1 minute read

Betty’s Bakery

Small Business Manual Accounting & Bookkeeping Practice Set

Close Prior Year Income and Expense Account Balances

Advertisement

After entering the prior year account balances as explained above, the next step requires transferring the prior year income and expense account balances to the Retained Earnings account

This is the process of ‘Closing the Books’ applicable to the previous year’s operational activity resulting in either a profit or loss.

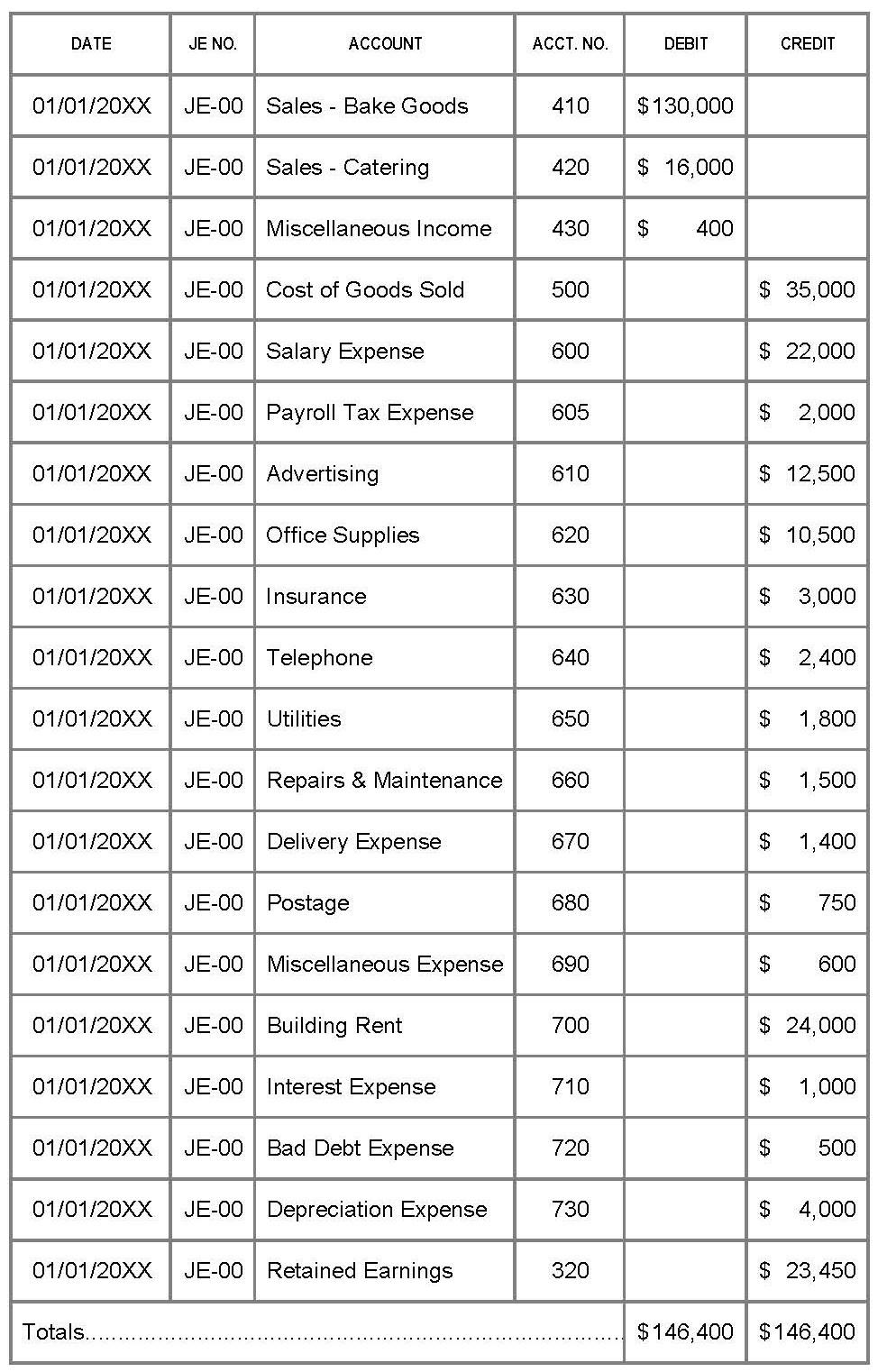

One large General Journal Entry is prepared in which the income account balances are DEBITED and the expense account balances are CREDITED as shown here.

The net difference between the income credit balance accounts and expense debit balance account is the company’s profit or loss

To record the General Journal Entry:

1. Locate the General Ledger at Pages 4.1 to 4.26.

2. For each line item on the journal entry, go to the General Ledger account indicated and enter the date, journal entry number, and amount in the debit or credit column and adjust the account balances

General Journal Entry to Close the Books (Prior Year Income and Expense Accounts)

3. For example, Sales–Baked Goods Account number 410: Date 01/01/20XX, Posting Reference JE-00, enter $130,000 in the debit column, and change the account balance to zero.

Next, review the company’s source documents for the first month of operations for the new year and enter the transactions into the six journals.