6 minute read

Between a rock and a hardpalce

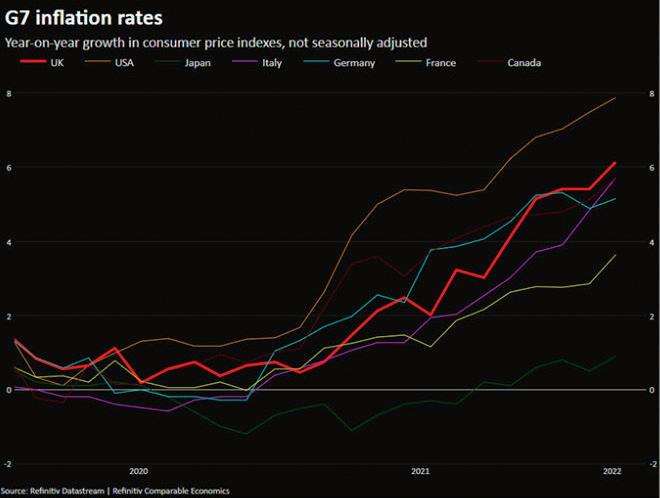

Welcome news last week – interest rates have started to rise on both sides of the Atlantic. The US Federal Reserve and the Bank of England (BoE) finally recognise that the current inflation spike is no transient problem. But it’s premature to put out the flags and give three cheers – these rate rises will do nothing to quash inflation. They were too paltry for that. Central banks on both sides of the Atlantic are sitting between a rock – worries that inflation is starting to run out of control – and a hard place – worries that efforts to control inflation by putting up interest rates are going to be too little, too late. The conventional economists’ way of dealing with inflation is that central banks must raise interest rates. That makes credit more expensive; people will spend less and tighten their belts and might even save a bit with higher rates. That conjunction of events will lead to an economy which runs ‘cooler’. At least, that’s the theory. Only eccentric autocrats such as Turkey’s President Recep Tayyip Erdoğan think that cutting interest rates can quell inflation. Good luck with that Mr President; Turkey’s annual inflation rose to almost 70% in April, the highest for two decades. So in the face of news that US consumer prices rose by 8.5% in March on an annualised basis – the highest in 40 years, the Fed last week “delivered the biggest interest-rate increase since 2000” said Bloomberg; the increase was .50%, meaning that the federal funds rate (the interest rate banks use to lend to each other on a short-term basis) will now be 0.75% to 1%. Jay Powell, chairman of the Fed, told Congress in early March that hindsight “says we should have moved earlier”. The UK’s official inflation rate in March was 7%. So the BoE hiked the UK rate from its previous 0.75% to 1%. The gloom deepened as the Bank also said that inflation will reach more than 10% by the end of this year and a recession will happen – the Bank expects the UK economy to contract by 0.25% in 2023 and remain weak in the next two years. Half a year ago the BoE thought UK inflation would peak at 5%. As for the US, Jay Powell, chairman of the Fed, has long been tarred with his ‘inflation is transitory’ message. The US is now saddled with a negative interest rate of 8% – Dollars held in cash are losing 8% of their purchasing power. As one commentator put it, “while policy is being tightened it could scarcely be called tight”.

Inflating the bubbles

Advertisement

Who has confidence in central bankers’ predictions about the future? After getting things wrong, and egregiously wrong for so long, their credibility is at rock-bottom. Yes, there have been some shocking ‘black swan’ (i.e. unpredictable) events (Russia’s invasion of Ukraine being the most extreme example) but prior to that the US, UK and Eurozone economies handled the Covid-19 pandemic extremely poorly. The knee-jerk lockdowns (still being imposed in China) paralyzed the global economy, created all kinds of supply-chain bottlenecks (some remain, reducing exports and pushing up prices), and prevented all kinds of migrant workforces from taking up jobs. Why are vegetable oils in short supply today and much more expensive? Yes, Ukraine is a major global supplier of sunflower oil and its exports have fallen because of the war. But the palm oil plantations of Malaysia, the world’s second biggest producer of palm oil, a vegetable oil used in many different consumer products, depends on migrant labour to pick the palm oil fruits from their trees. Under Covid restrictions tens of thousands of migrant workers could not travel, Malaysia’s palm oil exports dropped, and prices soared. The war in Ukraine has merely worsened a pre-existing situation. Under Covid, interest rates were cut to zero, and ‘quantitative easing’ programmes, large scale asset buying by four leading central banks

(which began in 2009 ) continued, and expanded their collective balance sheet to more than $26 trillion. The Fed’s balance sheet has expanded from under $1 trillion pre-2008 to close to $9 trillion today. Now the Fed will embark on a reversal of this policy – ‘quantitative tightening’ will start at a monthly pace of $95 billion, more than double the amount it tried to trim its balance sheet during 2017-19. Back then this tightening saw stock prices tumble and the Fed quickly withdrew the tightening, in March 2019. On top of that governments flooded the market with trillions of newly-created fiat money to ‘support’ people who were barred from their employment and businesses that couldn’t function. Sometimes these measures were bizarre – in the UK, the government introduced in August 2020, when the pandemic was still in full flood, the so-called ‘Eat Out to Help Out’ scheme, at a cost of £840 million, whereby the government provided 50% off the cost of food and/ or non-alcoholic drinks at participating restaurants. And the many ‘support’ schemes were inevitably ripe for criminal activities, stealing from the government/taxpayers. In the US, the Secret Service reckons that around $100 billion of pandemic relief funds was stolen. The era of ‘cheap money’ – which for 13 years has fuelled bubbles everywhere, in stock markets, housing markets, cryptocurrencies – may be coming to an end, but like a super-tanker the inertia could take a while to slow down – the bubbles may carry on inflating for a while yet. In the US, unit labour costs – the full cost of employing each worker – are currently rising their fastest in four decades. In Germany, the biggest trade union, IG Metall, which represents 85,000 steelworkers, is now demanding a wage increase of up to 8.2%. The IG Metall wage discussions are widely seen as providing a benchmark for wage increases across the Eurozone. The biggest fear for the European Central Bank (ECB) – tackling record Eurozone inflation of 7.5% – is that this wage negotiation could spark an inflationary ‘wage-price spiral’. In the UK, average house prices are more than 12% higher year-on-year. In the US, the median existing house price is up by 15% year-on-year; “owning a home is becoming unaffordable for many Americans”.

Crisis – what crisis?

Central bankers are human beings like us. They are as sensitive to pointed fingers and accusations of having made a mess of things as any of us. When we are found to have failed in some important task it’s normal to try to brazen it out. So we should not be surprised that in the US the chair of the Fed, Jay Powell, in the UK the BoE’s governor Andrew Bailey, and at ECB’s president Christine Lagarde are all putting on a brave face and hoping that the current high inflation levels can be brought back to their ‘targets’ of 2% without the need for much higher interest rates – which would push the post-Covid economic recovery offcourse. But they are going to need a lot of good luck – they and other central bankers are “flying on a wing and a prayer”. More consumer pain is on the cards. The ‘cost of living crisis’ is likely to mutate into a combined ‘cost of living+recessionary pressures crisis’ – that is, stagflation, a condition in which we will have higher inflation, lower growth, and possible recessions in many economies. Nor should we discount the possibility that central banks, listening to their governments perhaps, may consider letting inflation run a little higher than their target of around 2%. Higher inflation reduces the real value of debts, as it causes the value of a fiat currency to decline over time. Slow, chronic inflation is the most politically palatable way of reducing national debt in a way that is almost imperceptible to the electorate. With the US national debt now more than $30 trillion and crucial mid-term elections in the US set for later this year, President Joe Biden and his economy officials are walking a tightrope suspended over a deep canyon