Guide to Retirement Income

Principal Sponsor

Despite the nay-sayers, Australia has developed a superannuation system which is the envy of many other developed economies but, in many respects, it remains a work in progress especially with respect to post-retirement.

While the superannuation guarantee (SG) regime has served to build Australian superannuation assets to in excess of $3 trillion, it is the decumulation phase which remains a work in progress simply because successive Governments have failed to deliver tax/policy frameworks which are both consistent and conducive.

It is in this environment that over the past decade there has been much talk around the development of post-retirement products in the context of Comprehensive Income Products for Retirement (CIPRs) but, to date, precious few outcomes capable of inspiring companies or superannuation funds to deliver new products.

And just to complicate the issue, and notwithstanding the discussion around the development of a retirement income covenant, the Treasurer, Josh Frydenberg, has signalled a retirement income system review without, as yet, announcing the terms of reference.

In this Guide to Retirement Income, Money Management seeks to traverse the history of the retirement incomes debate in Australia while drawing upon the views of the major stakeholders on what might eventually evolve.

What is clear from this guide is that many companies operating in the Australian financial services industry are ready, willing and able to deliver new products and services to better equip Australians for their retirements but are reluctant to do so until they fully understand the unfolding regulatory landscape.

That is why whatever the Government has in mind to be achieved from its review should be revealed to the industry as soon as possible.

Mike Taylor Managing Editor

Launched 32 years ago, Money Management has firmly established itself as the leading source of news and analysis for Australia’s financial services sector.

In this time, Money Management has rapidly evolved from a B2B newspaper into a respected provider of accredited education and training, research, professional support and advocacy as well as thought leadership in the financial services space.

While it remains the most-read print and online publication by financial planners in Australia and is widely recognised as a leading advocate for this profession, Money Management's growing audience is a diverse one that also includes fund managers, accountants, risk advisers and superannuation fund trustees.

Money Management is also the clear publication of choice for finance institutions – both domestic and international – seeking to connect with the high-earning and well-educated professionals working in Australia’s financial services sector.

FE Money Management Pty Ltd Level 10 4 Martin Place, Sydney, 2000

Managing Director: Mika-John Southworth Tel: 0455 553 775 mika-john.southworth @moneymanagement.com.au

Managing Editor/Editorial Director: Mike Taylor Tel: 0438 789 214 mike.taylor@moneymanagement.com.au

Associate Editor - Research: Oksana Patron Tel: 0439 137 814 oksana.patron@moneymanagement.com.au

News Editor: Jassmyn Goh Tel: 0438 957 266 jassmyn.goh@moneymanagement.com.au

Senior Journalist: Laura Dew Tel: 0438 836 560 laura.dew@moneymanagement.com.au

Marketing Manager: Odette de Souza Tel: 0404 439 000 odette.desouza@financialexpress.net

ADVERTISING

Sales Director: Craig Pecar Tel: 0438 905 121 craig.pecar@moneymanagement.com.au

Account Manager: Amy Barnett Tel: 0438 879 685 amy.barnett@financialexpress.net

Account Manager: Amelia King Tel: 0407 702 765 amelia.king@financialexpress.net

PRODUCTION

FE is a financial information and communications company founded in the UK in 1996.

It has offices in Australia, India, Hong Kong, and the Czech Republic. It provides data, software, research, and ratings to help asset managers and financial advisers make better investment decisions.

ACN 618 558 295

www.financialexpress.net

© Copyright FE Money Management Pty Ltd, 2019

Graphic Design: Henry Blazhevskyi

Subscription enquiries: www.moneymanagement.com.au/ subscriptions

Money Management is printed by Bluestar Print, Silverwater NSW. Published fortnightly.

All Money Management material is copyright. Reproduction in whole or in part is not allowed without written permission from the editor. © 2019. Supplied images © 2019 iStock by Getty Images. Opinions expressed in Money Management are not necessarily those of Money Management or FE Money Management Pty Ltd.

Mike Taylor writes that in the half-decade of discussion around retirement incomes policy there has been plenty of talk, multiple proposals but very little real progress.

It has now been more than half a decade since the Government initiated the debate around Comprehensive Income Products for Retirement (CIPRs) but with the Treasurer, Josh Frydenberg, having flagged a review of Australia’s retirement income system, do not hold your breath waiting for a definitive outcome Frydenberg flagged the review of Australia’s retirement income system in the

lead-up to the 18 May Federal Election but, at the time of writing in late September, he had still not delivered on the terms of reference for the inquiry.

But it seems almost inevitable that any review of the retirement income system must traverse the issue of CIPRs which, as has been

Continued on page 8

Continued from page 7

written elsewhere in the guide, explains why major groups such as Willis Towers Watson have no great expectation of new products being brought to market any time soon.

However, it is a measure of just how long the issue of CIPRs has been in the market that it was early 2017 that the then Minister for Revenue and Financial Services, Kelly O’Dwyer released draft superannuation income stream regulations for public consultation.

In circumstances where the tax settings around annuities had always been the sticking point for the development of retirement income products, the former minister’s words were strongly welcomed by the superannuation industry.

“Superannuation funds and life insurance companies will receive a tax exemption on income from assets supporting these new income stream products provided they are currently payable or, in the case of deferred products, held for an individual that has reached retirement,” O’Dwyer’s March 2017 statement said.

“These new rules will remove taxation barriers to the development of new products that will provide greater flexibility in the design of income stream products to give more choice to consumers, while ensuring income is provided throughout retirement,” she said.

“The development of these new products is a precursor to the development of Comprehensive Income Stream Products for Retirement, or CIPRs.”

It was notable that allied to the 2018 Federal Budget, O’Dwyer then released the framework of a retirement income covenant

stating it would “form the cornerstone of the new framework”.

“It will be added to the Superannuation Industry (Supervision) Act 1993 , which will elevate the consideration of members’ retirement income needs to sit alongside the other fundamental obligations of trustees, such as the investment, risk management and insurance needs of their members,” she said.

“To fulfil the overarching purpose of superannuation, it is essential that trustees develop a retirement income strategy and consider the retirement income needs of their members,” O’Dwyer said.

The Government announcement said the framework would also include supporting regulations that obliged trustees to offer their members a comprehensive income product for retirement and to guide and support members to select the right retirement solution.

“The Government is prioritising the retirement income covenant and supporting regulations as the first phase of the retirement income framework. The disclosure metrics, also announced in the Budget, are another crucial part of the framework to better inform consumers and aid comparison of retirement products,” the minister’s statement said.

The problem was, of course, that while the Government provided the superannuation industry with the opportunity to provide submissions on the proposed covenant principles by 15 June, last year. More than a year and one Federal Election later, there has been no definitive outcome and the issue has again become clouded by Frydenberg’s pre-election review announcement.

But what became clear in the various submissions filed with Treasury around the retirement incomes covenant and the development of CIPRs is that the superannuation industry wanted more detail than the Government had thus far provided.

The reservations of the superannuation industry were probably best reflected in the views expressed by the Association of Superannuation Funds of Australia (ASFA) which urged both a lengthy transition period and a specific legislative regime around the requirement for CIPRs.

As well, the ASFA submission suggested that an industry working group had concluded that, perhaps, CIPRs were not, of themselves, the ultimate answer.

“It was observed that there are activities that could improve income in retirement, other than offering longevity risk products, including:

• Providing projections of income on member statements, to start effecting the shift in thinking from ‘accumulation of a lump sum’ to ‘entitlement to an income stream’;

• Improving financial literacy and educating Australians about superannuation, including the benefits of compounding returns and other benefits with respect to investing for retirement. This could extend to inclusion in school curriculums, with reinforcement in senior school as young Australians enter the workforce for the first time and receive contributions to superannuation;

• Improving the provision of information and advice to members, especially in the form of projections, guidance and information as to their level of superannuation as compared against default or selected benchmarks, as an engagement strategy; and

• Provide more guidance and advice at the time of, and after, retirement, including how to manage the various investment risks and how to invest, and drawdown, appropriately through retirement.”

Indeed, the ASFA submission suggested that CIPRs should be an opt-in exercise for superannuation fund members.

Continued on page 10

Continued from page 9

For its part the SMSF Association was more bullish about the concept of a retirement covenant declaring that the “superannuation system has been too accumulation phase focussed and the retirement covenant will serve as an important instrument to correct this”.

However, the SMSF Association was less enamoured of self-managed super funds (SMSFs) being required to develop CIPRs.

“We believe the proposed application of the retirement covenant for SMSFs, which only requires them to consider the first covenant principle of developing a retirement income strategy, is appropriate,” it said. “This is appropriate as SMSF members operate as the trustees of their fund and this close connection between fund and member does not necessitate needs for enhanced engagement and developing CIPRs.”

The Association of Financial Advisers (AFA) was even more clear-cut in its view of CIPRs, arguing that such products would not be for everyone.

“Whilst we do not disagree with the stated objectives of a CIPR, we question the practicality of achieving a broadly constant income over time. There will always be transition points, particularly where a deferred lifetime annuity might kick in and where an account-based pension (ABP) is declining rapidly. We also question whether the charts in the Appendix actually demonstrate that such an outcome is achieved by what is proposed. This seems inconsistent,” the AFA submission said.

“We also make the point that spending

may naturally decline over time in retirement as people are less capable of overseas and domestic travel and are less likely to spend money on entertainment. This will be partly offset by an increase in health costs. Nonetheless, the need for income in retirement is unlikely to be constant over the course of an extended period of retirement.

“Whilst it is suggested that the use of a deferred lifetime annuity will give members greater confidence to spend at a higher rate whilst in retirement, we expect that this would simply add an additional stage point and since members will have less money in their ABP, they will still have concern about whether their ABP assets will last until their DLA [deferred lifetime annuities] commences.”

It is our view that for clients who have a high risk appetite and significant assets, a 100% allocation to an account-based pension may be the most appropriate outcome. Given that the ABP will typically be invested in a higher proportion of growth assets, as compared to the underlying investment allocation for annuities, they should be expected to overperform over the longer term. Thus, where there are significant assets available to invest, the investment return should be higher in an account-based pension, and there should be little risk of assets running out.”

So what has changed since the Treasury closed off the receipt of submissions to the Retirement Income Covenant Position Paper and the Treasurer’s proposed retirement income inquiry?

Very little, unless the Treasurer has something in mind for the 2020 Budget.

So what has changed since the Treasury closed off the receipt of submissions to the Retirement Income Covenant Position Paper and the Treasurer’s proposed retirement income inquiry?

As advisers, you know no two clients are the same. It takes in-depth conversations to fully understand each client’s needs and what a successful retirement looks like to them.

Te chnical and product knowledge are valuable skills for any adviser, including the ability to navigate the more complex areas of Australia’s retirement system. The ability to simply demonstrate this knowledge, while offering solutions which help a client achieve their retirement goals within the system, are central to an adviser’s value proposition.

AMP developed the Retirement Modelling Tool to help you have these conversations with clients. The modelling incorporates the risk profiles and circumstances of clients to produce simple visual timelines which summarises available retirement structures and income streams using a combination of account-based pension, annuity and Centrelink payments.

Unlock hundreds of scenarios in seconds

The tool instantly runs through 900 scenarios and will show the ones that meet the client’s

What you need to know

income and withdrawal needs as well as their risk profile. Analysis provided by the tool includes the client’s retirement income, assets and Centrelink payments over 15 or 25 years. Further analysis is available for a specific scenario with the ability to run 2,000 scenarios projecting different returns taking into account market volatility and sequencing risk. It can also help structure the client’s investments in their account-based pension to achieve their goals.

Simple visual displays, including charts and timelines, provide advisers with a clear picture of the strategies and comparative outcomes. Advisers can then use their knowledge of the client’s view on longevity, their health, and inflation estimates to choose the scenario the most suits their needs.

If you’d like to know more about AMP’s Retirement Modelling Tool, contact AMP on 1800 667 841.

AMP's Retirement Modelling Tool is only accessible to financial advisers and is not available to retail clients. Any advice in this advertisement is general only and is provided by NMMT Limited ABN 42 058 835 573, AFSL 234653 (NMMT), a member of the AMP group. Individuals should consider the MyNorth Super and Pension PDS available at northonline.com.au and their own circumstances before deciding what's right for them. The issuer of MyNorth Pension product is N.M. Superannuation Pty Limited ABN 31 008 428 322, AFSL 234654, a member of the AMP group. MyNorth is a registered trademark of NMMT. If an individual decides to acquire or vary a financial product or service, NMMT and/or other companies within the AMP group will receive fees and other benefits, which will be a dollar amount or a percentage of either the premium you pay or the value of your investments. Contact AMP on 1800 667 841 for more details.

Experts believe retirement income products need to be flexible, certain, and help retirees with their spending. But it is clear the development of these products continues to be stifled the longer the government pushes the legislated framework down the priority list, Jassmyn Goh finds.

The development of Comprehensive Income Products for Retirement (CIPRs) seems to be moving at a glacial pace.

Only a few years ago product providers, superannuation funds, and other stakeholders were quickly filling in submissions to the Government’s consultation on the development of a retirement income framework, and product providers such as Challenger were raving on about its CIPR solutions.

Fast forward to 2019, there is still no legislation on a framework for these products, and only some funds have started developing products while others have not started.

CIPRs seem like they’ve been put on the back-burner thanks to distractions such as new Age Pension means testing rules introduced on 1 July, 2019 – to help the industry develop innovative products to help retirees manage the risk of outliving their income – and the Government looking to introduce the retirement income covenant.

However, this covenant was supposed to be introduced by 1 July, 2019 which included the requirement for trustees to offer CIPR products by 1 July, 2020. As of writing, the government

still has not yet legislated the covenant but has pushed back the CIPR date to 1 July, 2022.

The further the government pushes the framework down the priority list, so does any detail with CIPRs.

Rice Warner chief executive, Andrew Boal, told Money Management that he was not aware that a lot of super funds were proactively working hard to create CIPRs as they were preoccupied with dealing with regulatory requirements.

“Some funds have annuities on their platforms that members can choose but not a lot of work is being done to develop a CIPR that incorporates an annuity into an overall retirement offer,” he said.

“Some funds are looking at altering the investments within their existing accountbased pensions and how that is synchronised with the Age Pension.”

Boal noted half the reason CIPR development was so slow was because it had been put on the back-burner and half because funds

Continued on page 16

Continued from page 15

were waiting for legislation to be passed.

“To some extent there’s an element of ‘wait to see what it looks like in case we have to redo the work’ and so if we’re expecting legislation to come soon then it would be prudent to wait,” he said.

However, Willis Towers Watson head of retirement solutions, Nick Callil, believes there will be a spate of product announcements in the retirement income space by leading funds over the next six to 12 months.

Callil said while government activity was sluggish big funds with resources realise that independent of government retirement income was also a business issue.

As retirees were a growing part of super funds’ membership base they needed to look after these members and protect those assets to maintain scale.

“I would be surprised if most of the leading funds did not announce a product or an intention to create an enhanced product over the next 12 months,” Callil said.

“Retirement is complex and no doubt there is reluctance to take a step forward but when the bigger funds start rolling out products it will create a powerful incentive, or safe zone for others to do the same.”

Without a framework, Callil said funds needed to investigate lenders, look at different retiree cohorts and what sort of products they should be offered. These elements, he said, needed to be addressed by the time the guidelines were released.

Callil noted that funds and product providers needed to think about better spending of accumulated assets in the early stages of retirement and longevity when designing CIPRs.

He said retirees with meaningful balances were being too frugal and not enjoying their savings as retirees were often defaulted to minimum drawdown rules. Retirees often had more money in their account in their 80s than in their 70s and funds needed to find a mechanism to promote better spending. However, funds had to keep in mind that the mechanism needed to allow retirees adequate savings should they live past their life expectancy.

Aberdeen Standard Investments Australian head of retirement and product strategy, Jason Nyilas, said he was concerned that super funds and product providers had not designed enough within retirement income products and the ones available were not similar in approach.

“Some are enterprise based, some are retail based, some may or may not focus on lifetime, and some even include reverse mortgages,” he said.

“There are so many different shapes and sizes it makes it difficult for advisers to understand and select something that best fit their clients’ needs.”

Nyilas said the solutions were not flexible or certain enough for the ‘tsunami’ of people looking to retire over the next decade, given their various circumstances leading to retirement.

“If you combine flexibility and certainty you can achieve a product that is flexible, gives high income, and has features in place to guarantee you income,” Nyilas said.

“That’s not an easy ask for a product provider because it requires a lot of sophistication but it is what the ask is.”

Nyilas noted that an important component of this was affordable advice and said technology would be key.

Agreeing, Boal said retirement income products needed to provide more certainty.

“The products need to meet the needs of a whole lot of people but perform differently for each person,” Boal said.

“One of the things funds need to grapple

with is the role of longevity protection. There is a large sector in the industry that is not convinced that annuities that offer good value for members.

“However, retirees are currently typically underspending in retirement mainly because they’re uncertain on how much money they need and how long they’ll live.

“We need retirement income products that provide more certainty so that retirees have the confidence to spend.”

Boal said deferred lifetime annuities or some other kind of pooled longevity protection would have a lot to offer for retirees,

Continued on page 18

Continued from page 17

particularly for retirees in the middle bracket in terms of assets.

“In that means-tested ground between $300,000 to $800,000 – these are the people that will really benefit in longevity protection,” he said.

“For people with less than $300,000 the Age Pension will provide around 80% of their income and people who have above $800,000 are probably in a better position to manage their own longevity.”

Boal noted that advisers needed to really think about helping retirees with spending safely.

“How much retirees can afford to spend safely – that’s the key question people are looking to get assistance with. Hopefully products will come into the landscape soon that can help support the answering of some of those questions,” he said.

For Callil, advice needed to be focused on the right part of the whole retirement journey which was getting people to understand what their needs were, how to transition to retirement, and tax regimes.

Callil believed there was no need for further tax or social security changes for CIPRs to work or to help take up of the products as the “main planks were in place for these products to be launched”.

Callil referred to the fact that innovative retirement products had the same tax treatment as other products such as annuities, and social security rules had recently been amended – the means test.

“Now we need direction from government to take the lead and no doubt it’s been a long

wait period for CIPRs but funds have realised that it’s time to move,” he said. He said the industry and government needed to look at:

• A retirement income objective that concluded that the retirement provision should be in income form and that capital balances should be spent down over retirement;

• Retirement income estimates that were mandatory for super funds with some sensible limited exceptions at the fund and individual level;

• Careful use of the term ’income’ which could confuse members with the dual meaning of investment earnings and income received from a fund during retirement phase. ‘Drawdown’ or a similar term would be a more appropriate term to refer to amounts paid to retirees in pension phase;

• Well-designed drawdown rules to ensure they were not too conservative and did not promote inappropriately low spending; and

• Better retirement products to allow retirees with meaningful balances to spend their savings more confidently earlier in retirement only if they are sufficiently comfortable that they will not run out of money in advanced old age.

The complexity, Callil said, in retirement was far more than in the accumulation phase and the objective of retirement income needed to look at the whole system rather than just superannuation.

How much retirees can afford to spend safely – that’s the key question people are looking to get assistance with. Hopefully products will come into the landscape soon that can help support the answering of some of those questions.

– Andrew Boal

The investment returns received just before and after retirement can make a big difference to how long retirement savings will last – highlighting the importance of achieving growth with capital protection.

In the investment world, the saying “it’s the long-term that counts” is often used to dispel fears about market timing. That might be true if your client can keep their money invested for the long term. But what if they need to drawdown their money to maintain their lifestyle in retirement? How can they start spending now without worrying about having to adjust their lifestyle later?

The seven or so years before and after retirement are known as the ‘retirement risk zone’. During this time, your client’s savings are at their highest, but it’s also when they’re most vulnerable to market volatility. That’s because there’s less time to recover, and the combination of falling asset prices and capital drawdowns for income compound the impact of a capital loss. These losses in retirement can have a nasty knock-on effect for retirees, potentially resulting in:

• having fewer assets, which makes it harder to recover from those losses

• adjusting lifestyle (spending less) to help assets last longer

• running out of money sooner than expected, even if markets offer higher returns later in retirement.

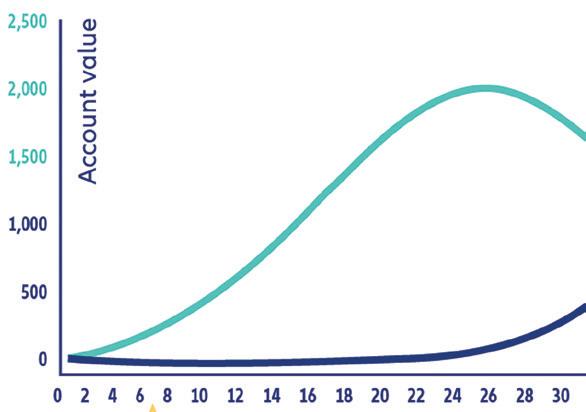

Sequencing risk refers to the order in which returns are achieved from a particular portfolio. How it impacts a portfolio can differ greatly between an accumulation portfolio with no drawdowns versus a retirement portfolio with regular draws down.

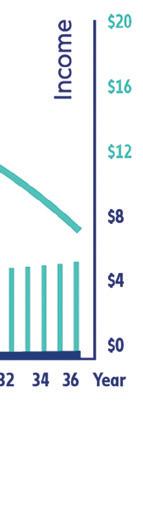

For instance, Chart 1 shows two accumulation portfolios that have the same expected return, and the same volatility of return, with the order of the returns reversed.

Chart 1

As you can see, if a person can keep their money invested for the whole period, the order in which they achieve those returns doesn’t matter as the end result is the same.

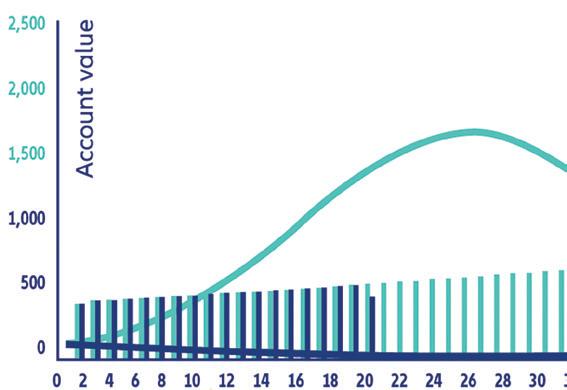

However, when a retiree is drawing money out of their account every year, the order of the returns can have a massive impact on when the retirement portfolio runs to zero, as shown in Chart 2.

One of the retirees runs out of money after 20 years, while the other retiree still has a substantial account balance after 36 years simply because of the sequencing of their returns even though the portfolios had the same risk/return metrics. This dramatic difference highlights

sequencing risks as a significant measure of risk that needs to be addressed in retirement portfolios.

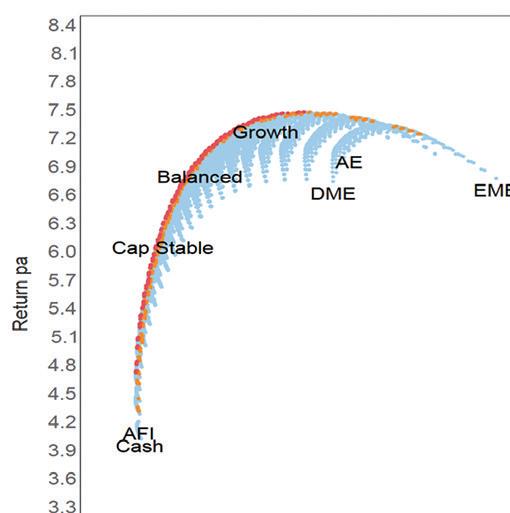

The traditional view is that retirees should have a more conservative portfolio with reduced growth assets in order to lower the risk of capital loss. But when we consider that many people fear of running out of money in retirement, this should change the way we define what risk is for a retiree.

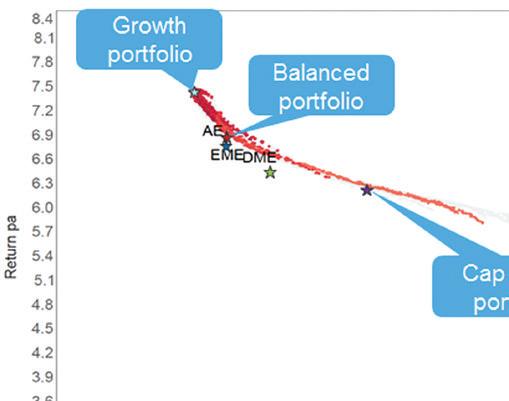

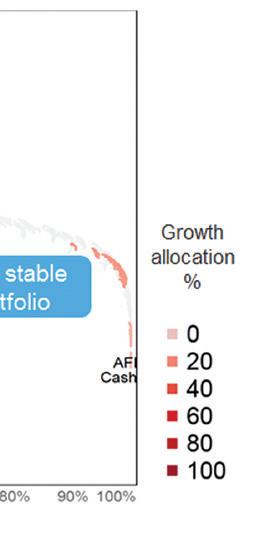

Chart 3 shows the typical efficient frontier, with risk measured by the volatility of returns:

Continued from page 19

As you’d expect, the more growth assets you add to a portfolio, the higher the return expectation and the higher the volatility of returns.

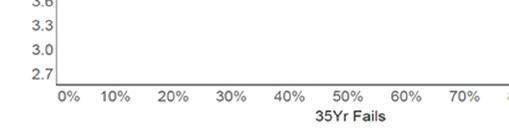

If instead we look at the measure of risk being the number of times that a portfolio will run out of money over a certain period of time, then the chart looks like this:

4

Source: Macquarie Bank

This chart shows a conservative portfolio actually has the highest risk of running out of money, while a growth portfolio is the lowest risk portfolio.

What all this is telling us is that retirees still need growth assets in their portfolio to sustain their income requirements. But they also need the right capital protection strategies in place to reduce the impact of sequencing risk.

It’s time for a new approach to building retirement portfolios. The traditional approach—reducing growth assets and mitigating volatility—just doesn’t effectively address the need for retirees to grow their savings in retirement and the key risk to retirement savings, the sequencing of returns. By applying this new approach, you can tick both of these boxes and help your clients live their best retirement.

This information is current as at October 2019 unless otherwise specified. This information has been prepared specifically for authorised financial advisers in Australia, and is not intended for retail investors. This material is for general information purposes only. Any advice provided in this material does not take into account your objectives, financial situation or needs. Before acting on anything contained in this material, you should speak to your financial adviser and consider the appropriateness of the information received, having regard to your objectives, financial situation or needs. No person should rely on the content of this material or act on the basis of anything stated herein. Allianz Retire+ and its related entities, agents or employees do not accept any liability for any loss arising whether directly or indirectly from any use of this material. Past performance is not a reliable indicator of future performance.

PIMCO provides investment management and other support services to Allianz Retire+ but is not responsible for the performance of any Allianz Retire+ product, or any other product or service promoted or supplied by Allianz. Use of the POWERED BY PIMCO trade mark, or any other use of the PIMCO name, is not a recommendation of any particular security, strategy or investment product.

AMP’s Alex Wade points to the challenges inherent in comparing superannuation funds for pre-retirees and argues for more use of risk-based comparisons.

Ask anyone on the street if they are confident to compare super funds and you’ll likely have them scratching their heads. For our industry to rebuild trust and become more transparent, we need a better way for all Australians to compare super funds, so they can cut through the ‘noise’.

That’s why AMP is welcoming the Australian Prudential Regulation Authority’s (APRA’s) moves to overhaul the way superannuation data is collected and reported. As an industry we need a better system to help Australians more effectively compare products based on key indicators such as returns, fees and importantly, their appetite for and ability to withstand risk.

Currently, Australians are forced to calculate and compare their superannuation based on obscure industry measures, such as unit pricing, to benchmark their fund against the market. Furthermore, consumers can’t rely on government comparisons because the data is inconsistent and inadequate.

APRA’s decision to move to a simpler and more consumer-friendly traffic light system or heat map will potentially give super funds a rating of green, amber or

red based on returns, insurance, fees and fund sustainability. This is good news for consumers if it helps arm them with the right information to help assess how their fund is performing in an easily accessible format. While we haven’t yet seen the detail, we support the intent of making super easier to compare, and look forward to contributing to discussions when more detail is released.

However, it won’t be an easy task. Currently, all funds are required to publish the investment risk of each fund under APRA product dashboard reporting requirements. This is one measure, and on its own, is not likely to be understood by members and needs greater understanding and effectiveness for making comparisons. Particularly given the measure itself is based on the probability of loss, rather than the size of loss, and is not used by managers as genuine indicator of risk.

Beyond this, many funds appear ranked based on returns and fees alone – and while both incredibly important measures – comprehensive comparisons will require

Continued on page 26

Continued from page 25

APRA to take risk into account. At present, many members rely on fund labels such as “balanced” to inform their judgement, without realising that the underlying risk in these funds can be quite different.

While it might be appropriate for someone in their twenties, who is able to ride out the highs and lows of the market, to concentrate on returns and fees alone; steering someone in retirement or towards the end of their working life to a product that may have high returns, but carries significant risk, could be disastrous in the event of a downturn. This is especially the case when they have a limited horizon in which to recoup those losses, while they simultaneously draw down on their remaining balance to fund retirement.

People need to be able to understand what risk their fund is taking. The greater the transparency, the better placed consumers are to make an informed decision. One thing for certain is that markets rise and fall, and you don’t want to get caught at the tail end of a downward cycle. A fund that is rated “green” will be considered an endorsement, so the methodology must be appropriate for the members’ needs.

Currently, there are no standard guidelines for classification of growth and defensive assets in superannuation. This makes it particularly difficult for consumers to make apples with apples comparisons when trying to assess performance in line with risk.

We are seeing an increasing number of

industry and retail funds investing in unlisted property and infrastructure labelling the investments as defensive.

In recent times these investments have performed well, boosting returns for the funds. But there is no doubt they lack transparency, and in the event of a downturn they may carry considerable risk.

APRA needs to come up with a system to accurately compare funds – risk should be firmly on the table and reflected in the comparisons. We acknowledge that this is not an easy task for APRA, given the industry itself has debated with this issue for some time.

As an industry we must all start working together to find and agree to the right methodology that makes it easier for Australians to accurately compare their super products. We’re not there yet.

These issues are still being debated by the industry. AMP will contribute to APRA’s consultation process and will support an outcome that genuinely serves to ensure Australians can choose the right fund for their individual situation.

As an industry, we need to reduce complexity and show we genuinely have our members’ best interests at heart. We have been debating the quality of data and difficulty in comparing super for years. The time has come to get it right, and the right measure will keep the industry accountable.

Alex Wade is chief executive officer, Australian Wealth Management at AMP.

APRA needs to come up with a system to accurately compare funds – risk should be firmly on the table and reflected in the comparisons. We acknowledge that this is not an easy task for APRA, given the industry itself has debated with this issue for some time.

Waiting for the Government to finally move on Comprehensive Income Products in Retirement risks denying superannuation funds the opportunity to innovate, according to Parametric.

Superannuation funds should be acting to get ahead of the Federal Government’s timetable with respect to developing post-retirement products, according to an implementation specialist with Parametric Portfolio Associates.

Parametric’s chief investment officer, Paul Bouchey, said it was superannuation funds which should be setting the pace, not the Government.

“Although superannuation funds can follow the Government’s legislative timetable to develop a Comprehensive Income Product for Retirement (CIPR) by 1 July, 2022, that’s hardly an optimal outcome for fund members who have retired or are making retirement plans now,” he said. “They want a timetable dictated by their needs – not Government legislation.

“It will require superannuation funds to ‘get over’ the powerful anchoring bias of an accumulation mindset to design good solutions for retired members and members in retirement-planning phase.”

Parametric Australia managing director, Raewyn Williams, agreed with Bouchey’s analysis saying superannuation funds should not consider developing CIPRs as a chore but, rather, an opportunity.

Bouchey and Williams said that although there was keen debate about the use of

annuities (or other innovative longevity risk pooling solutions) in a CIPR, superannuation funds should not be distracted from thinking about clever ways their CIPR or other retirement solution could achieve their equity exposure.

“Certainly, it’s clear that the investments backing a CIPR will need to have some exposure to equities or other growth assets,” Bouchy said. “Superannuation funds should be looking now for different approaches, such as specific defensive or low volatility strategies and factor-based strategies that use simple construction rules to produce better-than-market income and volatility outcomes.

“Other equity options include emerging markets strategies with good downside risk properties and Australian equity strategies that recognise the value of franking credits to retirees as an additional source of yield while addressing the risks of simplistic frankingtilted approaches.”

Williams suggested that, structurally, superannuation funds should also think about whether segregating their pension assets from their accumulation assets – at least for some asset classes – makes sense.

By Mike Taylor

While there is good news for pensioners with cuts to deeming rates and an increase in the pension, those who don’t yet qualify will have to wait longer to access the Age Pension John Perri writes

September saw several Centrelink changes take effect.

Courtesy of deeming rate changes, which came into effect in July, some partpensioners will have received a backdated lump sum payment earlier in September. This payment also coincides with a scheduled increase to the rate of Age pension, giving some pensioners a double pay rise.

This good news comes on top of other changes which took effect earlier in the year, including:

• the increased amount available under the Pension Loan Scheme, and extended eligibility to all those of Age Pension age (and equivalent DVA payments) and selffunded retirees, and

• the increase in Work bonus to $300 per fortnight and extended to those who are self-employed (i.e. in a partnership or sole traders).

Although the changes for many pensioners might be relatively small, having some extra money in their budgets to tackle cost-of-living expenses is a positive thing.

The Age Pension age has increased to 66 (from 65.5). This means that clients turning age 65.5 between 1 July 2019 and 31 December 2019 will not have reached their pension age and must wait until age 66 (from 1 January 2020) to qualify.

The delay in qualification may impact retirement planning and cashflow modelling for your clients. On the other hand, it might benefit those couples with sheltering strategies in place.

It’s also worth remembering that since 1 July 2019, new means testing rules apply to new lifetime income streams commencing from this date.

With the increase to Age Pension age continuing in increments for another four years, it’s worth engaging pre-retirees now to ensure they won’t suffer an income gap if they need to retire before they qualify for the pension.

John Perri, Technical Strategy Manager, AMP

AMP Life Limited 84 079 300 379 has provided this information for adviser use only.

More than a platform, MyNorth offers a full wrap service to help advisers build their clients’ investment, super and retirement portfolios with • over 440 managed funds, • managed portfolios, • shares, and • cash options.

MyNorth has over $29.5 billion in AUM (as at August 2019) and is one of Australia’s fastest growing super and investment platforms. AMP is committed to keeping MyNorth competitive and contemporary to help your clients confidently reach their financial goals.

See the advertisement in this guide for more details in the disclaimer.

amp.com.au/mynorth

33 Alfred Street SYDNEY NSW 2000

T: 1800 667 841

Allianz Retire+ is an Australian company dedicated to developing retirement products to meet the unique needs of Australian retirees. We have brought together Allianz’s world-class insurance know-how with PIMCO’s unrivalled investment expertise to deliver security and stability throughout retirement. Our combined heritage, long-standing stability and global reach ensures that our retirement products can last a lifetime and evolve with the ups and downs of the market and the changing needs of our clients.

W: allianzretireplus.com.au

T: 1300 421 060 (between 8.30am and 5.30pm AET, Mon-Fri)

E: adviserfeedback@allianzretireplus.com.au

Find out why Australia’s leading Financial Advisers use FE Analytics to:

• Access the leading source of SMA & fund data

• Build, compare & monitor managed accounts

• Track ASX equities, ETFs & managed funds

• Conduct full portfolio performance reporting

• Conduct multi-asset benchmarking & objective comparisons

FE Analytics is the leading model portfolio research, performance and analytics software. Discover how it can help your business with a limited 14 day FREE trial.