3 minute read

HOT-MELT PRODUCERS INSPIRED TO PRIORITISE SUSTAINABILITY IN PACKAGING, NONWOVENS, AND CONSTRUCTION

from FEICA CONNECT 53

by FEICA

by John Nelson, Editor, Smithers

Recent analysis of the hot melt sector from Smithers – the leading consultancy for the paper, print, and packaging industries –reveals new challenges for a global market worth $8.21 billion in 2022.

Advertisement

Many of these involve reacting to economic and geopolitical issues, including Covid-19, the rise of e-commerce shipping, and the war in Ukraine; as well as aligning to the wider trend towards sustainability in consumer goods.

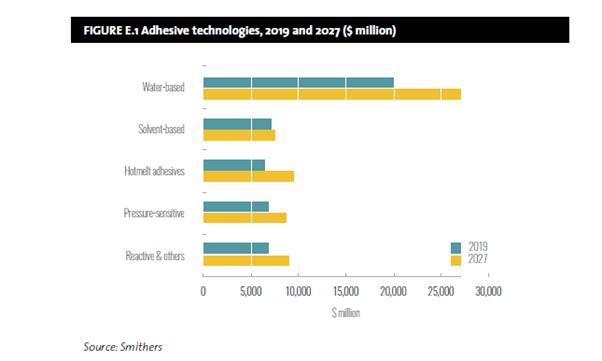

Exclusive data from Smithers’ study The Future of Hot Melt Adhesives to 2027 show that in 2022 Europe consumed a projected 565,000 tonnes of hot malt adhesives. This places the region second in the world, behind Asia. Total consumption worldwide is projected at 2.36 million tonnes of hot melts in 2022, this is forecast to reach 2.77 million tonnes in 2027.

Its analysis also sub-divides the market by core end-use sectors. The three most important for hot melt consumption are:

Packaging (29.4% market share in 2021)

Construction/wood (17.5%)

Nonwoven/hygiene goods (16.8%)

Packaging

In packaging, hot melts are the standard technology for constructing corrugated boxes, folding cartons, and other formats. It is also a segment where calls for greater sustainability are loudest, especially in Europe.

Corrugated has seen some positive effect from Covid, with a surge in demand online shopping and e-commerce delivery helping to compensate for lost volumes of corrugated used in international shipping. Corrugated formats are over 80% of the world e-commerce market and continues to grow strongly (+10.5% year-on-year, Smithers, 2022). In 2023 a total of 30.3 million tonnes of board material will need to be converted into e-commerce boxes.

Recyclability is a key consideration. Many brand owners are trialling replacing existing plastic packaging formats with paperboard alternatives bonded with hot melts. This is not suitable for all segments, but it is a noticeable trend for ambient and less sensitive foods, such as confectionary or savoury snacks.

The wider focus on sustainability is placing a premium on bio-based materials in hot melts, and within fossil-based raw materials on using more solvent-free formulations, where feasible. Biodegradable and monocomponent adhesives are increasingly popular as a means to optimise the rate of recovery for paper fibres at end-of-life.

There are also other benefits hot melts can have in packaging, including for low temperature formulations – which are also economically advantageous given recent energy price rises.

Better performing hot melts which use a smaller volume of adhesive to form an efficient bond can also aid converters looking to cut their carbon footprint. This can be enhanced with more precise adhesive application equipment, such as hot melt stitching platforms.

Construction

Construction includes both the bonding of buildings themselves, as well internal fixtures, and furniture. Recent economic uncertainty and residual Covid lockdowns, especially in China has slowed demand for hot melts in this application; although there have been some rises in DIY, home improvement, and furniture sales. Some countries are also benefitting from government-led Covidrecovery stimulus spending. Still the global economic outlook remains fragile, slowing private investment in construction and impacting demand for hot melts.

Nonwovens

In theory, many different adhesives systems can be used for disposable nonwoven hygiene products, such as solvent-based or waterborne PSAs, but regulatory requirements and extremely fast production lines make hot melts the best fit for this application. The principal hygiene/nonwoven goods are diapers/nappies, female hygiene, and adult incontinence products. The disposable diaper market is the largest product group for hot melts (65-70% of demand by weight of adhesive).

A value growth of about +2% year-on-year is forecast through to 2027, driven mainly by increasing use of hot melts in construction, even though the overall market is expected to stagnate due to higher costs and interest rates. There will also be greater demand for quick-bonding hot melt sets in large surface laminations.

Profitability in this segment has been impacted by increased commoditisation with the main influence to push adhesive prices downwards. As hygiene products often seek to portray themselves as lifestyle brands, there is also a strong increase in demand for green material choice in this segment. There is now new interest in greener hot melts. Major diaper brands are looking to prioritise sustainably sourced ingredients, as well as investigating the plausibility of recycling diapers.

Some manufacturers are also experimenting with ultrasonic bonding as an alternative to adhesives in smaller niche hygiene segments, such as medical fabrics or puppy training mats. There was an increase in demand for these in 2020 as consumers loaded up on essential supplies prior to the implementation of full lockdown orders.

Otherwise in developed markets there has been little deflection in demand for hygiene goods. There has been a slowing of their penetration into some developing markets, in line with a decline in the growth rate for local consumer purchasing power.

The Future of Hot Melt Adhesives to 2027 is available to purchase now from Smithers.

Smithers will also be publishing its latest exclusive data on the complete European adhesives industry later this year and presenting it at the 2023 FEICA Exhibition and Expo (13-15 September 2023) in Tarragona, Spain