7 minute read

Review of Operations

Operations Review

Keeping Our Sectors GrowinG

Advertisement

Review of Operations

The Bank achieved targeted utilization of J$6.0 billion for financial year 2011 despite the many challenges posed by the prevailing conditions in the domestic economy. This outturn represents an increase of 9% over the results achieved for the corresponding period last year and was largely influenced by an aggressive marketing campaign which sought to promote the Bank’s competitively priced products to the SME market.

REVENUE

For the financial year ended 31 March 2011, the Bank posted revenue of J$524.8 million, a reduction of 15% on the J$618.1 million recorded in 2010. Net interest income was recorded at J$272.3 million down from the J$345.1 million recorded at year-end 2010. This reduction resulted from the broader Government strategy of reducing lending rates with the aim of stimulating lending within the economy as well as the gradual decline in investment rates occasioned by the Jamaica Debt Exchange (JDX).

PROFIT

The relative stability in the exchange rates of the major trading currencies towards the latter part of the year, enabled the Bank to reverse losses incurred during the early months, particularly on its Canadian Dollar portfolio used to finance transactions under the Cuban Line of Credit. As a result, income earned from foreign exchange activities recovered to post a gain of J$19.7 million at year end 2011 as against J$120.3 million in 2010, resulting in operating profit of J$297.6 million being realised at year-end 2011, a decrease of 42% on prior year results. The main contributors to the reduction in operating profit were the decline in foreign exchange gains as well as market rates on Government securities which impacted the Bank’s earnings during the period. Increased administrative expenses largely as a result of extraordinary adjustments required under IAS 19 in respect of the Bank’s Pension Fund contribution, further reduced the Bank’s profit position, as profit before taxation for the year fell to J$7.4 million at year end 2011.

For the financial year ended 31 March 2011, the Bank’s total assets were reported at $7.9 billion, in line with the results of the previous year 2010. Notes Discounted increased by 27%, ending the year at $2.9 billion up from the $2.3 billion recorded in 2010 due to increased loan utilisation. Cash and deposits reflected a reduction from J$1.7 billion in 2009/2010 to J$1.3 billion, at year-end 2011 as funds were utilised in the Bank’s lending activities.

SHAREHOLDERS’ EQUITY

Profit earned during the year and increased retained earnings helped to push Shareholder’s Equity to $1.9 billion at year-end 2010/2011, reflecting a marginal increase over 2010 results of $1.8 billion.

REVIEW AND ANALYSIS OF LENDING OPERATIONS

Supported by sustained marketing efforts and increased interaction with stakeholders, the Bank achieved its loan utilization target of J$6.0 billion for the financial year ended 2011 and continued to provide competitively priced trade financing and medium term loans to the productive sector.

The Bank continued to record strong performance in its short term United States dollar Trade Credit facilities used to finance the importation of raw materials and intermediate goods. Loans approved and disbursed through these arrangements reflected 36% growth year-over-year, moving from US$16.4 million in 2010 to US$22.3 million at financial yearend 2011. This positive development was reflected in the overall demand for United States dollar loans which showed disbursements increasing from US$35.6 million in 2010 to US$44.9 million at year-end 2011, an improvement of 26%.

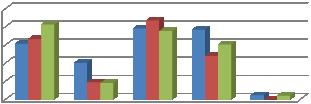

Local currency loan disbursements however, recorded a marginal decline, ending the year at J$2.2 billion, a reduction of 4.3% on the amount of J$2.3 billion recorded in 2010. The manufacturing and agro-processing sectors continued to be the main recipients of the Bank’s financing facilities, receiving approximately J$4.0 billion or 60% of total loans disbursed during the period. Food and beverage and the distribution and services sectors accounted for the remaining 40% of loans disbursed during the year.

LOANS DISBURSED BY SECTOR

2.5 2 1.5 RETURN ON 1 ASSETS 0 0.5 -0.5 -1 -1.5

2009 2010 2011

The Bank continued to exercise effective credit management and due diligence in the administration of the loan portfolio and at 31 March 2011, the Bank’s bad debt portfolio as a percentage of total loans, was recorded at 0.73%. This performance was particularly gratifying in the context of the increase in loan loss provisions across the financial services sector as reported by the Central Bank, as well as the Bank’s increased risk exposure, as it deepened its foray into direct lending. CUBAN LINE OF CREDIT

The Cuban Line of Credit negotiated in 1997 to facilitate the export of Jamaican goods to Cuba, gradually returned to full operation after temporary suspension due to setbacks experienced with Cuba’s main export earning sectors. The Line is again showing signs of growth, with exports financed during the year reported at US$3.4 million, significantly above the US$1.3 million reported last year. The Bank continued to work closely with its counterpart in Cuba as well as members of the local exporting community to maintain full utilization of the Line of Credit.

VALUE OF LOANS DISBURSED OVER LAST 3 FINANCIAL YEARS

6600 6400 6200 6000 5800 5600 5400 5200 5000

This innovative product safeguards both foreign and local receivables against commercial risk of non-payment by foreign and local buyers and facilitates the expansion of trade into new and existing markets. The insurance policy covers 85% (commercial risk) and 90% (political risk) of the loss amount with the exporters assuming the remaining 15% and 10% respectively. For the period under review, the Bank insured receivables approximating $1.5 billion. The EXIM Bank reinsures its insurance portfolio under an overseas Quota Share agreement, whereby it cedes 60% of its premium income for 60% coverage of its insurable risk.

Trade Credit Insurance (TCI) offers coverage at competitive premium rates and also facilitates the financing of receivables through the Bank’s Insurance Policy Discounting Facility (IPDF), a post-shipment financing scheme which allows policyholders to obtain short term working capital loans. Several policyholders have benefitted from this loan programme and the Bank continues to market this product to encourage the productive sector to utilize the benefits available to policyholders. Loans disbursed under this facility during the review period were reported at $57.4 million.

Through its association with the BERNE Union, the international organization of Export Credit Agencies, the Bank has access to financial, credit and other information on trends in the industry worldwide which it leverages for the benefit of its policyholders to enhance their trading relationships.

HUMAN RESOURCE

DEVELOPMENT

Changes in the economic environment worldwide and locally required the Bank to implement strategies to not only maintain viability, but to have a greater economic impact. The Bank therefore adopted strategic objectives and goals which required adjustments on the part of management and staff to realign attitudes and behaviours which were more supportive of its strategic objectives.

With this in mind, the Bank facilitated staff participation in workshops as well as special training programmes focusing primarily on strategic planning and implementation, change management, customer satisfaction, waste reduction and productivity which strengthened the capability of the staff to perform at required levels.

Additionally, several initiatives aimed at improving employee relations, staff satisfaction and engagement were successfully undertaken. Through the Employee Relations Committee, the staff initiated public speaking workshops and also launched a Wellness Programme which was highlighted by the staging of a ‘Biggest Loser Competition’ in which staff members were rewarded. The enthusiasm demonstrated by participants, exemplified employee engagement and interaction.

Leila Tomlinson Wareika Basic School

As part of its corporate social responsibility, the Bank continued its sponsorship of charities and other worthy causes in the wider society as part of its Outreach programmes. Of special note is the Bank’s continued relationship with the Leila Tomlinson Wareika Basic School located in Wareika Hills in East Kingston. The Bank has also forged a relationship with the Jamaica Christian Boys Home, an institution established for the care and protection of needy children. These and other worthy projects including the Golden Age Home are sponsored through the kind contributions of the Bank’s caring and generous staff.

CORPORATE CITIZENSHIP

The Bank continued to demonstrate its wider support for the development of manufacturing and exports, and continued its sponsorship of the cash award along with the EXIM Bank’s Trophy to the winner of the Governor General’s Award for Manufacturing and Good Corporate Citizenship at the Jamaica Manufacturers’ Association Annual Awards Banquet.

give.”

Nido Qubein, Author, Speaker, Philanthropist