4 minute read

Non-financial disclosure in the EU

COMPARATIVE PE RSPECTIVE

Non-financial disclosure in the EU

Advertisement

The EU initiated sustainability-related recommendations for European entities in the early 1990s. Signed in 1992, against the backdrop of the United Nations’ Rio Declaration 5 , the “Towards Sustainability” treaty aimed at promoting sustainable development with a focus on environmental issues (EU, 1992). This program focused mainly on five specific sectors, namely manufacturing, energy, transport, agriculture, and tourism to monitor and assess their sustainable development. Furthermore, the EU started discussing how traditional reporting could better reflect the environmental impacts and non-financial performance in general. As a result, in 2001, the European Commission (EC) issued recommendations on the recognition, measurement, and disclosure of environmental issues in the annual accounts and annual reports of companies (EC, 2001). Moreover, in 2003, the EC extended the focus to social-related disclosure as well. Directive 2003/51/EC highlighted that when appropriate, companies should include environmental and employee information in their annual reports for stakeholders to understand companies’ respective performance. This directive was labelled as the “Accounts Modernization Directive” and has paved the way for future more stringent regulations. 2014 saw a milestone on the EU’s corporate reporting journey, with the adoption of the Non-Financial Reporting Directive (NFRD).

The NFRD targets large public-interest companies6 in the EU with more than 500 employees and mandates the disclosure of non-financial information (EU, 2014). Compared to voluntary disclosure which has been criticized for lacking standardization and comparability (Hibbitt and Collison, 2004; Jeffrey and Perkins, 2013), the objective of the NFRD is to ensure transparency and comparability. Specifically, the NFRD requires the disclosure of environmental, social, employee, human rights, and anti-corruption and bribery matters (see Table 1). In a first step to supporting companies improve the quality and relevance of their non-financial disclosures, the EC in 2019 issued non-binding guidelines.

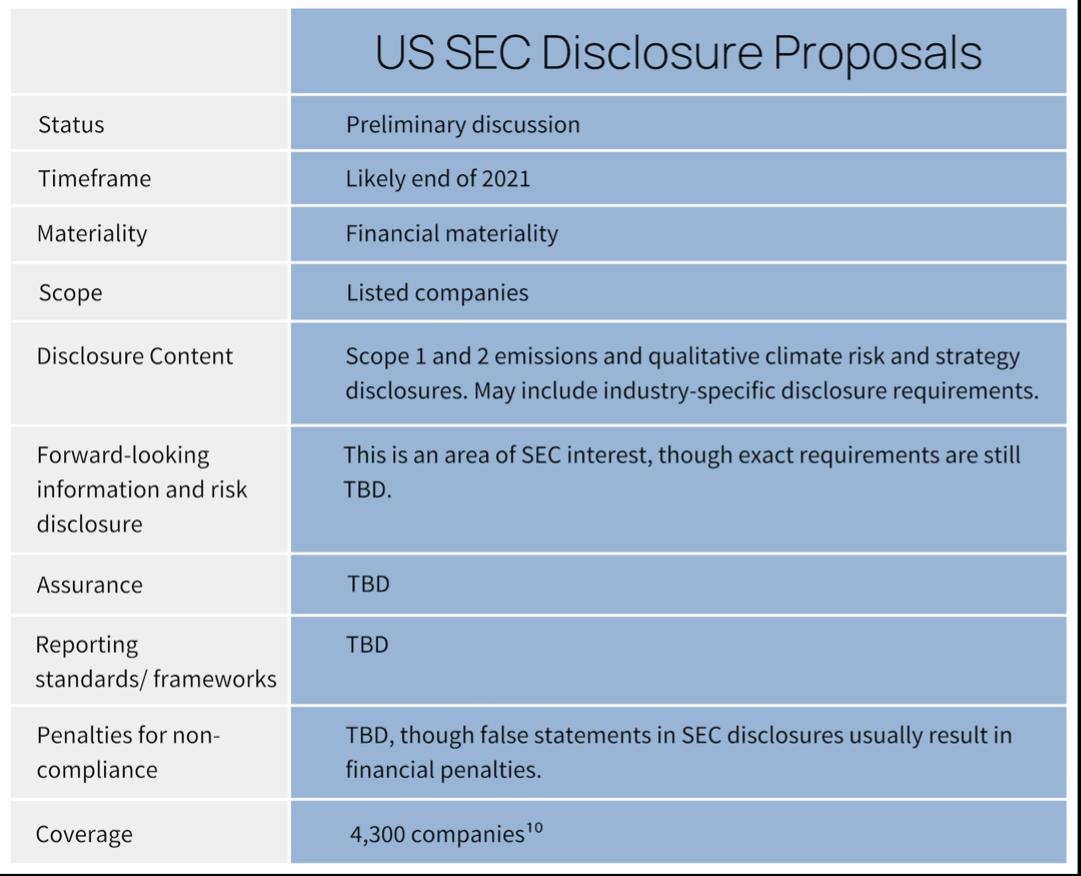

More recently, criticism has been emerging about the guidelines’ effectiveness (Masiero, Arkhipova, Massaro, & Bagnoli, 2020; Korca and Costa, 2021) and several studies identified shortcomings of the NFRD (See Korca et al., 2021; Matuszak & Różańska, 2017; Tarquinio, Posadas & Pedicone, 2020). Against this backdrop and in light of an increasing body of research confirming the superiority of mandatory over voluntary disclosure in providing higher-quality data to investors (Kalesnik, Wilkens & Zink, 2020), the European Commission initiated a revision process for the NFRD in 2020 (EC, 2020). In April 2021, the EC tabled a proposal for the Corporate Sustainability Reporting Directive (CSRD), including significant changes to the EU’s mandatory reporting framework. The CSRD, if adopted in its current form by the colegislators (i.e., the European Council and Parliament) will expand the reporting scope from all large companies to all listed companies (including listed SMEs) by removing the threshold of 500 employees. Furthermore, the new directive adds requirements such as supply chain disclosure, digitalization of information, mandatory assurance, and forward-looking disclosure (see Table 1), which are highlighted as relevant in the vast and growing body of scientific literature on disclosure. For instance, assurance of non-financial disclosure facilitates access to financial capital (García‐Sánchez, Hussain, Martínez‐Ferrero & Ruiz‐Barbadillo, 2019) and decreases capital market information asymmetries (Fuhrmann, Ott, Looks, Guenther, 2017). Furthermore, forward-looking disclosure is useful to all stakeholders to better understand companies’ targets for the future (Kiliç and Kuzey, 2018). Therefore, the CSRD aims to significantly

5https://www.un.org/en/development/desa/population/migration/generalassembly/docs/globalcompact/A_CONF.151_26_Vol.I_Declarati on.pdf 6 The definition of large companies is taken from the Accounting Directive which defines large undertakings as those exceeding at least two of the three following criteria: i) a balance sheet greater than EUR 20,000,000, ii) a net turnover of more than EUR 40,000,000 and iii) an average number of employees above 250 throughout the financial year.

improve availability and quality of sustainability information (EC, 2021a) and respond to concerns raised by market participants and stakeholders in general.

Table 1. Overview of NFRD and CSRD

In contrast to the NFRD, which did not lay down specific reporting requirements (Masiero et al., 2020; Korca & Costa, 2021), the CSRD aims to set clearer requirements. In this regard, the European Financial Reporting Advisory Group (EFRAG) is developing the EU reporting standards for all entities falling under the CSRD scope. In contrast to the nonbinding guidelines for the NFRD, the EU reporting standards will be mandatory and tailored to specific industries and company size. In addition, companies complying with the CSRD will have to report in line with the Sustainable Finance Disclosure Regulation (SFDR) (EU, 2019) and the EU Taxonomy Regulation (EU, 2020). The SFDR aims to increase transparency on sustainability matters by targeting financial institutions and market participants. Specifically, from March 2021, the SFDR requires disclosure of sustainability information both at the entity and product level.

The EU Taxonomy Regulation entered into force in July 2020 setting out six main objectives which entities must meet to be classified as environmentally sustainable.

The EC continues to require companies to measure the impact and identify risks and opportunities related to non-financial aspects. While the previous regulations on non-financial disclosure received criticisms on several aspects, the upcoming directives such as the CSRD might overcome some limitations of previous regulations.