16-17-Roger_A4 Temp 21/05/2012 11:37 Page 16

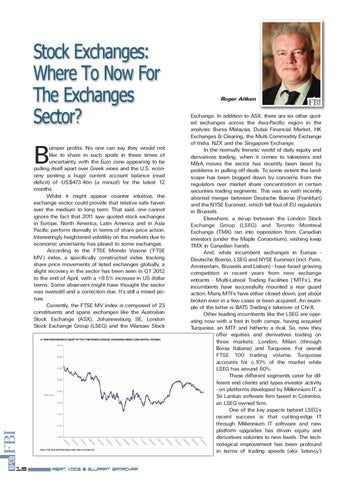

Stock Exchanges: Where To Now For The Exchanges Sector? umper profits. No one can say they would not like to share in such spoils in these times of uncertainty, with the Euro zone appearing to be pulling itself apart over Greek woes and the U.S. economy posting a huge current account balance (read deficit) of -US$473.4bn (a minus!) for the latest 12 months. Whilst it might appear counter intuitive, the exchange sector could provide that relative safe haven over the medium to long term. That said, one cannot ignore the fact that 2011 saw quoted stock exchanges in Europe, North America, Latin America and in Asia Pacific perform dismally in terms of share price action. Interestingly heightened volatility on the markets due to economic uncertainty has played to some exchanges. According to the FTSE Mondo Visione (‘FTSE MV’) index, a specifically constructed index tracking share price movements of listed exchanges globally, a slight recovery in the sector has been seen in Q1 2012 to the end of April, with a +8.5% increase in US dollar terms. Some observers might have thought the sector was oversold and a correction due. It’s still a mixed picture. Currently, the FTSE MV index is composed of 23 constituents and spans exchanges like the Australian Stock Exchange (ASX), Johannesburg SE, London Stock Exchange Group (LSEG) and the Warsaw Stock

B

16

Asian Voice & Gujarat Samachar

Roger Aitken Exchange. In addition to ASX, there are six other quoted exchanges across the Asia-Pacific region in the analysis: Bursa Malaysia, Dubai Financial Market, HK Exchanges & Clearing, the Multi Commodity Exchange of India, NZX and the Singapore Exchange. In the normally frenetic world of daily equity and derivatives trading, when it comes to takeovers and M&A moves the sector has recently been beset by problems in pulling off deals. To some extent the landscape has been bogged down by concerns from the regulators over market share concentration in certain securities trading segments. This was so with recently aborted merger between Deutsche Boerse (Frankfurt) and the NYSE Euronext, which fell foul of EU regulators in Brussels. Elsewhere, a tie-up between the London Stock Exchange Group (LSEG) and Toronto Montreal Exchange (TMX) ran into opposition from Canadian investors (under the Maple Consortium), wishing keep TMX in Canadian hands. And, while incumbent exchanges in Europe Deutsche Boerse, LSEG and NYSE Euronext (incl. Paris, Amsterdam, Brussels and Lisbon) - have faced growing competition in recent years from new exchange entrants - Multi-Lateral Trading Facilities (‘MTFs’), the incumbents have successfully mounted a rear guard action. Many MTFs have either closed down, just about broken even in a few cases or been acquired. An example of the latter is BATS Trading’s takeover of Chi-X. Other leading incumbents like the LSEG are operating now with a foot in both camps, having acquired Turquoise, an MTF and hitherto a rival. So, now they offer equities and derivatives trading on three markets: London, Milan (through Borsa Italiana) and Turquoise. For overall FTSE 100 trading volume, Turquoise accounts for c.10% of the market while LSEG has around 60%. These different segments cater for different end clients and types investor activity - on platforms developed by Millennium IT, a Sri Lankan software firm based in Colombo, an LSEG owned firm. One of the key aspects behind LSEG’s recent success is that cutting-edge IT through Millennium IT software and new platform upgrades has driven equity and derivatives volumes to new levels. The technological improvement has been profound in terms of trading speeds (aka ‘latency’)