2 minute read

Examination Trends

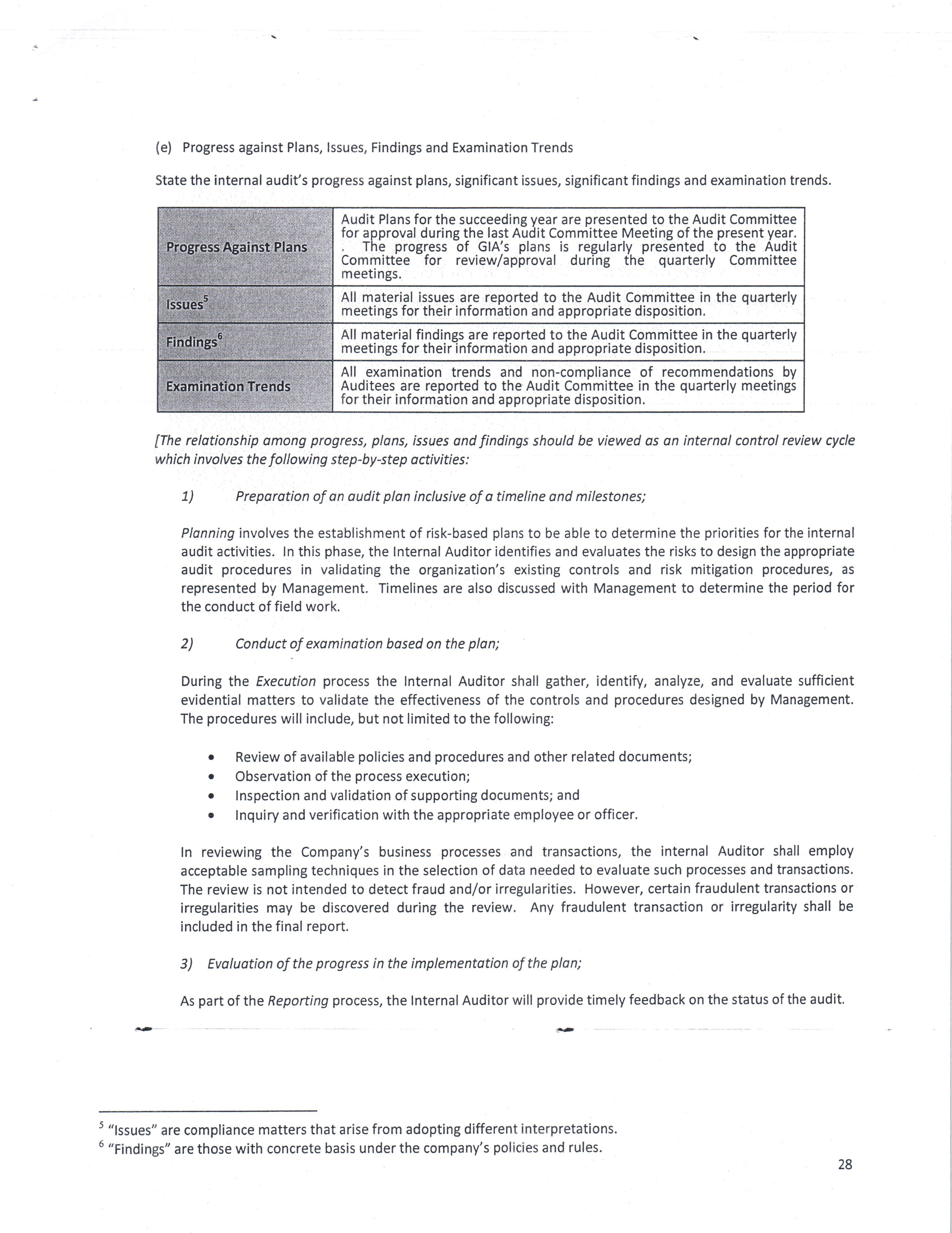

(e) Progress against Plans, lssues, Findings and Examination Trends

State the internal audit's progress against plans, significant issues, significant findings and examination trends.

Advertisement

Audit Plans for the succeeding year are presented to the Audit Committee for approval during the last Audit Committee Meeting of the present year. . The progress of GIA's plans is regularly presented to the Audit Committee tor review/approval during the quarterly Committee

meetings. All material issues are reported to the Audit Committee in the quarterly meetings for their informbtion and appropriate disposition. All material findings are reported to the Audit Committee in the quarterly meetings for their information and appropriate disposition. All examination trends and non-compliance of recommendations by Auditees are reported to the Audit Committee in the quarterly meetings for their informition and appropriate disposition.

[The relationship omong progress, plans, issues and findings should be viewed as on internal control review cycle which involves the following step-by-step activities:

1) Preparation of an audit plan inclusive of a timeline and milestones;

Planning involves the establishment of risk-based plans to be able to determine the priorities for the internal audit activities. In this phase, the lnternal Auditor identifies and evaluates the risks to design the appropriate audit procedures in validating the organization's existing controls and risk mitigation procedures, as represented by Management. Timelines are also discussed with Management to determine the period for the conduct of field work.

2) Conduct of exomination based on the plan;

During the Execution process the lnternal Auditor shall gather, identify, analyze, and evaluate sufficient evidential matters to validate the effectiveness of the controls and procedures designed by Management. The procedures will include, but not limited to the following:

o

o

O

o Review of available policies and procedures and other related documents; Observation of the process execution; Inspection and validation of supporting documents; and Inquiry and verification with the appropriate employee or officer.

In reviewing the Company's business processes and transactions, the internal Auditor shall employ

acceptable sampling techniques in the selection of data needed to evaluate such processes and transactions. The review is not intended to detect fraud and/or irregularities. However, certain fraudulent transactions or irregularities may be discovered during the review. Any fraudulent transaction or irregularity shall be included in the final report.

3) Evoluotion of the progress in the implementotion of the plan;

As part of the Reporting process, the lnternal Auditor will provide timely feedback on the status of the audit,

5 "lssues" are compliance matters that arise from adopting different interpretations. u "Findings" are those with concrete basis under the company's policies and rules.