2 minute read

Performance Monitoring

Council will continue to report its financial performance each quarter.

Additionally, an annual review is undertaken of the Long Term Financial Plan to review assumptions and assess the robustness of the model. Key performance measures used in this assessment include:

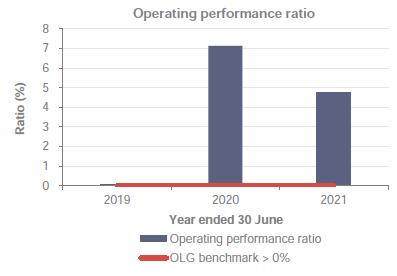

OPERATING PERFORMANCE

This ratio measures whether operating expenditure is contained within operating income. The benchmark for this ratio is 0 percent or greater. An operating deficit occurs when total expenses are greater than total income (excluding all capital amounts). This includes a council’s day to day income and expenses. Councils are encouraged to budget for a surplus result, and to consider asset condition and maintenance requirements. The ratio is calculated by total continuing operating revenue (excluding capital grants and contributions), less operating expenses, divided by total continuing operating revenue (excluding capital grants and contributions).

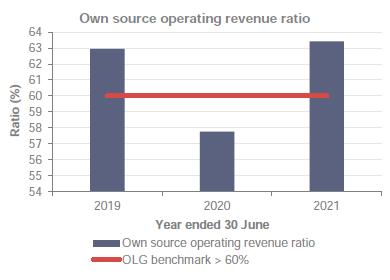

OWN SOURCE OPERATING REVENUE

This ratio measures financial flexibility and indicates reliance on external funding sources such as grants and contributions. A council’s financial flexibility improves as its own source revenue (including rates, annual charges and user fees and charges) increases. The benchmark is greater than 60 percent. The ratio is calculated by total continuing operating revenue less all grants and contributions divided by total continuing operating revenue inclusive of capital grants and contributions.

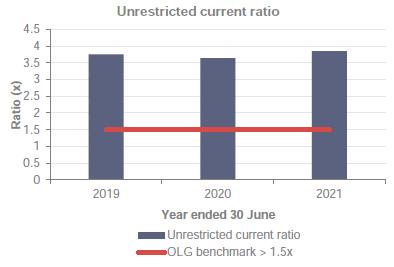

UNRESTRICTED CURRENT RATIO

This ratio measures working capital and Council’s ability to meet short term obligations. Restrictions placed on various funding sources (e.g. Section 7.11 development contributions, roads contributions) complicate the traditional current ratio used to assess liquidity of businesses, as cash allocated to specific projects is restricted and cannot be used to meet a council’s other operating and borrowing costs. For example, an unrestricted ratio of 4.45 means that council has $4.45 in unrestricted current assets to meet each $1.00 of unrestricted current liabilities. A ratio of less than 1.5 is considered unsatisfactory and could indicate, along with other financial indicators, that the council may face some financial risk. The ratio is calculated by current assets less all external restrictions divided by current liabilities less specific purpose liabilities.

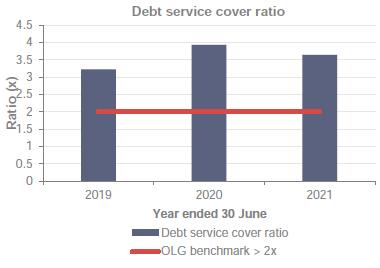

DEBT SERVICE COVER RATIO

This ratio measures the availability of operating cash to service debt including interest, principal and lease payments. Councils have approximately twice as many financial assets as they do outstanding borrowings. The benchmark for this ratio is greater than 2.0. A high ratio indicates the council has significant capacity to repay debt. The ratio is calculated by operating results before capital, excluding interest and depreciation/impairment/ amortisation divided by principal repayments (from Statement of Cashflow) and interest on loans.

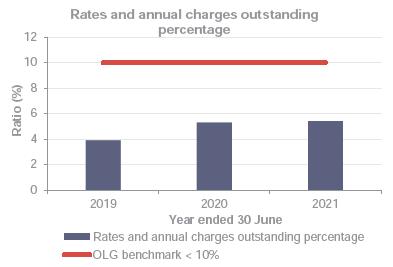

RATES AND ANNUAL CHARGES OUTSTANDING PERCENTAGE

This ratio assesses the impact of uncollected rates and annual charges on liquidity and the efficiency of councils’ debt recovery. Some councils may have agreements in place to assist ratepayers in an attempt to reduce the debt owed to council. The benchmark for outstanding rates is <10 percent for regional areas. The ratio is calculated by rates and annual charges outstanding divided by rates and annual charges levied by council.