110 minute read

Siam Commercial Bank’s

Siam Commercial Bank’s restructuring highlights Thai banks’ need for complexity

SCB’s launch of its new holding company reflects a trend for banks to become more complex financial firms.

SCB’s planned reorganisation is taking place amidst greater investment in fintech

Expect the next few years to play out like a survival game à la Netflix’s hit series, Squid Game, for Thailand’s traditional banks, highlighted by one of the country’s largest banks reorganising to become a more financial technology-focused firm, analysts said. This reflects the need for local banks to become more complex entities to keep up with the competition.

Siam Commercial Bank’s (SCB) planned reorganisation mirrors a wider trend amongst Thai banks that seek to become more complex financial groups in order to push up profits and retail competitiveness, Fitch Ratings said in a report.

On 22 September, the bank unveiled plans to set up a holding company, SCBX, that will own the group’s operating entities, including SCB. The group aims to complete the transaction by the second quarter of 2022 after securing necessary approvals. The new entity aims to become a regional financial technology conglomerate by 2025 and build a 200 million strong customer base.

Both Fitch Ratings and Moody’s Investors Service expect the reorganisation to have little impact on SCB’s credit. However, Moody’s did warn of potential financial contagion from SCBX’s nonbanking businesses, although the risk is low, the ratings agency added.

Instead, Fitch sees the phenomena as part of a bigger trend of Thai banks being pushed to transform operations due to a challenging operating environment for traditional bank businesses.

Traditional banks in Thailand have long grappled with a prolonged long-growth and low-interest-rate environment that inhibits their growth opportunities. This has led to several transformative mergers and acquisitions in the local banking sector during the past two years, the ratings agency added.

“SCB’s planned reorganisation is taking place amidst greater investment in fintech via standalone subsidiaries and in partnership with key non-bank players,” the Fitch noted in a report.

Indeed, SCB specifically stated in its reorganisation announcement that it aims to become a regional financial technology group spanning a variety of financial businesses and platforms.

“In 2025, the arrival of decentralised finance technology, the expansion and penetration of global platforms into the financial business, post-COVID 19 consumer behaviour, and dramatic changes to regulations will reshape business models, forcing banks into playing roles as intermediaries and making traditional banking fees less and less important. Such conventional roles will no longer satisfy the emerging needs and expectations of consumers,” said Siam Commercial Bank CEO and Chairman of the Executive Committee Arthid Nanthawithaya in the reorganisation announcement.

He added that in four years, consumers’ reliance on banks will wane, which will unavoidably harm the future value proposition for traditional banking investors.

“SCB must no longer limit itself to the traditional banking business, but rather take advantage of its financial strength to accelerate its aggressive expansion into other types of financial businesses that the market demands, build technological capabilities, and manage a large technology platform to keep pace with global players,” Nanthawithaya added, noting that it is crucial to quickly enter the “new arena of competition” in order to survive in the next three to five years.

For their part, Fitch welcomed the proposed restructuring, noting that it will likely improve the central bank’s ability to regulate SCB, as non-traditional and non-financial subsidiaries will be transferred to the holding company.

The ratings agency added that the SCB group’s new format may be replicated at other large financial institutions as their organisational structures become more complex.

SCB must no longer limit itself to the traditional banking business

RETAIL BANKING: CITI GLOBAL WEALTH Citi outlines wealth goals including over $150b AUM across the APAC franchise

Fontainha expounds on Citi’s wealth goals, which include adding $150b AUM across the Asia Pacific franchise and hiring 2,300 more banking professionals in four years’ time.

In January, Citi announced the formation of Citi Global Wealth (CGW), combining its Private Bank and Consumer Wealth Business under one banner, under the leadership of its former global head of investor sales and relationship management, Jim O’Donnell. In Asia, the mantle of head was given to the former retail head, Fabio Fontainha, and private bank head, Steven Lo.

With approximately US$300b in assets under management (AUM), Citi is already amongst the top three wealth managers in APAC — and Fontainha and Lo have been tasked with further driving Citi to maintain and even surpass its position as one of the top wealth managers in Asia (excluding Japan), which boasts of a $42t wealth market.

“Asia is an important source of growth to our firm. It is a source of enhanced returns for Citi; and an area where we see innovation happening at speed. We also believe that our global wealth strategy will benefit from a stronger position in Asia,” Fabio Fontainha, co-head of Citi Global Wealth in Asia Pacific, told the Asian Banking & Finance in an exclusive interview. “We can invest here and take successful ideas to other parts of the firm to drive change and to support the transformation of our bank.”

Goals include adding over US$150b AUM across the APAC franchise by 2025. Hiring plans are also underway with hundreds of new professionals joining Citi APAC as part of its target to add 2,300 professionals in the bank, 1,100 of which are relationship managers and private bankers.

In his first major interview since taking on the co-head role, Fontainha shares his vision for the bank’s wealth business in Asia.

What are the aspirations of Citi Global Wealth in Asia?

“A favourable industry backdrop has set the stage for Citi’s doubling down on wealth management. Global wealth is growing at a rapid pace at over 5% over the past two decades, with Asia growing the fastest at 11% over the same period, driven by China.

“The opportunity is available across all segments, from affluent to ultra-high net worth. Given our presence across the wealth continuum, this plays to our strengths in the region where we have a unique platform.

“We are privileged to have served our wealth management clients in Asia for decades. Our vision now is to further leverage Citi’s aspirational brand and CGW’s strategy is focused on delivering the firm’s global network, high-quality advisory and content, combining it with leading capital markets and product expertise.

“This new business integrates the Citi Private Bank and the Consumer Wealth organisation, including the International Personal Bank, into a single platform that will serve clients from the affluent level all the way through to ultra-high net worth individuals and Family Offices.

“Importantly, we are also coming at this wealth opportunity from a position of strength in the region — Citi is already a top three-wealth manager in Asia with over US$300b in client AUMs.

“We have Wealth Management Hubs in Singapore and Hong Kong that will serve as important centres to grow further the wealth business across the region. The CGW hub strategy will be complemented by our leading digital capabilities. This is important as we think of our clients as individuals who have the ambition to access the best products and solutions and are increasingly agnostic to where that is delivered from.

“Citi is also the most global bank in the world — our bank has on the ground operations in close to 100 countries. This matters more than ever as this global perspective is increasingly a competitive advantage as we discuss wealth opportunities across the world with our clients. The wealth conversation with Asian clients is increasingly global.

“We also have leading institutional businesses in the region — from FX, to hedging, to capital markets, and

Global wealth is growing at a rapid pace at over 5% over the past two decades, with Asia growing the fastest at 11%

Fabio Fontainha, Co-head, Citi Global Wealth APAC

Wealth in Asia, in the last 20 years, rose from $5.1t to $42t

In APAC, personal wealth is growing rapidly, the demographic dynamics remain favourable, including increasing levels of entrepreneurship

Global wealth assets will continue to grow; emerging economies will grow faster than developed markets in the long-term

M&A opportunities. By bringing together the best of our institutional and retail capabilities under CGW, we are uniquely positioned to build a leading integrated Wealth Management business that will serve clients seamlessly along the wealth continuum. Through technology and a deliberate talent strategy, we aspire to introduce these solutions to our clients as they increase their wealth over time.”

How important is Asia in supporting Citi’s global wealth ambitions?

“We see a tremendous opportunity in Asia, specifically in China and across the broader region. Wealth in Asia, in the last 20 years, rose from $5.1t to $42t, excluding Japan. But other changes are happening at the same time as all this personal wealth is created. We will observe, over the next several years, changes coming from decumulation needs, mass customisation algorithms, client-banker remote interaction technologies, portfolio customisation, and more.

“We all know that global wealth assets will continue to grow; emerging economies will grow faster than developed markets in the long-term; and that High Net Worth and Ultra High Net Worth segments will continue to expand dramatically around the region — and we want to purposely be a part of that journey. We can grow with our clients; be able to provide them with all of the banking and wealth products and services they need along the way.

“In this region, personal wealth continues to grow rapidly, the demographic dynamics remain favourable, including increasing levels of entrepreneurship. These factors, combined with several others are leading to an increased demand for wealth management services, which we expect to capture with our differentiated global offer.

What can Citi do differently in wealth, versus peers, given it is a crowded market?

“We are putting the full force of the firm behind this effort. It is all about integrating our platforms and resolve for the gaps we see. We want to create a single, integrated wealth platform that will serve all wealth management clients, providing tailored capabilities for affluent individuals to ultra-high net worth families.

“We have several components that differentiate us from our competitors, and these components put together with purpose can produce a differentiated offer that we expect to resonate with our client segments. Our global footprint, extensive banking and lending services, worldclass capital markets expertise, digital capabilities, research and content capabilities, open architecture, talent base, and aspirational brand are a few of these components. We can offer it all under one distinctive value proposition.

Could you expound about Citi’s hiring plans and targets for CGW?

“By 2025, we are looking to add 2,300 professionals, including 1,100 relationship managers and private bankers, and invest in innovative technology to support growth – much of these will be across Hong Kong and Singapore. We have hired several hundred already in 2021 and new talent is increasingly attracted to our value proposition alongside our ambition.

“We are also looking to add in excess of US$150b AUM across the Asia Pacific franchise by 2025 and further extend our leadership position in the region.

“We have very specific objectives that ultimately will produce great solutions to help our clients grow and achieve their financial objectives. We are building a plan with tangible milestones across technology, digitisation, simplification, and robust controls.

UnionPay QR code evolves traditional banking services from being delivered through branches to e-channels

BEA Hong Kong customers say bye to cards with QR ATM

All they need are their phones to withdraw much-needed cash.

The next time cardholders of Bank of East Asia (BEA) in Hong Kong find themselves service not only reduces the risk of customers losing cards but also safeguards them from the threat of in need of cash, they no longer have to worry about bringing their card, thanks to the new UnionPay QR code cash withdrawal service.

Enabled in all 200 ATMs of BEA across the city, cardholders need only to bring themselves and their phones to access their funds.

To secure their accounts, BEA requires cardholders to present proof of their identity, and can do so through a plethora of customer authentication options: from presenting their biometrics to onetime passwords, and then scanning a QR code via their BEA mobile apps.

Account access is afforded extra protection thanks to the mobile banking access control. Basically, for customers to get their cash, they also need to log on to their mobile app accounts first. card skimming. “We are seeing encouraging take up so far. We believe that the efficient transaction process and extensive ATM support network should drive further uptake,” a spokesperson from BEA told Asian Banking & Finance.

‘Mobile First’

The QR withdrawal service is part of the bank’s “Mobile First” strategy, the spokesperson said.

“Enabling UnionPay QR code cash withdrawal service will improve customer experience and usability, meet the growing demand for mobile banking and payment services and effectively evolve traditional banking services from being delivered through branches to e-channels.” Apart from contactless withdrawals, BEA customers are also given a variety of withdrawal options that will allow them to save time and avoid physical contact amidst an era of ongoing coronavirus infections. For example, the BEA representative said that cardholders can now pre-set withdrawal instructions in advance. This reduces the transaction processing time when compared to traditional ATM card withdrawals. The pre-set withdrawal instructions are secured by various customer authentications such as mobile soft tokens, biometrics and OTPs, the bank added.

The QR The future is cardless

withdrawal BEA also now uses ATMs service is part with fewer touches, catering to of the BEA’s customers who would prefer to ‘Mobile First’ minimise physical contact with strategy public equipment these days. Plans are already underway to expand the service beyond Hong Kong. “Apart from local withdrawal, UPI plans to extend the new cardless service to Macau and Mainland China in the near future. We look forward to becoming one of the pilot banks to offer the service,” the spokesperson said.

Going cardless

In an exclusive correspondence, a BEA spokesperson told Asian Banking & Finance that the

2021 RANKING

1 BANK

DBS BANK

Number of Employees 2021

Number of Employees 2020 2020 RANKING CEO OR COUNTRY HEAD

12,000 OVER 12,000 1 Shee Tse Koon

2

3

4

5 OVERSEA-CHINESE BANKING CORP

STANDARD CHARTERED BANK

UNITED OVERSEAS BANK

CITI SINGAPORE 10,032** 10,032

ABOUT 10,000 9,000 5

3

MORE THAN 9,000 MORE THAN 9,000 2

AROUND 8,500 8,500 4

6 HONG KONG AND SHANGHAI BANKING CORPORATION 3,300 AROUND 3,550 6

7 BNP PARIBAS 2,200 - Helen Wong

Patrick Lee

Wee Ee Cheong

Amol Gupte

Wong Kee Joo

Joris Dierckx

8 MAYBANK SINGAPORE 2,000

9 CREDIT AGRICOLE CORPORATE AND INVESTMENT BANK 1,237 2,000

1,220 8 Dr. John Lee

10 Jean-Pierre Michalowski

10

11

12

13

14 CIMB BANK

BANK OF CHINA

MIZUHO BANK

RHB SINGAPORE

STATE BANK OF INDIA 1,055

955**

>700**

639

124 1,300

955

>700

737

140 9 Victor Lee

11 Cheng Jun*

13

12 Guan Yeow Kwang*

Danny Quah

14 Kishore Kumar Poludasu

15

16

17 ICICI BANK

BANK OF INDIA

UCO BANK 90

77**

42** 110

77

42 15

16

17 Anupam Verma

Geetha Nagarajan*

Rajeev Gupta*

* Info obtained from MAS website ** Info retained from 2020 rankings

TOTAL 61,951 62,363

2021 RANKING BANK

Number of Employees 2021

1 HONG KONG AND SHANGHAI BANKING CORPORATION 29,000

2

3 BANK OF CHINA (HONG KONG)

HANG SENG BANK, Limited 12,557

7,881

4

5 STANDARD CHARTERED BANK

THE BANK OF EAST ASIA, Limited 6,000

5,576

6 CITI HONG KONG 4,300

7 DBS BANK (HONG KONG) Limited 4,000

8 INDUSTRIAL AND COMMERCIAL BANK OF CHINA (ASIA) 3,097

9 DAH SING BANK 3,079

10 CHINA CONSTRUCTION BANK (ASIA) CORPORATION 2,500*

11 OCBC WING HANG BANK 2,104*

12 CHINA CITIC BANK INTERNATIONAL 2,000

13 SHANGHAI COMMERCIAL BANK 1,896

14 CHONG HING BANK 1,758

15 CMB WING LUNG BANK (renamed from Wing Lung Bank) 1,751

16 PUBLIC BANK 1,362

17 CHIYU BANKING CORPORATION 620*

18 TAI SANG BANK 30

Number of Employees 2020

31,000*

12,592

8,515

6,500

5,564

4,200

4,000

3,187*

3,097

2,500*

2,104

2,000

1,633

1,800

1,763

564*

620*

33 2020 RANKING CEO OR COUNTRY HEAD

1 Diana Cesar

2 Sun Yu

3 Louisa Cheang

4 Mary Huen

5 Adrian Li Man-kiu and Brian Li Man-bun

6 Angel Ng

7 Sebastian Paredes

8 Wu Long

9 Hon-Hing Wong (Derek Wong)

10 Jun Zhang

11

12

13 Wu Beng Na

Bi Mingqiang

David Sek-chi Kwok

14

15

16

17

18 Jianxin Zong

Hong Bo

Tan Yoke Kong

Zheng Wei

Cheung Yau Shing

TOTAL 89,511 91,672

*figures retained from previous year’s rankings

Get to know the winners of the Asian Banking & Finance Awards 2021

With the past year providing lots of uncertainties in the financial services sector, banks face intense pressure to continue assisting their clients and help organisations grow their businesses and manage risks amidst the challenging environment. With the ever-changing customer preferences and increased comfort with digital products and services, financial institutions who were able to adapt and leverage digital technology are able to provide to customers and benchmark themselves against market competition.

In recognition of companies that continuously strive to grow and provide services to customers, the 2021 Wholesale Banking Awards, Retail Banking Awards, and Corporate and Investment Banking Awards recognised over 180 exceptional banks across the Asia Pacific.

The awards were handed via digital presentations to the winners due to the pandemic. Winning companies were also interviewed from today, July 29 to August 31 to share their thoughts on winning the most prestigious banking awards in Asia. This year’s winners were judged based on the companies’ achievements, solutions to the challenge experienced in the past year, project effectiveness, and client impact.

The nominations were judged by a panel consisting of John Dovaston, Asia Pacific Financial Services Leader at PwC; Nam Soon Liew, Regional Managing Partner, ASEAN at EY; Kok-Yong Ho, Leader, Financial Services Industry, Southeast Asia & Singapore at Deloitte; and Anton Ruddenklau Partner, Head of Financial Services Advisory Global Co-Leader, Fintech at KPMG International.

“Financial institutions that didn’t back down from the challenge and have adapted amidst the crisis have proved to be on the top of the industry. Asian Banking & Finance awards aim to recognise these exceptional firms and challenge them to provide top-tier products and services to their clients as we continue to move forward into the new normal, “ said Tim Charlton, publisher of Asian Banking & Finance magazine.

Below is a list of all the winning companies. Congratulations!

Wholesale Banking Awards 2021

Abu Dhabi Commercial Bank

UAE Domestic Trade Finance Bank of the Year

Alliance Bank Malaysia Berhad

Malaysia Domestic Initiative of the Year Malaysia Domestic Trade Finance Bank of the Year

Bangkok Bank Public Company Limited

Thailand Domestic Trade Finance Bank of the Year

PT Bank Central Asia Tbk

Domestic API Project of the Year - Indonesia

Bank Nizwa SAOG

Oman Domestic Foreign Exchange Bank of the Year

Bank of Ayudhya PCL (Krungsri)

Thailand Domestic Technology and Operations Bank of the Year Thailand Domestic Initiative of the Year

Bank of China (Hong Kong)

Hong Kong Domestic RMB Internationalisation Initiative of the Year Hong Kong Domestic Trade Finance Bank of the Year Hong Kong Domestic Cash Management Bank of the Year

Bank of the Philippine Islands

Philippines Domestic Trade Finance Bank of the Year Philippines Domestic Cash Management Bank of the Year

Bank SinoPac

Taiwan Domestic Remittance Initiative of the Year

Barclays Bank PLC UAE Branch

UAE International Cash Management Bank of the Year

Cathay United Bank

Taiwan Domestic Cash Management Bank of the Year Taiwan Domestic Trade Finance Bank of the Year

CB Bank

Myanmar Domestic Cash Management Bank of the Year Myanmar Domestic Trade Finance Bank of the Year

CIMB Bank Berhad, Singapore branch

Singapore International COVID Management Initiative of the Year

Commercial Bank of Ceylon PLC

Sri Lanka Domestic Trade Finance Bank of the Year

CTBC Bank

Taiwan Domestic Foreign Exchange Bank of the Year Taiwan Domestic Project Finance Bank of the Year

DBS Bank Taiwan

Taiwan International Initiative of the Year Taiwan International Cash Management Bank of the Year

DBS Bank

Singapore Domestic Project Finance Bank of the Year Singapore Domestic Technology and Operations Bank of the Year

DBS Bank India

India International Cash Management Bank of the Year

Habib Bank Limited

Pakistan Domestic Cash Management Bank of the Year Pakistan Domestic Project Finance Bank of the Year

Hang Seng Bank

Hong Kong Domestic AI Initiative of the Year Hong Kong Domestic COVID Management Initiative of the Year

HSBC Bank (China) Company Limited

China International Cash Management Bank of the Year

The Hong Kong and Shanghai Banking Corporation Limited

Hong Kong International Cash Management Bank of the Year

The Hong Kong and Shanghai Banking Corporation Limited (Thailand Branch)

Thailand International Cash Management Bank of the Year

HSBC Bank (Vietnam) Limited

Vietnam International COVID Management Initiative of the Year Vietnam International Trade Finance Bank of the Year

ICICI Bank

India Domestic COVID Management Initiative of the Year India Domestic Foreign Exchange Bank of the Year India Domestic Liquidity Management Initiative of the Year India Domestic Trade Finance Bank of the Year

Indusind Bank Ltd

India Domestic Cash Management Bank of the Year

KASIKORNBANK

Thailand Domestic Cash Management Bank of the Year Thailand Domestic COVID Management Initiative of the Year

Kotak Mahindra

India Domestic Digital Onboarding Initiative of the Year

LaoVietBank

Laos Domestic Initiative of the Year

Maybank Investment Bank

Malaysia Domestic COVID Management Initiative of the Year

Maybank Investment Bank Berhad

Malaysia Domestic Project Finance Bank of the Year

Meghna Bank Ltd.

Bangladesh Domestic Initiative of the Year

National Development Bank

Sri Lanka Domestic Project Finance Bank of the Year Sri Lanka Domestic Cash Management Bank of the Year

Nabil Bank

Nepal Domestic Technology and Operations Bank of the Year

Nepal SBI Bank

Nepal Domestic COVID Management Initiative of the Year Nepal Domestic Initiative of the Year

OCBC Bank (Malaysia) Berhad

Malaysia International Cash Management Bank of the Year Malaysia International Project Finance Bank of the Year

OCBC NISP

Indonesia Domestic Cash Management Bank of the Year

Prime Bank

Bangladesh Domestic Cash Management Bank of the Year

Bank Mandiri

Indonesia Domestic Trade Finance Bank of the Year

RCBC

Philippines Domestic COVID Management Initiative of the Year

RHB Banking Group

Malaysia Domestic Foreign Exchange Bank of the Year

Sacombank

Vietnam Domestic Technology and Operations Bank of the Year Vietnam Domestic Trade Finance Bank of the Year

Saigon-Hanoi Commercial Joint Stock Bank

Vietnam Domestic COVID Management Initiative of the Year

Standard Chartered Bank

UAE International Trade Finance Bank of the Year

Standard Chartered Bank

Singapore International Initiative of the Year Singapore International Technology & Operations Bank of the Year Singapore International Cash Management Bank of the Year

Standard Chartered Bank (Vietnam) Limited

Vietnam International Cash Management Bank of the Year Vietnam International Initiative of the Year

State Bank of India, Australia

Australia International Initiative of the Year

Taishin International Bank

Taiwan Domestic M&A Initiative of the Year

Turk Ekonomi Bankasi A.S.

Turkey Domestic Cash Management Bank of the Year

United Arab Bank

UAE Domestic Technology and Operations Bank of the Year

United Overseas Bank (Malaysia) Berhad

Malaysia International Trade Finance Bank of the Year Malaysia International Initiative of the Year

UOB

Brunei International Project Finance Bank of the Year

UOB

Singapore Domestic Initiative of the Year

YES BANK

India Domestic Transaction Banking Initiative of the Year

Retail Banking Awards 2021

ABA Bank

Domestic Retail Bank of the Year - Cambodia

Affin Bank Berhad

Initiative of the Year - Malaysia Start-up Banking Initiative of the Year - Malaysia Millennial product Initiative of the Year - Malaysia

Ahli Bank S.A.O.G.

Domestic Retail Bank of the Year - Oman

Al Rajhi Bank

Digital Banking Initiative of the Year - Saudi Arabia Mobile Banking & Payment Initiative of the Year - Saudi Arabia

Albaraka Islamic Bank

Marketing & Brand Initiative of the Year - Bahrain

Alliance Bank Malaysia Berhad

Financial Inclusion Initiative of the Year - Malaysia Mobile Banking & Payment Initiative of the Year - Malaysia Service Innovation of the Year - Malaysia

AmBank Group

SME Bank of the Year - Malaysia

Ardshinbank CJSC

Domestic Retail Bank of the Year - Armenia

Aspire

Fintech Startup of the Year - Singapore

Asakabank

Domestic Retail Bank of the Year - Uzbekistan

au Jibun Bank Corporation

Wealth Management Platform of the Year - Japan

AU Small Finance Bank

Digital Banking Initiative of the Year - India

Axis Bank Limited

Financial Inclusion Initiative of the Year - India

Baiduri Bank

Domestic Retail Bank of the Year - Brunei Marketing & Brand Initiative of the Year - Brunei

BIDV

SME Bank of the Year - Vietnam

Bank of Ayudhya Public Co. Ltd.

Marketing & Brand Initiative of the Year - Thailand Financial Inclusion Initiative of the Year - Thailand

Bank of China (Hong Kong) Limited

Mobile Banking & Payment Initiative of the Year - Hong Kong

The Bank of East Asia, Limited

Domestic Retail Bank of the Year - Hong Kong Initiative of the Year - Hong Kong

Bank SinoPac

Mobile Banking & Payment Initiative of the Year - Taiwan Open Banking Initiative of the Year - Taiwan Branch Innovation of the Year - Bronze

Banque Misr

COVID Management Initiative of the Year - Egypt Digital Wallet Initiative of the Year - Egypt

BDO Foundation

COVID Management Initiative of the Year - Philippines

BDO Private Bank

Wealth Management Platform of the Year - Philippines

BDO Unibank

Marketing & Brand Initiative of the Year - Philippines

Cebuana Lhuillier Rural Bank, Inc.

Rural/Cooperative Bank of the Year - Philippines

Chang Hwa Commercial Bank Ltd

Banking for Women Initiative of the Year - Taiwan

CIMB Bank Berhad, Singapore branch

Website of the Year - Singapore Consumer Finance Product of the Year - Singapore

CIMB Philippines

Virtual Bank of the Year - Philippines Strategic Partnership of the Year - Philippines

CIMB Thai Bank Public Company Limited

Digital Banking Initiative of the Year - Thailand Wealth Management Platform of the Year - Thailand

Commercial Bank of Ceylon PLC

Digital Banking Initiative of the Year - Sri Lanka

Commercial Bank of Dubai

Domestic Retail Bank of the Year - UAE Consumer Finance Product of the Year - UAE

PT Bank DBS Indonesia

Service Innovation of the Year - Indonesia

DBS Bank

Digital Banking Initiative of the Year - Singapore Mobile Banking & Payment Initiative of the Year - Singapore COVID Management Initiative of the Year - Singapore

DBS Bank Taiwan

Credit Card Initiative of the Year - Taiwan Digital Banking Initiative of the Year - Taiwan Employer Award of the Year - Gold

HBL

Mobile Banking & Payment Initiative of the Year - Pakistan

HDBank

Mid-sized Domestic Retail Bank of the Year - Vietnam Digital Banking Transformation of the Year - Vietnam

HKT Flexi Limited

New Consumer Lending Product of the Year - Hong Kong Consumer Finance Product of the Year - Hong Kong

HNB FINANCE PLC

Marketing & Brand Initiative of the Year - Sri Lanka

Hong Leong Finance Limited

ASEAN Finance Company of the Year

HSBC

Debit Card Initiative of the Year - Hong Kong

HSBC Amanah Malaysia Berhad

Credit Card Initiative of the Year - Malaysia

HSBC Bank (China) Company Limited

International Retail Bank of the Year - China Wealth Management Platform of the Year - China

HSBC Bank (Singapore) Limited

Credit Card Initiative of the Year - Singapore Wealth Management Platform of the Year - Singapore

HSBC Bank (Vietnam) Ltd

Marketing & Brand Initiative of the Year - Vietnam

HSBC India

Corporate Social Responsibility & Green Program of the Year - Gold

HSBC Philippines

International Retail Bank of the Year - Philippines

HSBC Sri Lanka

International Retail Bank of the Year - Sri Lanka

PT. Bank HSBC Indonesia

Marketing & Brand Initiative of the Year – Indonesia

ICICI Bank

COVID Management Initiative of the Year - India Domestic Retail Bank of the Year - India

IndusInd Bank Ltd.

Mobile Banking & Payment Initiative of the Year - India Open Banking Initiative of the Year - India

Jusan Bank

Digital Banking Initiative of the Year - Kazakhstan Online Banking Initiative of the Year - Kazakhstan

JS Bank Limited

SME Bank of the Year - Pakistan Consumer Finance Product of the Year - Pakistan

KBZ Bank

COVID Management Initiative of the Year - Myanmar New Consumer Lending Product of the Year - Myanmar

Malayan Banking Berhad

Marketing & Brand Initiative of the Year - Malaysia

Maybank Singapore Limited

Marketing & Brand Initiative of the Year - Singapore

Mutual Trust Bank Limited

Banking for Women Initiative of the Year - Bangladesh Core Banking System Initiative of the Year - Bangladesh

National Bank of Vanuatu Limited

Financial Inclusion Initiative of the Year - Vanuatu

National Development Bank PLC

Domestic Retail Bank of the Year - Sri Lanka SME Bank of the Year - Sri Lanka

Ngern Tid Lor Public Company Limited

Finance Company of the Year - Thailand

OCBC Bank

ASEAN SME Bank of the Year

OCBC NISP

SME Bank of the Year – Indonesia

Philippine National Bank

Mortgage and Home Loan Product of the Year - Philippines

PrimeCredit Limited

Finance Company of the Year - Hong Kong

PT Bank CIMB Niaga Tbk – Emerging Business Banking

Digital Banking Initiative of the Year - Indonesia

PT Bank CTBC Indonesia

New Consumer Lending Product of the Year - Indonesia

PT Bank Permata, Tbk

Mortgage and Home Loan Product of the Year - Indonesia Strategic Partnership of the Year - Indonesia

PT Visionet Internasional (OVO)

Financial Inclusion Initiative of the Year - Indonesia COVID Management Initiative of the Year - Indonesia

PT. Bank Commonwealth

Wealth Management Platform of the Year - Indonesia

PT. Bank Maybank Indonesia

Core Banking System Initiative of the Year - Indonesia

PT. Bank Muamalat Indonesia

Mobile Banking & Payment Initiative of the Year - Indonesia

Public Bank Berhad

Domestic Retail Bank of the Year - Malaysia COVID Management Initiative of the Year - Malaysia

Rakbank

Mobile Banking & Payment Initiative of the Year - UAE

RCBC Bankard

Mobile Banking & Payment Initiative of the Year - Philippines

Rizal Commercial Banking Corporation

Debit Card Initiative of the Year - Philippines Mid-sized Domestic Retail Bank of the Year - Philippines

Robinsons Bank Corporation

Consumer Finance Product of the Year - Philippines Service Innovation of the Year - Philippines

Sacombank

Digital Banking Initiative of the Year - Vietnam

Saigon-Hanoi Commercial Joint Stock Bank

Corporate Social Responsibility & Green Program of the Year - Bronze Banking for Women Initiative of the Year - Vietnam

OCBC Bank & SAS Institute

Branch Innovation of the Year - Silver Online Banking Initiative of the Year - Singapore

SDB Bank

Website of the Year - Sri Lanka

Shinhan Bank Vietnam

International Retail Bank of the Year - Vietnam

Siam Commercial Bank PCL.

Domestic Retail Bank of the Year - Thailand Strategic Partnership of the Year - Thailand

SME Bank of Cambodia PLC.

SME Bank of the Year - Cambodia

Standard Chartered Bank Malaysia Berhad

Wealth Management Platform of the Year - Malaysia

Standard Chartered Bank

International Retail Bank of the Year - India

Standard Chartered, Sri Lanka

Credit Card Initiative of the Year - Sri Lanka

Standard Chartered Bank (Hong Kong) Limited

Digital Banking Initiative of the Year - Hong Kong Employer Award of the Year - Silver Employer Award of the Year - Hong Kong International Retail Bank of the Year - Hong Kong

Standard Chartered Bank (Taiwan) Limited

Corporate Social Responsibility & Green Program of the Year - Silver International Retail Bank of the Year - Taiwan Wealth Management Platform of the Year - Taiwan

STATE BANK OF INDIA, MALDIVES

International Retail Bank of the Year - Maldives COVID Management Initiative of the Year - Maldives

Taishin International Bank

Service Innovation of the Year - Taiwan COVID Management Initiative of the Year - Taiwan New Consumer Lending Product of the Year - Taiwan

The Hongkong and Shanghai Banking Corporation Limited

International Retail Bank of the Year - Bangladesh

TrueMoney Vietnam

Digital Wallet Initiative of the Year - Vietnam

U Microfinance Bank Limited

Rural/Cooperative Bank of the Year - Pakistan

uab bank Berhad

Mid-sized Domestic Retail Bank of the Year - Myanmar

Union Bank of the Philippines

Financial Inclusion Initiative of the Year - Philippines SME Bank of the Year - Philippines Credit Card Initiative of the Year – Philippines

United Overseas Bank (M) Berhad (UOBM)

International Retail Bank of the Year - Malaysia Digital Banking Initiative of the Year - Malaysia

UOB Thailand

International Retail Bank of the Year - Thailand

United Overseas Bank (Vietnam) Limited

New Consumer Lending Product of the Year - Vietnam

United Overseas Bank Limited

Banking for Women Initiative of the Year - Singapore Branch Innovation of the Year - Gold Domestic Retail Bank of the Year - Singapore Investment Product Innovation of the Year - Singapore

Vietnam Public Joint Stock Commercial Bank Initiative of the Year for Account Services - Vietnam

VPBank Finance Company Limited

Employer Award of the Year - Bronze Finance Company of the Year - Vietnam

WeLab Bank

Virtual Bank of the Year - Hong Kong Financial Inclusion Initiative of the Year - Hong Kong Corporate and Investment Banking Awards 2021

Aktif Bank

Innovative Deal of the Year - Turkey Project Infrastructure Finance Deal of the Year - Turkey

Al Rajhi Bank

Innovative Deal of the Year - Saudi Arabia

Asia Green Development Public Company Limited

Innovative Deal of the Year - Myanmar

Bank Muscat SAOG

Corporate & Investment Bank of the Year - Oman Innovative Deal of the Year - Oman Mergers and Acquisitions Deal of the Year - Oman

BankDhofar

Technology Innovation of the Year - Oman

BankIslami Pakistan Limited

Syndicated Deal of the Year - Pakistan

BDO Capital & Investment Corporation

Mergers and Acquisitions Deal of the Year - Philippines Corporate & Investment Bank of the Year - Philippines Domestic Project Infrastructure Finance Deal of the Year - Philippines

BPI Capital Corporation

Real Estate Equity Deal of the Year - Philippines Innovative Deal of the Year - Philippines

Bualuang Securities Public Company Limited

Securities House of the Year - Thailand

China Bank Capital Corporation

Debt Deal of the Year - Philippines Syndicated Loan of the Year - Philippines

CTBC Bank

Mergers and Acquisitions Deal of the Year - Taiwan

DBS

Mergers and Acquisitions Deal of the Year - Singapore Corporate & Investment Bank of the Year - Singapore Corporate Client Initiative of the Year - Singapore Equity Deal of the Year - Singapore Green Deal of the Year - Singapore

FAYSAL BANK LIMITED

Innovative Deal of the Year - Pakistan

First Abu Dhabi Bank (FAB)

Corporate and Investment Bank of the Year - UAE Green Deal of the Year - UAE

Garanti BBVA

Corporate & Investment Bank of the Year - Turkey Green Deal of the Year - Turkey Project Infrastructure Finance Deal of the Year - Turkey

Habib Bank Limited - HBL

Equity Deal of the Year - Pakistan

HDFC Bank Limited

Corporate & Investment Bank of the Year - India

Kenanga Investment Bank Berhad

Project Infrastructure Finance Deal of the Year - Malaysia

Kings Financial Capital

Corporate Client Initiative of the Year - UAE

Kotak Mahindra Bank Limited

Debt Deal of the Year - India Equity Deal of the Year - India

Kuwait International Bank (KIB)

Debt Deal of the Year - Kuwait

Mashreqbank psc

Debt Deal of the Year - UAE Syndicated Loan of the Year - UAE

Maybank Kim Eng

Equity Deal of the Year - Malaysia Syndicated Loan of the Year - Malaysia Debt Deal of the Year - Malaysia

Meezan Bank

Renewable Energy Bank of the Year - Pakistan Green Deal of the Year - Pakistan

National Bank of Pakistan

Corporate & Investment Bank of the Year - Pakistan Corporate Client Initiative of the Year - Pakistan Debt Deal of the Year - Pakistan Project Infrastructure Finance Deal of the Year - Pakistan

National Development Bank PLC

Corporate & Investment Bank of the Year - Sri Lanka Corporate Client Initiative of the Year - Sri Lanka Project Infrastructure Finance Deal of the Year - Sri Lanka

NMB Bank Ltd.

Green Deal of the Year - Nepal

Philippine National Bank

Green Deal of the Year - Philippines Consumer Equity Deal of the Year - Philippines

PT Bank CIMB Niaga Tbk

Corporate & Investment Bank of the Year - Indonesia Corporate Client Initiative of the Year - Indonesia Syndicated Loan of the Year - Indonesia

QINVEST LLC

Innovative Deal of the Year - Qatar

RCBC Capital Corporation

Cross-border Project Infrastructure Finance Deal of the Year - Philippines Debt Deal of the Year - Philippines

RHB

Islamic Equity Deal - Malaysia

SB Capital Investment Corporation

Corporate Client Initiative of the Year - Philippines

SBI Capital Markets Limited

Mergers and Acquisitions Deal of the Year - India

Siam Commercial Bank PCL.

Corporate & Investment Bank of the Year - Thailand Debt Deal of the Year - Thailand Mergers and Acquisitions Deal of the Year - Thailand

SinoPac Securities Corporation

Debt Deal of the Year - Taiwan Green Deal of the Year - Taiwan

Sohar International Bank SAOG

Debt Deal of the Year - Oman Equity Deal of the Year - Oman

Taipei Fubon Commercial Bank Co., Ltd.

Innovative Deal of the Year - Taiwan Syndicated Loan of the Year - Taiwan

Taishin Securities Co., Ltd.

Management Buyout of the Year - Taiwan Securities House of the Year - Taiwan

Tan Viet Securities Incorporation

Securities House of the Year - Vietnam

The Bank of Punjab

Project Infrastructure Finance Deal of the Year - Pakistan

TISCO Securities Company Limited

Equity Deal of the Year - Thailand

UOB

Innovative Deal of the Year - Singapore Debt Deal of the Year - Singapore Debt Deal of the Year - China Syndicated Loan of the Year - Singapore

Standard Chartered Bank (Hong Kong) Limited Standard Chartered Bank (Hong Kong) Limited Standard Chartered Bank (Hong Kong) Limited

BDO Capital & Investment Corporation BDO Foundation

BDO Private Bank BDO Unibank

HSBC Bank (China) Company Limited

HSBC Philippines HSBC Amanah Malaysia Berhad

HSBC Indonesia

HSBC Philippines HSBC Indonesia

CIMB Bank Berhad, Singapore branch au Jibun Bank Corporation

Nepal SBI Bank OCBC Bank

Bank of China (Hong Kong) Philippine National Bank

SME Bank of Cambodia PLC.

The Bank of East Asia, Limited

Union Bank of the Philippines PrimeCredit Limited

UOB

UOB Thailand

Bank Mandiri PT Bank Permata

BCA HBL

Standard Chartered India

BIDV

CIMB Thai Bank Public Company Limited CIMB Niaga

Affin Bank Berhad

UOB

RCBC Bankard

RCBC

United Overseas Bank (M) Berhad United Overseas Bank (M) Berhad Ngern Tid Lor Public Company Limited

Siam Commercial Bank PCL.

HSBC Amanah Malaysia wins award for leading sustainability innovation

HSBC Amanah Malaysia began its sustainability journey in 2017 as one of the earliest adopters of Malaysia’s central bank, Bank Negara Malaysia’s Valuebased Intermediation framework aimed at encouraging Islamic banks in Malaysia to shift to a new and holistic mindset that considers the impact of banking on both the people and the planet.

The bank’s commitment to sustainability was further strengthened in 2020 when it embarked on a 24-month transformation to become HSBC Group’s first sustainable bank by 2022. This is in line with the global banking group’s wider ambition to transform the group’s operations and supply chain to net-zero by 2030, and subsequently become a net-zero financier by 2050 or sooner.

The Credit Card Initiative of the Year - Malaysia 2021 award for HSBC Amanah Credit Card-i is recognition of HSBC Amanah’s leadership position through product innovation to influence customers and the broader community on sustainability and encouraging collective action. The award underlines HSBC’s long-term commitment to driving a sustainable future from finances, to well-being and the environment—all these whilst delicately balancing continued shareholder growth and return.

Impacting change by inspiring inclusive action As part of a broader strategy within the bank to affect change internally and externally towards a sustainable future, HSBC Amanah Credit Card-i’s new ESG (Environmental, Social, and Governance) proposition was the first amongst international Islamic banks in Malaysia.

For every charitable donation made by cardholders on their HSBC Amanah Credit Cards, HSBC will donate 1% of the charity spend to selected local charities or nonprofit organisations. The charities currently supported include the Global Environment Centre, Yayasan Chow Kit, Pintar Foundation and Pertiwi Soup Kitchen, in alignment with different pillars within the United Nations Sustainable Development Goals.

Together with the ESG proposition, HSBC has partnered with a social business, Incitement, to create a dedicated digital platform for customers to contribute to local charities and non-profit organisations supported by HSBC. The partnership allows the bank to leverage on digital capabilities to further drive awareness and accessibility of local charities.

Through the platform, customer contributions are 100% transparent on where donations are contributed. Customers will also receive automatic updates regarding the progress and, at the end of each charitable cause, a summarised impact report will be made available on the platform.

Ultimately, this creates a win-win outcome for customers who want to lend a hand to communities and causes that matter to them – whether through monetary contributions or volunteerism – and the people and organisations who receive the aid.

HSBC Switches To Recycled Plastic Payment Cards

Sustainability can enable organisations to create financial performance, whilst at the same time achieving positive environmental and social impact

at the same time, achieving positive environmental and social impact. And our new ESG proposition does exactly this – we have created a new innovative solution for our credit cards that will enable us to make an impactful difference to our communities and the environment.”

Beyond the ESG innovation, HSBC Amanah was also the first within HSBC Group to launch credit cards made from 85% recycled plastic (rPVC) in January 2021, with the use of rPVC in all cards to rise to 100% later in the year. With this pioneering move, carbon emissions from our credit card production are expected to be significantly reduced in 2021 and beyond.

Combined, these retail initiatives, amongst others, together with other key entity-wide sustainability strategies form the impetus for HSBC to achieve its sustainability aspirations locally and globally. By doing more for Malaysia and the world, HSBC hopes to open a world of opportunities for the communities it serves whilst ensuring that our collective duty and shared obligation towards society and the environment are fulfilled.

Holistic strategy towards net zero “At HSBC, we have a responsibility to our customers, employees, and the communities in which we serve. We recognise that economic growth must also be sustainable if we are to achieve success in the long term,” said HSBC Amanah Malaysia CEO Raja Amir Shah about the ESG charity feature.

“Sustainability can enable organisations to create financial performance, whilst

Rural Banking needs to be About More than Just Agri & Livestock Lending

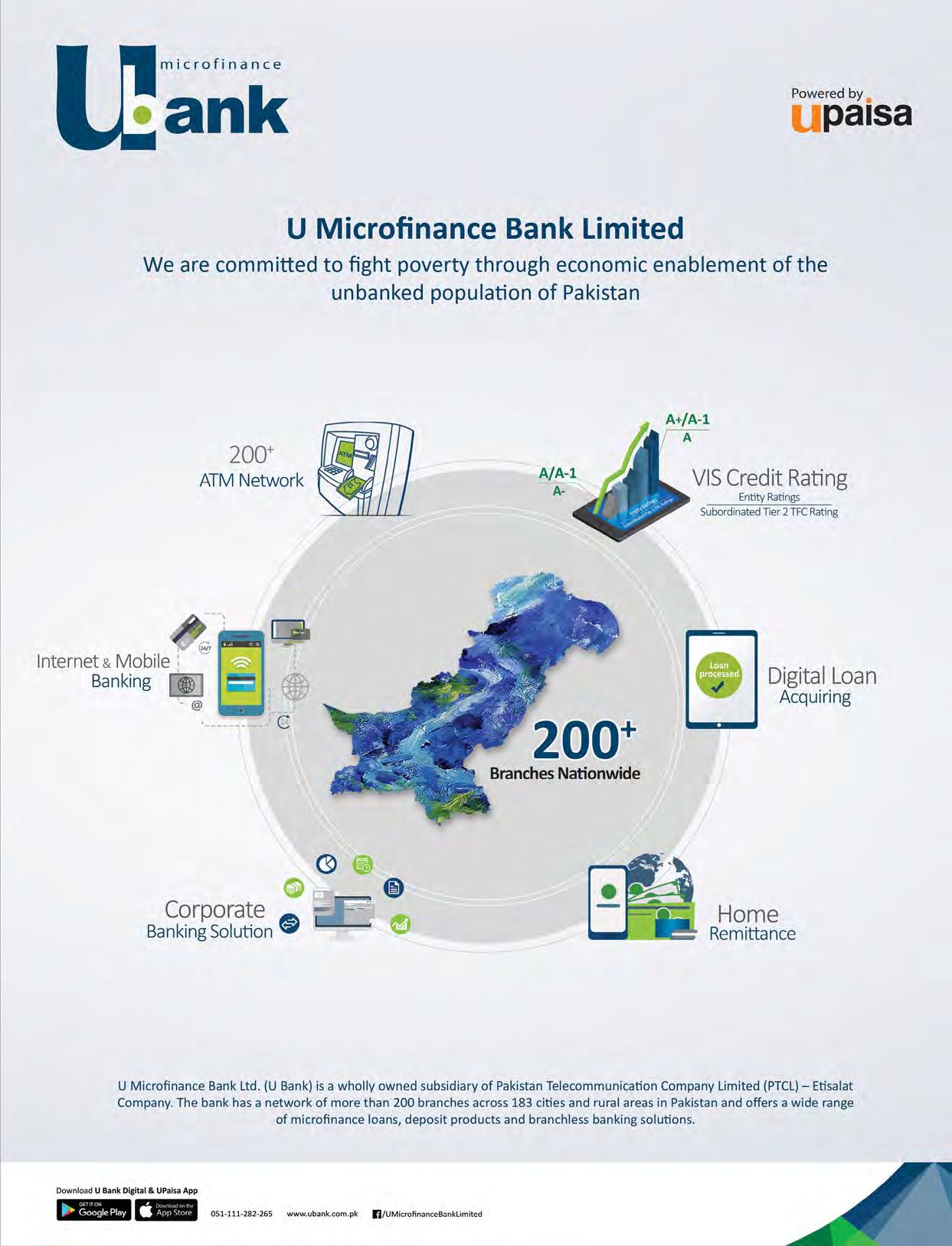

Globally, poverty continues to be a disproportionately rural problem, with an estimated 79% of the worldwide poor living in rural areas. We see a similar trend in Pakistan where the financially included population remains predominantly urban (68%). The microfinance sector by virtue of working on the frontlines of poverty by extending credit to those typically considered uncreditworthy by the banking sector has become key players in battling this disproportionate lack of financial inclusion, particularly in rural areas.

Whilst U Microfinance Bank Private Limited (U Bank) remains devoted to progress the national agenda of financial inclusion, our approach towards this mission is vastly different from the norm. At U Bank our primary customer segment is the economically active poor i.e. farmers, small entrepreneurs, and daily wagers, and whilst their needs are vastly different from the affluent customer segments in cities they do have similar aspirations for creating wealth, managing their savings and improving the quality of their lives beyond their need for credit.

Despite this reality there is a gross absence of banking facilities in rural Pakistan. At U Bank our customer’s needs have always driven our strategy and as a result today we have the largest on-ground presence in the microfinance sector with 201 branches and ATMs across 183 rural and urban areas in the country. Moreover, U Bank is strategically located in places, where the bank’s branch and ATM network is the nearest formal banking option available to customers, thus ensuring the availability of modern banking facilities to the rural population. These customers otherwise have to rely solely on retail agents to meet their basic financial transaction needs, a system that faces liquidity and exploitation of customerrelated issues which spoil customer experience and erode their trust.

Furthermore, being a full menu bank, we have constructed a diverse product suite that caters to clients in both rural and urban areas. Considering the former, our dedicated product team conducts extensive market research to pinpoint the needs of rural customers and develop bespoke products for them. All of these products stimulate progress and prosperity in rural areas through the creation of income-generating opportunities. We also recognise that women are less likely to escape poverty as they experience greater social and financial risk. Therefore, U Bank has designed products to ensure the health and well-being of women

in poverty. Our work goes beyond working on just lending product innovation and we devote significant energy and resources towards design pilot projects which help us improve the value-chains in which our key customers operate. An example of this comes via our work within the agri value-chain where we are piloting with a startup Ricult to gain satellite imagery-based crop health and harvesting data as well as micro-weather insights for our farmer customer. This pilot has been showing promising results for both internal portfolio management and crop health management for the farmers.

As a bank operating in the rural space we have also been extremely mindful of the impacts of the COVID-19, also referred to as a ‘developing country pandemic’ due to its disproportionate impact on poor and vulnerable populations. Due to this consideration even despite the difficult

U Bank’s primary customer segment are farmers, small entrepreneurs, and daily wager U Bank Branch

condition due to imposed nationwide lockdown, U Bank took a determined stand to not discontinue lending to our core customer base. We are aware that our customers are dependent on day-to-day activity for survival and would not be able to recover from reduced cash flow. This decision was not made without evaluating the associated business risks, and the bank made the strategic decision to help our customers use their non-productive gold assets as collateral to meet their emergency cash needs whilst securing more of our portfolio at the same time creating a win-win situation for all parties involved.

We believe that the future of finance is the brightest if it is targeted towards typically excluded segments i.e. the poor, rural and vulnerable. Our core values of merit, commitment, innovation, ethics, and transparency guide us towards greater penetration, outreach, and efficiency and improving access to low-income communities throughout the country and hence elevating the economic, social, and environmental impact that our organisation has. We are committed to keep advancing our way of doing business, and build a bank of the future, that not only creates greater ease of doing business but also considers convenience and ease for our customers, all whilst innovating and adopting technological developments to offer unique and innovative product and service offerings that meet the ever-evolving needs of our clientele.

Standard Chartered Hong Kong secures multiple awards at the 2021 ABF Retail Banking Awards

StanChart spearheads international digital banking with empowered employees

Mary Huen, CEO, Hong Kong and Ong Lay Choo, Managing Director, Head, Consumer, Private and Business Banking, Hong Kong, unveiled the Priority Private Centre at K11 ATELIER Victoria Dockside

Standard Chartered Hong Kong has been making efforts for its comprehensive digital innovations leading to a more fluid banking experience for its customers and increased morale of its employees.

Because of this, the leading international banking group earned three recognitions at the 2021 Asian Banking & Finance Retail Banking Awards. Standard Chartered was hailed as the International Retail Bank of the Year, and Digital Banking Initiative of the Year.

The company invested in digital banking systems to introduce a seamless and efficient banking experience to its clients. Through this innovation, the bank was able to use data analytics to communicate more effectively and offer a more personalised service to its customers, whilst improving the overall efficiency of the process.

According to Standard Chartered, the bank has focused on understanding its clients’ behaviour through data and analytics to identify client challenges in digital touchpoints. “This enabled us to customise our communication and offer to enhance the effectiveness of digital sales and service adoption program,” said Ong Lay Choo, Managing Director and Head of Consumer, Private and Business Banking, Hong Kong.

The digitisation of the banking process allowed Standard Chartered to introduce instant services using the SC Mobile App, which covers multiple services from instant banking account opening, instant approval for loans, and fund transfer to name a few. Users of the app are also given real-time information about their card transactions and other matters like international exchange rate.

The digital bank process also allowed for more flexibility to its clients to use multiple services engaging in transactions and money transfers. The banking app gave users the power to use their accounts for different needs without having to physically appear in a local branch.

“On top of instant services, clients are also in demand for more options and flexibility. Recently, we launched a service that allows our clients to use credit cards as debit sources for local transfers in SC Mobile App. Such will enable clients to pay their rent, education expenses, and even friends via own credit cards,” said Lay Choo.

Standard Chartered is keen to using digital technology to improve the banking experience of customers. Despite the limitations brought by the pandemic, the bank was able to offer a

personalised Relationship Manager (RM) service to its clients in a more efficient manner.

“We launched the MyRM platform in the midst of COVID-19 last year. It is a great tool for our RMs to keep in connection with our clients in a secure way when they are not able to visit the branches. By leveraging on key functions like documents and file sharing, screen sharing, text chat, and audio call functions, RMs can easily provide investment advice and services via our SC Mobile App or online banking platform. All conversations and exchanged information will be kept confidential,” said Lay Choo.

Aside from providing world-class service to its customers, Standard Chartered also prides itself on being an employee-friendly organization,

maintaining a high-quality workforce provided with the best-in-class working environment. The bank has pioneered inclusive initiatives for its employees, such as rolling out hybrid working and allowing permanent flexible working to all eligible employees ahead of others.

The company believes that a work culture that embraces diversity and inclusivity presents a great working environment to employees and enables them to unleash their true potential in their respective careers.

“Diversity and Inclusion (D&I) is embedded in our values and an inherent part of our brand and culture. This is about creating a workplace culture that helps every colleague to contribute to their full potential. It is more than just policies, initiatives, and processes: it is about how we work together and ensure everyone feels respected for who they are in the bank,” said Florence Wong, Managing Director and Head of Human Resources, Hong Kong, Macau, Japan and Co-Head of Human Resources, Greater Bay Area.

The company had invested in their efforts to provide a dynamic working culture to its employees and introduced four different networks to drive the D&I culture, including Women in Network, Parents and Caregivers, LGBTA and Disabilities. Besides these networks, the company has initiated Inclusive Leadership Program and enabled leaders within the organization to learn how to lead with inclusion and to promote D&I culture across the whole company.

Florence Wong, Managing Director, Head, HR, Hong Kong, Macau, Japan & Co-Head HR Greater Bay Area

CIMB THAI BANK RECOGNISED AT ABF RETAIL BANKING AWARDS

CIMB Thai Bank took home the “Wealth Management Platform of the Year – Thailand” award for the second consecutive year as well as the “Digital Banking Initiative of the Year – Thailand” award at the recently-concluded Retail Banking Awards 2021. This event honours the most outstanding banks and financial institutions that have introduced ground-breaking products and services that empowered them to successfully adapt with the rapidly evolving tech and banking landscape.

Since embarking on their digital journey in late 2018, CIMB Thai has been focused on constantly expanding the digital frontier with regards to providing accessible financial services throughout Thailand. Being one of the first banks to exit the regulatory electronic Know Your Customer (e-KYC) Sandbox, the bank has taken major strides digitally, rolling out initiatives including a fully-digital process to open a banking account, as well as transitioning smoothly from a brick-andmortar model into a seamless mobile-first banking experience, allowing them to fulfil customers’ financial needs wherever they are, whenever they need it.

What sets CIMB Thai apart from other banks is that customers do not need to

step into a physical bank branch to bank with them. In 2020, CIMB Thai enabled additional onboarding journeys, allowing new-to-bank customers to perform KYC at any of the 13,000+ Counter Service outlets at 7-Eleven convenience stores nationwide, or even leverage KYC information from customers’ existing banks via the National Digital Identity (NDID) blockchain framework. As a result, even though CIMB Thai has scaled down physical branch presence by 16%, their Digital Savings Account opening performance has grown 7x by the end of the year.

CIMB Thai has also achieved some notable wealth-related milestones in 2020, the most prominent being the solidification of their position as a top distributor for bonds and structured products in Thailand, leading in market share for both. In Q4, the bank enhanced their wealth proposition even further by launching a new 15year exclusive non-life bancassurance partnership with Sompo Insurance to offer fully-integrated insurance solutions.

CIMB Thai’s prowess in wealth blends perfectly with their digital initiatives, as they enabled digital primary bonds subscriptions on the CIMB TH Digital Banking application in 2020, allowing customers to subscribe to primary bonds directly from within the application. This quickly grew into a success story as they issued over THB2bn in bonds digitally within a year. In fact, a recent digital bond issuance reached THB1bn in volume (100x compared to their first issuance), signifying increasing user confidence in their digital wealth platform.

For those who still prefer face-to-face interaction, especially for the affluent segment, CIMB Thai has also unveiled brand-new Wealth Centres in Silom Complex and Central Ladprao. Equipped with a wide range of innovative wealth services to better serve the Preferred segment, the new branches include a smart wealth advisory system, a revamped store layout and personalised wealth offerings, just to name a few.

Data and analytics play a critical role in enabling the successful delivery of

CIMB Thai’s digital wealth products and services. Leveraging the multifaceted data from various interactions with customers across the bank, they have successfully developed several meaningful models to create more value for customers, including a Next-ProductTo-Buy (NPTB) model, which greatly enhances the bank’s ability to recommend the best products to fit customers’ needs, as well as a Hidden Preferred model, allowing CIMB Thai to identify affluent individuals via behavioural trends so that the bank can reach out with exclusive Preferred offers.

Amidst an ever-changing, increasingly digital world, CIMB Thai will constantly adapt to provide a seamless banking experience for their customers. The bank plans to launch more wealth-focused enhancements to allow customers to do more, including an integration with FundConnext, where customers can access and invest in mutual funds offered by fund houses throughout Thailand. They have recently launched digital secondary bonds capabilities via their platform, while other initiatives in the pipeline include enabling wealth robo-advisory and an enhanced consolidated financial portfolio for customers to manage their wealth.

CIMB Thai aspires to continue driving the future of banking in Thailand and ASEAN. They stated that all of these could not have been achieved without the support of their customers as well as the various partners that they have worked with.

Why is solar leading the rise of renewable energy in Asia?

U-Solar: Simplifying the switch to solar energy for Asia U-Solar is Asia’s first one-stop solar ecosystem financing platform. Through partnerships with solar developers, contractors, businesses, and homeowners across Singapore, Malaysia, Indonesia, and Thailand, U-Solar brings together ecosystem players and end-users on one integrated platform.

With U-Solar, businesses can own a solar power system at minimal upfront investment, whilst homeowners can enjoy 0% interest payment plans with a UOB credit card. It is supported by the UOB Smart City Sustainable Finance Framework, which guides the Bank’s financing efforts to encourage the development of smart and sustainable cities across the region through a streamlined and transparent process.

As of July 2021, U-Solar has facilitated the generation of almost 163.9GW hours of solar power across its four markets, reducing more than 81,500 tonnes CO2 equivalent in greenhouse gas emissions, which is equivalent to having close to 1.35 million new tree seedlings grow over 10 years or taking more than 17,737 cars off the road for a year.

Visit www.UOBgroup.com/u-solar to find out more.

Source: Solarvest

Renewable energy has claimed a greater share of electricity generation and is projected to lead total power generation from 20351. This is a result of increasing cost-competitiveness, supportive renewable policies and institutional frameworks, and price volatility of traditional energy sources.

The COVID-19 pandemic has also been a catalyst for change and has accelerated the push for sustainability. As governments and businesses look towards a green recovery, global investments in renewables and energy transition could double to US$2t per annum2 over 2021 – 2023. In Southeast Asia, countries have set renewable energy targets of up to 35% of the total energy mix3 by 2037.

Solar energy and its benefits Southeast Asia’s geographical location allows the region to enjoy ideal levels of solar radiation. Additionally, the cost of solar installation has declined by over 70% between 2010 – 20204, making solar energy a cheaper source than traditional fossil fuel and more accessible. This makes solar energy the most viable solution to meet the region’s electricity demand and sustainability targets.

Installing a rooftop solar system can bring about multiple benefits to buildings and homeowners. Other than providing immediate savings on electricity bills, solar panels also protect the rooftop by shielding it from harmful ultraviolet rays and cooling the temperature of the roof, thus prolonging its durability. Powering businesses and homes Although most buildings and homeowners are aware of the savings and environmental benefits of solar energy, the perceived cost, and hassle of installation and maintenance is usually a deterrence. This is where financial institutions can play an important role to support end-users. If flexible financing options are available, end-users will be incentivised to install solar power systems as they can do so with minimal upfront investment.

For SMEs in particular, partnering with a financial institution that has established frameworks is crucial to ensure that initiatives qualify for sustainable financing. This allows them to enjoy enhanced branding as an ESG-conscious corporation without investing heavily in building their own framework.

Source: SolarGy Source: TML Energy

1 Source: Forbes report quoting Carbon Tracker 2 Source: International Renewable Energy Agency (IRENA) 3 Source: International Energy Agency (IEA) 4 Source: National Renewable Energy Laboratory (NREL). 70% is the average decline for installation of residential, commercial rooftop and utility scale solar systems.

UOB Malaysia continues to create true value with impactful transaction banking solutions.

Whilst local and global businesses alike are facing financial and operational challenges during the COVID-19 pandemic, banks have a critical role to play in helping them weather the current storm. This provides banks with an opportunity to innovate new ways to support their clients to transit into more efficient ways of doing business. For this, banks need to be agile to embrace change from serving a single client to serving an ecosystem.

It is with this thought that at UOB Malaysia, we have modelled our approach in creating innovative and ecosystem-based solutions encompassing Cash Management and Financial Supply Chain Management (FSCM) solutions for clients to support and sustain business growth.

To illustrate this, UOB Malaysia has crafted a Distributor Financing Programme under the FSCM structure for a multinational beverage company, allowing access to RM120m working capital for their distributors to drive cost efficiency, liquidity creation, and risk mitigation. With this programme, the client was able to cut into more than half its Days Sales Outstanding from 45 days to 21 days, which translates to an average of 2% per annum interest earned as nonoperating income. This is achieved without additional collateral or commercial risk on the part of the client nor their ecosystem players. With adequate liquidity and working capital, the client’s sales grew double digit. These positive results also helped cushion the client’s liquidity in its ecosystem especially during this pandemic.

The implementation of the FSCM solution has also opened up opportunities for the client and its distributors to have access to a wide array of transaction banking solutions, including, but not limited to, receivables, payments, and liquidity management solutions.

UOB Malaysia has been one of the market’s active proponents of FSCM and its benefits to the entire ecosystem, both

UOB Malaysia Headquarters (Menara UOB) upstream and downstream. We have also implemented more than 20 successful programmes involving close to 40 anchors, nearly 100 spokes with more than RM2b total in our balance sheet. With anchors and spokes from industries including construction and industrial, oil and gas, telecommunications, manufacturing and fast-moving consumer goods, FSCM is highly adaptable and suitable across industries. Another emerging trend that has become increasingly crucial for business long-term By putting financial innovation at the forefront in creating sustainable ecosystem-based solutions, customers will truly unlock their business potential to weather the current storm and survivability during this unprecedented time is the digital transformation of business processes. Whilst gradual progress has been made in emerge stronger the digital space to encourage more cashless payments amongst businesses, there is still a gap when it comes to the collection process, specifically with cash-on-delivery payments. UOB mCollect, a digital collections solution, is ideated to fill the gap by helping businesses in moving towards financial efficiency. It is best suited for distributors, wholesalers, and midsized producers who rely heavily on a cash-ondelivery mode of payment collections. As an example, one of our clients in the food processing, packaging, and distribution business makes hundreds of deliveries on a daily basis. With payment collections usually made by cash, its sales staff had to spend time and effort on verifying amount and payee details and reconciling the payments at the end of each day. Handling physical cash also exposes clients to the risks of potential fraud and robbery. In addition, this manual collection process is susceptible to human error and slows down the actual cash depositing process into the client’s account.

With UOB mCollect, the client’s sales staff are able to collect payments digitally using a single QR code, streamlining the collection process, and reducing the time needed for each delivery. This also benefits the client’s finance team, as payments received through UOB mCollect are automatically reconciled against each invoice, reducing the time required to reconcile payments. For businesses with Enterprise Resource Planning or ERP solution, such as this client, they can enjoy the added benefit of being able to easily integrate with UOB mCollect by just downloading a mobile app.

Lucas Chew, executive director and country head of Transaction Banking, UOB Malaysia, said, “This unprecedented time should serve as a reflection for banks to continuously steer towards creating true value with impactful and innovative solutions to support customer business growth and viability post-pandemic. By putting financial innovation at the forefront in creating sustainable ecosystem-based solutions, customers will truly unlock their business potential to weather the current storm and emerge stronger.”

OCBC banking on digital growth for greater convenience to customers

The COVID-19 pandemic has transformed the way businesses interact with their customers. Forever. Businesses shifted online and now rely more heavily on the digital space to reap sales and market outreach. Consequently, the digitalisation of businesses has sent the adoption of digital payments into hyperdrive, challenging banks in the market to provide more frictionless and innovative digital payments services.

When choosing from a plethora of business payment solutions, there are several crucial factors customers will consider such as transaction fees and reconciliation methods. This is especially so for SMEs. Unlike large businesses, it is important for small businesses to carefully choose a payment system that provides them with full control over their collections, and without too great a turnaround time and unpredictability.

OCBC Bank (Malaysia) Berhad’s (OCBC Bank) digital efforts are premised on its Purpose Statement, to help individuals and businesses across communities achieve their aspirations by providing innovative financial services that meet their needs. With our current measurements of Digital Adoption, we would say >50% of our business customers are highly digitally engaged with our digital solutions and offerings. By helping our SME customers Go Digital with OCBC, we have enabled them to work things out more seamlessly. We would want to see every customer have a ‘bank in the pocket’ through our Mobile First Strategy.

As one of the longest established foreign banks in Malaysia, OCBC Bank has redefined the way businesses collect payments instore and online with the launch of OCBC OneCollect, a mobile app that facilitates contactless collection via QR payments. Through its strong regional connectivity, OCBC Bank’s OneCollect enables the collection of local payments (MYR) through DuitNow QR and cross-border payments (SGD) through PayNow QR. DuitNow QR is the Malaysian QR standard for allowing customers to scan & pay from any participating banks or eWallet of their choice. Similarly, PayNow QR is the national QR standard in Singapore supported by nine banks in Singapore where payment is debited directly from the savings account of the buyer. Hence, if you are looking to sell products online internationally to Singapore,

chances are very good that you wouldn’t need to worry whether or not your customer is using the same currency as you anymore.

Being the first bank in Malaysia to bring PayNow QR to the market, OCBC OneCollect was welcomed by businesses, especially those located in the southern region of the Peninsular, and has since become the

OCBC Bank’s digital efforts aim to help individuals and businesses across communities achieve their aspirations by providing innovative financial services that meet their needs.

preferred option for them. By collecting through OCBC OneCollect, customers can pay for goods and services in-store or online without needing to touch anything or worry about virus transmission. This is particularly beneficial during times like this when the impact of the pandemic has become even greater than we first thought. What’s more, merchants can expect to enjoy fast settlement and competitive Merchant Discount Rates (MDR).

When you have cash flow moving in and out of your business, you’ll need to track and analyse it closely, so it doesn’t drift into the red zone. In order to make a sound business decision, you will need solid information, especially about your business financials —and this tool is able to help.

Fully integrated into OCBC Velocity (Business Internet Banking), OCBC Business Financial Management (BFM) provides time-starved businesses with past and current cash flow data and forecasts their future cash flow, giving them an idea of where their business is heading and allowing them to respond to the situation more effectively. It also offers a drill-in to view your complex income and expenditure items by different categories.

In addition, we understand that manual invoice generation and payment tracking can be tedious and timeconsuming. Therefore, Business Financial Management is here to do all the heavy lifting for your invoicing process. It enables you to customise invoices based on different requirements, send invoices, and tracking payments more easily.

Ultimately, suitable business payments and financial solutions should help accelerate your business collections and provide predictability and clarity of your financial situation. Amidst the pandemic, it is indispensable to adapt, adjust and improvise your business to thrive. Remember, the more control you have over the money moving in and out of your company, the better you can weather market fluctuations and instability.

Financial Inclusion Innovation for the Underbanked Thais

Ngern Tid Lor ramps up technology capabilities to assist customers in digital adoption.

With more than three decades of experience in providing financial services to the underbanked Thai population, Ngern Tid Lor Public Company Limited (TIDLOR) is the leader in the fastgrowing vehicle title loan market in Thailand. It is also a non-life and life insurance broker with the largest number of licensed branch staff in the country. With over 1,000 branches nationwide, the company aims to alleviate poverty in Thailand by providing fair, transparent, and convenient financial services.

The underbanked population is traditionally considered as digitally challenged and thus almost all service providers focus on opening low-cost branches as a growth strategy. However, TIDLOR observed that digital adoption of customers has been increasing dramatically for those less than 45 years old, especially during the COVID-19 pandemic. In order to meet the increasing demand, it sets out to massively ramp up its technology capabilities such as mobile technologies, data analytics, cybersecurity, automated processing, and ecosystem integration, by doubling its IT spending/investment and tripling its IT resources to over three hundred people.

In 2020, its years of investment started to bear fruits with key projects launched successively that have massively upgraded the way it provides services from branches, agents, and to customers directly, including:

Branch Experience Digital Transformation From originating motorcycle loans, selling motor insurance, to processing repayments, all key branch services are provided through an iPad. The ease of use has reduced staff training and service turnaround time, whilst increasing customer satisfaction. As the functionality on iPad continues to be enhanced, it will eventually enable TIDLOR’s agents to provide the same services as their own branches. As a result, TIDLOR’s distribution network could be expanded massively without opening more branches.

Ngern Tid Lor’s efforts transformed the organisation with new competencies and perspectives to serve its customers with innovations for years to come

Digital Acquisition Platform With its expertise in digital acquisition, TIDLOR has achieved the #1 searched brand on Google, generating 3.5 times of web traffic from its competitors. Its digital acquisition platform also contributes 25% of new insurance and non-loan customers at an increasing rate, significantly reducing the cost of acquisition. Furthermore, it has also implemented a machine-learning trained chatbot on Facebook, resulting in an over 160% increase in leads generated from Facebook inquiries.