1 minute read

FOUR WAYS TO BEAT HIGHER INTEREST RATES

by Robin McGlone Managing Director, Move Up Mortgage. (rmcglone@moveupmortgage.com)

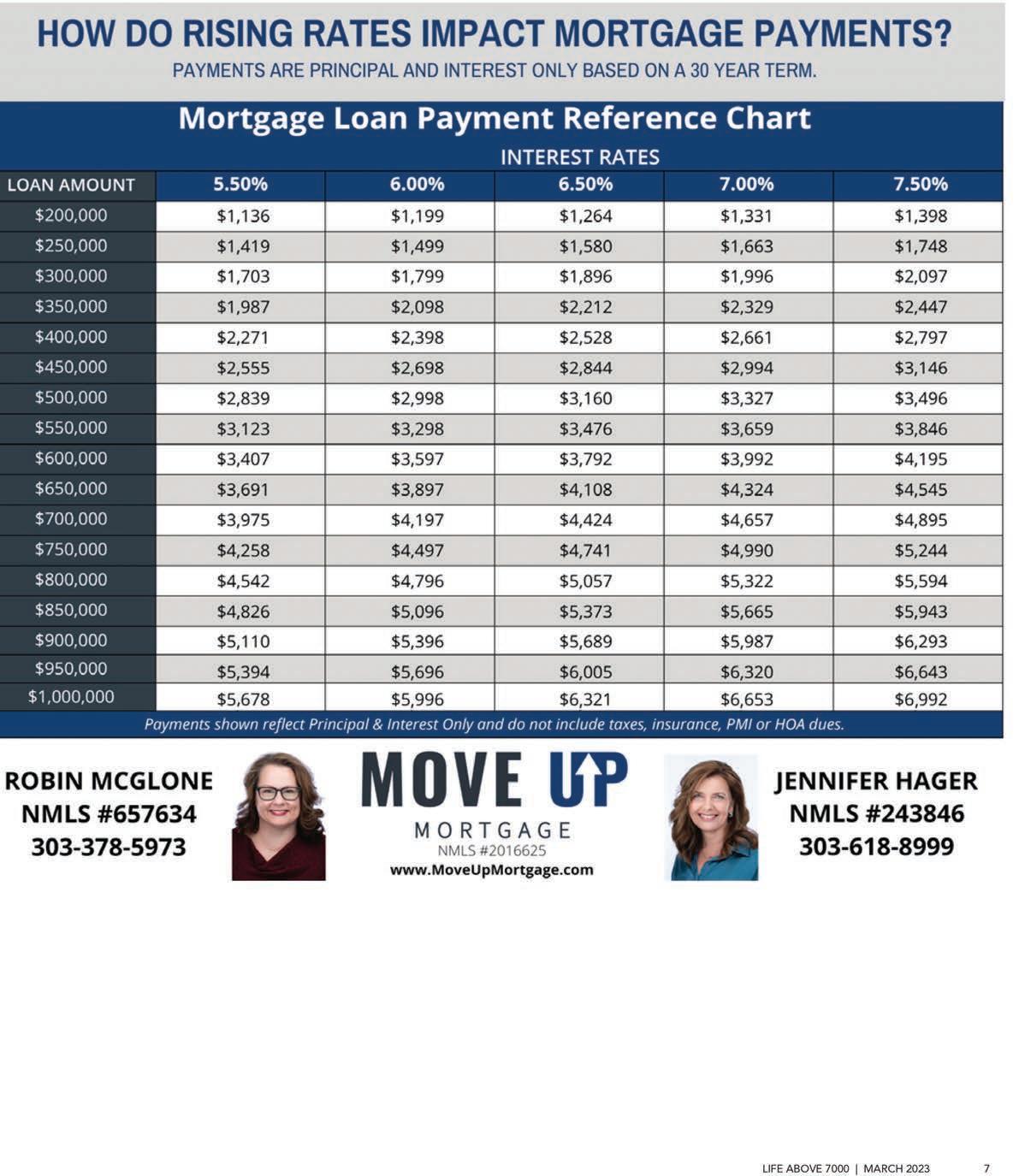

Not a day goes by where I don’t get the question, “when are interest rates going to drop?” There are good indications that mortgage interest rates will drop at some point in the coming 12-24 months, but the short-term view is difficult to predict. In the meantime, how do you maximize your buying power in a higher interest rate market? Let’s talk strategies!

(1) Ask the seller for help. This is not a new idea, but over the last few years, the sellers were in the driver’s seat and had many offers to choose from, so seller “concessions” weren’t viable. Now, Sellers may be agreeable to paying your closing costs, or putting money into an interest rate buydown as part of your sales contract. Lenders are offering some creative options (a 2/1 buydown, where you can lower your rate for the first two years of the loan and save thousands on your payment, for example). Or, a seller could pay for your closing costs, leaving you more money to put down and lower your payment. Most loan programs will allow the seller to contribute 3% of the sales price, and in some cases up to 6%, to help you lower your rate or fund your closing costs.

(2) Maximize your credit score. Credit scores are a SIGNIFICANT factor in the interest rate you are offered for a mortgage. By engaging with a local mortgage lender early in the process, 3-4 months before you want to purchase a home, you can find ways to raise your credit score and ensure you have access to the best rates possible.

(3) Marry your home, date your rate. The good news about mortgages… you can always refinance in the future if rates drop. Reset your expectations, be flexible on the current payment, and work with a good local lender to watch interest rates after you close on your home purchase and execute a refinance when the time is right. Most lenders, like us, offer a discount on refinance costs for repeat customers, too.

(4) Get a second opinion. Lenders have different programs and interest rates vary (somewhat) lender to lender. It never hurts to get a 2nd opinion and compare lenders fees, interest rates and programs. There is a misnomer that your credit will be negatively impacted if two lenders pull your credit report - You have four inquiries within a 90 day period from mortgage companies before you would see any negative change to your credit score.

What we do know from historical data? Getting into the homeownership “game” is typically the best choice, regardless of interest rates. Call a good local mortgage lender to discuss your goals!