1 minute read

d levels

was another robust year for PB/TvIDF production and ship ments by U.S. manufacturers," said CPA president Rich Margosian. "The rebound in MDF shipments after a decline in 1995 is especially encouraging and confums the increasingly diverse use of MDF in the marketplace. At the same time, increases in particleboard shipments remained steady and strong last year."

The increase recovered more than 50% of the 1994-95 loss, and was the fourth increase during the past five years.

Yet the gap between U.S. particleboard capacity and shipments continued to widen, with particleboard producers shipping last year at a rate of 88.6Vo of their production capacity.

At 3.51 BsF, particleboard industrial shipments in 1996 were 200 million sq. ft. (ur'rsn) higher than in 1995. This 6Va increase expanded the industrial board share of total particleboard shipments to 8O.4Vo from 1995's '78.87o.

1996 U.S. Particleboard Shipments

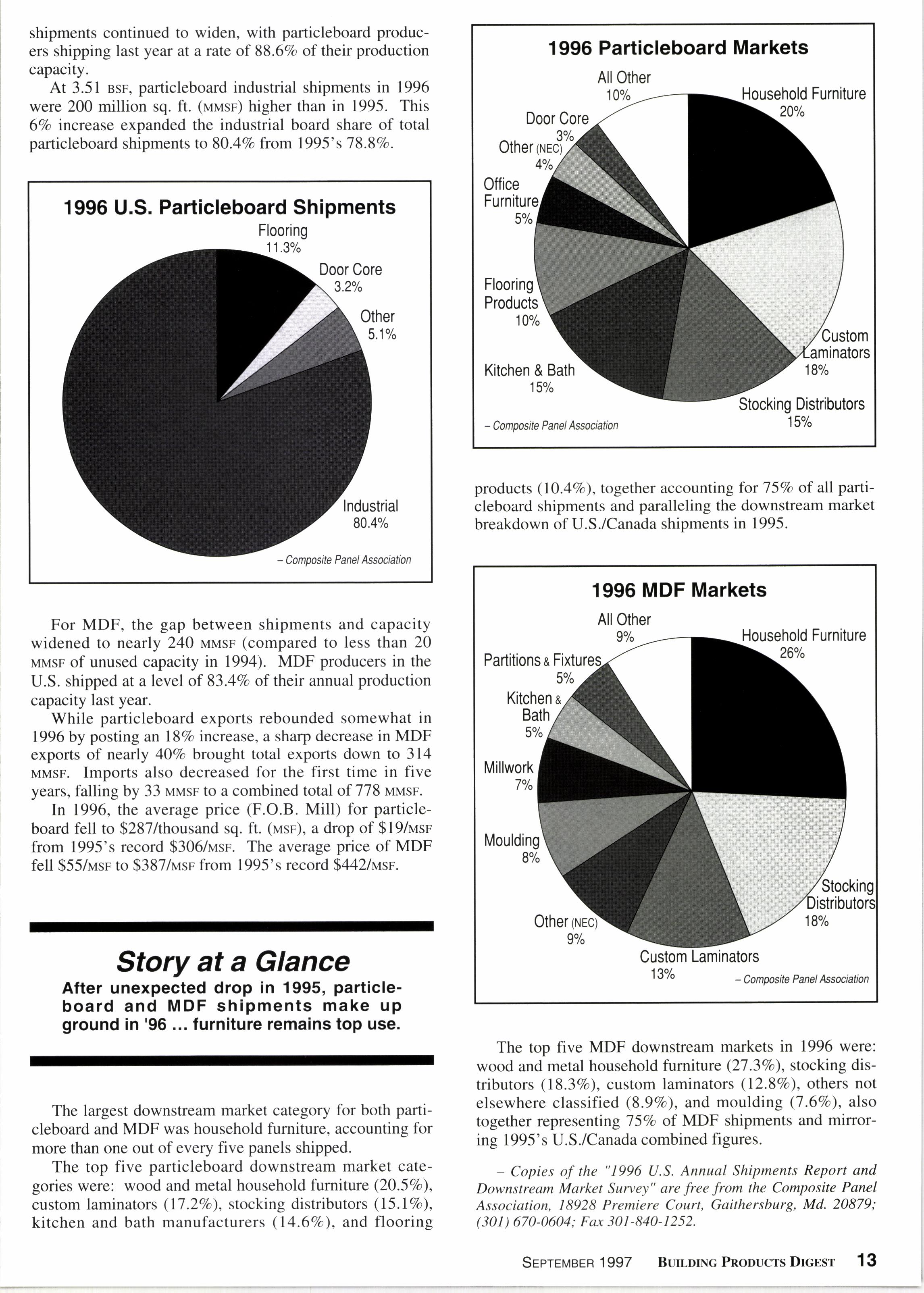

1996 Particleboard Markets

For MDF, the gap between shipments and capacity widened to nearly 240 rvrrrrsr'(compared to less than 20 MMSF of unused capacity in 1994). MDF producers in the U.S. shipped at a level of 83.4Vo of their annual production capacity last year.

While particleboard exports rebounded somewhat in 1996 by posting an lSVo increase, a sharp decrease in MDF exports of nearly 40Vo brought total exports down to 314 rvrusn. Imports also decreased for the first time in five years, falling by 33 r'avsn to a combined total of 778 MMsF. ln 1996, the average price (F.O.B. Mill) for particleboard fell to $287lthousand sq. ft. (r'asn), a drop of $l9futsn from 1995's record $306/rnrsn. The average price of MDF fell $55/rrasr to $387/use from 1995's record $442lrrasr'.

Story at a Glance

After unexpected drop in 1995, particleboard and MDF shipments make up ground in '96 furniture remains top use.

The largest downstream market category for both particleboard and MDF was household furniture, accounting for more than one out of every five panels shipped.

The top five particleboard downstream market categories were: wood and metal household furniture (20.5Eo), custom laminators (l7.2Vo), stocking distributors (l5.lvo), kitchen and bath manufacturers (l4.6Vo), and flooring products (lO.4Vo), together accounting for 757o of all particleboard shipments and paralleling the downstream market breakdown of U.S./Canada shipments in 1995.

The top five MDF downstream markets in 1996 were: wood and metal household furniture (27 .37o), stocking distributors (l8.3%o), custom laminators (l2.8Vo), others not elsewhere classified (8.9Vo), and moulding (7.6Vo), also together representing 757o of MDF shipments and mirroring 1995's U.S./Canada combined figures.

- Copies of the "1996 U.S. Annual Shipments Report and Downstream Market Survey" are free from the Composite Panel Association, i,8928 Premiere Court, Gaithersburg, Md. 20879; (301) 670-0604; Fax 301-840-1252.