5 minute read

Rystad Energy

from PESGB January/February 2021

by GESGB

PES

Olga Kerimova, SVP Analysis and Kristine Vassbotn, Senior Analyst

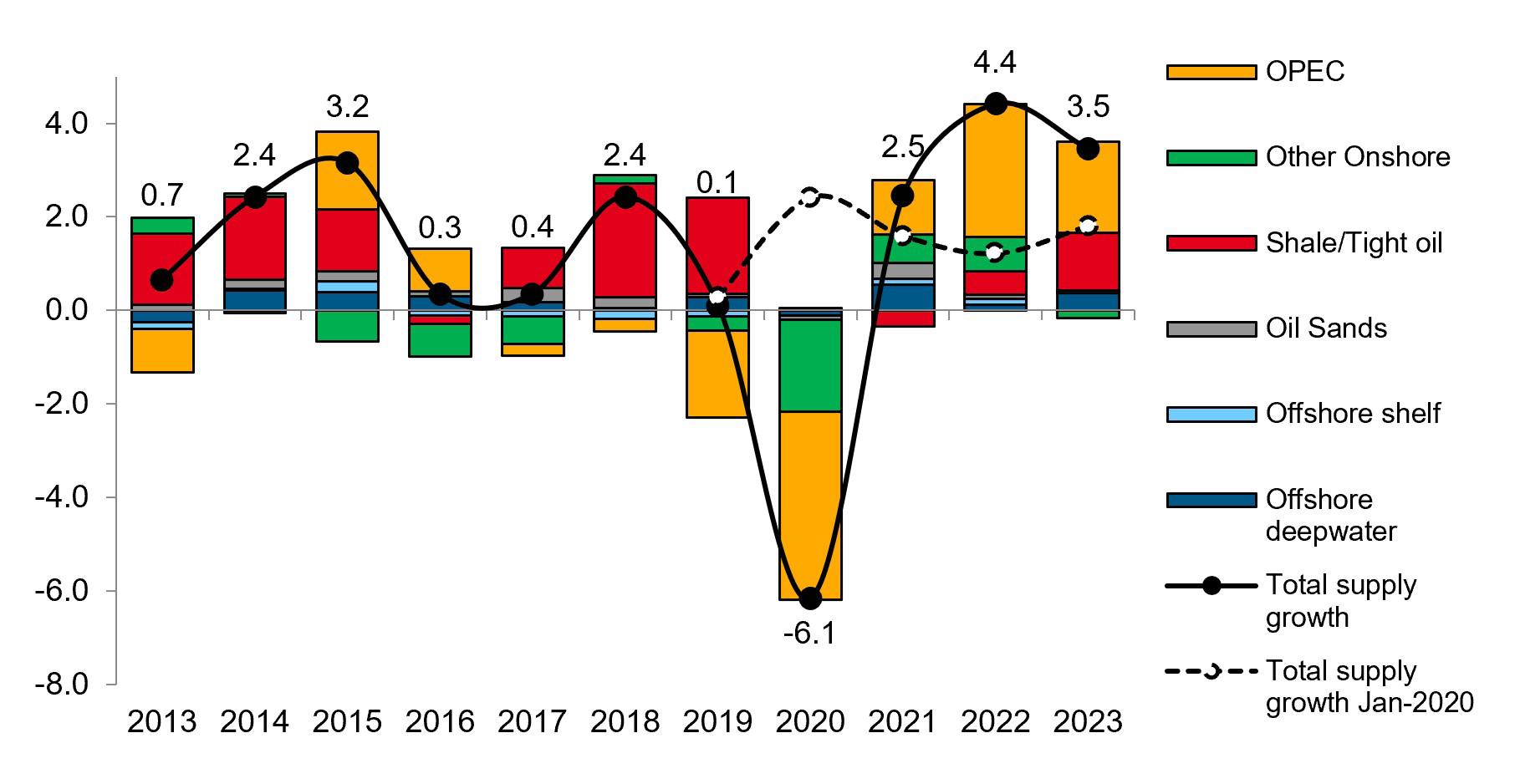

Global liquids supply shrank by 6.1 million barrels per day (bpd) last year as a result of the crash in oil prices and the global outbreak of Covid-19. Supply is expected to recover in 2021, primarily driven by additions from OPEC+. This article explains the key industry trends from last year and highlights the expectations for 2021 through analysis of supply growth, exploration success and spending trends.

Figure 1: Year-on-year net additions in global liquids supply. Supply split by supply segment – million bbl/d. (Source: UCube from Rystad Energy, January 2021)

Figure 1 shows changes in global liquids production from different supply segments and compares the current outlook to our forecast a year ago. Last year’s supply decline was driven by OPEC, which accounted for an estimated 4 million bpd of the 6.1 billion bpd drop, while conventional nonOPEC sources contributed 2 million bpd. In contrast, shale and tight oil production remained flat compared with 2019 volumes. Rystad Energy expects this year’s recovery in liquids additions to average 2.5 million bpd. The growth is spread across the different segments, except for shale, which is expected to decline 0.35 million bpd. Furthermore, oil sands supply could grow by 0.35 million bpd, while offshore (non-OPEC) is expected to increase by 0.7 million bpd. We expect higher conventional onshore production from non-OPEC countries of around 0.6 million bpd, driven by Russia and Kazakhstan. Total OPEC liquids production is expected to climb by 1.2 million bpd due to expanded OPEC+ quotas. OPEC+ met in December 2020 to tweak the supply strategy for the coming year and agreed to gradually increase production by a maximum 0.5 million bpd per month from January 2021, towards the nearly 2 million bpd higher target level which has been in place since 12 April 2020.

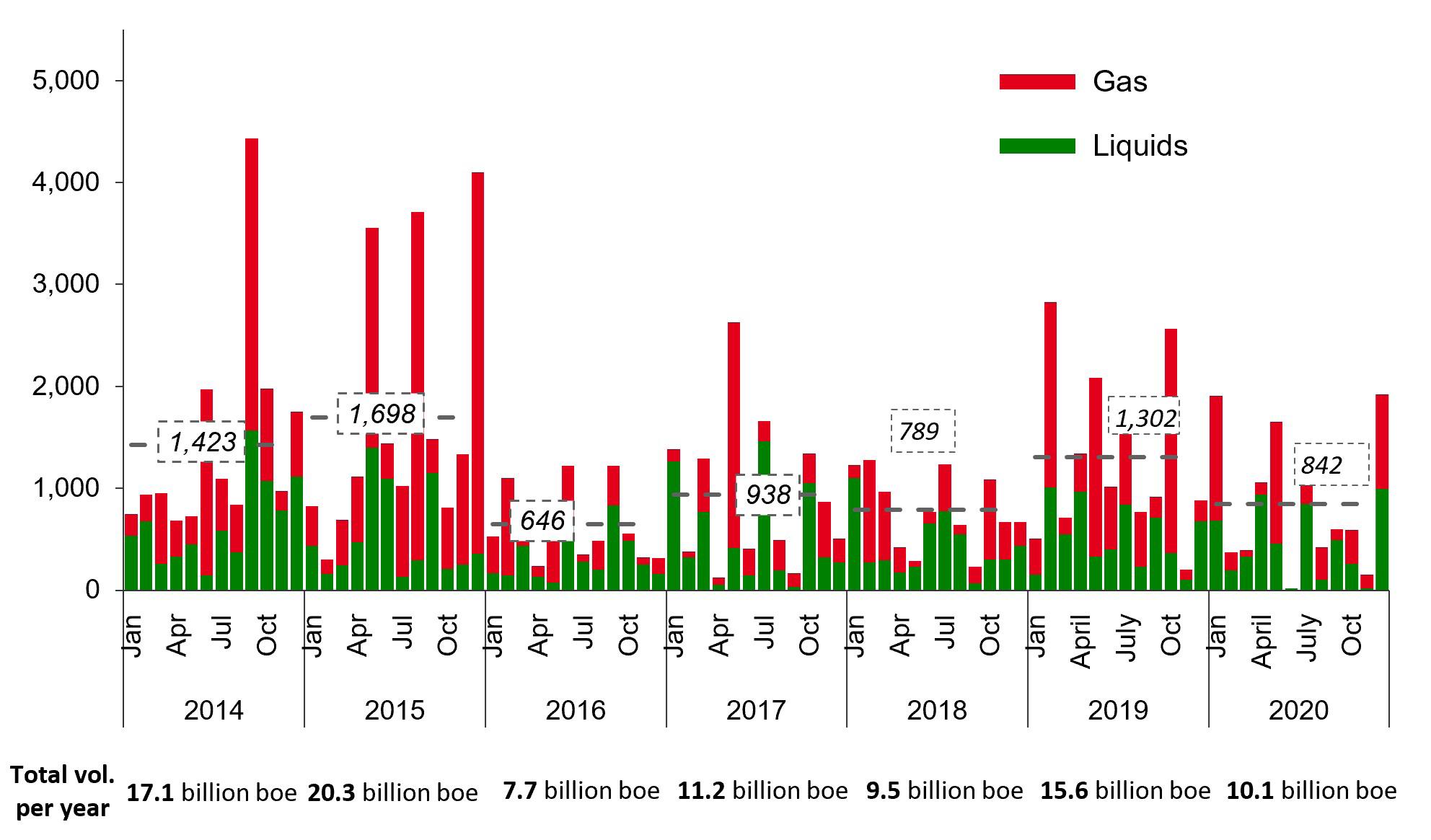

Figure 2: Total discovered conventional volumes per month - Million boe (Source: Rystad Energy Upstream Trends Report, January 2021)

Total conventional oil and gas discoveries remained resilient in 2020 despite drilling delays and cost cuts, with new-found volumes estimated at 10.1 billion boe. Discoveries held up well compared with the record low volumes of 7.7 billion boe from 2016, but fell compared with 2019, when monthly discoveries averaged just over 1.3 billion boe for a total estimated volume of 15.6 billion boe, representing a 64% increase over 2018 (Figure 2). January, May, July and December were the strongest months of 2020 in terms of added discoveries – May alone provided 1.7 billion boe in discovered volumes, with Gazprom’s 75 Let Pobedy discovery accounting for around 75% of these resources. The gas field is located in the Skuratovskaya prospect on the shelf of the Yamal Peninsula off Russia’s northern coast. Another large gas discovery was announced in the UAE in January of 2020 with the Jebel Ali gas field, which is estimated to hold 1.1 billion boe in recoverable resources. Apache (operator) and Total (with 50% working interest) made the 700 million boe Kwaskwasi discovery off Suriname in July, the third discovery in the country’s Block 58 last year. December was the strongest month of 2020 with an estimated 1.9 billion boe in discovered volumes, as Rosneft announced twin gas discoveries in the East Prinovozemelsky Block 1 & 2 where Vikulovskaya and Ragozinskaya are estimated to hold around 830 million boe in recoverable resources. Other notable discoveries last year include Guyana’s Redtail in the ExxonMobil-operated Stabroek block, discovered in September, and Total’s Luiperd discovery off South Africa, discovered in late October.

PES

Figure 3: Total E&P investments by supply segment – Billion USD nominal (Source: UCube from Rystad Energy, January 2021)

The previous downturn following the 2014 oil-price slump caused upstream expenditures to drop 25% in 2015 and an additional 25% in 2016, before a recovery brought spending to about $550 billion in 2018 and 2019. Investments are expected to have dropped about 30% to $380 billion last year (Figure 3). The largest decline is seen in the shale segment, where we estimate that investments more than halved last year as operators slashed their activity as a response to the low oil prices. The forecast for the next three years is further reduced by about 30% compared to our forecast from a year ago, as a result of the low oil prices and hence lower expected activity and spending, primarily in the US shale/tight oil segment. This year, shale spending is expected to grow by 2% while offshore combined is expected to fall another 2%. Rystad Energy expects that tight oil will see the largest growth in investments over the next three years as the segment bounces back from last year’s drop. In terms of geographical split, the Americas and Africa are expected to drive the recovery in global investments. Conclusion A year ago, we looked forward to substantial growth in the 2020 global liquids supply. However, the oil price crash coupled with the Covid-19fueled demand destruction led to an estimated 6.1 million bpd liquids supply drop last year as shale producers slashed capital budgets and OPEC+ countries agreed to cut production. This year, we expect to see a 2.5 million bpd liquids supply growth, led primarily by the December 2020 OPEC+ agreement to gradually increase production. Over the next three years, we also expect to see a growth in capital investments and increasing additions from the shale/tight oil supply segment.

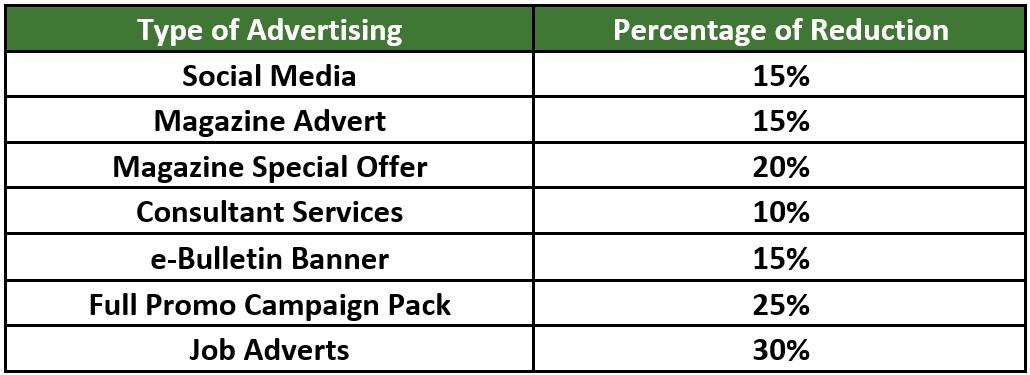

ALL OUR ADVERTISING SERVICES REDUCED UP TO 30%

Book an advert for February, March or April and enjoy low prices on all of our advertising services, up to 30% reduction! It’s an offer like we’ve never had before, and there may not be better chance to raise your profile within the PESGB community this winter!