12 minute read

The 650bn rupee question: will monetary tightening bridge the diver- gence between monetary and fiscal policy?

The 650bn rupee question:

will monetary tightening bridge the divergence between monetary and fiscal policy?

Advertisement

When the government is being fiscally frivolous, is the interest rate the only way to make them stop?

By Ariba Shahid

Earlier this week, the State Bank of Pakistan announced a 150 bps policy rate hike. Conventional wisdom would say that the logic behind a policy rate hike is inflation. Higher interest rates make loans more expensive for both businesses and consumers, and everyone ends up spending more on interest payments But more even than getting the government to increase interest payments, the goal of the SBP in increasing the policy rate seems to be dissuading the government from borrowing more. In essence, the move is a babysitting measure meant to discourage the government from being fiscally irresponsible. The official explanation given behind the hike was that “this action, together with much needed fiscal consolidation, should help moderate demand to a more sustainable pace while keeping inflation expectations anchored and containing risks to external stability.”

The SBP’s call for “timely action” to “restore fiscal prudence, while providing adequate and targeted social protection to the most vulnerable” also indicates that a key element of the statement released by the central bank is the divergence between the monetary and fiscal policy. This is the first time in the recent few years where the SBP is calling for fiscal prudence. This hints at how things may have gotten out of hand.

The MPS pointed towards the pressures added by an expansionary fiscal policy. The SBP said that the fiscal stance in FY22 is now expected to be expansionary instead of budgeted consolidation. The impact of this divergence is that the SBP is left to do the brunt work and make up for the gap left by the government which has left an impact on economic indicators and fundamentals.

The Rs 650bn misalignment

The IMF projected expenditure to be at $ 11,731 bn for FY22, however, the estimated value for the year turns out to be $12,381. As per IMF estimates, the government of Pakistan has overstepped in public spending by at least $650bn than what was previously projected. This includes current expenditure, interest expenditure, subsidies expenditure, and development expenditure and net lending.

“External pressures remain elevated and the inflation outlook has deteriorated due to both home-grown and international factors. Domestically, an expansionary fiscal stance this year, exacerbated by the recent energy subsidy package, has fueled demand and lingering policy uncertainty has compounded pressures on the exchange rate,” read the statement.

“The central bank’s statement conveys, in so many words, that the real problem lies on the fiscal side. Without the economic managers in power agreeing to cut spending, the central bank will always keep playing catchup [with bond market players that are demanding higher yields, and based on real interest rates],” says Uzair Younus, Director of the Pakistan Initiative at the Atlantic Council. “However, the hike once again indicates that the central bank is behind the curve and is hesitant to impose severe costs on the government for abandoning fiscal prudence,” adds Younus

The statement also shows that the SBP is of the opinion that fiscal prudence is very much possible in the present given it was followed even during the peak of the pandemic. Highlighting the importance of fiscal prudence, the SBP mentions, “such prudence enabled Pakistan’s public debt to decline from 75 percent of GDP in FY19 to 71 percent in 2021 despite the Covid shock, in sharp contrast to the average increase of around 10 percent of GDP across emerging markets over the same period.”

Does the government have this kind of money?

The simple answer to this question is no, it does not. Flashback to last year’s budget when the government was overenthusiastic about revenues, and as a result pushed out a business friendly budget. The budget showed the government was in no mood to cut back on fiscal expenditure. It seemed like the days of austerity were over. However, what was interesting is that the government was relying heavily on the petroleum development levy as a form of revenue. The Government anticipated tax revenue to come in at Rs 5829 billion growing 17.45%. Whereas, non tax revenue was expected to grow 29.19% from Rs 1610bn to Rs 2080. This was strange considering the global commodity cycle. The world was reopening and the drastic increase in demand for fuel resulted in fuel prices already heading up.

But global prices refused to cooperate with the government’s projections. As they spiraled out of control, the room to impose fresh taxes on fuels diminished proportionately. Fuel prices have just been increased by the incumbent government by 20% or Rs 30. However, there still remains a subsidy on fuel prices. There will be considerable time before the government is able to earn off fuel, a commodity that was once seen as a source of revenue for the government.

Between February when the subsidy was first introduced by the Imran administration up until June when the subsidy was slashed by the incumbent Sharif regime, the federal government copped a blow of nearly Rs 300 billion,

As per data by the SBP, the petroleum levy revenue went down 90% for the period of July 2021 to September 2020 compared to the same period last year. As per the budget, expenditure on subsidies was projected at Rs 682 billion, which was 3.26 times what the subsidy expenditure was in FY21, during a pandemic.

Do policy rate hikes make sense?

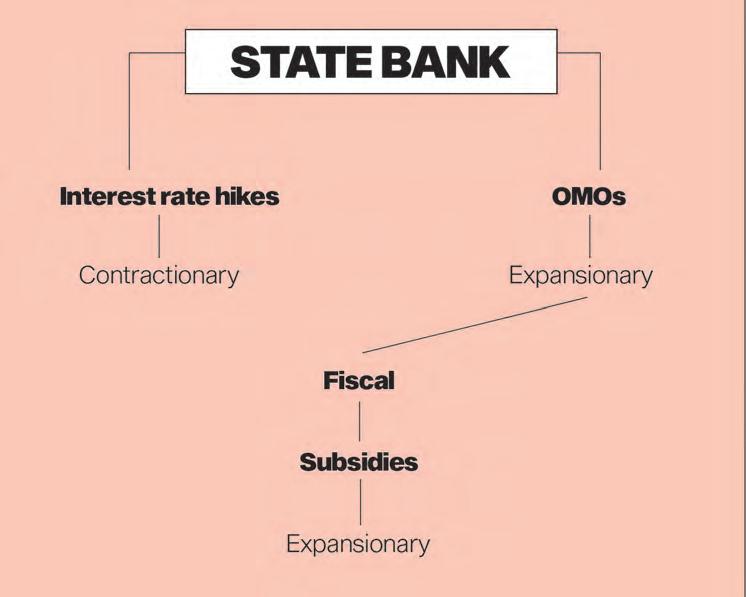

In essence at this point in time, the monetary policy is in effect a tool to deter the government from borrowing more considering the high rates. This is because the inflation Pakistan is now witnessing is primarily cost push inflation as opposed to money supply driven demand pull inflation. Cost-push inflation occurs when the cost of business increases in the form of higher energy prices, higher raw material prices and rising wages. Due to the rising costs, the aggregate supply retreats and again many buyers end up chasing fewer goods. This again leads to a rise in prices. This form of inflation is difficult to reverse as it creates an inflationary spiral. Furthermore, this inflation will only subside with a rise in aggregate supply in the economy, which cannot be done overnight therefore, reliance on imports remains. Of course, governments often tend at moments like this to borrow from the central bank, particularly in developing countries. The borrowing only makes matters worse, and if the central bank does not dish out the cash the government can go to commercial banks. This results in a crowding out of finances in the private sector. To stop the government from doing this, a tool in the hand of the central bank is hiking policy rates to make it more expensive for the government to borrow. Restricting the government from borrowing is thus an anti-inflationary measure. The SBP focuses on achieving monetary stability by controlling inflation close to its annual and medium-term targets set by the government. This means it is in the mandate of the SBP to control inflation, however, the tool it predominantly has is the tool to control money supply. When policy rates are hiked up, the supply of money decreases. This is because people find it more rewarding to park their money into savings as the saving rate is higher; or they do not take out loans to spend due to the high cost of borrowing.

As a result, the supply of money is curtailed. This is usually done when there is demand pull inflation where too few goods are chased by lots of money driving prices up. When a contractionary monetary policy is put to use, inflation is expected to go down, unemployment and output are said to decrease too. This is often done to prevent the economy from overheating and to avoid the bust part of the boom-bust cycle.

Essentially, when there is little demand-pull inflation because most of the inflation is cost push driven, the hiking of policy rates makes little impact. It is said that if policy rates are hiked exorbitantly, especially once they attain real interest rate levels, i.e. higher than actual inflation; they tend to be counterproductive and in some cases bring around a wave of inflation.

A different school of thought is based on the cost-push effects of interest rates which suggest raising interest rates to a very high level is often reflected in a higher price level. This is called the Gibson Paradox, a concept dating back to 1923. It uses observation to explain that real interest rates and changes in the general price level are positively correlated at times. The term was first used by John Maynard Keynes.

Reliance on borrowing working capital caused higher interest rates to translate into a higher cost of working capital and a rise in inflation. In the case that firms decide not to borrow working capital from banks, the opportunity cost of their own funds rise with market interest rates, which also impact the price level.

In the case of Pakistan, we haven’t entered real interest rate territory yet despite more than 600bps worth of hiking in less than a year. Until real interest rates aren’t achieved, the cost of borrowing is still cheap while the cost of saving is significantly less rewarding, therefore the money supply is not truly contained, and the SBP needs to do more for inflation.

OMOs cancelling out monetary policy?

If the SBP manages to deter the government from borrowing large amounts to foot the bill for its spending patterns, the SBP is intentionally or unintentionally trying to bring a convergence in policy. It is also a question whether the government will actually be put off by the high cost of borrowing, because they could just borrow more at a later date. This will further push up inflation because of the fiscal expansionary policy and the cost associated with interest rates rising.

This enforcing of fiscal austerity is beyond the SBPs targets, however when the government is being fiscally frivolous for political clout, it looks like the autonomous and independent actors such as the SBP have to pull it together.

However, there is a conflict here. Despite the SBP indirectly raising the cost of borrowing for the government, it is also in a way subsidizing it through open market operations (OMO). OMOs are important because not only do they help implement the monetary policy, but also help central banks to manage the short term interest rate in line with the objectives of its stated Monetary Policy stance.

OMOs help central banks control the total money supply by expanding when conducting an OMO injection, and contracting when mopping up liquidity.

In the current scenario, the SBP is indirectly financing the government through these frequent OMOs.

Profit has previously written an explainer for what OMOs are. However, to simplify it in a few lines, Younus says, “Think of OMOs as your mamu wanting to give money to your mom but he can’t. Instead, he gives you Rs 5000 and tells you to give Rs 4000 to your mom. He lets you keep the Rs 1000.” In this analogy, you are the commercial bank, your mom is the government, and your mamu is the central bank.

When the government purchases from the interbank, it is affecting the money supply. This reduces the availability of those t-bills or bonds, as a result, the price of the remaining bonds go up. When bond prices rise, the yields fall. This brings interest rates down in the overall economy.

There was initially a ban on government borrowing from the SBP under the IMF programme till September 2022; however following the SBP Act, the government has now given up and agreed to permanently close the door to this option through legislation.

“The bank shall not extend any direct credit to or guarantee any obligations of the government, or any government-owned entity or any other public entity”, states the clause.

In case you’re wondering why can’t the government just borrow infinite amounts from the central bank itself – because it increases the money supply rapidly which drives up inflation. Borrowing has to be done against some collateral.

As per the Act Section 409 C, the SBP shall not purchase securities issued by the government or any government-owned entity or any other public entity in the primary market. The Central Bank may purchase such securities in the secondary market.

Simply put, the government is in a crunch. The government has been increasingly demanding domestic commercial financing, especially in the absence of foreign inflows. The larger the demand, the more power for banks. Banks, however, have been driving up yields considering the inflationary environment; despite a central bank that is showing caution at hiking policy rates.

In order to meet its expenses, the government continues to borrow from commercial banks because it cannot borrow from the SBP directly.

During the January 24 Monetary Policy Committee Press conference, Profit asked governor SBP, Dr Reza Baqir about the 63 day OMO injections and the concept of cheap money for the government. The governor responded saying that the SBP in accordance with the SBP Act, while not being able to lend directly to the government, can step in and inject liquidity when needed.

What this means is the SBP, while not being able to lend to the government directly, can help it get credit at a better yield through OMO injections. This helps drive up profits for banks because they get a decent spread, and helps the government.

What this also means is that on hand the policy rate is being hiked to control money supply for businesses, individuals, and the government. On the other hand, the OMOs are cancelling out the effect of the policy rate hike on government borrowing. This means, the impact of the policy rate hike is essentially just on businesses and individuals, not really the government which already had the liberty to borrow more at a later time to pay off existing debt.

Is everything just cancelling each other out?

So the OMOs are cancelling the policy rate hikes out. The expansionary fiscal policy is canceling the policy rate hikes too. A country should not have both an expansionary fiscal policy with a contractionary monetary policy; nor should the government have a contractionary monetary policy whilst an expansionary government lending policy through OMOs. All this is counterproductive in attaining the one thing they’re out targeting, inflation. What all this suggests is that Pakistan needs clear directed approach in its policies, especially for long term decisions. This confused policy making will not only balloon the Rs 650 bn, but makes lives difficult for businesses and individuals, the people the institutions should be set out to help. In all this, one hopes that the IMF is able to knock sense back in and set the government on track for fiscal austerity. Once that is put into place, the SBP will not need to step in with OMOs to provide cheap credit. Only then will the monetary policy make sense and have an impact. Until then, all we can do is wait and hope things dont get out of control. n