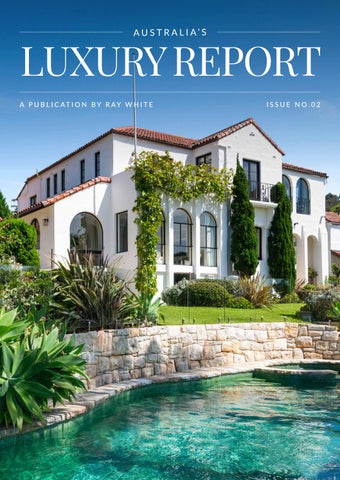

LUXURY REPORT

Introduction

Australia’s luxury property landscape in 2025 presents a fascinating study of wealth creation, lifestyle preferences, and architectural innovation. From the harbourside mansions of Sydney to the coastal retreats of Queensland and the emerging premium markets of Perth, the definition of luxury real estate continues to evolve in response to changing demographics, technology, and consumer values.

In this second edition of our Luxury Report, Ray White brings together comprehensive analysis from our Economics team to examine not just what defines luxury today, but also who is buying it, how it’s being designed, and where the growth markets are emerging across Australia.

Our Chief Economist Nerida Conisbee provides detailed economic analysis of the architectural and landscape features that characterise Australia’s most expensive homes, while our Head of Research Vanessa Rader explores the fascinating intersection between high-end retail and premium real estate, as well as the transformative impact of wellness features on luxury property values. Our Senior Data Analyst Atom Go Tian offers valuable insights into who’s buying luxury properties, how we define luxury across

different markets, and which luxury growth markets are showing the strongest momentum.

This report also examines parallel luxury markets, particularly the marine industry, which offers valuable insights into wealth distribution and consumption patterns among Australia’s affluent. These patterns often mirror or even anticipate trends we later see in premium real estate.

As Australia’s largest real estate group, with an unrivalled presence in the luxury segment across every state and territory, Ray White is uniquely positioned to provide this comprehensive analysis of the premium property market. As our group markets three times more residential property across Australia than the next largest group, and is further supported by our dedicated Marine and Commercial divisions, we offer our clients unparalleled insights into luxury real estate trends nationwide.

We trust this report will serve as a valuable resource for property owners, investors, developers, and industry professionals seeking to understand the evolving dynamics of Australia’s luxury property market in 2025.

DAN WHITE MANAGING DIRECTOR, RAY WHITE GROUP

Executive summary

Our second edition of the Ray White Luxury Report offers a comprehensive analysis of Australia's premium property market in 2025. Through detailed examination of high-value transactions, architectural trends, and demographic shifts, we provide insights into the evolving nature of luxury real estate across the country.

The price tag for luxury homes across Australia now starts at $2.52 million - up 72 per cent from ten years ago - but what counts as "luxury" varies significantly depending on location. Sydney remains Australia's most expensive market, where luxury begins at $4 million. Surprisingly, Gold Coast has now taken second place at $2.6 million, pushing ahead of Melbourne's $2.49 million entry point.

South East Queensland has become the clear success story in Australia's high-end property market. Gold Coast luxury home prices have more than doubled since 2015, while Sunshine Coast has grown faster than any other luxury market in the country. Brisbane has also transformed dramatically, with luxury properties jumping from under $1 million to over $2 million in the past decade. These three Queensland regions now represent the fastest-growing luxury markets in Australia.

Our analysis of the year's top 20 sales reveals today's luxury purchasers are predominantly self-made entrepreneurs from diverse sectors including

e-commerce, property development, financial services, fashion, and technology. While buyers in their late 40s to 50s continue to form the core market, we're witnessing increasing participation from millennial entrepreneurs, particularly those who have built wealth through digital businesses.

Perth demonstrates exceptional momentum with all three of its luxury suburbs ranking in the top 10 nationwide for price growth, led by NedlandsDalkeith-Crawley at 8.8 per cent. Meanwhile, Melbourne's luxury market shows signs of cooling, with several premium suburbs experiencing price declines - a stark contrast to the heated Queensland market.

The architectural and landscape features of Australia's most expensive homes reveal sophisticated investment priorities, with wellness facilities, sustainable elements, and indoor-outdoor integration now considered essential rather than optional. Properties with comprehensive wellness features command price premiums of 10-25 per cent, reflecting a fundamental shift in what constitutes luxury in today's market.

As we navigate 2025, these evolving patterns suggest a more nuanced approach to luxury property investment, with opportunities emerging beyond traditionally dominant markets and new definitions of premium living reshaping Australia's high-end real estate landscape.

What is LUXURY?

Throughout Australia, luxury real estate represents far more than just a price pointit embodies an evolving standard of quality, design, and exclusivity that continues to redefine itself across different markets.

Luxury is an evolving standard composed of quality, design, and exclusivity. What qualifies as luxury today may become commonplace tomorrow as tastes and markets shift. More than just a price point, luxury represents the pinnacle of craftsmanship, attention to detail, and scarcity within a market. It varies dramatically by location; what’s considered standard in Sydney might be exceptional elsewhere in Australia.

True luxury in real estate combines premium materials, architectural distinction, prime location, and limited availability. It reflects both the financial threshold of the top five per cent of properties in a market and the intangible qualities that make a home exceptional. As our data reveals, the concept of luxury continues to transform across Australia’s diverse regions, shaped by changing demographics, wealth distribution, and lifestyle preferences.

From a national perspective, luxury properties in Australia now command prices exceeding $2.52 million, representing a 72 per cent increase from $1.49 million a decade ago.

ATOM GO TIAN

RAY WHITE SENIOR DATA ANALYST

However, standards for luxury vary significantly across major cities, with Sydney maintaining the highest threshold at $4 million. What qualifies as luxury elsewhere in Australia often sits closer to Sydney’s median price range.

The most dramatic shifts have occurred in South East Queensland’s markets over recent years. Gold Coast luxury house

$2.6 million, now exceeding Melbourne. Sunshine Coast has shown the highest growth rate among all major markets, while Brisbane has seen luxury thresholds jump from under $1 million to over $2 million. Together, these three Queensland regions represent Australia’s fastest-growing luxury real estate sector.

In contrast, Melbourne’s luxury house prices grew by just 47 per cent over ten years, from $1.6 million to $2.49 million,

LUXURY HOUSE

PRICE GROWTH IN AUSTRALIA’S MAJOR CITIES

House prices in the 95th percentile for March 2025 v 2015

SOURCE: NEOVAL

and notably decreased over the past year - the only major city to experience such a decline. This cooling trend stands in stark contrast to the heated Queensland market.

Looking to the west, Perth shows exceptional recent potential with a 10 per cent increase in luxury house prices over the past year. Growth remained muted during the first half of the decade but has accelerated dramatically in recent years. Similarly, Adelaide has demonstrated strong momentum with six per cent growth in the past year and a doubling of prices over the decade. Adelaide’s luxury threshold could

reach $2 million before Canberra, which has experienced more moderate growth. Darwin remains the least developed luxury market, with high-end properties still priced below $1 million.

It’s worth noting that only two of Australia’s nine major cities, Sydney and Gold Coast, maintain luxury house prices above the national threshold of $2.5 million, highlighting how the luxury market remains concentrated in select locations. This concentration underscores the exclusivity that defines true luxury.

From a national perspective, luxury properties in Australia now command prices exceeding $2.52 million, representing a 72 per cent increase from $1.49 million a decade ago.

Turning to apartments, luxury units in Australia start at $1.6 million, a 52 per cent increase from the $1 million threshold in 2015.

Compared to houses, the luxury unit market shows more restrained growth outside of Queensland’s coastal regions. Sydney leads with luxury units starting at $2.2 million, while Gold Coast and Sunshine Coast are the only other cities

with luxury unit thresholds exceeding $2 million. Given the explosive growth in these Queensland coastal markets, it’s not difficult to imagine a future where South East Queensland becomes Australia’s premier luxury apartment destination.

Melbourne’s luxury unit market has shown sluggish 38 per cent growth over ten years and recently experienced price decreases, mirroring the trend in its house

market. Brisbane, while lagging behind its Queensland coastal neighbours, shows promising recent growth at 7.5 per cent annually. Perth leads in one-year unit price growth at 10.4 per cent, though its long-term performance has been relatively weak compared to eastern markets.

Canberra’s luxury unit market has grown to $1.15 million, up 53 per cent over the decade, though recent growth has

LUXURY UNIT PRICE GROWTH IN AUSTRALIA’S MAJOR CITIES

Unit prices in the 95th percentile for March 2025 v 2015

SYDNEY

BRISBANE

PERTH

GOLD COAST CANBERRA

MELBOURNE ADELAIDE

SUNSHINE COAST

DARWIN

AUSTRALIA

SOURCE: NEOVAL

stalled at just 0.1 per cent. Adelaide’s luxury units have reached the same $1.15 million mark with stronger momentum, showing 59 per cent ten-year growth and a healthy eight per cent rise in the past year. Darwin remains an outlier as the only city where luxury unit prices have fallen over the decade, dropping 11 per cent to $688,000, with only minimal recovery of 1.1 per cent last year.

Luxury units in Australia start at $1.6 million, a 52 per cent increase from the $1 million threshold in 2015.

Who is BUYING?

ATOM GO TIAN

RAY WHITE SENIOR DATA ANALYST

In the rarefied air of Australia’s ultra-luxury property market, a staggering $663 million changed hands across just 20 transactions, revealing not only where Australia’s wealthiest choose to live, but also who they are and how their wealth was created.

Eastern Sydney continues to be the place to be, with the Double Bay-Bellevue Hill and Rose Bay-Vaucluse-Watsons Bay enclaves accounting for more than half of all top transactions. Bellevue Hill alone appears five times on the list, while Vaucluse claims four spots. Beyond Sydney’s harbour views, Melbourne’s old-money suburbs of Toorak and Brighton each secured positions, while lifestyle destinations like Noosa Heads, Byron Bay, and Portsea also featured prominently.

The crown jewel of these transactions stands as “Alcooringa,” a Spanish Mission-

style residence perched majestically on Victoria Road in Bellevue Hill. This architectural masterpiece commanded an eye-watering $80 million; a figure that towers over even its closest competitor by $30 million. The seller was Australian food blogger and mansion flipper Stephanie Conley-Buhre whose investment acumen proved spectacular, having purchased the property just three years prior for $30 million. Interestingly, Conley-Buhre appears elsewhere on the list as a buyer, after securing the third most expensive property for $43.5 million.

$663 million changed hands across just 20 transactions

Perhaps most revealing is the dramatic shift in buyer demographics. Corporate executives, once the mainstay of premium property purchases, now represent the minority. Today’s ultra-luxury buyers emerge from a diverse entrepreneurial spectrum including e-commerce founders, property developers, financial services entrepreneurs, aged care provider founders, fashion label designers, retail business owners, mining technology magnates, and restaurateurs. Of the twenty buyers, only four held traditional employment positions; two from healthcare (including pharmaceuticals and medical devices), one from finance and investment, and one from food and beverage.

While buyers aged in their late 40s to 50s dominate the market, millennials are making notable inroads. The story of Shadi Kord, founder of fashion boutique MESHKI, and her husband Bayan Fanaeyan, of men’s fashion label LÈ BAUS, exemplifies this trend. The couple upgraded from a $2.55 million Double Bay apartment to a designer Bellevue Hill residence for $22.75 million. This pattern repeats with other online fashion entrepreneurs like Daniel and Georgia Contos of White Fox, who have similarly leveraged social media influence into substantial property portfolios.

The international dimension adds another layer of complexity to this exclusive market. Five of the twenty transactions involved expat buyers based primarily in Singapore and China, signaling Australia’s enduring appeal as both an investment destination and potential future home for the globallymobile wealthy. The most intriguing figure remains the purchaser of “Alcooringa” itself, described in records only as an “overseasbased expat,” highlighting the sometimes opaque nature of transactions at this level.

Expensive homes are changing hands in new ways. Today’s ultra-luxury property buyers are primarily self-made business owners, especially those who built digital and tech companies, rather than corporate executives who once dominated this market. The wealth behind these purchases now comes from a much wider range of industries, with online businesses and technology ventures leading the way. Perhaps most notably, there’s been a significant drop in buyers using inherited or family money, as first-generation entrepreneurs who built their fortunes from scratch are now the ones acquiring these multi-million dollar properties. This shift toward self-made wealth marks a fundamental change in who can afford Australia’s most exclusive neighbourhoods.

Economic analysis of ARCHITECTURAL FEATURES IN AUSTRALIA’S 20 MOST EXPENSIVE HOMES

NERIDA CONISBEE RAY WHITE CHIEF ECONOMIST

What distinguishes Australia’s most exceptional homes? You could ask an architect, who would offer valuable insights on design principles and spatial innovation. Or you could approach it like an economist with data and a spreadsheet, which is precisely what we’ve done, bringing a slightly different perspective.

To do this analysis, we examined the 20 highest-priced properties sold in Australia over the past 12 months using visual and data analytics. This review identified seven key architectural elements that define today’s premium residences.

Key architectural findings

1.

INDOOR-OUTDOOR INTEGRATION

(75 per cent prevalence)

High-end disappearing glass wall systems typically require substantial six to seven-figure investments, representing significant capital allocation decisions. In properties with premium views, these systems deliver something that justifies their considerable cost. One Vaucluse property featured an extensive system spanning several metres, demonstrating

3. MULTI-LEVEL FUNCTIONALITY

(90 per cent prevalence)

Looking at how vertical space is used in luxury homes reveals interesting insights about value creation. While average home buyers think in terms of price per square metre, the luxury market thinks about volume, transforming basement levels into premium lifestyle spaces (home theatres, gyms, wellness areas) that generate substantial additional value.

the importance of planning for view maximisation to boost value in waterfront locations.

The economics here are straightforward: when a property commands a premium price primarily for its location and views, the value of a seamless vista far exceeds implementation costs.

2. MATERIAL CONTRAST AND LAYERING

(85 per cent prevalence)

The mixing of premium materials creates sophisticated visual impact while driving significant price premiums. Our data analysis reveals consistent investment in rare materials, which are seen as a marker of quality in the luxury space. One Point Piper residence featured bathroom walls made from single slabs of Calacatta Viola

marble, a costly premium material, paired with custom-milled Tasmanian Blackwood.

These material combinations signify quality, allowing properties to command substantially higher per-square-metre valuations compared to similar properties with standard materials.

One Bellevue Hill property featured a five-level residence with an entire luxury wellness complex beneath the main living areas, effectively increasing the property’s usable floor area by 42 per cent within the same land footprint. This represents an excellent investment opportunity; converting traditionally lower-valued space into areas that approach the per-squaremetre value of above-ground living spaces.

5. CLIMATE-RESPONSIVE DESIGN

(80 per cent prevalence)

Climate-responsive design elements represent both environmental consciousness and comfort optimisation. Strategic shading, adjustable facades, and cross-ventilation features require substantial upfront investment but deliver impressive long-term efficiency gains and enhanced living environments.

A Mosman property featured an automated louver system that adjusts throughout the

4. ARCHITECTURAL FLEXIBILITY

(65 per cent prevalence)

Adaptable spaces reflect the evolving needs of sophisticated households while delivering long-term value through future-proofing. Premium properties with separate wings that function independently while connected to main living areas provide versatility that appeals to discerning buyers.

A forward-thinking Double Bay residence included what an architect would call

“functional elasticity”, spaces that could expand or contract based on needs without major renovation. This approach represents a calculated investment in long-term use, significantly improving resale potential by accommodating everything from multi-generational living to work-from-home arrangements.

day based on sun position, wind speed, and temperature, with an upfront cost in the mid-six figures. The resulting energy efficiency reduced operating costs by approximately two-thirds compared to conventional climate control systems. This demonstrates how buyers are increasingly factoring lifecycle costs into purchase decisions, recognising operational efficiency as a significant value component.

6. CURVED ARCHITECTURAL ELEMENTS

(60 per cent prevalence)

Curved architectural elements reveal an appreciation for design artistry in luxury homes. Curved walls, arched doorways, and organic shapes typically increase construction costs by about a third to nearly half compared to straight-line equivalents, yet remain prevalent in premium properties due to their distinctive visual impact.

One particularly impressive Rose Bay home featured a spiral staircase enclosed in a

7. INTERIOR LIFESTYLE AMENITIES

(100 per cent prevalence)

Premium interior amenities enhance the living experience in Australia’s finest homes. When home theatres rival commercial cinemas and wellness areas outshine exclusive spas, these residences provide unprecedented convenience and privacy value.

These specialised rooms from professionalgrade home theatres to comprehensive

wellness suites with saunas, steam rooms, and treatment areas represent thoughtful investments in creating complete living environments. The universal presence of these features across all analysed properties indicates strong market consensus on their value contribution, making them essential components for properties competing in this market segment.

curved glass wall, representing a sevenfigure investment. While this might seem excessive, cost-benefit analysis indicates these investments are economically rational when they establish unique property characteristics that reduce direct market comparisons and create memorable architectural experiences that drive premium pricing.

Economic analysis of LANDSCAPE FEATURES IN AUSTRALIA’S 20 MOST EXPENSIVE HOMES

NERIDA CONISBEE RAY WHITE CHIEF ECONOMIST

Australia’s most expensive homes reveal as much about their owners through what’s missing in their landscapes as through what’s included. While these properties feature sophisticated swimming pools, formal gardens, and elaborate privacy solutions, they notably lack elements like flying foxes (zip lines), adventure playgrounds, or recreational areas designed for children and teenagers.

This absence reflects the demographic profile of ultra-wealthy property purchasers in Australia, who have

traditionally tended to be older. Their outdoor spaces function primarily as extensions of adult-oriented indoor living - prioritising sophisticated entertainment zones, visual impact, and privacy rather than diverse family recreational areas.

For this analysis, we examined the outdoor spaces of the 20 highest-priced properties sold in Australia over the past 12 months. This review identified eight key landscape features that characterise premium properties.

Key landscape findings

1. ARCHITECTURAL SWIMMING POOLS

(80 per cent prevalence)

2. SOPHISTICATED PRIVACY SOLUTIONS

(95 per cent prevalence)

3. CLIMATE-ADAPTIVE FORMAL GARDENS

(75 per cent prevalence)

The economic analysis of garden design reveals fascinating adaptations of European formal aesthetics to Australian conditions. Premium properties consistently feature structured garden rooms and formal layouts executed with native and Mediterranean plant species selected for drought tolerance, creating a balance between traditional luxury garden aesthetics and practical environmental considerations.

These formal gardens represent substantial ongoing investments, with annual maintenance costs often exceeding six figures. However, this spending pattern indicates that established gardens with mature elements create significant competitive advantages in the luxury market.

Swimming pools in premium properties are no longer just recreational features but architectural statements requiring substantial six-figure investments. The prevalence of infinity edges, glass walls, and dramatic lighting systems reflects calculated decisions about property differentiation and view maximisation. One Palm Beach property featured a cantilevered pool extending toward the ocean horizon, seemingly floating in space while creating a visual connection between built and natural environments.

The economics are compelling: while a standard pool might add marginal value to an average home, an architecturally integrated water feature in a premium property creates a multiplier effect, enhancing both the immediate living experience and the property’s market positioning. Our analysis shows these distinctive water features typically deliver value well beyond their implementation costs when thoughtfully integrated into the overall design concept.

Avoiding prying eyes through strategic landscaping represents one of the most consistent investments across luxury properties. Rather than utilitarian fencing, premium properties employ layered approaches combining mature specimen trees, architectural hedging, and topographic modifications to create security without visual barriers.

One Point Piper property used mature tree transplantation and green wall installations to create complete privacy from neighbouring properties while maintaining harbour views. The prevalence of these sophisticated screening solutions demonstrates their perceived value in the luxury market, where privacy combined with outlook represents a premium combination that significantly enhances property valuation.

4. MULTI-FUNCTIONAL OUTDOOR ENTERTAINMENT ZONES

(85 per cent prevalence)

Luxury properties increasingly feature comprehensive outdoor living environments that function as extensions of interior spaces. These areas include fully-equipped outdoor kitchens, weatherprotected dining spaces, and integrated audiovisual systems. The most exceptional properties create seamless transitions between indoor and outdoor environments

while maintaining consistent design language and material quality.

From an investment perspective, these outdoor entertainment zones effectively increase a property’s usable living space at a lower per-square-metre cost than interior expansion.

5. SUSTAINABLE LUXURY FEATURES

(50 per cent prevalence)

Half of the analysed properties featured significant sustainable landscape elements, indicating a growing value proposition for environmental features in the premium market. Advanced rainwater harvesting systems, solar arrays integrated into architectural elements, and comprehensive native plantings represent substantial investments that deliver both practical benefits and market differentiation.

6. WATERFRONT INTEGRATION STRATEGIES

(55 per cent prevalence)

For properties with water frontage, specialised landscape elements that mediate between built and natural environments were popular. Private beaches, custom boating facilities, and engineered seawalls represent substantial investments that directly enhance lifestyle utility and property distinctiveness.

One Palm Beach property featured a private beach, along with a customdesigned boathouse that doubled as a selfcontained guest pavilion. These waterfront integration elements can require a sevenfigure investment.

7. STRATEGIC LIGHTING AS DESIGN ELEMENT

(80 per cent prevalence)

Landscape lighting in premium properties transcends simple illumination and becomes sophisticated architectural elements. Computer-modelled lighting systems highlighting specimen trees, water features, and architectural elements represent substantial technical investments. These systems create dramatic nighttime environments that effectively double the property’s visual appeal by creating entirely different day and night experiences.

One Rose Bay property included timers and environmental sensors, creating programmable lighting scenes that responded to seasons and weather conditions. While representing a significant capital allocation, these systems create distinctive nighttime environments that substantially extend usable outdoor time and enhance overall property presence.

A Mosman property incorporated a water management system that retained most rainfall on-site while supporting extensive gardens. This investment created both operational efficiency and resilience against water restrictions, positioning the property advantageously in a market increasingly concerned with sustainability and selfsufficiency.

8. TENNIS COURTS

(30 per cent prevalence)

Interestingly, our analysis revealed relatively low prevalence of dedicated recreational facilities beyond swimming pools. Only 30 per cent of properties featured tennis courts, reflecting important demographic insights about the luxury property market.

The limited presence of these recreational elements likely reflects the demographic profile of ultra-wealthy property purchasers, who tend to be older with adult children. This pattern indicates a preference for entertainment spaces suited to mature social interaction rather than family-oriented recreational facilities. Properties featuring tennis courts typically marketed them as part of wellness programs rather than family recreation, reflecting buyer priorities focused on adult lifestyle rather than children’s activities.

Luxury living: THE INTERSECTION OF HIGH-END RETAIL AND PREMIUM REAL ESTATE IN AUSTRALIA

VANESSA RADER RAY WHITE GROUP HEAD OF RESEARCH

Australia’s luxury landscape is experiencing a notable transformation in 2025, with evolving patterns of elite consumption reshaping both the high-end retail sector and premium property markets. As the luxury retail market reaches $7.7 billion, with 643 businesses operating across the country, clear patterns are emerging that signal opportunities and considerations for Australia’s premium property sector.

The Australian luxury retail market has demonstrated impressive resilience, growing at a consistent annual rate of 3.8 per cent

between 2020 and 2025 despite global economic challenges. This growth trajectory is expected to continue over the next five years, indicating sustained demand for premium products and experiences among Australia’s affluent consumers.

This upward trend presents a stark contrast to international markets like the United States, where luxury spending declined for ten consecutive quarters before showing early signs of recovery in 2025. Australia’s comparatively stable luxury retail environment suggests a more resilient high-

net-worth consumer base, creating fertile ground for both retail and residential luxury developments.

Australia’s luxury retail market reaches $7.7 billion with 643 businesses

Key players shaping Australia’s luxury landscape

Australia’s luxury retail market features a moderate but increasing level of competition, dominated by international powerhouses including Louis Vuitton Australia, Richemont Australia, and Hermès Australia. Louis Vuitton Australia currently holds the largest market share, reflecting global trends where established heritage brands maintain significant influence despite the emergence of new luxury concepts.

The concentration of luxury retail in specific urban corridors, particularly in Sydney and Melbourne, creates natural synergies with premium residential property markets. Proximity to these high-end retail clusters has become an increasingly important consideration for luxury property buyers, creating value uplift for residential developments in these precincts.

BEYOND BORDERS: AUSTRALIA’S RELATIVE INSULATION

Unlike some international luxury markets, Australia’s luxury retail sector remains relatively insulated from trade tensions, with both import and export tariffs having minimal impact on industry revenue. This stability provides additional security for the luxury ecosystem, including adjacent markets like premium residential property.

The number of luxury retail businesses in Australia has grown at a compound annual rate of 4.8 per cent between 2020 and

2025, outpacing the revenue growth rate and indicating increasing fragmentation and specialisation within the market. This trend toward more diverse and tailored luxury offerings mirrors developments in the residential property sector, where bespoke, highly customised developments increasingly command premium prices.

The number of luxury retail businesses in Australia has grown at a compound annual rate of 4.8 per cent between 2020 and 2025.

Several key patterns emerging in Australia’s luxury retail sector have direct implications for the premium residential market:

1. Experience-led consumption

Just as luxury retailers increasingly focus on creating memorable in-store experiences rather than simply selling products, successful premium residential developments are emphasising lifestyle offerings beyond the physical dwelling. Properties that incorporate exceptional design, wellness amenities, and service elements are commanding significant premiums in the current market.

2. The rise of bespoke craftsmanship

Australian luxury consumers are demonstrating growing appreciation for craftsmanship and materiality, with quality and provenance increasingly outweighing brand names alone. This shift is directly paralleled in residential preferences, where authentic materials, artisanal details, and evidence of exceptional craftsmanship have become key selling points for discerning buyers.

3. Generational evolution

The Australian luxury market is experiencing a generational shift, with younger affluent consumers bringing different values and preferences to both retail and real estate decisions. While established high-net-worth individuals continue to drive the majority of current luxury spending, developers and retailers alike are adapting their offerings to appeal to the next generation of luxury consumers, who often prioritise authenticity, sustainability, and experiential value.

INTERIOR DESIGN: THE BRIDGE BETWEEN RETAIL AND RESIDENTIAL

Australian interior design trends for 2025 reflect the evolving definition of luxury that spans both retail and residential spaces. The emergence of “gentle luxury” combining refined aesthetics with comfort and authenticity represents a sophisticated middle ground between minimalism and maximalism that appeals to today’s discerning consumers.

This design approach is characterised by rich, earthy colour palettes featuring tones like Mocha Mousse (Pantone’s 2025 Colour of the Year), silvery greys, creamy beiges, and warm terracottas. These colours create environments focussed on harmony and tranquility, addressing the growing desire for homes that provide sanctuary while still conveying sophistication.

The trend extends to material choices, with increasing emphasis on natural textures, quality fabrics, and thoughtfully selected furniture that tells a story rather than simply signalling status. Properties that successfully incorporate these design elements typically achieve stronger market performance, particularly in the ultra-premium segment.

STRATEGIC CONSIDERATIONS FOR LUXURY PROPERTY STAKEHOLDERS

For developers, investors, and marketers in Australia’s premium residential sector, understanding the relationship between luxury retail trends and property preferences offers several strategic advantages:

01

Location synergies

Properties with proximity to established or emerging luxury retail precincts benefit from the spillover effect of high-end brand presence, creating opportunities for premium positioning.

03

Demographic targeting

With different demographic segments exhibiting distinct luxury preferences, residential developments can benefit from tailored approaches that address the specific priorities of their target market, whether established high-net-worth individuals or emerging affluent consumers.

02

Experiential value

Developments that prioritise experiential elements alongside physical attributes align with the broader shift toward experienceled luxury consumption, potentially commanding higher premiums.

04

Material investment

As luxury consumers become increasingly educated about quality and craftsmanship, properties that showcase exceptional materials and artisanal elements generally outperform those focused merely on surface aesthetics.

The outlook for Australia’s premium markets

Looking ahead, Australia’s luxury residential market appears well-positioned to benefit from the continued growth and evolution of luxury consumption patterns. With the luxury retail sector projected to maintain its upward trajectory, and Australian consumers demonstrating sustained appetite for premium experiences, the fundamentals for the high-end property market remain strong.

Properties that successfully align with the evolving definition of luxury, emphasising authentic experiences, exceptional

craftsmanship, and thoughtful design, will likely command the strongest position in Australia’s increasingly sophisticated premium real estate landscape.

The relationship between luxury retail and residential markets continues to deepen, creating opportunities for stakeholders who understand and leverage these interconnections. As both sectors adapt to changing consumer preferences and global trends, Australia’s distinctive approach to luxury living positions it uniquely within the international premium marketplace.

Wellness real estate: THE NEW LUXURY STANDARD

The wellness revolution is transforming luxury real estate, with health and wellness features evolving from optional amenities to essential elements of high-end properties. This shift, accelerated by the pandemic, has fundamentally changed buyer expectations and redefined what constitutes luxury in today’s market.

The Global Wellness Institute reports that the wellness real estate market has expanded dramatically, growing from $438 billion in 2023 to a projected $913 billion by 2028. Australia has emerged as a significant player in this market, ranking tenth globally in overall wellness economy size ($126.68 billion) and an impressive seventh in wellness spending per capita at $4,824 per person. The Australian wellness economy now represents 7.27 per cent of the country’s GDP, highlighting the sector’s growing economic importance.

VANESSA RADER RAY WHITE GROUP HEAD OF RESEARCH

This growth trend is particularly noteworthy in the post-pandemic landscape, where Australia’s wellness economy has reached 134 per cent of its pre-pandemic level, outpacing many other markets. Nearly one third of Australia’s wellness market

expansion since 2019 has been driven by wellness real estate, reflecting a fundamental shift in how homebuyers view their living spaces and establishing Australia as the world’s fourth-largest wellness real estate market as of 2023.

Key wellness features in luxury homes

Modern luxury properties now incorporate an impressive range of wellness features designed to promote physical health, mental wellbeing, and emotional balance:

HEALTH-ENHANCING TECHNOLOGIES

• Seamless indoor-outdoor connections that bring nature into daily living

• Natural, non-toxic materials and finishes that improve air quality

• Abundant natural light through strategic window placement to boost mood and energy

• Living walls and indoor gardens that purify air and reduce stress

• Water features that create calming soundscapes and improve humidity levels

• Views and access to natural landscapes that promote mental restoration

DEDICATED WELLNESS SPACES

• Private spas with saunas, steam rooms, and treatment areas

• Hot and cold plunge pools and magnesium baths for recovery and relaxation

• State-of-the-art home gyms with the latest equipment and virtual training capabilities

• Yoga and meditation studios with sound insulation and calming aesthetics

• Dedicated massage and treatment rooms for in-home wellness services

BIOPHILIC DESIGN ELEMENTS

• Advanced air purification systems that filter pollutants, allergens, and pathogens

• Water filtration technology ensuring pure drinking and bathing water

• Circadian lighting systems that adjust throughout the day to support natural sleep cycles

• Smart home systems that monitor indoor air quality, temperature, and humidity

• Specialised equipment like hyperbaric oxygen chambers and infrared saunas

• EMF-reducing technology to create low-radiation rest spaces

Buyers want homes that not only impress guests but also support their daily health routines, from morning workouts to evening relaxation rituals.

SHIFTING EXPECTATIONS IN LUXURY REAL ESTATE

The traditional markers of luxury real estate have undergone a remarkable transformation. While spacious floor plans and premium locations remain important, buyers now expect properties to actively contribute to their physical and mental wellbeing.

Previously, luxury homes emphasised entertainment spaces like home theatres, wine cellars, and game rooms. Today’s luxury buyers prioritise wellness facilities, often allocating prime floorspace to these areas. In space-constrained properties, wellness features now take precedence over once-standard inclusions.

The expectations have shifted from passive luxury to active wellness. Buyers want homes that not only impress guests but also support their daily health routines, from morning workouts to evening relaxation rituals. This represents a fundamental change in how luxury homeowners interact with their living spaces.

Australia is uniquely positioned to capitalise on the wellness real estate trend. The country’s abundant natural light, favourable climate, and connection to outdoor living create an ideal foundation for wellness-focused properties. From beachside developments featuring saltwater pools and coastal walking trails, to urban properties with rooftop gardens and wellness facilities, Australian luxury properties increasingly emphasise connection to the natural environment.

In major cities like Sydney, Melbourne, and Brisbane, luxury developments are integrating wellness amenities that rival five-star resort spas. These features include not only physical facilities but also programming elements like in-house wellness consultants, nutrition services, and fitness coaching.

Regional markets are also seeing increased demand for wellness features, particularly in areas known for their natural beauty and lifestyle benefits. Coastal regions, wine countries, and mountain retreats are becoming wellness real estate hotspots, where luxury properties are designed to maximise connection with the natural environment.

Properties with integrated wellness features often command higher prices and draw increased interest in comparable homes without these amenities. Wellnesscertified homes (such as those meeting WELL Building Standard criteria) attract health-conscious buyers willing to pay a premium for spaces that promote physical and mental wellbeing.

The return on investment for wellness features often exceeds that of traditional luxury upgrades, as research indicates that properties with comprehensive wellness features can command price premiums of 10-25 per cent compared to similar properties without these amenities.

This wellness premium is increasingly recognised by developers and investors, who are incorporating comprehensive wellness facilities into new luxury developments. From urban high-rises with spa-quality amenities to suburban estates with dedicated wellness wings, the market is responding to this shift in buyer priorities.

Looking forward

As wellness real estate continues to evolve globally and in Australia, we can expect to see more innovative features becoming standard in luxury homes. The emphasis on creating spaces that support holistic health - physical, mental, and emotional - will only strengthen as buyers increasingly view their homes as sanctuaries for restoration and rejuvenation.

Future trends are likely to include more sophisticated technology integration, such as AI-powered wellness monitoring and personalised environmental controls. We’ll also see greater emphasis on sustainability as wellness and environmental consciousness continue to converge in buyer preferences.

For luxury homebuyers in 2025 and beyond, wellness features are no longer just nice-to-have amenities, they’re essential elements of properties that support overall quality of life and wellbeing, representing a fundamental and lasting shift in what defines luxury real estate.

The Australian marine industry: KEY TRENDS AND MARKET INSIGHTS

VANESSA RADER RAY WHITE GROUP HEAD OF RESEARCH

As the luxury property market continues to evolve in Australia, the marine industry represents a parallel ecosystem of high-value assets that offers fascinating insights into wealth distribution, consumer preferences, and emerging technologies. For those tracking Australia’s premium lifestyle sectors, understanding the marine industry’s trajectory provides valuable context about how affluent Australians are choosing to invest and enjoy their prosperity.

MARKET DYNAMICS AND

BUYER PROFILES

The Australian boating market shows distinct regional differences, according to Ray White Marine CEO Brock Rodwell.

“Sydney is characterised by institutional wealth with buyers typically from blue chip office locations,” Rodwell explains, while the Gold Coast represents “a younger market that’s a bit more flashy” with more finance involvement.

Surprisingly, “Melbourne has the highest concentration of larger vessel registrations, though many of these vessels are kept overseas,” notes Rodwell. Meanwhile, Perth is emerging as a growth market centred around affluent areas like Peppermint Grove and Claremont, with buyers largely from mining and agriculture sectors.

Post-COVID, the industry has witnessed a shift in buyer demographics. “We’ve done one or two Bitcoin deals,” reports Rodwell, noting the emergence of tech entrepreneurs in the market. “During COVID, because digital entrepreneurs just skyrocketed, we saw younger buyers purchasing more expensive boats.”

While family decisions remain common in boat purchases, Rodwell observes more solo purchasers emerging: “Younger wealthy tech guys and entrepreneurs make solo decisions.”

Australia’s marine industry continues to thrive in 2025, with over 2,000 businesses generating $10.12 billion in turnover - a 5 per cent increase from 2023. The data paints a vivid picture of a nation deeply connected to its waterways. With 2.5 million Australians holding boat licences (one in ten citizens) highlighting boating as one of the nation’s leading pastimes, the sector has become a cornerstone of Australia’s outdoor lifestyle economy.

What makes this industry particularly noteworthy for observers of luxury markets is how the patterns of ownership, the shift in vessel preferences, and the demographic changes among buyers mirror, and sometimes anticipate, broader trends in premium asset ownership. From cryptocurrency wealth to sustainability concerns, the marine sector offers a microcosm of Australia’s evolving relationship with luxury.

2,000 $10.12 billion

BUSINESSES GENERATING IN TURNOVER

2.5 million AUSTRALIANS HOLDING BOAT LICENSES (ONE IN 10 CITIZENS)

Key trends shaping the market

LARGER VESSELS WITH APARTMENT-STYLE LIVING

The most significant trend is the shift toward larger vessels. Data shows boats in the 6-8m category experiencing 18.9 per cent growth over five years, followed by vessels over 10m (+8.4 per cent).

“Our average new boat size used to be about 50 foot and now it’s probably 70 foot,” Rodwell reports. “People after COVID want to stay on the boats longer and want further range.” This has created infrastructure challenges in Sydney, where berthing facilities are limited.

Australian buyers increasingly prefer “apartment-style living” on the water, with distinct layout preferences. “The Australian trend is they like having a raised galley. They like entertaining and cooking and preparing,” explains Rodwell, contrasting with traditional European layouts where galleys are located below deck.

HYBRID PROPULSION AND SUSTAINABILITY

The marine market is experiencing a surge in hybrid propulsion systems, combining traditional engines with electric motors and battery storage. These options now account for nearly 15 per cent of new boat sales in the 6-8m category, up from just three per cent in 2023.

“A lot of companies are doing hybrid models because the emissions have to come down,” Rodwell explains. “In Europe, you’ve got certain zones where you can’t go into national parks if you’ve got diesel engines.”

Advanced solar technology is also transforming the market: “You’ve got solar panels that are infused in the hull with unlimited range. As long as you’ve got some sunlight, you can just motor on.”

CURRENCY FLUCTUATIONS AND MARKET OPPORTUNITIES

Currency fluctuations significantly impact the market in 2025. “Foreign exchange rates can be difficult to navigate because our deals often involve euros and USD,” Rodwell explains.

However, this creates opportunities for Australian listings. “With the exchange rates where they are, people are focussing back on the local listings,” Rodwell notes. “Once you pay freight, duty, GST, and the currency, those local boats are looking more attractive.”

This is drawing international attention to Australian vessels. “When you tell them you’re saving a million or two just on the currency by itself, that pays for the shipping,” which can cost “between $100,000 to $250,000” depending on vessel size.

INNOVATIVE SALES APPROACHES

The industry is embracing new sales strategies, with Ray White Marine pioneering boat auctions at boat shows. “We’ve got six boats going in the Sanctuary Cove boat show and we’re auctioning two on the first day,” says Rodwell.

This auction approach mirrors real estate strategies: “It only works if you’ve got a genuine vendor ready to get it done. You need the reports that everyone wants because it’s 10 per cent on the day and five days settlement.”

Looking ahead

As we look toward the horizon for Australia’s marine industry, the confluence of larger vessels, advanced technology, and innovative sales methods creates a perfect environment for sustained growth. With hybrid propulsion technology rapidly gaining acceptance and Australian listings becoming more attractive to international buyers due to currency advantages, the industry is navigating toward a promising future.

The evolution toward more sophisticated, environmentally-conscious boating experiences aligns perfectly with Australia’s natural advantages - its vast coastline, diverse waterways, and outdoor

lifestyle culture - positioning the Australian marine industry as an increasingly important player in the global market.

For investors, property professionals, and luxury market observers, the marine sector’s trajectory offers valuable insights. The parallels between highend vessel ownership and premium property acquisition are striking, both markets are seeing similar buyer demographic shifts, sustainability concerns, and design preferences. As these twin pillars of Australia’s luxury lifestyle economy continue to evolve, they will likely influence each other in increasingly significant ways, creating new opportunities for cross-sector collaboration, investment, and innovation in the years ahead.

DEMAND SHIFT TO LARGER VESSELS

Five year growth of registrations as of July 2024

SOURCE: BIA STATE OF INDUSTRY SURVEY

Where is GROWTH?

ATOM GO TIAN

TOP LUXURY SUBURBS BY PRICE GROWTH

House prices in the 95th percentile for March 2025 v 2015

PERTH

NEDLANDS-DALKEITH-CRAWLEY

PERTH CITY BEACH

BRISBANE

NEWSTEAD-BOWEN HILLS

PERTH COTTESLOE

GOLD COAST

MERMAID BEACH–BROADBEACH

BRISBANE NEW FARM

GOLD COAST

SURFERS PARADISE-NORTH

SYDNEY

COOGEE-CLOVELLY

SYDNEY

CASTLE COVE-NORTHBRIDGE

SYDNEY

BONDI BEACH-NORTH BONDI

SOURCE: NEOVAL

Australia has 31 ‘luxury suburbs’ - areas where the typical house price exceeds $2.52 million, with an exception for Sydney where the luxury threshold is higher at $4.09 million (reflecting Sydney’s different standards of luxury). Despite this higher threshold, Sydney still leads the country with 11 luxury suburbs, followed by Melbourne (nine), Perth (three), Brisbane (two), Gold Coast (two), and Canberra (two).

Perth’s luxury market is showing the strongest performance, with all three of its luxury suburbs appearing in the top 10 for price growth nationwide.

Nedlands-Dalkeith-Crawley leads with an 8.8 per cent year-on-year increase, pushing typical house prices from $2.57 million to $2.81 million.

City Beach follows closely with 8.67 per cent growth to $3.08 million, while Cottesloe saw prices rise by 5.9 per cent to $3.30 million, making it the most expensive among the top growth areas.

Brisbane’s two luxury suburbs also make the top 10 list, with Newstead-Bowen Hills growing by 6.35 per cent and New Farm by 4.66 per cent. Similarly, the Gold Coast’s only two luxury areas, Mermaid Beach-Broadbeach and Surfers ParadiseNorth, feature prominently with growth rates of 4.73 per cent and 4.64 per cent respectively.

Despite having the most luxury suburbs, Sydney’s high-end property prices are experiencing more modest growth. The three Sydney areas that made the top 10 growth list - Coogee-Clovelly (2.45%), Castle Cove-Northbridge (2.16%), and Bondi Beach-North Bondi (2.02%) - pale in comparison to the leading performers. Meanwhile, Australia’s most prestigious areas, all in Sydney-Bellevue Hill ($6.54 million), Rose Bay-Vaucluse-Watsons Bay ($6.03 million), and Mosman North ($4.86 million) - recorded one-year growth of just 1.65 per cent, 1.61 per cent, and 1.55 per cent respectively.

Melbourne’s luxury market is struggling even more, with its nine luxury suburbs recording growth between -0.58 per cent and 0.59 per cent - the weakest performance among major Australian cities. Premium areas like Toorak (-0.12 per cent), Brighton (-0.24 per cent), and Malvern-Glen Iris (-0.58 per cent) actually

AUSTRALIA’S TOP LUXURY GROWTH AREAS 2025

experienced value declines. Similarly, Canberra’s two luxury areas showed modest growth between one per cent and two per cent, insufficient to place them among the top performers.

This distribution of growth reveals key trends in Australia’s high-end property market; Perth is experiencing a broadbased property boom that extends to its luxury segment; Sydney’s growth has slowed in the most expensive areas but continues in its more affordable luxury suburbs; Melbourne’s luxury market

NEW FARM

SURFERS

PARADISE NORTH

MERMAID BEACHBROADBEACH

shows signs of cooling with prices falling in some premium areas; and the strong showing from Brisbane and Gold Coast luxury areas indicates growing demand for premium Queensland property. Still, despite these shifts, Sydney still has far more luxury suburbs than any other city, a lead that will likely continue for the foreseeable future.

NedlandsDalkeith-Crawley leads with an 8.8 per cent yearon-year increase, pushing typical house prices from $2.57 million to $2.81 million.

NEDLANDS-DALKEITH-CRAWLEY

COTTESLOE

CITY BEACH

NEWSTEADBOWEN HILLS

CASTLE COVE-NORTHBRIDGE

BONDI BEACHNORTH BONDI

CLOVELLYCOOGEE

METHODOLOGY

The Ray White Luxury Report 2025 represents a comprehensive analysis of Australia's luxury market, drawing on multiple data sources and analytical approaches to provide authoritative insights into this segment.

For our analysis of "What is luxury?", we partnered with research group Neoval to analyse house and unit prices at the 95th percentile across Australian markets. We examined the price points from March 2015 and compared them with corresponding data as of March 2025 to establish 10-year growth trajectories. The 95th percentile represents the price point at which 95 per cent of properties in the market are priced lower and only five per cent are priced higher. This measurement specifically captures the premium segment of the market, effectively defining the entry point to luxury real estate in each location. By using the 95th percentile rather than average or median prices, we're able to focus precisely on the high-end market segment while filtering out the influence of ultra-premium outliers that might skew the data.

To determine who is buying Australia's most exclusive properties, we sourced data from Pricefinder (Valuer General Sales), focusing on top property transactions across Australia with contract dates between March 2024 and March 2025. After identifying the highest-value transactions, we researched the buyers

using publicly available information. This included reviewing company records, media profiles, and industry publications to understand buyers' careers, wealth sources, and backgrounds.

Our architectural and landscape analysis also drew on Pricefinder (Valuer General Sales) data, focusing on top sales across Australia where contract dates fell between March 2024 and March 2025. We pulled photos of each property from realestate.com.au and carefully examined them to identify common features, designs, and materials used in the most valuable Australian properties.

For our luxury retail analysis, we worked with the IBISWorld Luxury Retailing in Australia - Market Research Report (20152030), examining luxury retail market size, business count, and five-year growth rates.

The wellness real estate section drew on data from the Global Wellness Institute, including market size, growth rates, and wellness spending per capita. We analysed global and Australian-specific data on wellness expenditure, certification standards, and property price differentials to establish the concrete market impact of wellness features in residential real estate. This included examining price premiums achieved by wellness-optimised properties compared to conventional luxury homes with similar locations and specifications.

Our marine industry analysis leveraged Ray White Marine's proprietary transaction data and industry knowledge, including business count, market size, and growth in boat sizes by category. We conducted both quantitative analysis of sales volumes and qualitative assessment of buyer preferences and emerging trends.

Finally, to determine where growth is occurring in Australia's luxury markets, we again partnered with research group Neoval, analysing geometric mean house and unit prices at SA2 level. We calculated the geometric mean price for each Australian Bureau of Statistics SA2 region as of March 2024 and compared with corresponding figures from March 2025. We then ranked all luxury SA2s (those with geometric mean house prices exceeding $2.52 million) by their one-year percentage growth to identify the top 10 growth markets.

The geometric mean was selected as our primary statistical measure because it provides a more accurate representation of typical values in markets with significant price outliers. Unlike the arithmetic mean, which can be disproportionately influenced by extremely high-value transactions, the geometric mean calculates the central tendency by finding the nth root of the product of n values. This approach effectively mitigates the distorting effect of ultra-premium outlier sales while still capturing the underlying market dynamics.

APPENDIX 1.

TOP 50 SALES OVER PAST 12 MONTHS

APPENDIX 1.

APPENDIX 2.

TOP 10 SUBURBS BY STATE

NSW Greater Sydney Bellevue Hill

NSW Greater Sydney Rose Bay - Vaucluse - Watsons Bay

NSW Greater Sydney Mosman - North

NSW Greater Sydney Mosman - South

NSW Greater Sydney Dover Heights

NSW Greater Sydney Double Bay - Darling Point

NSW Greater Sydney Bondi - Tamarama - Bronte

NSW Greater Sydney Woollahra

NSW Greater Sydney Coogee - Clovelly

NSW Greater Sydney Castle Cove - Northbridge

VIC Greater Melbourne Toorak

VIC Greater Melbourne East Melbourne

VIC Greater Melbourne Brighton (Vic.)

VIC Greater Melbourne South Yarra - West

VIC Greater Melbourne Kew - South

VIC Greater Melbourne Surrey Hills (West) - Canterbury

VIC Greater Melbourne Balwyn

VIC Greater Melbourne Armadale

VIC Greater Melbourne Malvern - Glen Iris

VIC Greater Melbourne Camberwell

ACT Australian Capital Territory Forrest

ACT Australian Capital Territory O'Malley

ACT Australian Capital Territory Griffith (Act)

ACT Australian Capital Territory Red Hill (Act)

ACT Australian Capital Territory Yarralumla

ACT Australian Capital Territory Reid

ACT Australian Capital Territory Kingston (Act)

ACT Australian Capital Territory Turner

ACT Australian Capital Territory Deakin

ACT Australian Capital Territory Campbell

WA Greater Perth Cottesloe

WA Greater Perth City Beach

WA Greater Perth Nedlands - Dalkeith - Crawley

WA Greater Perth Mosman Park - Peppermint Grove

WA Greater Perth Swanbourne - Mount Claremont

$6,505,301

$5,949,510

$4,874,603

$4,821,443

$4,699,583

$4,635,337

$4,362,511

$4,264,581

$4,262,831

$4,152,677

$3,951,288

$3,145,131

$3,085,936

$3,048,457

$2,810,098

$2,779,025

$2,773,012

$2,636,741

$2,585,052

$2,499,038

$3,854,091

$2,543,742

$2,289,609

$2,250,522

$2,233,320

$2,198,907

$2,063,119

$1,997,247

$1,963,397

$1,825,129

$3,328,687

$3,066,877

$2,822,013

$2,509,219

$2,391,662

APPENDIX 2.

WA Greater Perth Claremont (Wa)

$2,378,726

WA Greater Perth Floreat $2,241,690

WA Greater Perth Applecross - Ardross $1,997,091

WA Greater Perth Subiaco - Shenton Park $1,934,157

WA Greater Perth Trigg - North Beach - Watermans Bay $1,881,059

QLD Greater Brisbane New Farm

$2,792,768

QLD Rest Of Qld Surfers Paradise - North $2,662,919

QLD Greater Brisbane Newstead - Bowen Hills $2,657,095

QLD Rest Of Qld Mermaid Beach - Broadbeach $2,631,431

QLD Greater Brisbane Ascot $2,465,175

QLD Rest Of Qld Surfers Paradise - South $2,448,533

QLD Rest Of Qld Noosa Heads $2,353,138

QLD Greater Brisbane Hamilton (Qld) $2,293,608

QLD Greater Brisbane Bulimba $2,289,302

QLD Rest Of Qld Sunshine Beach $2,220,730

SA Greater Adelaide Toorak Gardens $1,883,401

SA Greater Adelaide Beaumont - Glen Osmond $1,734,065

SA Greater Adelaide North Adelaide $1,690,591

SA Greater Adelaide Unley - Parkside $1,650,849

SA Greater Adelaide Goodwood - Millswood $1,622,396

SA Greater Adelaide Burnside - Wattle Park $1,614,122

SA Greater Adelaide St Peters - Marden $1,609,708

SA Greater Adelaide Walkerville $1,606,224

SA Greater Adelaide Mitcham (Sa) $1,564,449

SA Greater Adelaide Norwood (Sa) $1,468,299

NT Greater Darwin Larrakeyah $1,429,804

NT Greater Darwin Fannie Bay - The Gardens $1,079,321

NT Greater Darwin Woolner - Bayview - Winnellie $910,587

NT Greater Darwin Nightcliff $854,943

NT Greater Darwin Stuart Park $850,531

NT Greater Darwin Parap $841,365

NT Rest Of Nt Ross $833,183

NT Greater Darwin Lyons (Nt) $814,034

NT Greater Darwin Rapid Creek $757,964

NT Greater Darwin Howard Springs $756,517

Ray White Economics Team

NERIDA CONISBEE Chief Economist

VANESSA RADER Head of Research

JORDAN TORMEY Strategy Analyst

ATOM GO TIAN Senior Data Analyst

PAOLO SUMULONG Data Analyst

ANITA VENKATESH Content Strategy and Production Lead

KRISTEN PURCELL Senior Graphic Designer