected to become more widespread by the late 2030s or early 40s. These fuels, produced from hydrogen generated via electrolysis and powered by renewable energy, hold strong potential. Production is likely to be concentrated in regions with ample space and beneficial environments for solar and wind energy.

However, it is worth noting that for operators to seek the one best fuel among the ecologically sustainable choices could be a mistake. “Shipping doesn’t need a [fuel] winner – it needs a mix of fuels to cater to the different requirements of the whole industry,” underscores the report.

Concerning the financial aspect, Wärtsilä’s projections suggest that by 2030, sustainable fuels will be 3-5 times more expensive than currently are fossil fuels. Nonetheless, it is important to keep in mind that comparing future sustainable fuel costs to today’s fossil prices does not account for new regulations (already being implemented) that raise fossil fuel costs. Policies, such as the EU Emission Trading System and the block’s latest sector-specific Regulation, FuelEU Maritime, could create price parity between fossil bunkers and sustainable fuels as early as 2035. That, combined with the impact of efficiency measures and increased investment in sustainable fuel supply chains, should result in a change in cost dynamics in the sector.

The report also highlights that to achieve full decarbonisation by 2050, the shipping industry will require approximately 270 million tonnes of alternative fuels equivalent to HFO. Aside from the sizable fuel supply, the sector will also require significant investments in fuel infrastructure, new ships, and equipment upgrades across the global fleet. DNV estimates that annual spending will need to range from $8 billion to $28 billion on ships and $28 billion to $90 billion on scaling up production, fuel distribution, and bunkering infrastructure to meet the demand for carbon-neutral fuels by mid-century.

To help achieve carbon-neutrality in maritime, there needs to be a coordinated effort between policymakers, industry, and operators to drive the systemic changes needed for advancing production, infrastructure, supply chains, and technology for sustainable fuels. The shipping industry can learn from the global power sector’s shift to clean energy, where collaboration helped scale new solutions. For instance, photovoltaics were considered the costliest way to reduce carbon emissions in 2014, but it became the cheapest source of electricity just six years later. Solar and wind have rapidly become the most cost-effective electricity sources in just a decade, driven by clear and ambitious policies that enabled largescale development and cost reductions. Investment in sustainable fuels, regulatory incentives, and growing demand can stimulate supply and reduce fuel costs.

There is no ‘I’ in ‘team’

One of the biggest challenges to shipping’s decarbonisation efforts is ambivalence. Operators struggle to choose a fuel due to limited production and uncertainty over which technology will scale more efficiently. Simultaneously, fuel producers hesitate to increase production without assured demand. This uncertainty leaves shipowners, fuel producers, and other transport and logistics stakeholders in a state of inaction. However, with proper policies that aim to provide stability and are implemented quickly, sustainable fuel production will accelerate, breaking this cycle. Wärtsilä’s report lists several steps that policymakers can take to scale up sustainable fuel use in the maritime sector. First, to deliver certainty and stability, they should establish an internationally agreed upon, science-based pathway to phase out fossil fuels in alignment with IMO targets. This will provide operators with a consistent global timeline for planning investments and signal suppliers to ramp up sustainable fuel production.

Second, adopting a global standard for marine fuel carbon pricing and reinvesting CO2 tax revenues into the shipping industry will boost cost competitiveness, eventually achieving parity with fossil fuels and encouraging the development of sustainable alternatives.

Finally, increasing global collaboration between governments on innovation and infrastructure is essential to the widespread delivery of sustainable fuels. This can be achieved by participating in initiatives like the global Zero-Emission Shipping Mission or by working closely with the IMO to set global standards, ensuring a level playing field and avoiding regulatory disparities.

Industry collaboration is of pivotal importance, too. The report underscores that no single ship operator can generate enough demand to scale sustainable fuels; collectively, however, the industry can influence global markets. Owners-operators need to unite on the importance of low-carbon options. Additionally, decarbonisation requires the involvement of the entire ecosystem, including carriers, ports and terminals, manufacturers, shippers, investors, and energy suppliers. While smaller operators, who form a large part of the industry, often lack the resources to invest in sustainable fuels, larger fleet owners have the means to do so.

There is an opportunity to merge resources to scale sustainable fuels across the industry rather than just in isolated areas. Although some smaller carriers are advancing in areas like electrification, the broader sector risks falling behind if they are not included in decarbonisation plans. By pooling purchasing power through sector-wide procurement agreements, multiple operators can combine their demand, leading to lower fuel prices, reduced supply chain costs, and streamlined administrative responsibilities. Further, the industry should focus on sharing skills and knowledge by creating a centralised knowledge hub. Such a centre, supported by global maritime organisations like the IMO or the Getting To Zero Coalition, would allow smaller operators (who may not be able to have dedicated sustainability teams) to access the tools and expertise to plan for sustainable fuels.

This collective approach will also help build consensus on preferred fuels and signal demand to producers, ensuring that shipping secures a significant portion of the limited supply. This is important

because the sector will compete for sustainable fuels with other sectors, like aviation, industry, and long-distance trucking, all of which are on their own decarbonisation paths, too. This competition could limit fuel availability for shipping and keep prices elevated for an extended period. However, if the shipping industry is proactive, it can position itself as a leader by quickly establishing infrastructure and supply chains and adopting cleaner fuels on a large scale.

At the same time, collaboration with the mentioned sectors can increase fuel supplies for everyone. These relationships should not be competitive since they all share a common goal of establishing low-carbon fuels as the norm and should work together to build supply chains. The report gives an example of cooperation between the aviation sector, which requires the highest grade of fuel, and shipping, which can use lower grades while still reducing emissions. With proper guidelines, producers could create both fuel grades in the same production process, benefiting both sectors and generating demand while encouraging suppliers to invest with confidence in the growing demand from both industries. By working together with agendas like the International Civil Aviation Organization, the shipping industry can help establish a globally recognised framework for the production and distribution of sustainable fuels. This framework would clarify the fuel grade requirements for each sector, optimising production (and hence adding to producer profits) and increasing availability across international markets.

Acting now

Even though the report uses its modelling to offer the most accurate forecast, it is not possible to foresee all potential disruptions affecting the sector, such as supply chain issues, pandemics, global conflicts, and natural disasters, to name but a few. Therefore, the report includes key steps that individual operators can take to reduce emissions and prepare for future fuels.

First, it is crucial to prioritise efficiency by assessing each vessel’s capacity to implement measures that quickly lower fuel consumption and emissions. Short-term actions, like optimising ship speed and performance, can significantly reduce carbon footprint and prepare for the eventual use of more expensive zero-emission fuels. Combining efficiency measures with technologies like improved propulsion, wind-assisted sailing, and weather routing can further increase savings. This approach is the most straightforward way to meet emission targets and could achieve the entire 20% reduction required by the IMO by 2030 while also protecting against future fuel cost increases.

In addition to that, the IMO’s new Carbon Intensity Indicator (CII) rating scheme, effective from January 2023, makes efficiency a financial necessity. Vessels above a gross tonnage of 5,000 must annually submit ratings based on CO 2 emissions per cargo capacity and distance travelled. A poor CII rating decreases the vessel’s commercial value, makes it difficult to win contracts, and increases its fuel costs. Additionally, new regulations like the Energy Efficiency Existing Ship Index and the Energy Efficiency Design Index set minimum energy efficiency standards for existing and newbuilds, respectively. The FuelEU Maritime goes a (crucial enforcement) step further by penalising non-compliance and awarding those who invested in emission-reduction solutions.

Second, the report warns that investing in the wrong technology could lead to stranded assets if a more competitive fuel or solution emerges later on. That is why investing in fuel-flexible engines that can operate on multiple bunkers or be converted later can pay off in the long run. Already, with alternative fuel supplies still limited, many operators are opting for engines and fuel systems that can run on both sustainable and fossil fuels, allowing them to continue using traditional bunkers until a moment when the switch is necessary. The technology is rapidly emerging, too. In November 2023, Wärtsilä Marine introduced the world’s first four-stroke ammonia engine, which can immediately reduce greenhouse gas emissions by over 70%. According to the report, ammonia, as a key alternative fuel, is now at the forefront of the push toward zero-carbon emissions.

Similarly, in 2022, the Wärtsilä 32 Methanol engine and MethanolPac storage and supply system were launched –the first commercial solutions for using methanol as a marine fuel. By December 2023, four additional methanol engines were added to the lineup, all capable of significantly cutting the carbon footprint compared to traditional fuels while also greatly reducing nitrogen and sulphur oxides plus particulates.

And lastly, operators should “think upstream” – consider the entire supply chain when planning for future fuel needs. They can ensure sufficient fuel availability and protect their assets by applying their knowledge and expertise in future fuels to upstream supply challenges. For example, the container sector can leverage its experience with methanol engines to enhance fuel supply chains, boosting confidence across the industry.

When policy, industry, and individuals come together

According to Wärtsilä’s report, shipping will decarbonise with strong policies, industry collaboration, and proactive efforts from owners-operators. Effective policies will enhance the cost competitiveness of sustainable fuels and signal the demand needed to increase production.

The proliferation of skills and knowledge through industry-wide cooperation is crucial, as it will empower individual companies to turn uncertainty into a competitive edge and reduce operational costs by investing in efficiency and adaptable technologies concerning fuel options.

It is undeniable that sustainable fuels are on the horizon, driven by the IMO’s Marine Environment Protection Committee’s recently revised regulations as well as the EU. While energy efficiency measures offer immediate benefits, they will not suffice for long-term goals. The industry must quickly adopt sustainable fuels, with the success of this transition depending on current actions undertaken by stakeholders.

Lessons from the energy sector show that rapid scaling and cost reductions are possible when policy, industry, and individual actors collaborate to create predictable demand.