5 minute read

Buyer Beware – OEMs Increasingly Exercising Their Rights of First Refusal

By Tom Vangel & James Radke

Over the past several years, auto dealers across the country have experienced a rather robust buy/sell market. Manufacturers who previously sat on the sidelines and approved proposed buyers are now taking more of an interest in who the ultimate buyer of the dealership will be. Consequently, manufacturers of various line-makes have been electing to exercise their right of first refusal (ROFR) to appoint their favored candidate in lieu of the proposed buyer. Sometimes, where there are competing offers for the dealership, a disgruntled runner-up is able to convince the manufacturer to exercise the ROFR and appoint him instead of the proposed buyer. In other situations, the manufacturer may wish to appoint a minority dealer for a particular location, or it may prefer another candidate who operates other points for the manufacturer.

What does this mean for the proposed buyer? Unfortunately, under Massachusetts General Laws Chapter 93B, which governs the relationships between automotive manufacturers, distributors, and dealers, proposed buyers do not have legal standing to sue the manufacturer for the wrongful exercise of its ROFR. This is consistent with most automotive laws across the country.

This issue of standing was first decided in Massachusetts in 1985 in the case of Beard v. Toyota, which presented an unusual set of circumstances. In that case, approximately six weeks after the selling dealer signed a purchase and sale agree- ment for his Toyota dealership, he received a better offer for an additional $50,000. The seller convinced Toyota that it should not approve his original proposed buyer, allowing him to accept the higher offer. After receiving notice that Toyota had declined to approve his application, the original proposed buyer sued Toyota for wrongfully withholding its approval.

The Massachusetts Supreme Judicial Court (SJC) determined that the Legislature’s intent in enacting Chapter 93B was to protect motor vehicle franchisees and dealers from “the type of injury to which they have been susceptible by virtue of the inequality of their bargaining power and that of the affiliated manufacturers and distributors.” In other words, the law was intended to protect a Ford dealer, for example, from the unfair and oppressive actions of Ford; it was not intended to protect an unaffiliated buyer from the actions of the manufacturer. Thus, while the circumstances of the Beard case are unlikely to occur with any frequency - with a seller convincing the manufacturer to reject his own buyer - the case established the law in Massachusetts for the past 38 years.

In 2014, the SJC affirmed the principles of the Beard decision in litigation brought against Tesla arising from its direct sales model, finding that only a franchised Tesla dealer (of which there were none) or the Attorney General would have standing to sue Tesla for its direct-to-consumer model. Accordingly, the law in Massachusetts is clear that, unless the selling dealer is willing to object to the manufacturer’s exercise of its ROFR, the proposed buyer will have no standing to mount a legal challenge to the decision to appoint a favored candidate over an otherwise qualified prospective buyer.

Typically, selling dealers are agnostic concerning the identity of the successor franchisee, since the manufacturer’s exercise of the ROFR requires the new buyer to match every term in the asset purchase agreement and the real estate purchase and sale agreement, including due diligence periods, satisfaction of financing contingencies or lack thereof, and, most importantly, the purchase price and timing of the closing. The buyer appointed by the factory must close on the exact same terms as set forth in the agreements. Consequently, the selling dealer is not at all negatively impacted by the factory’s exercise of the ROFR and is usually just as happy to close with a different buyer. This is particularly true if there is any risk that the manufacturer may not approve the original buyer for legitimate reasons.

The consolation prize for the jilted buyer is that his legal and other out-of-pocket expenses associated with attempting to purchase the dealership must be reimbursed by either the manufacturer or its appointed buyer. A jilted buyer should not be bashful in calculating all of his expenses. Although typically reimbursement is only sought for actual out of pocket expenses for attorneys, accountants, environmental consultants, appraisers, and the like, the statute does not specifically preclude a dealer principal from seeking reimbursement for his lost time associated with pursuing the transaction. A buyer should include that as an eligible expense in the asset purchase agreement with a corresponding hourly rate.

Lastly, it should be noted that certain insider transactions are exempt from the manufacturer’s ROFR. Manufacturers are not permitted to exercise a ROFR over a sale to a co-owner of a dealership, a member of dealership management who was previously approved by the manufacturer as a manager, or an immediate family member of the dealer or co-owner.

Tom Vangel and Jamie Radke are partners with the law firm Murtha Cullina LLP in Boston who specialize in automotive law. They can be reached at 617-457-4072.

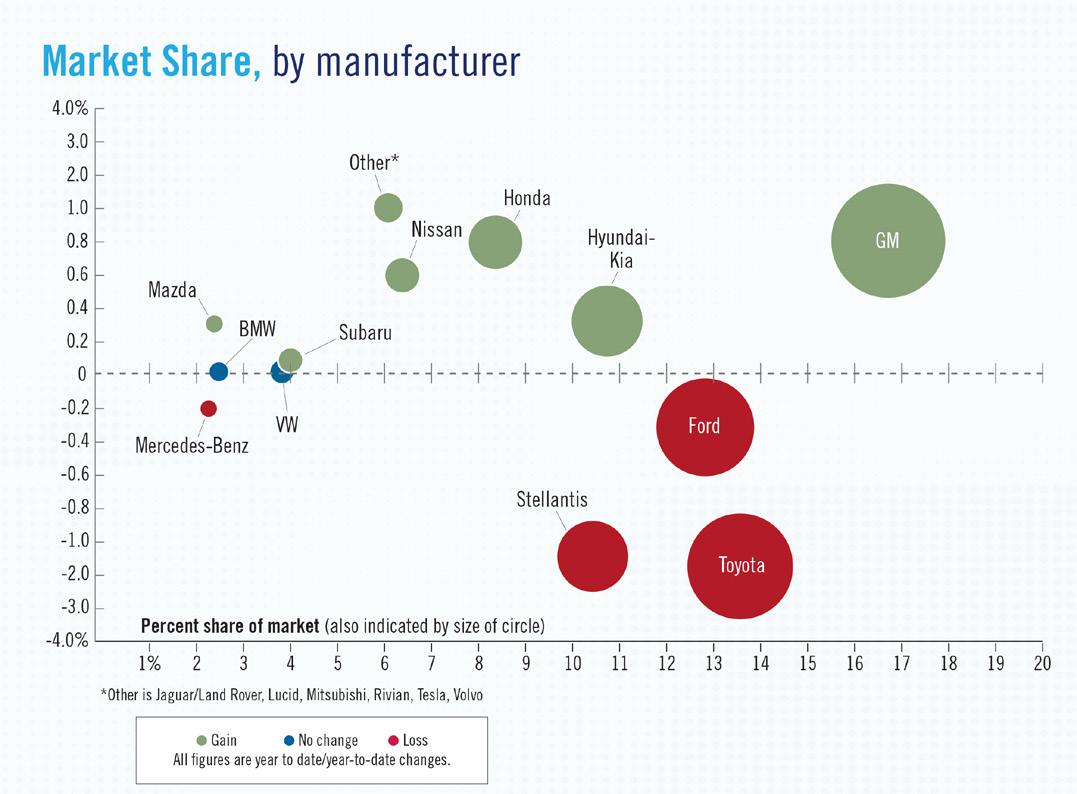

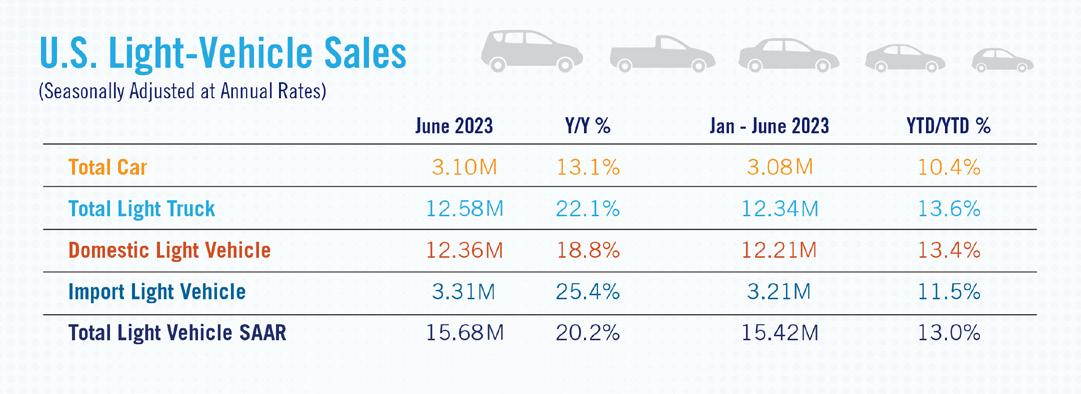

Strong new light-vehicle sales last month helped end the first half of the year on a high note. The June 2023 SAAR totaled 15.7 million units, an increase of 20.2% compared with the June 2022 SAAR. Raw sales volume in June 2023 was 1.37 million units, raising total sales volume for the first half of the year to 7.66 million units—up 13% compared with the first half of 2022. According to Wards intelligence, fleet sales were 18% of June 2023 volume, up from 16% in June 2022. Wards estimates that retail sales increased 7.6% year-over-year the first half of 2023, while fleet sales increased 45% over the same period.

Alternative fuel vehicles gained market share the first half of the year with sales of battery electric vehicles (BEVs), plug-in hybrids and hybrids comprising 15.4% of all new light vehicles sold. BEVs alone represented 6.9% of all new light-vehicle sales, up from 4.9% of sales the first half of 2022. Crossovers — at 46.6% of all new light-vehicles sold during the first half of the year — remained the most popular segment.

Improving new-vehicle availability helped drive the sales increases. New light-vehicle inventory on the ground and in-transit totaled 1.81 million units at the start of June 2023. We expect month-end inventory for June 2023 will increase slightly compared to the beginning of the month. Manufacturer incentive spending has increased incrementally as inventory has improved. According to J.D. Power, average incentive spending per unit is expected to total $1,798 in June 2023, up only slightly compared with May 2023 but a significant 95.9% increase compared with June 2022. J.D. Power also notes that leasing discounts have improved in recent months. In June 2023 leasing should account for 21% of new-vehicle retail sales, an improvement from the low of 16% in September 2022 but still below the pre-pandemic lease penetration of 30% in June 2019.

After a pause at its June meeting, the Fed has signaled it will increase the Fed Funds Rate further in coming months. These higher rates will be a headwind for new-vehicle sales. But there is still pent-up demand from retail and fleet customers, and high used-vehicle values will help consumers with their trade-in values. We expect new light-vehicle sales in the second half of the year to be similar to the first half. As a result, we have increased our overall 2023 forecast to 15.2 million units.