11 minute read

ANALYSIS

The US in no longer capable of recycling all its own domestic spent lead batteries. Yet battery manufacturers continue to get by with an international juggling act balancing supply and demand, writes Farid Ahmed, lead analyst for Wood Mackenzie.

The US lead industry — just about fit for purpose

Advertisement

Farid Ahmed, lead analyst for Wood Mackenzie The US is a major user of lead. Until overtaken by China in 2005, it had been the world’s leading consumer for as long as accurate data has been kept. What might come as a surprise is that US consumption has only increased by under 1% a year over the past 30 years. Compare that to China’s average of over 10% a year and India’s 9% over the same period.

Over the coming 20 years, US lead demand is essentially flat and India will overtake it before the end of this decade. But at an average of 1.6 million tonnes per year, American consumption remains significant for decades to come.

The US was the world’s largest lead producer until surpassed by China around 20 years ago. It will now drop to third place behind India in just a few years. Since 1990, US smelting capacity has fallen dramatically. It no longer has any primary smelting capability following closure of the Herculaneum plant in 2013.

This is despite annual production of over 250kt per year of lead in concentrates coming out of US mines.

Three other primary smelters have closed since 1990 — Boss, Omaha and Glover. This has collectively removed well over a third of a million tonnes of refined lead output from US production.

The permanent shuttering of US secondary smelters such as Frisco, Vernon and, in March 2021, Florence added another quarter of a million tonnes to this figure. In all, the cumulative drop in total US lead smelting capacity has been well over half a million tonnes in this period.

US supply-demand deficit

To understand the consequences of this reduced capability, one needs to examine how this stacks up against US demand for refined lead. The first chart shows the answer is: “not very well”. The US is deficient in production by one-third of its requirement and that situation will get worse with the loss of the Florence secondary plant.

The considerable supply-demand gap necessitates huge imports of lead into the US. These come primarily from Canada, Mexico and Korea, but also India, Kazakhstan, Australia, Russia, Peru and others. US imports have increased from a 225kt annual average in the 1990s to over half a million tonnes per year since Herculaneum shut in 2013.

Our forecasts for future lead demand and remaining US smelter capacity confirm this deficit will remain at, or above, that level unless production expands.

CHART 1 above (smelter closes) Chart 1: US closes its last primary smelters; lost output over half a million tonnes as more secondaries shut

CHART 2 Chart 2: Supply-demand gap needs more imported lead in future without smelter capacity expansion

Nearly 90% of US lead consumption is for making batteries and close to 100% of these are recycled. A good proportion of the remaining non-battery lead uses are also recyclable.

Why is it that, although demand is basically flat, the US still needs to import about one-third of its refined lead? Isn’t over 90% of its consumption recyclable? The answer is “yes” — the vast majority of lead consumed in the US is recycled. But, crucially, it is not necessarily recycled in the US.

Lead losses from the US supply chain

When we talk about ‘lead consumption’, it means where the lead is made into a product such as a battery, radiation shielding bricks, lead sheet or ammunition. It’s not where that product is subsequently used.

Thus, if refined lead is made into a battery in the US, and that battery is installed in a new vehicle in a Canadian car plant, and that vehicle is then exported to Europe, the consumption of that lead occurs in the US — not in Canada, not in Europe.

However, at the end of its life, that battery will be scrapped and recycled at a European smelter. It will probably then be manufactured back into a new battery at a European battery maker. The US supply chain will have lost the lead content of that car battery.

The US is a powerhouse of vehicle production. But, on average over the past decade, exports account for 3.3 million units of the typical 10 million annual output. Most of these would be factory-fitted with an Americanmade battery. So, again, that’s lead consumed in the US, but then lost from the US supply chain through vehicle exports.

Added to that are annual exports of some 15 million automotive batteries not fitted in a vehicle. America is also a leading producer of industrial batteries for motive power, standby power and energy storage. The recognized quality of these products generates a high level of export demand which, again, means the US supply chain loses lead.

The US actually imports more finished batteries than it exports.

Shipping containers full of lead batteries arrive every day at US ports from China, Korea and Vietnam or across the border from Mexico. The majority of these are automotive replacement batteries. Increasingly now, these also include batteries to be white-labelled as the product of a US brand.

It is quite common for ‘big brand’ battery makers in North America and Europe to buy in third party batteries from low-cost foreign producers when it is uneconomical for them to manufacture these low-volume or low-margin battery types themselves.

Scrap battery exports

Where America is haemorrhaging lead from its domestic market is in scrap batteries. As US refined lead output now comes entirely from recycling, the secondary industry relies on scrap batteries for the overwhelming majority of its raw materials.

The net trade in scrap deprives American smelters of their principal feedstock with used lead batteries leaving the country in large volumes.

The apparent loss of secondary raw material shown in the official trade numbers almost certainly falls a good way short of the reality. There are gaping inconsistencies between volumes reported as US exports under recognized HS codes for scrap lead batteries and the mirrored volumes reported by recipient countries as US imports.

The truth is that the two sets of numbers purporting to be the same thing can’t both be right, but they can both be wrong.

A US lead industry campaign is gathering momentum to stem this loss. It urges US authorities to block exports of this hazardous waste to destinations where safe recycling matching US standards cannot be assured.

The campaigners also point out that when exporters are active in the US market, buying used batteries to ship to Asia, the price of scrap will typically increase by 5%-10%, especially in regions nearer to the Eastern and Western Seaboards.

That hits margins at American smelters. Campaigners argue that not only is the US losing control over the safe recycling of a hazardous waste by exporting to countries with lower environmental and safety standards, but also that this increases the price and decreases the availability of this essential raw material to its domestic industry.

This, in turn, harms the competitiveness of the US lead and battery industries domestically against imports, and internationally in a competitive global marketplace.

What if America didn’t export scrap batteries? Wouldn’t it be much better if the US could keep all its scrap batteries, instead of them disappearing across the border to Mexico, or being stuffed into containers destined for Korea or India?

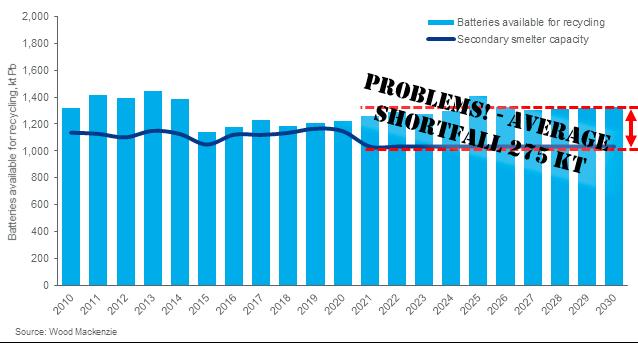

Chart 3: US recycling capacity can’t cope without exporting scrap batteries. Source: Wood Mackenzie

Chart 3 CAPACITY EXPANSION — CONFIDENCE, COSTS AND CONTROLS

Increasing capacity to match this average shortfall of 275kt per year over the next decade is not an easy route. Obtaining permits to expand an existing plant will likely meet with objections and obstructions at every step.

Building a brand-new smelter will face even more hostility than when it was last achieved with the Florence smelter a decade ago. Media campaigns can readily harness and manipulate the public mood and turn it against the lead industry.

Do lead smelters want to build more capacity following the net loss of recent decades? Putting the difficulties in building a new smelter to one side, do US lead producers have the appetite and financial incentive to build new capacity with a flat demand outlook and obstacles to operating plants?

Confidence to build new capacity will only come if there are controls in place to curtail the current level of exports. Otherwise, adding capacity will simply tighten the scrap market and drive prices higher.

Export demand from foreign smelters will not go away without legislation to significantly reduce the outflow of scrap. If all of this just serves to increase the price of making American batteries, what’s to stop US battery producers from importing more units to white-label and carmakers buying more foreign batteries to fit as original equipment?

The US lead and battery business wants to become more self-sufficient over this strategic resource to better control prices, improve competitiveness and improve the environmental performance of lead recycling at a global level.

This will only be achieved by finding some way to increase its ability to recycle lead together with export controls on scrap.

It will also need to consider alternatives to the traditional pyrometallurgical route. Some promising new technologies now in development use electrochemical processes to virtually eliminate emissions from the smelting process, leaving just the much lower emissions from refining.

This should make permitting and licensing much easier. It’s in the global lead industry’s self-interest to bring these processes from the laboratory to full commercial scale as quickly as possible.

In the meantime, it must continue striving to minimize emissions from traditional smelting, improving process technologies and investing in better controls. Until then, the US industry is stuck with the shortfall in its smelting capacity — and all the problems that brings.

US lead recyclers would then have an abundant supply of raw material to drive scrap prices lower, thereby improving operating margins and profitability.

We know that America’s demand for refined lead can’t be fully satisfied by current US lead smelting capacity. But the stark reality is that it is also insufficient to process all the available used batteries if none were lost from its domestic market.

In other words, the US has to export scrap because it can’t cope with the volume. That’s not the message the lead industry wants to hear as it campaigns to staunch the outflow of scrap. Expensive imports of refined lead must then replace that loss of precious metal from the domestic market.

We forecast an average shortfall of 275kt per year over the next decade between the volume of batteries potentially available to US recyclers and their capacity to process it. One solution to this problem is to just accept the US is going to lose a significant amount of raw material, pushing up prices and squeezing margins.

A new universe of lead beckons

One of the most talked about features of recent BCI meetings has been the Sally Breidegam Miksiewicz Innovation Award. This was set up in 2016, as a tribute to East Penn’s CEO following her untimely death in June 2014.

The award celebrates innovation in equipment, processes, services and products that advance the lead battery industry.

The range of innovations set up as candidates for the award has been startling.

Some have been as simple as a better design shape for a marine battery; others have embraced the latest technological advances in our understanding of the lead battery.

Some of the nominations have been breakthroughs in the laboratory but struggled to be commercialized. And yet others — think of advances in EFBs — have been quickly embraced as a new standard in an emerging marketplace that continues to grow exponentially.

But be they large or small, these innovations matter.

For the last decade a tonne of investment has been flung at developing better lithium batteries while lead research has been side-lined.

The revamp of the ALABC and its replacement by the Consortium for Battery Innovation is putting the lead battery back in the spotlight.

Clear advances are on their way and credit must go to CBI for pulling it all together.

That said credit must also go to a generation of lead researchers that have remained in the background — think RSR, Hammond, East Penn, Daramic and many others — that continue to shape the lead battery industry.