5 minute read

Executive summary

Digital transformation in finance has undergone a tectonic change due to Covid-19 one that no business can now escape. But not every organization is looking at the same manner of transformation.

To be sure, there are commonalities.

Advertisement

Finance and technology have rapidly coalesced. Customer behaviour across the board has remarkably shifted, be it digital payments or online purchases of financial products. Sweeping internet and smartphone penetration has enabled this structural change.

Regulators have also tried to keep pace with this change. Keeping customer convenience in mind, they have been supportive of building robust infrastructure. For instance, the India Stack1 initiative can be cited as the single biggest reason for the increased adoption of application programming interfaces (APIs)2 in the banking, financial services and insurance (BFSI) sector.

Licensed financial service providers in the game including fence sitters have read the tea leaves and embraced transformation, given the choice between that and risking extinction. They are relooking their technology architecture and striking relevant partnerships with third parties. The intent is to enable easier integration with APIs offered by third parties, shorten time to market, widen the product suite, increase the target customer base and enhance operating efficiency.

Nevertheless, stark differences exist amongst BFSI players. Not every organization has the same starting point, faces the same limitations or advantages, or serves the same set of customers leading to different outcomes for different sets of players.

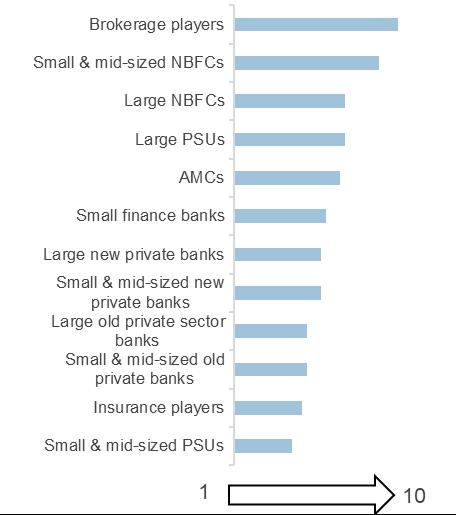

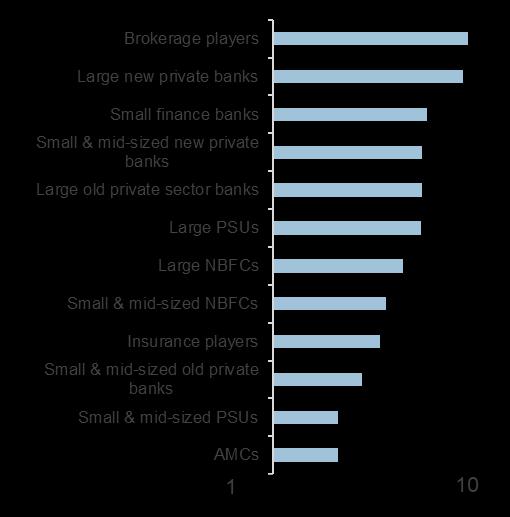

CRISIL Research assessed the impact of digitalisation and API adoption by 12 distinct cohorts of players in the BFSI industry. The study specifically sought to analyse it through two lenses of a) business growth, efficiency and customer experience, and b) financial inclusion

Our analysis shows that the pace of digitalisation and extent of collaboration with digital solution providers3 vary across players.

• Large private banks and, to some extent, large public sector banks (PSBs) are significantly ahead of their counterparts4 in terms of the impact of digitalisation and partnerships on their business.

• At the other end, while small and midsize lenders (banks and NBFCs included) have also ramped up their digital play, the impact on their business and operating efficiency is still modest, at best. For instance, around 70% of them still do not have partnerships with third-party APIs to help fetch bank account statements of loan applicants and standardise them for analysis and underwriting.

1 India Stack is a platform offering open set of APIs for different technology products and frameworks in the financial services space; the APIs/products on the platform are owned by different agencies & regulators

2 Refer to AnnexureI for more details on use cases of API

3 Digital solution providers include digital intermediaries, API providers, technology partners and neo-banks

4 Refer to Annexure II for more details

• Large insurance companies have also stepped up their focus on digitalisation and collaborations. However, with the sheer number of products on offer and the low awareness of insurance in India, the dependence on individual agents continues to be high, especially for life and health insurance.

• Mutual funds and brokerages have successfully leveraged technology and the increasing popularity of equity investments to dramatically expand their customer base.

That said, there still remains headroom for further growth by offering products and solutions relevant to the next rung of customers down the financial pyramid. Our study finds the following specific impacts of digitalisation on incumbents in the BFSI space:

Impact on Business growth, efficiency and customer experience,

1. Target market and product basket of incumbents has expanded, especially in respect of micro, small and medium-sized enterprises (MSMEs) or millennial customers.

2. Distinct improvement in operating efficiency across value chain: Customer on-boarding and credit underwriting have witnessed the highest level of digitalisation amongst processes in the lending value chain. Insurance players have improved their lead management system, digitalised their onboarding process, and implemented automated processes to validate death certificates and reduce the turnaround time in claim settlement.

Impact on Financial inclusion

1. Miles to go for financial inclusion: Access to credit remains a challenge for most MSMEs, as reflected in mere ~4% CAGR growth in active MSME loan accounts across licensed banks and NBFCs during 5-year period ending fiscal 2022. CRISIL Research estimates that less than 20% of the 70 million-odd MSMEs in India have access to formal credit of any kind as of March 2022. On the brighter side, the market has seen a phenomenal increase in disbursements of personal loans lower than Rs 50,000 ticket size, led by NBFCs, mainly on account of traction for BNPL products through online as well as offline channels.

2. Spreads charged to weaker borrowers has not come down: An example of this is the risk premium (as measured by the interest rate paid by them over and above the 10-year G-sec yield) for small-ticket home loans (less than Rs 10 lakh) has hardly witnessed any change in the last four years. This is despite a ~10% drop in operating cost per unit during fiscal 2018 to fiscal 2021 solely on account of digitalisation. This could be partly attributed to risk aversion consequent to the Covid-19 pandemic. Creditworthy customers, on the other hand, have seen a drop in interest rate spreads due to enhanced competition among lenders and extensive data availability.

Finally, what are the implications of digitalisation for regulators?

Regulation is becoming more complex. The regulatory lines especially blur when technology players front-end the transactions while operating in collaboration with a regulated financial entity. For example, for loans extended through embedded lending or the checkout finance model, the digital platforms/mobile applications are front-ended by entities not under regulatory supervision.

As the market evolves, regulators will have to strike a balance between protecting customer interest through regulation and permitting innovation. The Reserve Bank of India (RBI)’s Working Group5 on digital lending, in its November 2021 report, suggested tighter norms for BNPL, recommending that they be treated as part of balancesheet lending. The Working Group has also advocated prohibiting licensed entities from entering into any arrangement involving synthetic structures such as first loss default guarantee (FLDG)6 with digital solution providers that do not bring in regulatory capital. These recommendations by the Working Group are still under consideration of the regulator However, with an aim to protect consumer interest, the RBI notified key rules in August 20227 such as establishing standard practices on responsible pricing through the mention of an annual percentage rate (APR) and setting up of a nodal grievance redressal officer to deal with digital lending related issues

Going forward, more steps to control any systemic risk posed by the rapid adoption of digitalisation and APIs and partnerships between licensed financial service providers and digital solution providers are likely. As seen in advanced countries such as the United States (US) and the United Kingdom (UK), this may result in some entities choosing to apply for a licence with the RBI to avoid any adverse impact due to change in regulations.

Conclusion

Adoption of digitalisation and APIs currently is at best moderate among licensed financial service providers, with larger enterprises leading the way. The pandemic has accelerated the process of digitalisation and building API capabilities among service providers, and we expect the traction to remain strong as service providers intensify efforts to build new revenue streams and/or reduce costs and enter into agreements under the co-lending model. Nevertheless, there is ample scope for leveraging digitalisation to enhance availability of financial products and reduce their cost for underserved or unserved customers, especially with technology lowering operating costs for financiers.

5Report of the Working Group on Digital Lending including lending through online platforms and mobile apps (RBI, November 2021)

6The originator provides guarantee to the licensed entity, which disburses the loan, against default by the borrowers; the quantum of guarantee (as a % of overall loan disbursed) is decided mutually by the two parties.

7 In August 2022, the RBI notified the rules/regulation for immediate implementation basis the recommendations of the Working Group report in November 2021

Impact of digitalisation across cohorts on assessed parameters

(On a scale of 1-10; 1 = low adoption and 10 = high adoption)

Has it expanded the addressable market? Has it enhanced operational efficiency?

Has it helped offer new products?

Has customer service and engagement gone digital?

Has it helped reach more unserved and underserved customers?

Has it lowered the cost for unserved and underserved customers?

Source: CRISIL Research