THE biannual recalculation of the FE Crown Ratings reflected a broad-based fall in the markets last year.

Only nine Australian broad cap equity funds received a fivecrown rating, compared with over four times that in the September calculation. Inversely, the global broad cap equity sector saw 25 five-crown rated funds, compared with nine at the last calculation.

And, while most Aussie broad caps battled against sentiment flowing on from the Royal Commission, a drop in house prices and a pretty tough Q4 last year, some stalwarts, like Macquarie Investment Management and SG Hiscock & Company managed to grab hold of a five-Crown rating.

Looking at style more generally, the market showed no mercy to value or growth, but cyclicals, which dominate in value styles, were hit the hardest, meaning the market worked against value more than it did growth.

Strategies that managed to encompass diversity in terms of both geography and stock selection, however, were those which shone in the period.

FE’s head of data, Australia and New Zealand, Stuart Alsop, said the equity market in general has become more volatile in recent times, and there are signs this volatility is here to stay, so now, more than ever, it is an opportunity for fund managers, portfolio managers and strategies to set themselves apart and excel in active management.

BY MIKE TAYLOR

THE Association of Financial Advisers (AFA) has issued a statement formally objecting to the Australian Labor Party (ALP’s) plan to ban grandfathered commissions on investment and superannuation products by the end of 2019.

The AFA chief executive Phil Kewin said his organisation believed that such a move would hand yet another victory to the big end of town at the expense of small financial advice businesses and their clients.

“Attempting to turn off grandfathered commissions in such a short time frame will only serve to benefit institutions who will be able to hold onto them, with no compulsion to pass any benefit on to consumers,” he said. “Many clients currently receiving advice

services for these payments will lose access to them, without any reduction in their fees.”

“If the concern is that some advisers are receiving grandfathered commissions without providing a service, then there are other options to address this issue, without negatively impacting those clients who are in grandfathered commission paying products and are happily receiving services and advice from their financial adviser,” Kewin said Kewin said the argument that grandfathered commissions have continued for too long is not reflected in the facts claiming that “there were zero cases of inappropriate financial advice as a result of grandfathered commissions during the Banking Royal Commission hearings and

Continued on page 3

THIRTEEN superannuation funds have accepted they can’t cut the mustard under the Australian Prudential Regulation Authority’s (AFCA’s) member outcomes arrangements and are exiting the industry.

APRA chairman, Wayne Byres has told the Senate Economics Committee that the regulator had identified an initial group of 28 funds which it believed where delivering poor outcomes for members “across a range of dimensions”.

He said the trustees of those funds were challenged by APRA to justify how they were delivering value for members.

“Of these, 13 have looked at the evidence and have exited or are exiting the industry, and another seven have changed product pricing or fees in some way to make their offerings more competitive,” Byres said.

He said that, of the remainder, five were deemed on further exploration to have better performance than first appeared, and actions in relation to the other three were expected to be agreed shortly.

3

The Australian Securities and Investments Commission has been wounded by the Royal Commission and is out to prove a number of important points, no matter what the cost.

IT IS NOW eight years since Tony D’Aloisio was the chairman of the Australian Securities and Investments Commission (ASIC) and was heard likening the regulator to a policeman who turned up to a motor vehicle accident to clean up the mess.

Such an attitude gels with the recollection of financial services barrister, Noel Davis who, in a column published elsewhere in this edition of Money Management recalls being told by ASIC staffers of the regulator’s reluctance to pursue litigation against financial services miscreants because of the embarrassment of losing.

Just over 10 years on from the global financial crisis and armed with a new funding regime, more powers and access to greater penalties ASIC is portraying itself as more than just a country copper on clean-up duty. It is portraying itself as having transfigured from watchpoodle to fully-fledged watch-dog.

The criticisms levelled at ASIC during the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry together with the trenchant, if opportunistic criticisms of

politicians, have prompted the regulator to bare its teeth.

If any proof were needed of this it was last week’s announcement by ASIC’s new deputy chairman and resident silk, Daniel Crennan QC, that the regulator would be going to the trouble and expense of appealing the recent Federal Court decision upholding the position of Westpac Securities Administration Limited and BT Funds Management Limited with respect to the difference between general and personal advice.

ASIC’s decision, led by Crennan, to pursue the appeal will warrant being closely monitored because it will be both costly and, if successful, will establish some important precedents for the regulator not only in terms of what represents “general” and “personal” advice for the purposes of key sections of the Corporations Act but also how litigious ASIC is prepared to be.

The appeal against the Federal Court decision must also then be weighed against the reality that ASIC is currently weighing up the possibility of legal action against a number of people whose names were referred to the regulator by the Royal Commission into

Misconduct in the Banking, Superannuation and Financial Services Industry.

The names of those referred by the Commissioner, Kenneth Hayne, have not been disclosed but are speculated to include some former and current senior financial services executives giving rise to the likelihood that any charges escalated to the courts will be hotly-contested with the defendants acutely aware of the fact that the penalties available to ASIC have been significantly increased.

As a result of Government legislation passing the Parliament last week, the maximum prison penalty for the most serious offences has been increased to 15 years and for civil penalties for companies to operate under an increased cap of $525 million.

As well, the maximum civil penalties for individuals will increase to $1.05 million.

The bottom line, therefore, is that ASIC is on a mission to prove its detractors wrong and someone will be made to pay.

Mike Taylor Managing Editor

FE Money Management Pty Ltd

Level 10

4 Martin Place, Sydney, 2000

Managing Director: Mika-John Southworth

Tel: 0455 553 775

mika-john.southworth@moneymanagement.com.au

Managing Editor/Editorial Director: Mike Taylor Tel: 0438 789 214

mike.taylor@moneymanagement.com.au

Associate Editor - Research: Oksana Patron Tel: 0439 137 814

oksana.patron@moneymanagement.com.au

Features Journalist: Hannah Wootton Tel: 0438 957 266

hannah.wootton@moneymanagement.com.au

Journalist: Anastasia Santoreneos Tel: 0438 836 560

anastasia.santoreneos@moneymanagement.com.au

Events Executive: Candace Qi Tel: 0439 355 561 candace.qi@financialexpress.net

ADVERTISING

Sales Director: Craig Pecar

Tel: 0438 905 121 craig.pecar@moneymanagement.com.au

Account Manager: Ben Lloyd Tel: 0438 941 577 ben.lloyd@moneymanagement.com.au

Account Manager: Amy Barnett Tel: 0438 879 685 amy.barnett@financialexpress.net

PRODUCTION

Graphic Design: Henry Blazhevskyi

Subscription enquiries: www.moneymanagement.com.au/subscriptions customerservice@moneymanagement.com.au

Money Management is printed by Bluestar Print, Silverwater NSW. Published fortnightly.

Subscription rates: 1 year A$244 plus GST. Overseas prices apply. All Money Management material is copyright. Reproduction in whole or in part is not allowed without written permission from the editor. © 2019. Supplied images © 2019 iStock by Getty Images. Opinions expressed in Money Management are not necessarily those of Money Management or FE Money Management Pty Ltd.

ACN 618 558 295 www.financialexpress.net

© Copyright

BY MIKE TAYLOR

FINANCIAL PLANNING firms with long-running client disputes should brace themselves for referral to the Australian Financial Complaints Authority (AFCA), following a key move by the Treasurer, Josh Frydenberg.

The Treasurer has announced that the Government has extended AFCA’s remit to consider financial complaints dating back to 1 January, 2008, consistent with the time-span examined by the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

He said that AFCA would be able to consider disputes dating back to 1 January, 2008, that had not previously been hard and which fell within AFCA’s current monetary limits and compensation thresholds.

Frydenberg said that to give effect to the direction, AAFCA would now consult on updating its rules so that it was in a position to begin receiving

Continued from page 1

research by Investment Trends indicates that grandfathered commissions have declined from over 30 per cent of advice practice income in 2010 to just nine per cent in 2018.”

“At no stage have the objectives and potential consequences been discussed or debated,” he said. “Both Treasury and ASIC have confirmed that they have not done any research or investigation to confirm the current level of grandfathered commissions or the implications of seeking to remove it. Achieving the right outcome for clients is a much more complex proposition than is appreciated by any of the proponents for a ban.”

Kewin said the proposed ban was therefore simply an issue of political expediency, which numerous stakeholders had sought to use in order to leverage political, media and commercial benefit at the expense of small business and consumers.

“This is neither fair nor

complaints under its expanded remit from 1 July, this year.

The ANZ has already committed to allowing AFCA to examine cases dating back to 1 January, 2008.

acceptable as it jeopardises the livelihoods of professional, hard-working financial advisers. The potential financial and emotional impact on these people is profound. Forcing a transition sooner than practical also jeopardises the ability for clients to remain in an advice relationship.”

The AFA chief executive said the ALP’s proposed move was unnecessary, especially given that there were avenues for a sensible transition available to the Government and Opposition to consider, should they choose to work with the industry.”

He said small business financial advice practice owners had acquired businesses in recent years that included grandfathered commission clients and had taken out loans to fund these acquisitions on the basis of prevailing valuation methods.

“These small business owners had no expectation that grandfathered commission arrangements would come to a sudden end,” Kewin said.

BRISBANE-BASED financial planning firm, Futuro Financial Services Pty Ltd has ended its relationship with AMP Limited and is now 100 per cent privately owned and non-aligned.

The company’s executive chairman, Dennis Bashford announced that the relationship with AMP had been formally ended.

“With a 17-year track record at Futuro, we felt we were perfectly positioned to make the best of the current environment and as part of this have now formally finalised the end of our relationship with AMP,” he said.

He said that for the last 18 months Futuro had been “going through transitional change to satisfy tomorrow’s advisers”.

“We feel that the conscious move to become a non-aligned AFSL means we are looking forward to future with excitement and anticipation,” Bashford said.

Continued from page 1

The APRA chairman told the committee that further consolidation in the industry was likely as a result of the regulator’s action.

“It is difficult to argue that Australia needs as many as 200 superannuation funds or 40,000 plus investment options. But that well-worn adage remains true: past performance is not necessarily a good guide to future performance,” Byres said. “We also need to ensure that new competitors to the marketplace, who will inevitably start without a track record and potentially high costs until they can generate scale, are not prohibited from entering the system.”

He said that, for these reasons, APRA continued to advocate an approach that looked at performance of trustees across a number of dimensions, and did not rely solely on measures of historical returns over a particular time horizon as the only determinant of success or otherwise.

BY MIKE TAYLOR

OUTGOING National Australia Bank (NAB) chairman, Ken Henry will not be a member of the board committee which selects the bank’s new chief executive or his replacement as chairman.

NAB revealed Henry’s absence from the selection committee to the Australian Securities Exchange (ASX) at the same time as

confirming that exiting chief executive, Andrew Thorburn would receive a payment of $1,041,449 in lieu of 26 weeks’ notice along with accrued entitlements.

However, it said that Thorburn’s unvested deferred awards would be forfeited in accordance with plan rules.

NAB’s interim chief executive, non-executive director, Phil Chronican will receive a fixed monthly fee of $150,000 including superannuation, representing annualised remuneration of $1.8 million and will not receive nonexecutive director fees in the role.

The selection committee to recruit a new chairman will be chaired by director, David Armstrong while the CEO selection committee will be chaired by Ann Sherry.

CLEARVIEW has announced new pricing arrangements for its LifeSolutions customers effective from 1 March, claiming the changes reflect the realities of underlying claims experience across the industry and the economic environment.

In an announcement released by ClearView’s general manager of distribution, Christopher Blaxland-Walker the company said that premiums had been revised across all cover types including Life, Income Protection, Total and Permanent Disability (TPD), Trauma and Business Expense Cover.

It said that for stepped and hybrid premiums the changes would, in general, reduce Life and TPD premium rates and increase Trauma, Income Protection and Business Expenses premiums.

The company’s statement said premium rates for new Level premium business were generally increasing.

“Level premium rates are sensitive to investment market interest rates (we have to invest

some of the initial year level premium to pay for the longer term claims costs). With the sustained low interest rate environment, coupled with higher Income Protection and Trauma claims costs, unfortunately overall these rates have to increase,” it said.

THE secret to IOOF weathering the recommendations of the Royal Commission appears in large measure to be owed to the high proportion of self-employed advisers working under its dealer group brands.

IOOF describes it as “the selfemployed advice model”.

The company’s relatively modest estimate of client remediation costs and exposure to the loss of grandfathered commissions is owed to the fact that it has 1,379 self-employed advisers working within its Financial Services Partners, RI Advice, Millennium3, Bridges, Lonsdale and Consultum dealer groups and just 176 salaried advisers working within Shadforth.

Thus, the company estimates the total net impact of grandfathered commissions received in the first half of the current financial year as being $3.4 million, while it has described the financial impact on IOOF of an end to life/risk commissions as being “not financially material”.

Describing its approach to the recommendations flowing from the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry IOOF told investors that situation with respect to grandfathered commissions was very much in the hands of advisers.

“Advisers will need to consider the impact on their business including its remuneration structure and valuations, if not so already,” the company said. “There is potential contention around the date to end grandfathered commissions if Labor is election – it’s unlikely to be brought forward to any earlier than 1 July, 2020.”

On the question of life risk insurance commissions, IOOF said advisers would need to “consider their value proposition for insurance advice and how this would fit into a fee-only world in three years’ time”.

“This will also affect advice business valuations,” it said.

BY MIKE TAYLOR

AN accountant involved in the establishment of self-managed superannuation funds (SMSFs) has entered into an enforceable undertaking (EU) with the Australian Securities and Investments Commission (ASIC) after it found she had failed to act in the best interests of her clients and prioritised her own interests.

ASIC announced that the accountant, Jenan Oslem Thorne of Saber Superannuation Pty Ltd has entered into an EU which prevents her from providing financial services for a period of three years effective from 13 February, this year.

ASIC said it decided to review Thorne’s advice when it discovered, during its investigation into Park Trent Properties Group Pty Ltd,

that she was receiving referrals in relation to establishing SMSFs from Park Trent.

ASIC reviewed advice provided by Thorne when she was a representative of SMSF Advice Pty Ltd, a wholly owned subsidiary of AMP Limited, and concluded that she had advised some of her clients to establish SMSFs without taking their circumstances into account.

The ASIC announcement said the regulator found that Thorne hadn’t properly considered her clients’ existing superannuation arrangements or explored why they were interested in investing in direct residential property through an SMSF. When recommending SMSFs to some of her clients, she had inappropriately scoped advice by excluding insurance and retirement planning.

ASIC also found that Thorne did not

BY OKSANA PATRON

FORMER members of the Macquarie Asian Equities team have set up Stonehorn Global Partners and launched its new billion-dollar Asia Equity Fund. Also the firm would be joined by co-founders Duke Lo and John Lam who previously worked for 10 years together, managing over $4 billion.

The new entity would be headed by Sam Le Cornu and backed by Australia’s Trawalla Capital.

The new fund would have a disciplined investment process and would be unconstrained (benchmark, sector, country and market-cap agnostic). It would hold approximately 30 stocks in MSCI Asia ex-Japan.

The fund would be based on-the-ground in Hong Kong to better leverage the team’s local networks, language skills and high-level access to Asia’s leading companies, the firm said.

“Our investment approach is the same as what we did in the last decade” Lam said.

“The principles behind how we organize ourselves are also the same. What will be different this time is the environment, market inefficiencies will always exist, and all it really does is further set apart the good managers from the mediocre.”

Trawalla Capital, is a private investment firm of the Melbournebased Schwartz Family Office, headed by Alan and Carol Schwartz. Trawalla Capital would be also a shareholder in Stonehorn and a significant investor in the inaugural fund.

“Stonehorn Global Partners will be Trawalla Capital’s third portfolio company complementing Qualitas, a real estate investment management firm and Armitage Associates, a growth equity firm,” MrSchwartz said.

“We are therefore delighted to be partnering with Sam, John and Duke. They are established leaders who are proven in their field, whose values and approach are strongly aligned with our own.”

The fund would initially be open to investment from institutional and wholesale investors in Asia, Europe and Australia, including high networth individual investors, family offices and institutions.

It would be expected to be open to institutional and wholesale investors in April-June 2019, the firm said.

adequately stress-test SMSF strategies and had recommended SMSFs to some of her clients despite inadequate evidence to suggest that the strategies would provide increased retirement benefits.

Furthermore, Thorne had recommended that her accountancy practice, Saber Accountants Pty Ltd, prepare the annual accounts and tax returns for the SMSF clients. This led ASIC to determine that Thorne recommended the services of a related party to create extra revenue for herself.

As part of the EU, Thorne has agreed to inform all her former personal advice clients about the EU and provide contact details of her former licensee, SMSF Advice Pty Ltd. Former clients of Thorne who have enquiries or complaints regarding her advice or conduct should contact SMSF Advice Pty Ltd.

BY ANASTASIA SANTORENEOS

GIVEN the tough Q4 all funds across the board faced last year, Money Management looked at the performance of global equities in January this year to see which funds bounced back in January and gave investors the best start to 2019.

The top fund in January, UBS Global High Conviction, returned 10.66 per cent for the month – a massive feat compared to its bottom position the previous month, with -10.84 per cent returns. It’s similarly a step up from its performance in January last year, where it returned 3.41 per cent.

In fact, the top fund for the month returned around six per cent more than the top fund for December, Fidante Credit Suisse Global Private Equity, which returned (4.10 per cent).

The second-top fund, Invesco Wholesale Global Opportunities Hedged, similarly outdid its December performance, returning 10.34 per cent in January as opposed to -6.42 per cent in December. Again, like UBS, the fund also got off to a better start this year than last, where it returned 3.50 per cent.

Perpetual’s Wholesale Global Share Hedged returned 10.32 per cent compared to -7.50 per cent in December last year, and Pan-Tribal Global Equity returned 9.83 per cent as compared to -5.35 per cent the month prior.

The last fund to comprise the top five for the month was Evans and Partners International Hedged, which returned 9.63 per cent, which again is a feat compared to its December returns of -5.51 per cent, and its January 2018 returns of 1.03 per cent.

What’s clear is that the top funds genuinely doubled returns to make back the month, not unlike the MSCI AC World ex Australia index, which returned 4.78 per cent in January compared to -3.62 per cent in December last year.

As well, where only five funds in the sector managed to stay above the line and produce positive returns, only one fund, the Stewart Investors Wholesale Worldwide Leaders fund, dropped to negative for the month, returning -2.26 per cent.

BY MIKE TAYLOR

THE major banks would be made to divest their interests in financial planning and financial planners would have to be individually licensed under policy approach prescribed by the Australian Greens and revealed in a key Parliamentary Committee report.

In additional comments attaching to the House of Representatives fourth Review of the Four Major Banks, Greens committee member Adam Bandt said his party’s policy approach would require banks to divest themselves of financial advisory and brokerage services, such as CommSec and Nabtrade.

“The Greens would also ensure that the wealth management companies that the banks are selling are split so that superannuation is separated from product issuance and financial planning,” his commentary to the committee’s report said. “A failure to do so would still leave an inherent conflict of interest within essential service providers.”

CHALLENGER Limited has acknowledged that the negative perceptions of financial planners generated by the Royal Commission and other events are having an impact on its annuities business.

In commentary attaching to the release of its half-year results, Challenger said its Life business relied on financial advisers, both independent and part of major hubs, to distribute its products.

“Following hearings on financial advice in the Royal Commission into Misconduct in the Banking and Financial Services Industry there has been reduced customer confidence in retail financial advice and significant disruption across the adviser market,” it said.

“This includes increased adviser churn and reduced acquisition of new clients by financial advisers.”

“While there is a relatively less direct impact form the Royal Commission final report on Challenger, and Life’s customers are not questioning the quality of its products or services, the disrupted industry environment is impacting Life’s sales,” the commentary said.

“Life has a strong reputation with adviser trust in the quality of its products and services and is broadening its distribution reach by making its annuities available on platforms targeting the individual financial advisers market,” it said.

“Within the remaining complex and selective components of the finance industry, separation would be primarily on the basis of whether products are retail grade or investment grade, and whether customers are retail investors or sophisticated investors, as it currently is.”

The Greens would introduce a range of measures to increase protections for retail consumers including:

• Financial planners will have to establish an industry-wide indemnity scheme;

• Financial planners will have to be individually licenced and need to be owned and operated separate from any product issuance firms if they are to call themselves a financial planner;

• Mortgage brokers will need to be owned and operated separate from any lending institution; and

• Financial planners and mortgage brokers will no longer be able to receive commissionbased sales.

Westpac: It would have to divest its wealth management

arm, BT Financial Group, and break-up superannuation, insurance and wealth management.

ANZ, CBA and NAB:

ANZ, CBA and NAB are on the way to divesting their wealth management arms. But they will be compelled to finish the job and also have to divest their trading platforms.

Macquarie Bank:

It will no longer be able to operate as a retail bank (ADI) and investment bank.

AMP:

It will have to break-up. Currently it is an ADI, as well as offering superannuation, insurance and wealth management. It will need to choose one area to operate in.

MLC:

Currently owned by NAB, but is being sold off. In addition to this it will have to break up superannuation, insurance and wealth management.

OnePath:

Currently owned by ANZ, but is being sold off. In addition to this it will have to break up superannuation, general insurance and wealth management.

MORE research has emerged confirming financial planners and mortgage brokers rather than the major banks and product manufacturers have emerged worse off from the final report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

A Roy Morgan Research analysis confirmed that it is the financial services intermediaries who are being most negatively impacted.

It said that financial planners and mortgage brokers currently account or the distribution of 35 per cent of the total value of the major financial products and that this covered the combined value of home loans, superannuation, life/risk insurance and managed funds.

“A number of the recommendations of the Royal Commission relate to mortgage brokers and financial planners and, if adopted, are likely to negatively impact their usage, particularly as it relates to borrowers rather than lenders paying fees,” the research analysis said.

The Roy Morgan analysis provided a chart revealing how consumers obtained financial products and noted that the use of intermediaries was not the same for all major financial product groups, with the high level being for managed investments with 56 per cent being

owed to the use of financial planners. It said that for superannuation, employers played the major role and accounted for 60 per cent of the market, with intermediaries accounting for 32 per cent with this being mainly due to the default fund being the major fund chosen.

The research revealed that in the case of life/risk the main channel used was by going direct to the company (40 per cent) followed by employers (27 per cent) and intermediaries (24 per cent).

Commenting on the research results, Roy Morgan industry communications director, Norman Morris said a lot of the issues raised in the Royal Commission were as a result of how bank customers purchased their product and the extent to which their needs were understood and taken into account.

“Many of the problems reported were a result of consumers having insufficient financial literacy skills for the product they were purchasing and who were obtaining it through a channel not designed to focus on their best interests,” he said.

“This research shows how significant the intermediaries are in the purchasing decisions of the major financial products and as a result there is a need to understand who they are and how they are remunerated,” Morris said.

BY MIKE TAYLOR

FIDUCIAN Group has defied the Royal Commission and market challenges which have impacted other financial services groups to post a 15 per cent increase in statutory net profit after tax to $5.004 million for the half-year ended 31 December.

At the same time the company signalled no slackening in growth plans, with Fiducian telling the Australian Securities Exchange that the Board’s policy to build through structural growth by offering client administration services, sale of financial planning software and Fiducian Funds to external markets and as well through acquisition of financial planning portfolios was fully embraced by management.

It said the results were

gradually showing and that through all the recent shortterm turmoil the group had continued on growth and expansion plans and delivered a solid increase in earnings.

Looking at the current environment in Australia, the Fiducian announcement pointed

to recent market volatility and said that while it believed the market’s reactions to events had been overdone it believed such volatility would become the norm rather than the exception. The company declared an interim fully franked dividend of 11 cents per share.

AMP Limited has reflected the full impacts of the recent Royal Commission and other events reporting a significant decline in statutory net profit of just $28 million down from $848 million in the previous year due to advice remediation and subdued performance in wealth protection.

At the same time, the company listed transforming the wealth management business and reshaping the advice networks as being part of its 2019 priorities.

It said it would be streamlining wealth management’s operating model and product offering.

The company’s new chief executive, Francesco De Ferrari described 2018 as having been a challenging year for AMP with the continued growth of AMP Capital and AMP Bank managing to offset the headwinds faced in Australian wealth management.

He described the Royal Commission as having been “a confronting but valuable experience for the financial services industry” which had served as a catalyst for change at AMP.

“We have undertaken Board and leadership renewal, accelerated client remediation and sharpened our focus on delivering better value to customers, including reducing fees on our MySuper products,” he said.

De Ferrari said that 2019 would be a transitional year for AMP as it prioritised the complex legal separation of the life insurance business and delivered on its commitments to remediate advice customers and strengthen its risk management and governance controls.

The AMP results showed that its Australian wealth management earnings declined by $28 million to $363 million mainly due to higher margin compression from the MySuper fee reduction, weaker investment markets and the transition of clients to lower-cost contemporary products.

The company declared a final dividend of four cents per share.

A key parliamentary committee has thrown more focus on the future of IOOF’s acquisition of the ANZ’s OnePath pensions and investments business and the now critical role of the trustee board.

The House of Representatives Economic Committee report stemming on its fourth Review of the Four Major Banks specifically traversed the status of the IOOF/ ANZ transaction and noted that it was proving to be complex.

The committee report said ANZ’s deputy chief executive, Alexis George had been asked about the status of the sale and had said that it was incomplete.

The report also noted that George had said she was “conscious of the legal requirement for ANZ to act in the best interests of the members of its superannuation fund throughout the transition process”.

“The committee pointed to failures of governance and compliance by IOOF highlighted during the Royal Commission’s superannuation hearings and questioned how the sale of OnePath P&I could be in the best interests of its members,” the report said.

“Ms George responded by stating: we’ve had multiple contacts, formally and informally, with the management and with the board of IOOF to inquire about the issues that arose and what they were doing to address those, what they had done to address those in the past.”

“In addition, Ms George noted there is an independent trustee board to provide a check and balance against ANZ’s decisions,” the report said.

The committee’s report follows on from the final report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry which specifically referenced the key role of the OnePath trustee board and complemented it on the independence it had demonstrated to that point.

Financial services barrister Noel Davis examines the testimony given to the Royal Commission and its ultimate findings and suggests that for as much as it discovered there was plenty that it missed.

THE BANKING AND financial services Royal Commission final report identifies some of the poor behaviour and shortcomings in the delivery of financial services to customers, but does not identify all of the problems.

The Commission has already had a substantial financial impact on some of the financial institutions with large sums being taken out of their profits to compensate clients. However, clients, particularly retirees, who have been the subject of poor treatment or have received bad financial advice and have lost their savings have, relatively speaking, suffered far greater losses.

Where did it all go wrong?

Insofar as the financial institutions are concerned, the fault lies squarely with the boards of directors.

Many of those directors had little or no financial services experience. They didn’t, therefore, have the knowledge or the experience to make the enquiries to establish what the problems were in the way in which the businesses were being conducted and what the customers were being exposed to.

They did not, for example, generally establish board compliance committees which would have enabled the committee members to obtain hands on knowledge of what complaints were being made and what was happening in communications with the regulators.

Most of those institutions have problems with the way in which they are structured which result in them being riddled with conflicts of interest. They, generally, are the trustee of the superannuation and investment funds that they offer, the administrator of the funds, the investment manager of the funds’ moneys and the life insurer of the members of the superannuation funds. If the directors recognised the conflicts of interest inherit in these structures, they mostly didn’t

do anything about it.

Years ago, as a member of the Superannuation Complaints Tribunal (SCT) which dealt with superannuation cases, in a dispute over whether an insurer should have paid a disablement claim which should have been paid, I queried whether the employees of the financial institution who sat on the superannuation trustee board of directors and who agreed with the insurer’s decision to refuse the claim, had a conflict of interest given they were employees of the company that owned the insurer.

The submission to the Tribunal by the trustee was that there was no conflict of interest. There was, therefore, no recognition that there was a conflict problem.

The decisions of that Tribunal frequently identified shortcomings in the way in which some superannuation funds were administered but, in the 13 years I was a member of the Tribunal, I became aware that directors of the trustee of the fund which was the subject of a particular decision were often not told of the decision or the contents of it. Again, it appears that directors didn’t make enquiries about such decisions. Consequently, the issues identified in the decisions of the Tribunal continued to occur.

The failure of financial institutions to deal with the problems identified in the evidence to the Royal Commission was allowed to continue because of the

weak regulation that became apparent from the evidence. That has been long standing. A long time ago, when the Australian Securities and Investments Commission (ASIC) took over the regulation of superannuation from the former Insurance and Superannuation Commission, I did some training sessions for ASIC employees on regulating superannuation funds. When I and my colleagues discussed the circumstances in which ASIC would litigate or prosecute, the reaction of the ASIC officers was that litigation was to be avoided to avoid the embarrassment that would go with losing some cases. Finally, that appears to be changing. Perhaps, consequently, financial institutions and trustees will treat the regulators more seriously than they have in the past.

The Commission’s final report raised the question of whether charging clients for advice when none was provided was dishonest and, thereby, in breach of the legislation. A recent decision of the SCT required a financial institution to refund fees charged to a superannuation fund member for advice, when no advice was provided, but whether a prosecution for dishonesty will succeed is uncertain. For a successful prosecution to occur it will have to be proven, that the accused knew that no services were being provided.

An issue that did not receive much attention in the evidence

before the Commission and in its report, other than hosting employers, is the large amounts spent by industry not for profit superannuation funds on advertising and promotion.

In spending those amounts, the legislation requires that it must be in the members’ best interests. The argument often used to justify the expenditure, which of course reduces the earnings distributed to members’ accounts, is that it attracts new members which reduces the overall fees charged to members. The evidence that the members’ fees are reduced by advertising is scant. There will, of course, at some point, be a challenge by a member to this practice and the relevant trustee will have the opportunity to demonstrate that amounts spent on promotion is in the existing members’ best interests.

Performance fees and similar fees, where investment managers receive around 25 per cent of investment earnings above a minimum level, also did not receive attention by the Commission. It may, one day, be tested whether a particular investment arrangement which includes such fees is in the best interests of the affected members.

The Royal Commission did not concentrate to any extent on the millions of dollars of life savings that have been lost by investors, including retirees who can never get the money back, as a result of bad or fraudulent investment advice by a minority of financial planners. However, it may well be that the financial institutions who licenced those advisers might ultimately be held responsible for some of the losses, thus adding to their own losses.

Noel Davis is a Sydney barrister, a former director of financial services companies and a former member of the Superannuation Complaints Tribunal.

Actively monitor & optimise client’s models and managed accounts

Powerful research engine with unbiased tools, benchmarks and ratings

Demonstrate your value using best in class reporting

Ensure transparency; fee adjusted performance fully updated for RG97

Comprehensive Australian SMA, fund, superannuation and equity data

For information on how the award winning FE Analytics can help you deliver better client outcomes visit –www.financialexpress.net/contact or call 0280657187

Anastasia Santoreneos discusses strategic and holistic advice with last year’s Money Management Women in Financial Services Awards winner, Sunitha Chamala.

THE ROYAL COMMISSION prompted advisers to focus on enhancing the client experience, but last year’s Money Management Women in Financial Services Award’s Rising Star winner, Sunitha Chamala, is already ahead of the eight-ball, tailoring specialist technical advice for her clients to achieve their broader lifestyle goals.

Her role as a strategy adviser at Elston is to provide clients with specialist technical advice on all aspects of wealth planning that is tailored to their individual circumstances, and it’s something she says is crucial to long-term financial success.

“Strategic advice assists in maintaining a strong connection between the client’s individual circumstances and their underlying investments,” said Chamala.

It involves collaborating with professional partners like accountants and solicitors, optimising income, utilising tax structures where appropriate, taking risks, and having the right mix of assets.

It’s important, she says, because what clients need from their advisers can vary, with some needing peace of mind that they’re on the right track and others seeking a long-term relationship and a disciplined plan to accumulate and preserve wealth over time.

What’s key to technical advice, though, is that while those delivering it may only actively manage a portion of their clients’ overall assets, they must always consider these in the context of their clients’ position.

“This includes taking into consideration their other financial assets, their family situation, their personal attitudes and beliefs and

their lifestyle goals,” she says.

Looking at investments in isolation is a meaningless exercise, and alone, they’re a means to an end, she says.

“What drives good advice is a trusted relationship and a deep understanding of clients’ fears, hopes and expectations. Clients will be more successful if they are engaged in the advice process and are put in a position where they are able to make informed decisions about their own financial futures.”

Something that underpins her understanding of advice is her extensive education. Chamala is a Certified Financial Planner (CFP), a Self-Managed Super Fund Specialist, has a Bachelor of Commerce, majoring in Accounting and Finance, and has completed an Advanced Diploma of Financial Services.

“I believe that education is an important stepping stone to being a trusted adviser,” she said. “Without a degree, I would have found entering the financial planning industry quite challenging.”

While she says there’s no doubt much of what she learned over time stemmed from her experience meeting and working with clients, completing her Bachelor’s degree provided her with sound base knowledge as well as a broader understanding of commerce and economics.

“Completing the CFP Certification Program and attaining the Self Managed Super Fund Specialist Adviser accreditation has developed my technical knowledge and are powerful symbols to my clients of my commitment to education, professionalism and high ethical standards.”

And her advice to financial

“Clients will be more successful if they are engaged in the advice process and are put in a position where they are able to make informed decisions about their own financial futures.”

– Sunitha Chamala, Strategy Adviser, Elston

advice firms? Chamala says female advisers are being increasingly sought after, and firms should adapt their business models to cater to them.

“The advice that I would give to financial advice firms is to understand what drives female

advisers and cater to those needs. This will be highly dependent on the individual, but I have found that businesses with a team focus, social atmosphere, flexible working hours and both qualitative and quantitative KPIs have appealed to me in the past.”

Oksana Patron writes that while the ending of grandfathered commissions was touted to destroy the financial advice industry, Money Management ’ s recent online survey shows it is not the ending of grandfathering alone that will see a planner exodus.

THERE HAS BEEN ongoing debate as to what extent the Royal Commission’s final report recommendations, and the end of grandfathered commissions in particular, would change business models for financial planning groups and individual advisers.

Money Management conducted an online survey in the days following the Government’s announcement that it would back the switch-off of grandfathered commissions in 2021 to capture the sentiment of financial planners, and discover their expectations post-Royal Commission.

The respondents, of which 91 per cent were financial planners, were asked to assess to what degree Commissioner Hayne’s final recommendations would impact their businesses and how they expected this decision would translate into their future revenue streams.

According to the survey’s results, only 30 per cent of respondents said that the ending of grandfathered commissions alone would prompt them to leave the advice industry.

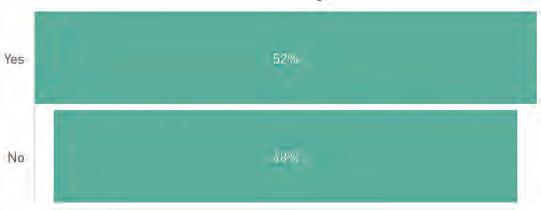

However, planners remained more divided when it came to assessing how a combination of switching off grandfathered commissions and the new Financial Adviser Standards and Ethics Authority (FASEA) education regime would affect their business decisions. In this case, the survey found that more than half of respondents (52 per cent) admitted that the combination of these two factors might see them leave the industry while, for the rest, an exodus remained still highly unlikely.

Money Management also asked its readers to what degree their businesses’ yearly turnover might

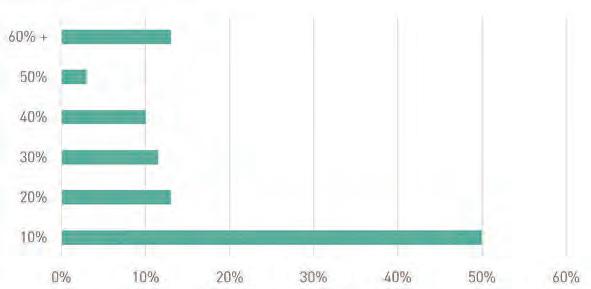

be affected by the end of grandfathering. The results showed that for half of them the end of grandfathering would remain insignificant and impact less than 10 per cent of their yearly turnover.

However, around 13 per cent of those surveyed admitted that scrapping grandfathered commissions would affect more than 60 per cent of their yearly turnover and another 13 per cent said that such a decision would impact around 20 per cent of their revenue streams.

According to another 11.5 per cent of respondents only 30 per cent of their annual turnover would be hit, with a further 10 per cent of respondents saying that such a decision would translate into 40 per cent of their turnover being hit by these recommendations.

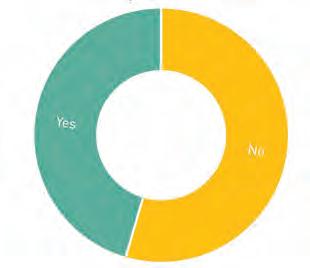

Additionally, the survey found that 45.5 per cent of respondents believed that the proposed 2021 end-date for grandfathering would erode their position on buyer of last resort.

The respondents also provided Money Management with a number of indications regarding where their future major revenue sources might be coming from.

The study confirmed that the end of grandfathered commissions would see planners bracing for flat fee-for-service, with some life/risk commissions as their main new remuneration stream after 2021.

At the same time, planners said they did not place high hopes on asset-based fees and did not expect these would be their dominant revenue streams under the new regulatory regime.

The study also reiterated Money Management ’s earlier findings that the main driver for the majority of planners who considered departing the industry was the new FASEA regime.

Chart 1: Proportion of planners who would leave the industry due to the end of grandfathered commissions

Chart 2: Proportion of planners who would leave the industry due to the end of grandfathered commissions and new FASEA regime

Chart 3: What percentage of your yearly turnover would be hit by the end of grandfathering?

Chart 4: Will the proposed 2021 end-date for grandfathering erode your position on BOLR?

Source: Money Management

Mike Taylor writes that the latest recalculation of the FE Crowns has reinforced the relative success of growth strategies and global allocations amid recent volatility, but that the pendulum may be ready to swing back towards value.

DIVERSIFICATION HAS BEEN the name of the game for those fund managers who have shone through in the latest FE Crowns recalculation.

With the past six months having been a period of volatility coupled with some significant geopolitical uncertainty, strategies which encompassed diversity in terms of both geography and stock selection were those which shone in the period with the Wingate Spectrum Fund and the Bell Global Emerging Companies Fund being two exemplars.

Sitting within the Australian Unity product suite, the Wingate Spectrum fund moved up from two crowns to five crowns based on having delivered in large part on its objective of achieving strong returns, regardless of the performance of global sharemarkets.

The Bell Global Emerging Companies fund also underscored the value of a diversified approach in volatile times, moving up from one crown to five crowns. Similarly, the Dimensional Global Core Equity Trust was rewarded with a similar lift from two crowns to five. While the Crown recalculation

has served to validate growthfocused strategies bringing some relative new-comers to the fore, it has also reinforced that some of the more notable fund managers such as Fidelity, Magellan and Platinum have maintained rather than exceeded their objectives.

By comparison, funds with a strong Australian equities focus were seen to struggle, particularly those with a small-to-mid-cap focus.

Commenting on the situation, independent analyst, Stephen van Eyk said the recalculation of the crowns had served to underscore the generally positive story with respect to growth strategies over the past five years, and particularly those which had maintained a selective focus on technology stocks.

He said those managers who had astutely invested in particular technology stocks had done particularly well while the Crown recalculation had also reflected the rewards which had been driven by those managers who had pursued global exposures and who had also benefited from movements in the Australian dollar by remaining unhedged.

However, van Eyk said that while the crowns had definitely reflected the degree to which growth strategies had outperformed value strategies over the period, this might not continue to be the case as markets moved further into 2019.

“Looking ahead, there is evidence to suggest that conditions in 2019 may suit value managers,” he said.

FE Australia’s head of data, Australia and New Zealand, Stuart Alsop agreed with van Eyk’s analysis, adding that the funds that performed best over the past six

months were those that most effectively navigated downside risk.

He said it was a case of which strategies were best suited to the environment of increased volatility in terms of their risk/return metrics.

Alsop said that while there had been a lot of commentary and speculation about how markets would play out in 2019, the FE Crown Ratings reflected the reality of what had occurred over the previous six months.

“They therefore represent a solid foundation upon which to build forecasts,” he said.

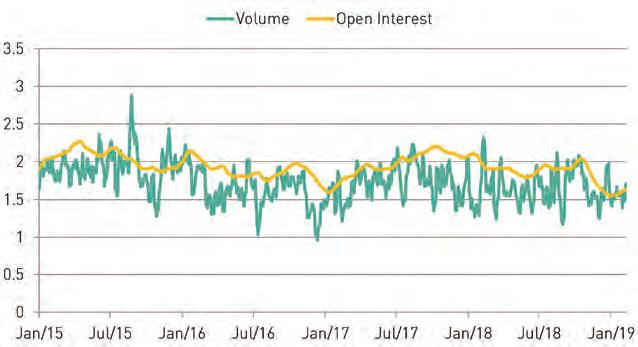

The Australian market felt the after effects of the Royal Commission and property price slump, while global markets battled against a looming US-China trade war. Anastasia Santoreneos writes that this year’s FE Crown rating recalculation reflects a rocky year for global and local economies.

THIS LATEST RECALCULATION of the FE Crown ratings saw Australian equities take a ratings hit while their global peers soared.

Just nine Aussie broad cap funds received five crowns, which is a significant drop from the 26 five-crown funds in the September calculation, with Macquiare Investment Management, SG Hiscock &

Company and Legg Mason still proving to be stalwarts in the sector.

What could have caused this drop, according to AMP economist, Shane Oliver, is a tough Q4 last year, a toll on sentiment following the Royal Commission, the slump in property prices and the flow on of that to retail stocks – specifically banks.

Wealth Within economist Dale Gillham directly attributed the fall in our market to the poor performance of just a handful of the biggest companies in the market, being the big four banks and Telstra.

The US-China trade war and worries about the US Federal Reserve similarly caused some commotion in the global market, but Oliver said global equities didn’t

struggle as much as those on home soil.

“The pressure probably wasn’t as intense [on global markets] depending on where you were looking at,” said Oliver. “Global equities also came down in value through the last six months or so though, which reflected the worries

Continued from page 16

of the global economy at the time.”

But to some degree, according to Oliver, having money overseas wasn’t necessarily a bad idea as the Aussie dollar fell at the same time.

“Global equity funds didn’t do as badly as Australian equity funds because the Australian dollar fell in value, which boosted the value of your offshore investment,” he said.

The February recalculation of the Crown ratings has indeed reflected this sentiment, with 25 global equity funds receiving five crowns as opposed to just six at the last calculation.

Colonial First State stood out among the managers, with four of its funds receiving a fivecrown rating, while two Macquarie funds also achieved

five crowns. Magellan’s Global fund received a five-crown rating, up from three crowns at the last calculation, and Vanguard’s Global Minimum Volatility fund received a five crowns at its first ever rating.

It was tough for the economists to say which investment style suited the market more and which missed the mark, but Oliver suggested the market probably wasn’t that supportive of value.

“A lot of the strength earlier on was in growth-orientated stocks, particularly globally, with tech stocks doing very well, and while that did get hit when the

market came down, cyclicals got hit harder,” he said.

And, given cyclicals tend to dominate in value styles, Oliver deduced the while the environment wasn’t particularly positive for either side, it tended to work against value more than it did against growth.

He predicts the global economy is likely to stabilise as economic policy moves in a more dovish and supportive direction, which would see shares do a lot better across the board.

“That should benefit shares generally, and within that context I think value shares will probably do the best,” he said. “The cyclicals, as confidence returns that the world’s not going into recession and growth stocks take a back seat, will rebound.”

He also expects emerging markets to do quite well should the trade war find a resolution, as that would see Chinese growth stabilise and support the asset class.

Locally, Gillham said materials, mining, energy, healthcare, consumer staples and utilities look good in 2019, but investors should exercise caution around financials given there’s still some uncertainty with the banks.

“If the big miners including BHP, RIO, FMG and the banks move up together, this will push the All Ordinaries Index up through its previous all-time high in2007 and in doing so create a bullish sentiment that will broadly lift other sectors in the market,” said Gillham.

A focus on global equities and fundamental stock selection were common themes amongst the seven funds to receive a stellar five FE Crowns on their inaugural rating, Hannah Wootton finds.

IT CAN BE difficult to get off to a strong start in the competitive landscape of funds management, but seven funds have managed to do just that by receiving five Crowns on their first FE Crown calculation.

AtlasTrend’s Online Shopping Spree and Big Data Big funds, Vanguard’s Managed Payout and Global Minimum Volatility, and the Montgomery Global, Nanuk New World, and Zurich Investments Concentrated Global Growth funds all achieved this honour. They each only hit three years of investment history in the last six months, meaning they didn’t qualify for a rating at last August’s determinations.

While these funds varied in size and manager, a common theme, unsurprisingly given the asset class’ strength before last quarter’s struggles, was a focus on global equities.

Six of the seven funds were global equities offerings and the exception, the Vanguard Managed Payout fund, still sourced 48.06 per cent of its assets from the sector. Its

next two largest asset weightings, of 25.06 per cent in global fixed interest and 14.9 per cent in Asia Pacific equities, kept with the international theme.

The decision to go global was key to AtlasTrend’s success, with founder and head of investments, Kevin Hua saying that he and his fellow two founders, Jade Ong and Kent Kwan, saw a “real gap in the market as Australia has an understandable local bias”.

When you consider what their two five Crown funds invest in (the names Big Data Big and Online Shopping Spree are selfexplanatory), looking internationally was especially key to their strong returns.

“It’s overseas that has the best companies for some big, long-term structural trends, such as data and e-commerce,” Hua said, pointing to Amazon as an example. “They are bigger and better companies [than domestic options] … and are global businesses that are global leaders.”

For both AtlasTrend and Vanguard, who had the equal most

funds to earn inaugural five Crown ratings, a fundamental approach to stock selection was unsurprisingly key to their success.

“Our QEG [Vanguard’s Quantitative Equity Group] manages there two funds … they are passionate researchers who rigorously test and scrutinise ideas to ensure that only the best ones make it into their models and investment processes,” Vanguard’s head of investments, Asia-Pacific, Daniel Reyes, told Money Management

“QEG finds that by focusing on investment themes designed for the long-term investor they can systematically capture inefficiencies or target exposures in the market that can add value to clients’ portfolios.”

Hua said his team also have “very much a fundamental approach in stock selection”.

“We first pick thematics with a long-term view, seeking out structural trends that we think will last 10, 15 years or longer,” he said.

From there, they distil a large

investment universe down based on quality, valuation and sustainable growth estimates, before intensely researching each company. As a small fund manager, this usually means dialling into market updates, for example, rather than meeting with companies as large as Amazon. Both fund managers also watch risk factors closely, unsurprisingly considering their five Crown ratings and the fact that the Crown Ratings methodology considers risk.

The Vanguard Managed Payout fund, for example, seeks to make monthly cash distributions, and to keep these and invested capital apace with inflation over the longterm, Reyes says.

The manager’s Global Minimum Volatility fund minimises volatility through quantitative modelling that both identifies shares with low expected volatility and shares that are expected to have low correlations with each other.

Hua too, keeps an eye on both macro and micro risks: “A lot of it can be noise, but one has to be pragmatic as well,” he said.

Technology can provide a helping hand for financial advice businesses adjusting to the post-Royal Commission industry landscape, Oksana Patron finds.

THE RECENT REVELATIONS from the Royal Commission’s final report have intensified pressure on the financial services industry, even though the sector had been already under the spotlight from regulators, and they’ve made it clear that it is now more important than ever to help financial advisers focus on what really matters for their businesses and clients.

Technology comes as a crucial part of this process and a lot will depend on how well it will handle accommodating planners’ redefined expectations and needs in these unique conditions, and how well it will underpin efforts to free up their time.

Tech providers will also need to focus on finding new ways to help planners address higher regulatory compliance requirements, enhance their usage of technology and data to help them meet their clients’ objective, and assist with the integration of information, the experts said.

In addition, tech will also need to prove its adequacy for advisers through a wider range of offerings with regards to education technology (edutech) solutions which, in turn, will be expected to support planners and their efforts to meet new professional accreditation obligations, imposed on the industry by the Financial Adviser Standards and Ethics Authority (FASEA), such as continuing professional development (CPD) requirements.

The recent findings from the Royal Commission suggested that a lack of respective regulatory compliance

technology might seriously threaten the existence of many licensees and advisers, Samantha Clarke, a chief executive of tech start-up Advice RegTech, said.

According to Clarke, who won the Innovator of the Year Award at the 2018 Money Management Women in Financial Services Awards, the core of a professional advice practice these days revolves around regulatory compliance technology, given a number of licensees going out of business or those struggling to comply with the new laws.

“The Royal Commission has made it clear that regulatory technology is an absolute must have for every licensee and advisers. If they don’t have regulatory compliance technology then they are putting their business at risk,” Clarke said.

“What we are hearing is, the time for them to develop their statements of advice has tripled or quadrupled so it means practically that customers aren’t getting the advice issued to them fast enough and that’s impacting their customer experience.”

Clarke stressed that even though the statements of advice (SOAs) are rarely read, it is the compliance requirement that needs to be 100 per cent correct, and this should be viewed in light of the recent report from the Australian Securities and Investments Commission (ASIC), according to which, more than 70 per cent of advice was considered non-compliant.

“So there is the huge opportunity to improve that really practical side of developing and checking the

statements of advice,” she said.

“What happened in the last few months is everybody is trying to do that, and we are trying to do that in a traditional way, and the traditional way is taking weeks and sometimes months to get the advice issues to consumers. So that is not a good outcome for consumers and for the industry.”

According to Clarke, some organizations are also trying to tackle this problem by “throwing more bodies at the compliance tasks”. However, such an approach would only drive up costs of business and would not be viable into the future.

“In the short-term, licensees would be spending a significant amount of money on extra costs on human reviewers, but in the medium to longer term, regulatory compliance technology can help scale the efforts of those human compliance reviewers and make reviews more viable from the business perspective,” Clarke added.

One thing is certain, the industry has come to a critical point, and both licensees and advisers should reflect on future proofing their businesses. But it is not all black and white.

According to Advice RegTech, the progressive tech savvy licensees have pre-empted a lot of the Royal Commission findings even before the interim report, with a number of advisers already identifying new opportunities, in particular in the area of regulatory technology (regtech), where technology could help them in the most effective way future proof their businesses.

“The key is finding fit for purpose solutions that enable greater efficiency and effectiveness in meeting those regulatory compliance requirements,” Clarke stressed.

However, according to Jacqui Henderson, chief executive of Advice Intelligence, traditional financial planning software no doubt failed licensees, financial

advisers and consumers, and the “old world” technology that existed within the financial planning industry was not designed for today’s regulatory environment or consumer experience.

Firstly, current technology failed to provide pre-emptive controls to monitor the quality of advice upstream of the advice process.

“Without quality assurance, there is a serious risk that sits with AFSL [Australian Financial Services Licence] holders as they can only be reactive, not proactive, in the delivery of quality advice of scale,” she said.

Secondly, ongoing servicing and transparent fee disclosure for consumers was powered mainly by archaic systems and there was a massive need, according to Henderson, to move financial planning into a world that was similar to that of net-banking.

Thirdly, technology did not directly link financial advice strategies and investments back to the client’s goals and provide ongoing tracking of these goals. “Therefore, the existing technology is simply not meeting the requirements of our modern advice sector and this needs to change,” she said.

However, on a more positive note, technology can transform financial advice into an engaging and client facing experience.

“Consumers want advice that directly relates to their own individual dreams and life aspirations – they want to feel like they are part of a collaborative process that is being done ‘with them’ not ‘to them’,” said Henderson. “They want to be educated, they want to feel empowered and they want a full picture so they can control the things they need to control, like their goals and cashflow.”

More importantly, consumers should understand that the advice they paid for and paper-based SoAs that were full of industry jargon were not doing them any favours, according to Advice Intelligence’s CEO.

On the other hand, according to Troy MacMillan, a chief executive at

Perth-based financial advisory The Wealth Designers (TWD) Australia, not all is lost when it comes to technology and advisers.

“Core to the success of any advisory firm is how much they focus on the delivery of value – that is, what the client actually values,” he said. “Technology isn’t TWD’s differentiator, it’s an enabler.”

It is expected that smart technology should free up time for firms like TWD to otherwise spend it face-to-face directly with clients for up to 60 per cent of working weeks.

“These levels of face-to-face time can’t be made without technology and are in facet key measures of the success of good technology implementations for firms like TWD,” MacMillan said.

When asked if there were any particular tech solutions that were critical from advisers’ perspective, MacMillan said: “Technology is like the electricity grid – you quite simply have to be on it, as we all need it.”

“My thoughts are that technology will replace many old financial planning models that are becoming commoditized but those particular firms are not in the principal advisory space like TWD.

“We strongly believe that technology is not the differentiator, it’s critically important to drive efficiencies, but not the reason we are in business.”

At the same time, advisers would need more resilient solutions and tools when it comes to customer relationship management (CRM), portfolio and project management, financial planning software, cloud and information management software, data analysis tools and out-sourced service offerings that enhance head office operations.

Furthermore, according to him, there were four key areas that were of particular importance to the adviser firms, including error-free and time-relevant information, project management software, and better presentation support and SEO software. In case of TWD, the requirements for project management software could be broken down into client, project and strategic management, which all were its core skills.

“We have found that old CRM’s have only ever provided client task management, but have lacked the integration required to quickly understand a firm’s live capacity which we call capacity planning’.”

Following this, advisers and licensees continue to feel under a lot of pressure as it was getting harder and more costly to provide advice to their clients, in the opinion of Advice Intelligence.

Therefore, compliance should be designed more as a ‘co-responsibility’ held by both the consumer and advisers in that way that advisers must tailor advice around the conversations they had with their individual clients in relations to their goals.

“In transforming financial planning into ‘real-time’, advisers can model future scenarios and demonstrate how different decisions impact their clients’ lives, as part of an advice ‘co-creation’ process,” Henderson said.

“By placing the client’s goals and life aspirations at the heart of the process, advice becomes more meaningful to them, encouraging lifelong engagement.”

At the same time, enhancing advisers’ soft skills around the human psychology aspects of financial advice and understanding their clients better is vital to providing a better outcome for clients as well as improving education standards across the board, according to Henderson.

“Financial advice is about helping clients to achieve their life aspirations and goals. It is about understanding then as a human being, their biases, their behavior, their money language, what motivates them, what key financial challenges they’ve faced,” she said.

“The advice community needs more focus on the conversational piece, asking the right questions and having more education around the human element of financial advice.”

Henderson stressed the shift, though, needed to be accompanied by technology that fully supported the human conversation.

There are still investment opportunities in Chinese equities this year, Jonathan Wu writes, and looking at the nation’s instant noodle sales can help you understand why.

THERE IS NO doubt in anyone’s mind as to what part of the investment cycle we are in – the late part. Albeit with bouts of volatility here and there since 2009, overall, it’s been a pretty good outcome for investors in risk assets.

But where to from here given we have a rising (albeit slower) rate environment in the US, and a slowing local economy started by sharp corrections in house prices? And what will China’s role be in this environment?

The first hit we had to global confidence was in the first week of January with Apple declaring a revenue warning over its most

popular offering – the iPhone, citing a significant proportion was due to a drop in sales in China. This shook the world into the belief that we are facing the beginning of the end.

When you look deeper into the situation though, one must realise that Apple is facing tougher competition in China from the likes of Huawei and Xiaomi rather than simply demand falling off. Again – you must read into context more than simply the headline. There is always a cause and effect below the surface.

As at the time of writing, China and the US are continuing trade

talks to try to find a compromise to prevent protectionism rearing its ugly head reversing almost 100 years of globalisation and the development of free trade.

Sooner or later, when the real economy (seen via corporate earnings) weakens due to the impacts of the tariffs, leaders will be more motivated to act. One case in point is that Trump continues to use the S&P500 as his barometer of success as President and Commander in Chief. If the S&P falls in a big way, Trump will be motivated to cut a deal with China as he would have other fights he needs to take on domestically (for

example, government shutdowns and wall building).

Now to understand China’s role in 2019 and beyond in relation to the world, one must look back at what it did during the Global Financial Crisis.

China launched an unprecedented level of stimulus (the world’s largest in recorded history) in 2008/9 to the tune of $4tr RMB (A$823bn). This, in simple terms, saved the world from collapse as it was looking very dark for a period while the world’s liquidity dissipated and no one had the ammunition to stimulate.

While China saved the world, their actions caused some unintended consequences via the build-up of excesses within the economy, such as over supply from steel mills, overbuilt infrastructure, and shadow banking. So, this time round, China has learnt its lessons and will stimulate gradually.

While the current market correction reflects some of what we saw during the correction seen in 2015/16, where many global investors ‘knew’ the Chinese economy was going to succumb to a hard landing (which never eventuated), the economy is under far less pressure.

The market didn’t fall quite as dramatically and as such also didn’t trigger as much concern about the financial system state of health. The renminbi is also under less pressure and foreign reserves are also above the $3tr USD figure. So, while the Chinese government is stimulating through increased liquidity injections and cutting of the RRR rate, it is nowhere near what it was in previous years.

Whenever the next major global recession occurs, China will not be the one to bail the world out, nor do they have any incentive to.

So, in this environment and being in the late part of the

investment cycle, are there still investment opportunities in Greater China equities? Yes, there are.

What the last 12 months has shown us is that there are many quality companies that have emerged due to the correction. We believe there is only one way of achieving investment success, and that is patience and time in market. If you asked us 12 months ago what we thought about valuations, we said that while the market is cheap, the companies we want to invest in are not within our buying range based on valuation metrics. Now they are.

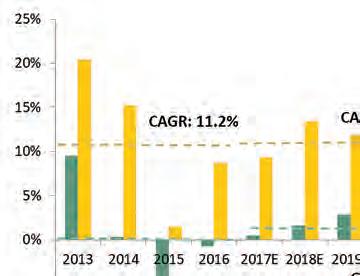

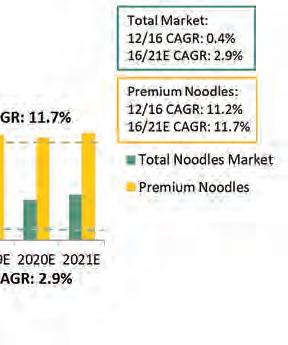

The instant noodle market, for which there will continue to be strong demand no matter the state of the investment cycle, is one good example. Instant noodles are considered a staple to the Asian diet and no matter which part of the income or wealth spectrum you belong to, they’re something that you will consume as a comfort food or simply out of convenience. Think of it like the humble meat pie or sausage roll here in Australia.

While the overall market is reasonably mature with CAGR in China of under one per cent in the last six to seven years, the premium market, which is defined by noodles costing more than five RMB ($0.80 AUD) per pack at the retail level, has been growing at

double digit levels over the same timeframe (11.5 per cent CAGR since 2012).

At the same time, one must also take into context the composition of the instant noodle market. As at the end of 2017, it was still 90 per cent mass market (< five RMB per packet). So, ultimately this is a consumption upgrade story (alongside many others in China). As the middleclass population grows, they are demanding higher quality goods.

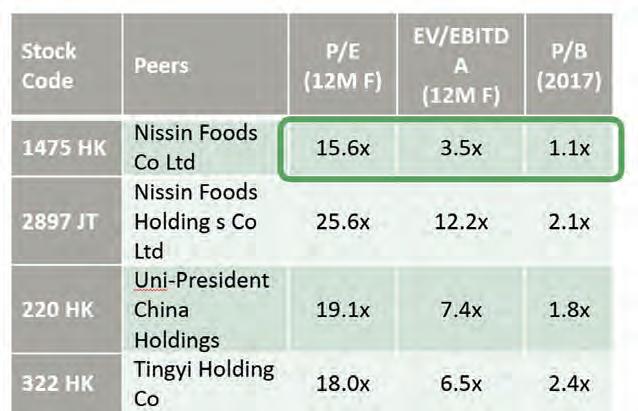

This is where a company like Nissan Foods comes into view. Nissan has its history back in Japan with its flagship products well recognised in both Hong Kong and Southern China

After spinning off from its Japanese parent in 2017, management have been focusing on building their China distribution networks and now they are the second largest premium brand in China with 20 per cent of total market share. In Hong Kong, they already have a 65 per cent market share which serves as a successful case study as to how high penetration can get with a higher median income level population set.

The current valuation level is very attractive (40 per cent and 15

per cent discount to its parent and peers respectively on a P/E basis), which affords us what we refer to as a ‘larger margin of safety’ no matter what short term blips were to hit market sentiment. So, just as in this example, no matter which part of the investment cycle we are in, opportunities are there for active investors who do more underlying fundamental research to seek out stocks which are unloved by the market. While you can never time the market, you do know when markets are relatively more or less attractive to enter for the long-term.

Simon Ho writes that sensible investors will be looking to own some sort of protection strategy this year, as the risk of a period of high volatility grows stronger.

that precipitate extreme volatility are in place in global markets, and investors should take steps to protect their portfolios.

Despite periods of episodic volatility over the past few years, it has actually been one of the least volatile times, for realised volatility, compared with time frames over the past 50 years.