4 minute read

Finding a path for private equity in the new market environment - Julius Baer

FINDING A PATH FOR PRIVATE EQUITY

IN THE NEW MARKET ENVIRONMENT

Advertisement

By Yves Bonzon, Group Chief Investment Officer at Swiss Wealth Manager Julius Baer.

Yves Bonzon

The world has entered a new paradigm. Since the beginning of the war in Ukraine, geopolitics, rather than economics, have been in charge. For investors, this means bracing for higher average inflation, as well as higher volatility. Portfolios that have been positioned for disinflation and relative political stability for 30 years will now have to shift gears to successfully navigate this new environment.

With inflation becoming a more persistent feature, fighting against capital erosion is more important than ever. The key to surviving an inflationary investment environment is to favour real assets over nominal claims in a portfolio.

One category of investments that could be considered in the context of a well-diversified portfolio, particularly in the current economic and geopolitical landscape, is private assets, most particularly the subset private equity. The relentless hunt for returns in an ultra-low yield environment has made the rise of private markets one of the biggest trends in finance over the last decade. Although the economic playing field is rapidly changing and the era of free money has come to an end, private markets still offer many advantages; they can be especially beneficial to investors in times of increased uncertainty.

The beauty of illiquidity

Besides the challenges posed by high valuations and the prospect of structurally higher interest rates, private equity still harbours plenty of advantages for investors: increasing accessibility, a broadened investment universe and the possibility to invest sustainably via impact investing are likely to increase interest in the asset class. And while the notorious illiquidity of its investments may be a deterrent to some, it may actually be an asset. We know that the average investor tends to underperform a long-term buy-andhold strategy because they trade too frequently, incorrectly rebalance their portfolios, and/or fail to time the market successfully.

Private equity illiquidity may mitigate the effects of these behavioural pitfalls. The illiquid nature and less frequent pricing information of private equity funds protects investors from themselves, helping them to stay invested and, in the end, reap the gains of their long-term investments.

Selection is key

If there is one key takeaway for investors when it comes to private equity, it’s that manager selection is paramount. Top managers who have a knowledge advantage about a particular industry and significant resources within their firms have an increased chance of outperforming public markets. Relying on mediocre private equity managers or,

even worse, selecting bottom-quartile managers will most likely lead to a significant underperformance.

It is true that the most prominent estimates suggest that average global private equity returns have either been in line or have somewhat surpassed public market performance, depending on the investment period and public benchmark taken. ‘Average’ is the key word here, as there is substantial performance dispersion across

geographies and between private equity managers, much more so than among public equity funds.

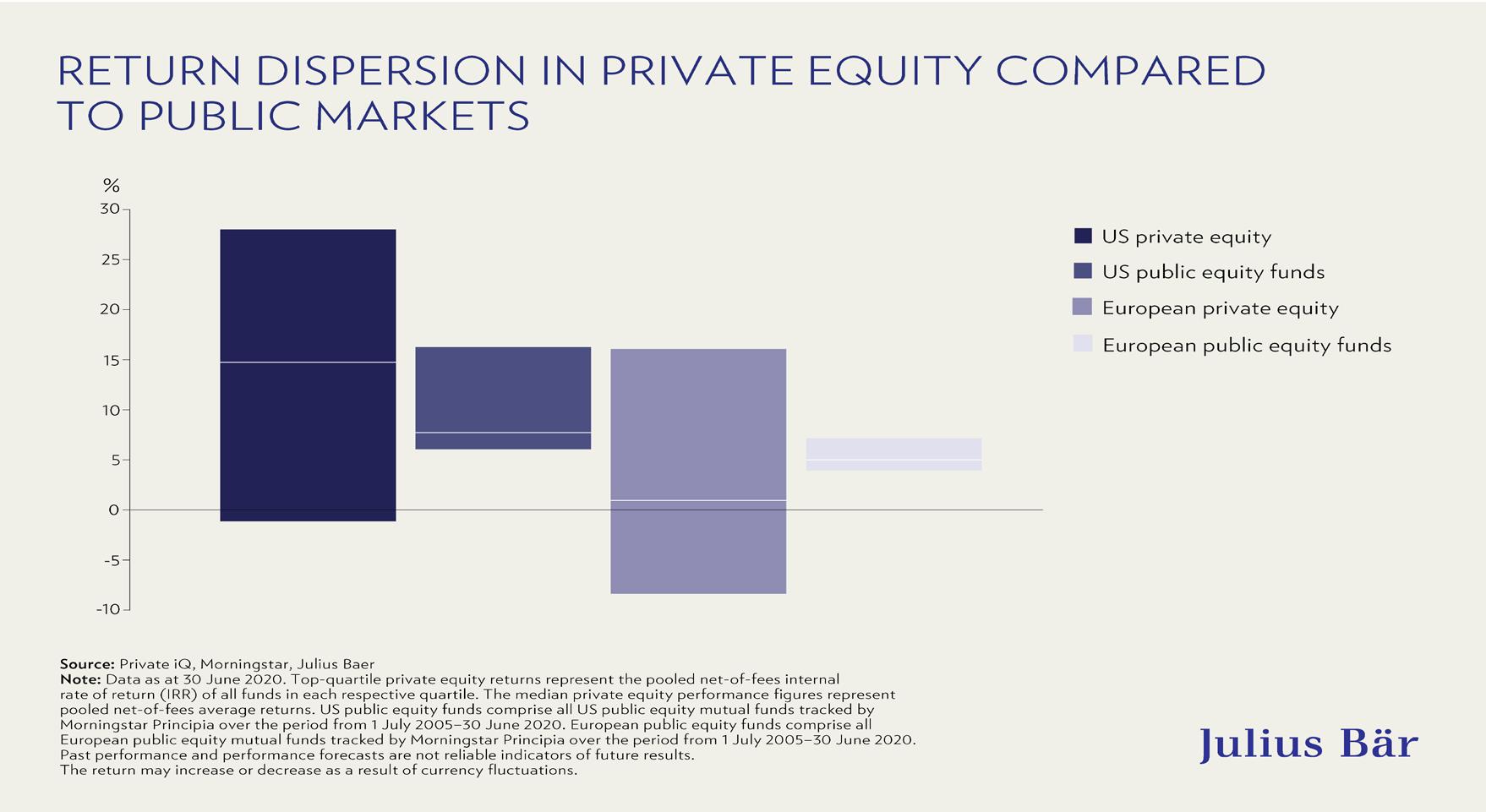

To illustrate just how substantial the performance dispersion is, we show the performance distribution of public and private equity managers in the US and Europe across the 15-year period from July 2005 to June 2020.

While top-quartile private equity managers in the US were able to generate annualised returns of over 28%, the bottom quartile failed to even achieve positive returns. Over the same period, the S&P 500 returned approximately 9% per annum. Also worth mentioning is that return dispersions in public markets are significantly lower than those in private equity funds, with top-to-bottom quartile spreads for public equity funds at around 10%, or one third of the spread in private equity.

The considerable spread between the top and bottom performances of private equity managers can be largely attributed to the managers’ capabilities and their respective investment processes. In the end, the returns in this space are significantly dependent on the sector in which they are active, the size of the portfolio companies

they target, their overall investment selection, as well as the timing of investments and exits. Notably, return dispersion also greatly differs among the various private equity strategies.

As a rule of thumb, the earlier the stage of investment, the higher the risk/return trade-off and the higher the return dispersion between top- and bottom-quartile managers. This means that, in general, investors involved in venture capital funds should be prepared for a greater return dispersion among managers than those involved in, for example, larger buyout funds.

Julius Baer – Bahrain is located on the 3rd floor of the BMB Building, Diplomatic Area. For more information, visit www.juliusbaer.com/international/en/