4 minute read

By Bryan Slovon

Setting Clients’ Budgets That Work

For clients, budgets are a simple yet overwhelming task. Those in the retirement red zone may not be accustomed to budgeting. Their income is often substantial for their lifestyle, without the worry of their monthly cash flow. Because of this, clients may be reluctant to set one, assuming it will restrict their retirement. Assisting the clients in preparing and maintaining a budget will transform their perception of their long-term finances, for the better.

Reassure: Budgets sustain, not restrict, clients’ monthly income in retirement. Communicate the flexibility of it and that it will be reviewed yearly, during their annual review, to make sure they are receiving the needed cash flow. The budget constructed for them is a draft and never the final version. Relay to clients that they can reach their retirement dreams with an implemented budget.

Define Goals: Identifying clients’ wants and needs in retirement allows them to grasp the bigger picture. They need to understand their general finances and target the necessary amount for monthly bills. Recognizing how much they want to spend on vacations and entertainment is also vital. Clients have their own aspirations with personal finance. Cater their budget to the destination.

Take the Process Step-by-Step: Although budgets are relatively uncomplicated, detailing and managing a successful one is a step-by-step method. After analyzing clients’ retirement goals, determine a figure that works best for them. A successful budget is a work in 4.

5. progress, so beginning their budget four months before they retire is ideal.

Assess each bill, no matter the amount. A credit card statement is just as important as a monthly mortgage payment. Clients will begin to recognize the required cash flow for their retirement dreams. Best case scenario, extra income is leftover for investments or wealth transfer tools.

Improve Cash Flow: Establishing clients’ budget are inconsequential if it does not improve their cash flow. Restructure their debt, while also demonstrating how clients can view their debt differently. Examine their total balance due to gain a better comprehension of their future financial situation. Also, ensure clients have an ample rainy-day fund of $50,000, or 6 months to a year of expenses. Having this emergency fund can significantly protect their budget in a crisis.

Review with clients, around six months after implementing their budget, that there is sufficient cash flow. Again, setting a budget that works is a process and needs to be reconstructed if inadequate. A budget is never a one-time thing.

Set a Deadline: Like any intimidating task, people may procrastinate if there is not an appropriate deadline. Set a time-limit for when the budget is due, which is usually a month. The individual needs ample time to prepare their statements but it’s necessary that they coordinate their financial information promptly. Notify them that there will be some back-and-forth and emphasize the importance of organizing 6.

7. their monthly bills from the past year. They also need to consider their incidentals throughout the year and any additional family expenses.

Simplicity is Key: Setting a budget can be a time-consuming activity. By streamlining the process, it allows the clients to focus on other priorities. Ask your clients if they would prefer their budget as a PDF or an Excel document. Often, the individual will prefer one over the other. Filling out the information directly on the spreadsheet is easiest for both clients and the financial consultant. For each segment, as well as the grand total, the sum should automatically add up in the document. Allow clients to edit the columns and sections so they can cater the budget to their lifestyle. Creating a miscellaneous section, for any extra expenses without a category, will also simplify the process.

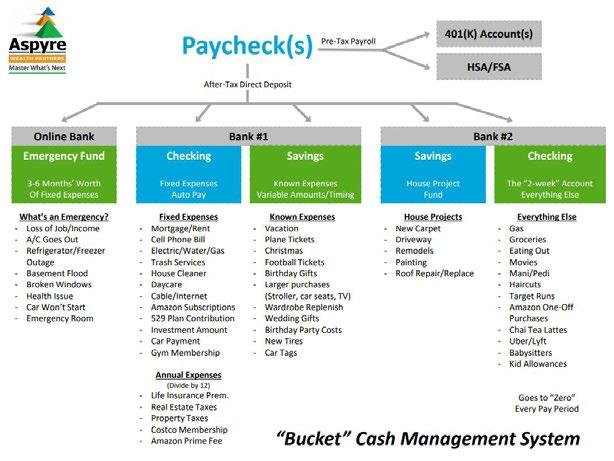

Compartmentalize: A well-presented design promotes readability. For example, the budget on next page allows clients to follow their financial decisions and understand the big picture. Each section is compartmentalized and labeled, allowing the individual to analyze each section without confusion. The data is all on one page, so the viewer can efficiently check the allocation of their monthly income.

Establishing a budget is not the clients’ most critical financial decision, but it is a process that takes planning and commitment. Improving their long-term living situation not only solidifies but enhances the trust they have placed with their financial consultant.

STORE Insignia Items

Bryan Slovon, MRFC®

Bryan S. Slovon, Managing Partner and CEO of Stuart Financial Group, an independent financial planning firm exclusively serving retirees and soon-to be retirees in the DC Metro area. He is a financial planner specializing in retirement planning and wealth preservation to a select group of clients for over 30 years. Contact: (301) 345-1635 www.stuartfg.com

Advisory services offered through J.W. Cole Advisors, Inc. (JWCA). Stuart Financial Group and JWCA are unaffiliated entities. www.store.iarfc.org/#InsigniaItems