3 minute read

New Zealand Research Report | August 2023

Survey results: Tides turn in Auckland, while pressure persists in Wellington

Results of two of our latest CBD office vacancy surveys show occupier demand in the capital city remains resolute, while Auckland is experiencing a shift in demand and supply dynamics that have likely ended a three year slide in survey results.

Advertisement

Leasing activity keeps going

The latest June 2023 survey shows Wellington CBD’s overall vacancy rate is at 5.6%, all but unchanged from the December 2022 figure.Vacancy in the capital city remains at one of the lowest rates recorded since 2008 signifying little respite for tenants searching for space. The current vacancy is well-below the 10-year average rate of 8.6%.

Auckland’s vacancy rate declined to 12.5% in the June 2023 survey, the first decline in vacancy since early 2020, and arresting a run of six consecutive increases that has led to imbalance between demand and supply in favour of tenants.

working conditions. Prime grade premises offer greater floor efficiency, enabling occupiers to easily vary layouts, increase collaboration and breakout spaces, while reducing desk counts. Higher quality premises are also better placed to provide employees with a richer workplace experience and meet increasingly integral Environmental, Social, and Governance (ESG) requirements.

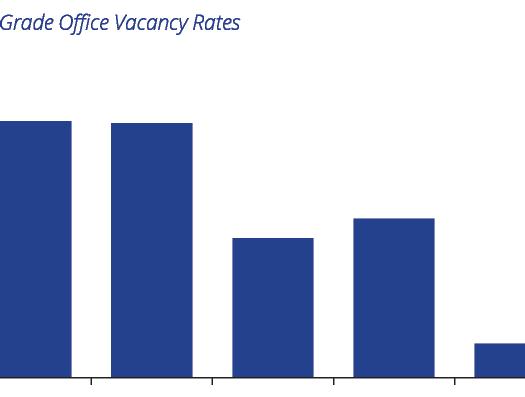

The bifurcation in vacancy rates between prime and secondary grade premises continues. In the first six months of 2023, prime grade vacancy in Auckland’s CBD is at 8.0%, in sharp contrast to the secondary (B-grade and lower) sector where vacancy is at 16.8%. In Wellington, conditions at the prime end of the market are even tighter, with prime-grade vacancy at just 1.7% versus a secondary rate of 6.8%.

While the preference for prime-grade premises is clear, location remains a significant factor for businesses. As a result, demand has been particularly strong within the Auckland CBD's northern precincts. Prime-grade vacancy rates within Britomart, Viaduct Harbour, Wynyard Quarter, and the Victoria Quarter precincts are all below 2%. Northern parts of the CBD Core precinct have also experienced elevated levels of demand bolstered by their proximity to high-quality retail and hospitality. By contrast, vacancy rates within the Western Corridor, Midtown, and Quay Park precincts remain at elevated levels.

A variation in vacancy across Wellington precincts is also evident with overall vacancy ranging from 8.5% in the CBD fringe to 3.3% in Thorndon. Variations in prime grade vacancy rates though are far more limited reflecting the shortage of stock. Prime grade vacancy was recorded in only the Core precinct, at 3.4%, and the CBD fringe at 1.8%.

How do we compare on a Trans-Tasman basis?

Prime grade premises in demand but location remains key

Prime (premium and A-grade) quality premises are in demand, but location remains key in occupier decision making, along with sustainability credentials and seismic ratings. In both centres, businesses continue to prefer higher quality spaces as they adapt to post-COVID

Vacancy rates in New Zealand’s two largest office markets compare favourably with those of Australia’s major centres Figures from the Property Council of Australia show that prime grade vacancy across the six major CBD office markets increased over the second half of 2022 from 12.4% to 12.7%. The increase has been driven by an active development pipeline which has seen new supply outstripping demand.

With the exception of Canberra, all six major Australian centres have prime grade vacancy rates that sit higher than Auckland and Wellington. New Zealand’s capital has the lowest vacancy rate across Australasia.

Of the six major Australian centres, Adelaide has the highest prime grade vacancy at 14.8% while Canberra is the country’s strongest performer at 7.0%. In the two largest markets, Sydney ended 2022 with a prime grade vacancy rate of 11.1% while in Melbourne, the figure was recorded at 12.4%.

Development has increased the quality but is set to slow Auckland and Wellington have seen high levels of construction activity in recent years as the development sector has responded to the demand for new high quality, environmentally sustainable buildings, which provide high seismic ratings.

The delivery of new high-grade space, and the removal of secondary quality accommodation from Auckland’s inventory has resulted in an increase in the overall quality of accommodation, while the total quantity of space has fallen to the lowest levels recorded since December 2008.

Auckland CBD’s prime grade inventory has reached a new record high of 700,560 sqm, increasing by 90,655 sqm over the five years from June 2018. Over the same period, the quantum of secondary grade stock has fallen by 121,875 sqm. As a result, prime grade space now accounts for just under 50% of the total inventory, up from 42% in mid-2018.

In Wellington, development projects have lifted prime grade supply by 60,000 sqm, with higher grade space now comprising 26% of total stock up from approximately 21% in June 2018.

When looking ahead, there is currently approximately 99,000 sqm of new development under construction in Auckland’s CBD and another 26,000 sqm under refurbishment. With a majority of these projects due to complete over the next 24 months, Auckland will experience a spike in supply. However, it is likely that further removals of secondary stock will offset a proportion of this gain. While an increase in vacancy can be expected as projects complete, it is likely to be short lived, particularly as new project commencements are set to slow significantly, given a softening economic backdrop, an escalation in construction costs, and constraints in land supply.

To continue reading and find out more, scan the QR Code