22 minute read

IN THIS U.S. FORECAST

• Could Artificial Intelligence (AI) replace your friendly local economic forecaster? Let’s find out.

• The U.S. economy is heading toward a slowdown in the second half of 2023. There is a slight possibility that a recession could be avoided, despite the numerous warning lights on the economy’s dashboard.

• Payroll job growth of 1.6% in 2023 will decelerate in 2024, falling to -1.3%, and contract again in 2025 at -0.5% before turning slightly positive at 0.3% in 2026.

• U.S. consumers powered the 2020 recovery. Following the end of most lockdowns, consumers were ready to spend. Since then, high energy prices, food costs, and housing costs have steadily eroded their purchasing power. While credit card debt and drawing down saving has temporarily patched the hole in their monthly budgets, this loss of purchasing power has set the table for the economic slowdown that approaches.

• Real consumption spending eased to 2.7% in 2022 due to falling real wages. Spending will decelerate to 1.8% in 2023 and then to 0.7% in 2024 before rising to 1.6% in 2025 and 2.3% in 2026.

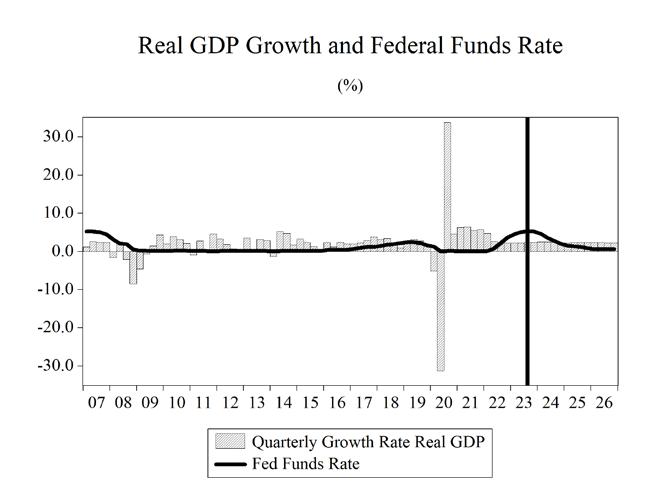

• Real GDP growth was -2.8% in 2020 but accelerated to 5.9% in 2021. It eased to 2.1% in 2022, it will further slow to 1.5% in 2023, slowing further to 0.5% in 2024. Then, real GDP growth will approach 1.3% in 2025, and 1.7% in 2026.

• The housing market remains tight. High prices plus 7% mortgage rates have eroded demand. However, persistently low inventories will reinforce the sector. Housing starts will decline from 1.6 million in 2022 to 1.4 million in 2023, and 1.3 million in 2024, and remain at this level through 2026.

• Despite resistance to the effects of Fed tightening thus far, the headline unemployment rate (U-3) is expected to rise from 3.6% to 6.3% early in 2025 before starting a gradual decline later that year.

• Core consumer price inflation will continue a slow decline in the latter half of 2023, even as energy prices are likely to push the headline consumer price index higher. By the end of 2024, inflation will be close to the Fed’s target level of 2% and interest rate cuts are unlikely to happen before this target is reached.

Everywhere you turn today it is hard to escape a discussion about artificial intelligence (AI). The promise and perils of machine learning. The discussions are reminiscent of those that surrounded the emergence of robotic technology a few decades ago. How many jobs will be lost as this technology replaces human workers? If AI is to replace workers, what jobs are most susceptible?

I suspect the ultimate impact of AI on the economy will be like that of robots: some jobs replaced by the technology, but many jobs receiving a boost in productivity (and pay) from using this new tool. However, I must admit that AI does make me feel a bit uncomfortable.

Robots are more about physical tasks whereas AI is a knowledge-based technology. After all, I never heard of anyone working on an economic forecasting robot, so why worry? Conversely, AI is all about information, more information than I could ever hope to process or retain.

So, to ease my worries or perhaps heighten my anxiety, I decided to give AI a test drive and see what its economic forecasting skills look like.

I set up a ChatGPT account and took AI for a test drive. Below are the AI responses to questions I posed.

Let’s cut right to the chase with the first question.

Default (GPT 3.5)

Ss

What is the outlook for the U.S. economy?

As an AI language model, I can provide you with a general outlook for the U.S. economy based on historical trends and patterns. However, please note that economic forecasts can vary and are subject to change due to various factors and uncertainties. As of my knowledge cutoff in September 2021, here are some key points to consider:

The U.S. economy has shown resilience and recovery following the global economic downturn caused by the COVID-19 pandemic. Fiscal stimulus measures, including government spending and monetary policy support, have helped bolster economic growth.

The labor market has been gradually improving, with declining unemployment rates as businesses reopen and hiring resumes. However, the pace of job creation and the quality of jobs remain important factors to monitor.

Inflation has been a topic of concern, with increased government spending and supply chain disruptions potentially leading to higher prices. Monitoring inflationary pressures and the Federal Reserve’s response will be crucial for economic stability.

The housing market has been robust, with low mortgage rates driving demand for housing. However, affordability challenges and supply constraints could impact the pace of growth in the sector.

Trade tensions and global economic dynamics continue to influence the U.S. economy. Shifts in international trade policies, geopolitical developments, and the pace of global economic recovery can have ripple effects on the U.S. economy.

Technological advancements and innovation across sectors are likely to play a significant role in shaping future economic growth and productivity.

It’s important to note that economic forecasts are subject to change based on a variety of factors, including policy decisions, market conditions, geopolitical events, and unforeseen circumstances. For the most up-to-date and accurate outlook, it is advisable to consult reputable sources such as government institutions, financial institutions, and economic research organizations.

Only using data that ends in September 2021? That’s not going to do, nearly two years of economic data was excluded. We are always looking in the rear-view mirror with economic data, two years is a pretty big gap.

AI was kind enough to throw the Institute for Economic Forecasting a bone in its answer:

“For the most up-to-date and accurate outlook, it is advisable to consult reputable sources such as government institutions, financial institutions, and economic research organizations.”

I don’t know if I’m going to fall for that though. I’m still getting a heavy HAL 9000 computer vibe from this whole technology.

SS Hey ChatGPT, can you tell me when the Fed will stop raising interest rates?

I’m sorry Sean, I’m afraid I can’t do that.

The U.S. national debt is over $32.6 trillion, and we are forecasting it to rise to $40 trillion by 2026, so the next question seems relevant.

SS How high can the U.S. national debt go before there is a crisis?

The U.S. national debt is a complex and multifaceted issue, and the point at which it may trigger a crisis is subjective and dependent on various factors. While it is challenging to pinpoint an exact threshold, a continuously rising national debt relative to the country’s GDP can have potential consequences. Here are a few key considerations:

1. Debt-to-GDP Ratio: The debt-to-GDP ratio is an important metric used to assess a country’s ability to manage its debt burden. If the debt grows faster than the economy, it can become increasingly burdensome. Historically, countries with debt-to-GDP ratios exceeding 100% have faced challenges in sustaining economic growth and managing their debt.

2. Investor Confidence: The willingness of investors to lend money to the government is crucial in determining if there will be a crisis. If investors become concerned about the sustainability of the debt or the ability of the government to make interest payments, they may demand higher interest rates or reduce their willingness to lend, making it more challenging and costly for the government to borrow.

3. Interest Rates: The level of interest rates is crucial in determining the affordability of servicing the debt. If interest rates rise significantly, it could increase the cost of debt payments, straining the government’s budget and potentially leading to fiscal challenges.

4. Economic Growth and Productivity: Strong economic growth and productivity can help mitigate the impact of a rising national debt by expanding the tax base and increasing government revenue. However, if economic growth falters or productivity declines, it can limit the government’s ability to manage its debt burden effectively.

It’s worth noting that the U.S. dollar’s status as the world’s reserve currency and the country’s ability to borrow in its own currency provide some advantages and flexibility. Nonetheless, a continuously increasing debt burden without a credible plan to address it can lead to fiscal imbalances, reduced investor confidence, and potential long-term economic challenges. Ultimately, maintaining a sustainable fiscal path, implementing prudent fiscal policies, promoting economic growth, and addressing long-term entitlement spending are essential to managing the national debt effectively and mitigating the risk of a crisis.

This is not a bad response, but it leaves out issues such as the intergenerational fairness of such debt or the political willingness to do anything to redress the problem.

I have a pretty good sense of humor, for an economist, and this is useful when speaking to noneconomists about the economic outlook and economic issues. But what about AI?

The last set of questions are meant to test machine learned humor as it relates to the economy.

SS Can you write a country song about high inflation in the U.S.?

(Verse 1) Well, the prices keep on rising, it’s a hard-hittin’ truth, Inflation’s got us reelin’, from our wallets to our boots, Gasoline and groceries, they’re all goin’ through the roof, This country’s singin’ the high inflation blues.

(Chorus) Oh, high inflation, why you gotta be so mean? Squeezin’ every dollar, turnin’ dreams into a stream, I’m workin’ all day, just to stay ahead of the game, But high inflation, you’re drivin’ us insane.

(Verse 2) I used to fill my tank without a second thought, But now I’m countin’ pennies for every mile I’ve bought, The cost of livin’ keeps on climbin’, it’s a battle fought, In this country singin’ the high inflation blues.

(Chorus) Oh, high inflation, why you gotta be so mean? Squeezin’ every dollar, turnin’ dreams into a stream, I’m workin’ all day, just to stay ahead of the game, But high inflation, you’re drivin’ us insane.

(Bridge) Well, the factories are strugglin’, the workers feel the strain, With prices risin’ faster than the pourin’ rain, We need a little relief from this economic pain, In this country singin’ the high inflation blues.

(Verse 3) From the corner store to Wall Street, it’s a fight we can’t ignore, We’re lookin’ for some answers, prayin’ for a better score, Holdin’ onto hope, as we face the cost of more, In this country singin’ the high inflation blues.

(Chorus) Oh, high inflation, why you gotta be so mean? Squeezin’ every dollar, turnin’ dreams into a stream, I’m workin’ all day, just to stay ahead of the game, But high inflation, you’re drivin’ us insane.

(Outro) We’ll keep on pushin’, through the ups and downs we’ll roam, Hoping for brighter days, when the prices find their home, Till then, we’ll stand together, singin’ this inflation song, In this country singin’ the high inflation blues.

I think Garth Brooks is safe for now. What about another musical genre?

SS Can you write a rap song about high inflation in the U.S.?

(Verse 1) Yo, listen up, let me drop some knowledge on the track, We’re talkin’ ‘bout high inflation, it’s a fact, Prices on the rise, gotta watch your stacks, In the land of the dollar, feelin’ the impact.

(Chorus) High inflation, it’s a situation, Squeezin’ wallets, causin’ frustration, Prices skyrocketin’, no exaggeration, Gotta navigate this economic equation.

(Verse 2) Gasoline pumpin’, prices keep on climbin’, Grocery store bills, man, they ain’t no jokin’, Dollar’s losing power, it’s steadily declinin’, Tryin’ to stretch that cash, but it keeps on shrinkin’.

(Pre-Chorus) It’s like a rollercoaster, ridin’ the tide, High inflation got us holdin’ on tight, But we won’t back down, we’ll keep the fight, Findin’ ways to cope, stayin’ sharp and wise.

(Chorus) High inflation, it’s a situation, Squeezin’ wallets, causin’ frustration, Prices skyrocketin’, no exaggeration, Gotta navigate this economic equation.

(Verse 3) Investors strategizin’, tryin’ to stay ahead, Hustlin’ every day, it’s the path we tread, Savin’ up and budgetin’, makin’ moves with care, In this game of numbers, we refuse to despair.

(Bridge) It’s a dance of supply and demand, Economic forces playin’ a hand, We need some stability, we need a plan, To tame this beast and take a stand.

(Chorus) High inflation, it’s a situation, Squeezin’ wallets, causin’ frustration, Prices skyrocketin’, no exaggeration, Gotta navigate this economic equation.

(Outro) So here we are, facin’ the challenge, United we stand, together we manage, Adaptin’ to the times, stayin’ resilient, High inflation won’t define our brilliance.

Dr.

Dre,

I think you are safe.

SS Can you tell me a dad joke about the Federal Reserve?

Sure, here’s a dad joke about the Federal Reserve: Why did the Federal Reserve bring a ladder to work?

Because they wanted to “adjust” the interest rates, one step at a time!

Appropriate level of corniness for a Fed themed Dad joke. Now for the ultimate test.

SS Why was Sky Mall the greatest magazine ever written?

Sky Mall was certainly a unique and entertaining magazine for many travelers. Here’s a lighthearted response:

Why was Sky Mall the greatest magazine ever written? Because it elevated window shopping to new heights! From inflatable neck pillows to pet strollers, it had something for every eccentric desire. Whether you needed a life-sized Bigfoot statue for your backyard or a self-stirring coffee mug, Sky Mall never failed to amuse and inspire with its quirky assortment. It made us all wonder, “Who needs practicality when you can have an inflatable hot tub for your tiny apartment?” So, let’s raise a glass (or an inflatable drink holder) to the beloved Sky Mall, where imagination took flight at 30,000 feet!

Not bad, AI, but I think I did it better.

No mention of the branding iron that allows you to monogram your steaks as you grill them? The glow-inthe-dark toilet seat? The combination carry-on bag/scooter that allows you to zip through the airport? The Roomba for your BBQ grill?

I think my job is safe. For now.

ANXIOUS INDEX Fear of Recession Still at a Level Historically Consistent with a Recession

The most recent release (2nd quarter of 2023) of the Survey of Professional Forecasters by the Federal Reserve Bank of Philadelphia states that the forecasters surveyed for the publication put a 45.16% chance that a decline in real GDP will occur in the 3rd quarter of 2023.

The Anxious Index

One-Quarter-Ahead Probability of Decline in Real GDP Quarterly, 1969:Q1 to 2023:Q3

One section of the Survey of Professional Forecasters asked panelists to estimate the probability that real GDP will decline in the quarter in which the survey is taken, as well as the probabilities of a decline in each of the following four quarters. The anxious index is the estimated probability of a decline in real GDP in the quarter after a survey is taken. In the survey taken in April for the 2nd quarter of 2023, the index stands at 45.16, meaning forecasters believe there is a 45.16% chance that real GDP will decline in the 3rd quarter of 2023. This is up slightly from 42.41% in the survey taken in the 1st quarter of 2023. This level for the anxious index is still historically consistent with the level that prevailed during previous recessions in the U.S.

The graph above plots the historical values of the anxious index, where the gray bars indicate periods of recession in the U.S. economy. The current level of the anxious index is more than 27 points higher than the average level during the previous economic recovery (17.99).

GDP OUTLOOK Economy to Slow in the Second Half of 2023. Recession? Definitely Maybe.

The National Bureau for Economic Research (NBER) declared on June 8, 2020, that the longest economic expansion in U.S. history enjoyed its final month in February 2020. This declaration meant that as of March, the U.S. economy was in recession. On July 19, 2021, the NBER declared that the recession had ended in April of 2020. This announcement meant that the deepest recession since the Great Depression was also the shortest recession in U.S. economic history (6 months was the previous record for the shortest recession.). It also confirmed that the economic lockdowns were the drivers of this horrible economic cycle.

Fiscal and monetary policy were unleashed in a historic manner to counter the toxic effect of the public health measures on the U.S. economy. While the combined policy effects were clearly not enough to offset the damage the lockdowns had done, they lessened the severity and length of the historic recession. The overreliance on fiscal stimulus, as the recovery progressed at a more than robust pace, turned out to be overkill. Multi-trillion-dollar deficits fueled a spending frenzy that continued for nearly three years after the recession ended. That spending was the spark that ignited inflation and ultimately sowed the seeds of a possible recession.

I believe that in the first half of 2022, the U.S. economy experienced a pasta bowl shaped recession. I also expect the next recession could arrive by the end of this year. Many economic indicators suggest that we are on the approach to another relatively short and shallow recession, one milder than the pasta bowl of 2022.

While the labor market showed little signs of the 2022 recession, the second pasta bowl recession will not be as innocuous when it comes to the labor market. I think we will see unemployment rising as 2023 progresses and this will continue into 2024 and 2025. Job growth will turn negative but not as sharply as was the case in the wake of the 2008-09 and 2020 recessions.

The reality of recessions in the U.S. is that they are determined based on the judgment of a small committee of economists, who may or may not be influenced by political cycles. There is no litmus test that can objectively determine when recessions start and end. The unusual nature of the economic cycles driven by COVID-19 policies make the determination of a recession a more complicated proposition.

Consumer Spending

Consumers have been ground down by two years of falling real wages, draining savings, and boosting their credit card debt.

U.S. consumers have been hit hard by high inflation. Even though wage and salary growth are the strongest they have been in years, the cost of living has eroded all those wage gains and then some. Since the second quarter of 2021, real median weekly wage and salary growth has been negative. This means that even though workers have more dollars in their paychecks, the amount of goods and services that they can purchase with these dollars has been declining for two years.

Consumer spending has been propped up by savings from the COVID era and by use of credit card debt. These patches to consumers’ budgets could only hold for so long, and we are expecting to see consumer spending give way to the erosion of real income in the second half of this year.

The headline rate of CPI inflation understated the impact that inflation has had on households because the biggest expenditures households make are for food, shelter, and transportation— all of which have had inflation rates much higher than the overall CPI. The recent slowing of the rate of inflation is helping to provide a floor that should keep consumer spending from falling too far, but the damage has already been done.

Inflation has hit households hard. 62.8% of consumer expenditures go to food, shelter, and transportation; and all three categories have seen outsized price increases over the past 20 months. Consumer confidence was at a 40-year low as of August 2022, but has now rebounded from those lows.

The public health policies aimed at slowing the spread of COVID-19 caused spending growth in 2020 to contract by 3.0%. Consumption spending growth slowed from 8.3% in 2021 to 2.7% in 2022. During 2023-2026, consumer spending growth is expected to average 1.6%. Consumer spending growth will be dampened by the recession to 1.8% in 2023 and 0.7% in 2024 before accelerating in the next two years to 1.6% and 2.3% in 2026.

Investment

The COVID-19 recession and the presidential election in 2020 created an atmosphere of high uncertainty in the economy. Uncertainty, the enemy of investment spending, caused businesses to pullback on investment that year.

Nonresidential fixed investment spending eased in 2019 to 3.6% from 6.5% in 2018. In 2020, investment spending contracted by 4.9%.

Spending on equipment and software turned negative in 2020 and contracted by 10.5%. In 2021, spending grew 10.3%—an outsized 20.8 percentage point swing. Average growth in this type of investment spending is expected to be -0.6% over the 2023-2026 timeframe, with the economic slowdown and higher interest rates weighing on these expenditures through 2026, but most heavily in 2024 and 2025.

Investment in aircraft is historically volatile and a single aircraft order from a major airline can move this figure by tens of billions of dollars. The problems Boeing faced with its 737 Max planes weighed heavily in 201819. This caused a sharp reversal of growth in 2019 to -41.6%. 2020 made matters initially and temporarily worse for the industry as air travel collapsed globally when the COVID-19 pandemic spread. But as things reopened in

2020, investment surged by 34.5%. That was followed by another sharp increase in 2021 as investment surged 29.0%.

This rebound in 2021 decelerated in 2022 as airlines faced labor shortages. However, aircraft purchases still grew by 16.3% that year. Over the next four years, spending on aircraft is expected to grow an average of 3.7%, with growth hitting 17.4% in 2023. Quarter-toquarter and even year-over-year volatility in this type of investment spending is the rule, not the exception.

The 2016 slowdown in overall investment spending also reflected the negative impact of oil prices falling by nearly two-thirds. Consumers enjoyed the low prices at the gasoline pump, but oil producers—shale and otherwise—cut back on investments as oil prices dropped below $40 per barrel early in 2016. The rig count in the U.S. hit a seventy-year low of 404 in response to plunging oil prices. In the middle of the COVID recession, an oil price war broke out and drove spot prices to below zero at one point. This price drop caused the U.S. rig count to further plummet to 282. Higher oil prices due in part to the strong economic recovery have pushed the current rig count to 664 which is 103 rigs fewer than a year ago. The Russian invasion of Ukraine temporarily pushed oil prices to record highs, and this historically would continue to drive the rig counts even higher, though the response has been muted under Biden’s administration anti-fossil fuel policies.

Over the past month, the price of oil has increased to $80 per barrel. This may boost investment spending in the near term, but the prospect of a slowing economy is a headwind for this type of investment spending.

In 2017, investment in mining and petroleum equipment growth hit 40.4% and came in at 27.8% for 2018, before declining by 0.3% in 2019, and plunging to -38.4% in 2020. Investment will average a 3.6% growth per year during 2023-2026 after growing 14.5% in 2022 and -1.6% in 2023. It will be hindered by the impacts of the green energy initiatives of the Biden administration, but rising prices in 202426 will support investment spending.

Business nonresidential structures investment growth decelerated to 2.3% in 2019 before contracting by 10.1% in 2020, again by 6.4% in 2021, and contracting for a third straight year by 6.6% in 2022. Nonresidential spending will continue to contract at an average rate of 1.6% during the four years of our forecast horizon.

Interest rates plummeted during the pandemic. The Federal Reserve cut short-term interest rates to near zero and kept them there for nearly two years. The interest rates on U.S. Treasury bonds fell to historic lows but have since risen significantly. Rising interest rates are not good for investment, but since the Fed has now switched gears to go into an aggressive inflationfighting mode and will likely have to keep interest rates elevated through 2024. This will be a persistent headwind for business investment spending.

Business spending on industrial equipment will shrink at an annual average rate of -1.2% from 2023-2026. Investment spending growth on computers and peripherals will average 3.6% during 2023-2026. Spending on communications equipment should expand at an average annual rate of 4.8% during the same four-year span, with spending in 2025 expanding at an 8.1% rate.

Residential fixed investment growth hit 10.7% in 2021. Growth will average -1.8% during 2023-2026, as higher prices combined with rising mortgage rates eroded demand and caused investment spending to contract 10.7% in 2022 and 12.0% in 2023.

We expect housing starts to decelerate in 2023 then remain steady over the following year before accelerating. After reaching nearly 1.6 million in 2021, starts will fall to 1.38 million in 2023 before leveling out for several years and hitting a level slightly below 1.30 million in 2026. Higher mortgage rates and high home prices are headwinds, as is the economic slowdown, and all three will continue to shape the residential sector for the next two years. The ongoing shortage of housing that is plaguing the sector in many parts of the country will provide solid support preventing starts from falling in a dramatic fashion.

Government Spending

Government budget management has become a series of continuing resolutions, COVID-19 stimulus packages, and spending made under the umbrella of a pandemic emergency declaration. This spending is devoid of any policy discussions or debates about priorities, problems, or objectives. Unsurprisingly, our public finances are adrift, and deficits climbed back to the $1 trillion mark in 2019 even before the torrent of spending spurred by the pandemic. This was all before public health measures plunged the economy into the deepest recession since the Great Depression, further worsening the fiscal outlook.

Federal government spending growth was 3.9% in 2019 before jumping to 6.2% in 2020. During the 2023-2026 period, federal government spending growth is going to be slightly negative, growing at an annual average pace of 1.1%. Over the same time frame, state and local governments will see spending growth at an average rate of 1.4%.

We are projecting deficits through 2026 that will consistently average nearly $1.85 trillion. The amount that the projected deficits will add to the national debt over the next four years will be more than $7.4 trillion, pushing the total national debt to more than $40 trillion and a debt-to-GDP ratio of 141%. With higher interest rates in the economy, the burden of servicing this debt will rise as well. Spending by the Biden administration (and Congress) will help push this debt to even higher levels than we are currently projecting if interest rates rise more quickly than anticipated. Slower-than-projected economic growth or a recession would also push projected deficits higher, though the possibility of faster-than-projected economic growth would help mitigate the growth of these deficits.

Currently, the national debt is over $32.6 trillion and rising. This represents a debt of nearly $253,686 per taxpayer and $97,468 per citizen. The unfunded liabilities of the U.S. are even more disturbing. These include Social Security, Medicare parts A, B, and D, and Federal debt held by the public and federal employee and veteran benefits, representing more than $192.5 trillion in liabilities, boiling down to more than $574,101 per citizen.1

Net Exports

COVID-19 created havoc in the global economy. International trade crumbled in the 2nd quarter of 2020. Real exports collapsed by 60.9% at an annual rate, while real imports plunged by 53.7%. But like the rest of the economy, the external sector came rushing back in the 3rd quarter of 2020. Real exports grew at an annual rate of 59.5% that quarter, with real imports growing at an 88.2% pace as consumer spending was reignited.

The U.S. dollar appreciated for five straight years against our major trading partners, including an outsized 15.7% appreciation in 2015. In 2016, this trend moderated; in 2017 and 2018, the dollar gave back some of these gains. However, after the Fed raised interest rates and the U.S. economy experienced faster growth relative to our trading partners, the dollar appreciated again in 2019 at a 3.5% pace before depreciating 1.1% in pandemic-addled 2020.

Beginning in the second half of 2021, the dollar began a significant appreciation that continued through the third quarter of 2022 and included a very large 21% appreciation in the second quarter of 2022, followed by another jump of 20% in the third quarter of that year. For the full year the dollar appreciated by 10.2% in 2022.

A stronger dollar boosts imports and reduces exports by making our goods and services more expensive to foreigners while at the same time making imported goods and services less expensive to U.S. consumers. This results in a worsening of the trade deficit, which is the difference between the dollar value of exports and the dollar value of imports.

However, the effects of currency changes take time to work on the actual quantity of trade flows, resulting in what is known as the J-curve effect on net exports. Because of this effect, an appreciation of the dollar initially decreases the trade deficit before eventually increasing it. Why? Importers and exporters do not enter contracts based on the total dollar value of the transaction, but rather the actual quantity of goods to be shipped (automobiles, flat-screen televisions, etc.). As the exchange rate varies in the short run, the values of these shipments and, thus, net exports vary as well. Over time, however, the quantities do adjust in response to the exchange-rate fluctuations, and this is what gives rise to the J-curve effect.

The Russia-Ukraine war, the ensuing sanctions, and rise in uncertainty impacted global trade, but Russia is a minor trading partner with the U.S. and the direct effects of any restriction in trade have been relatively small. This has not been the case for Europe.

Unemployment

The national headline unemployment rate (U-3) in June 2023 stood at 3.6%: down 11.2 percentage points from the April 2020 reading of 14.8%, which was the highest level since the Great Depression era. The labor force participation rate rose in June 2023 to 62.6% from the June 2022 rate of 62.2%.

The June jobs report fell short of expectations as growth in payroll jobs hit 209,000, when the expected growth of this figure had been 225,000. Payrolls have surpassed February 2020 levels, recovering all the jobs lost from a historic and self-inflicted recession.

The Bureau of Labor Statistics (BLS) produces alternative measures of labor market weakness, including the broadest measure of unemployment (U-6). U-6 accounts for discouraged workers (currently 310,000 workers), underemployed workers—working part-time but not by choice— (currently 4.19 million workers), and workers who are marginally attached to the labor force—those who have looked for work in the past 12 months, but are not currently looking, yet indicate a willingness to work (1.4 million workers). None of these 5.8 million-plus workers are accounted for in the February headline unemployment rate of 3.6%.

U-6 stands at 6.9% as of February 2023, down 5.9 points from the September 2020 level, and down 0.2 percentage points from the start of 2022. The current level of U-6 is on par with its 6.9% level in July 2019. U-6 was stuck in double digits for more than seven years. It had been in single digits for fifty-one consecutive months, beginning in December 2015 before surging during the lockdowns in April and May of 2020.

The spread between U-6 and U-3 measures of unemployment sits at 3.3 percentage points and is 4.1 points below the peak spread of 7.4 points that took place in September of 2011.