7 minute read

LOWER MANHATTAN REAL ESTATE MARKET REPORT

Lower Manhattan’s office market continued to show signs of struggle in the first quarter. Leasing totals declined from the end of 2022 and vacancy rates remain stubbornly high, particularly in Class B properties. The district’s ongoing challenges are mirrored across all Manhattan submarkets as the city’s office market navigates continued macroeconomic uncertainty. Though office leasing is still trying to find its footing, other sectors of Lower Manhattan’s economy continue to mount a recovery. Median apartment rents dipped slightly but remain high as Lower Manhattan remains a residential neighborhood of choice. The hospitality industry has reason for optimism, with new hotels opening, travel increasing and positive momentum in both hotel occupancy and room rates. Fourteen retailers have opened so far in early 2023, similar to rates seen at the end of last year, and another 16 recently announced plans for new storefronts in Lower Manhattan.

Leasing Activity Declines Across Manhattan

Leasing fell significantly across all Manhattan office markets during the first quarter. Prospective tenants continue to delay or forego new leasing amid ongoing macroeconomic headwinds and the persistence of hybrid work. Lower Manhattan recorded 500,000 sq. ft. of office leasing according to CBRE — the second consecutive quarter in which leasing activity declined, and the lowest quarterly total since the first quarter of 2021. Leasing activity fell by 36% from the previous quarter and remains 51% below the five-year quarterly average.

Midtown saw 2.52 million sq. ft. of leasing activity in the first quarter, down 2% from the previous quarter and 31% behind the five-year quarterly average. This is the second consecutive quarter below 3 million sq. ft. and the secondlowest quarterly total since the spring of 2021.

Lower Manhattan Annual New Leasing Activity, 2017-2023

500,000

Square Feet Of New Leasing In The First Quarter — 51% Below The Five-Year Quarterly Average

Midtown South recorded 832,000 sq. ft. of leasing in the first quarter — down 22% from the previous and 33% below the five-year quarterly average. Leasing in Midtown South has now fallen below the five-year quarterly average in three out of the last four quarters.

Increase in Renewals Drives Leasing Activity

Renewals accounted for 340,000 sq. ft. of first quarter leasing, up 85% from the first quarter of 2022 and more than three times the levels seen in the previous quarter. Law firm Cadwalader Wickersham & Taft signed a 225,000 sq. ft. renewal at 200 Liberty Street, downsizing from its previous 348,897 sq. ft. footprint. Cadwalder’s renewal was the second largest deal in Manhattan during the first quarter. Other large tenants to recommit to Lower Manhattan include Stripe, the payment processing technology firm, which signed a one-year extension of its 115,000 sq. ft. lease at 199 Water Street, The King’s College, which renewed its 52,542 sq. ft. lease at 52 Broadway, and the Brennan Center for Justice, which renewed its 49,885 lease at 120 Broadway.

The tech and creative sectors continued to drive relocations to Lower Manhattan. Stubhub signed a lease for 44,000 sq. ft. at 3 World Trade Center, relocating and consolidating from multiple locations in Midtown. StubHub’s lease brings 3 WTC to nearly 90% leased. MakerBot Industries, a 3D printing technology company, signed a lease for 30,467 SF at 100 Pearl Street, relocating from 1 Metrotech Center in Brooklyn. Two advertising agencies signed leases totaling 19,000 sq. ft. at 75 Broad Street, both relocating from Midtown South. Finally, Kain Capital LLC, a financial services firm, signed a 4,700 sq. ft. lease at One World Trade Center, relocating from Midtown.

Moves within Lower Manhattan also accounted for a sizable share of leasing during the first quarter. Revlon signed a lease for 68,518 sq. ft. of DailyPay sublet space at 55 Water Street, relocating and downsizing from its previous 106,915 sq. ft. footprint at One New York Plaza. Axsome Therapeutics, Inc., a biopharmaceutical company, relocated from 22 Cortlandt Street to a 48,486 sq. ft. space at One World Trade Center. Community Access, a mental health services nonprofit, consolidated its offices at 32 Old Slip and 80 Broad Street into a 16,242 sq. ft. space at One State Street Plaza.

Lower Manhattan Top Leases, Q1 2023

Other notable deals executed in the first quarter include telecommunications firm MetTel Inc.’s 50,079 sq. ft. lease at 55 Water Street and Capstone Investment Advisors’ 40,716 sq. ft. lease at 7 World Trade Center.

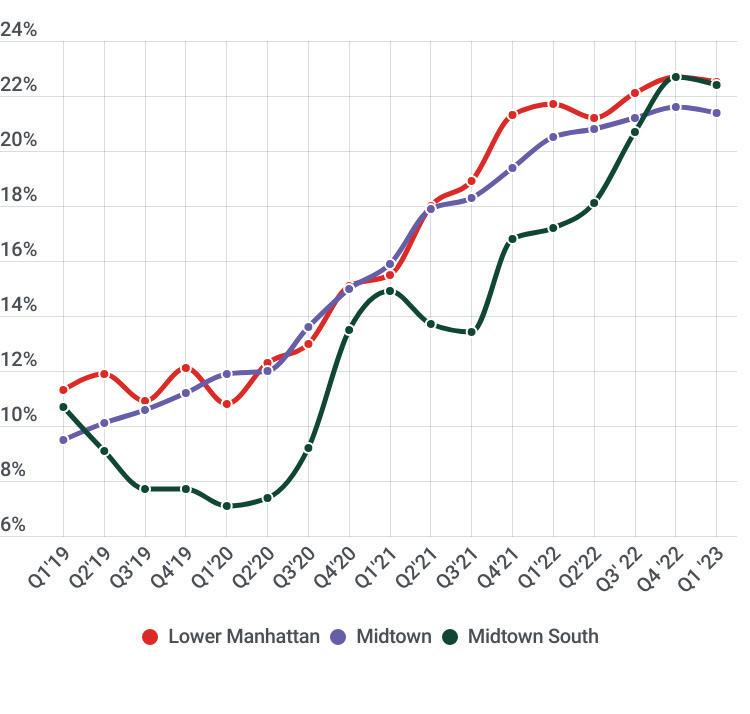

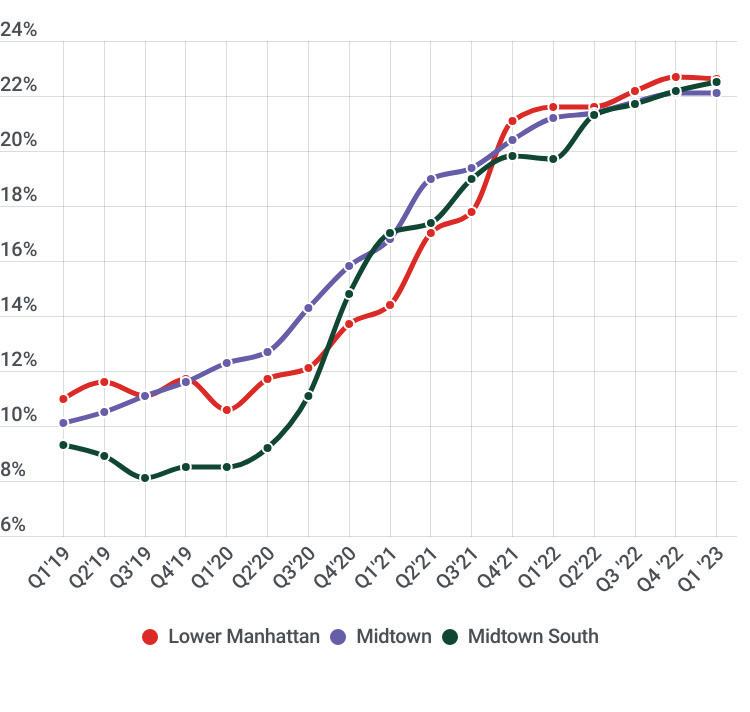

Vacancy Rates Remain High Across Manhattan

According to Cushman & Wakefield, Lower Manhattan’s overall vacancy rate inched down by 10 basis points (bps) to 22.6% in the first quarter after reaching a record high at the end of 2022. Overall vacancy remains slightly higher year-over-year, reflecting several large blocks of space that entered the market last year. Across office-class types in Lower Manhattan, Class A vacancy fell slightly from the previous quarter to 22.5%, though it grew by 0.8% yearover-year. The class B vacancy rate was 24.4%, up 1.4% year-over-year.

Amid sluggish leasing activity, the addition of new direct and sublease spaces outpaced new leasing in the first quarter. Though flight to quality continues to drive new leasing, Class A and overall vacancies in the World Trade submarket (consisting of mostly newer buildings in and around Brookfield Place and the World Trade Center campus) increased by 9.4% and 8.2%, respectively, growing to 20.2% and 18.5% as nearly 151,000 sq. ft. were added to the market in the first quarter. Additionally, Lower Manhattan now contains two submarkets with vacancy rates above 31 percent: the Financial West submarket (roughly west of Broadway, south of Liberty Street) is now 33.2% vacant. This is a slight improvement from the previous quarter, but still the highest vacancy among all Manhattan submarkets. In the Insurance District (roughly east of Broadway, north of Maiden Lane), vacancy rates grew to 31.8%, up 30 bps from the previous quarter.

Though Lower Manhattan’s vacancy rate remains the highest in Manhattan, the borough’s other markets are also experiencing stubbornly high levels of vacancy. Class A vacancy rates were above 21% for the second consecutive quarter and overall vacancy rates were above 22% for the second consecutive quarter across all Manhattan office markets at the beginning of 2023.

Midtown’s overall vacancy rate was flat over the previous quarter but increased over the past year from 21.2% to 22.1%. Class A office vacancy in Midtown dipped slightly to 21.4% as direct space was removed from the market, while class B office vacancy grew slightly to an all time high of 23.8%.

Overall Vacancy Rates by Submarket

Source: Cushman & Wakefield

Class A Vacancy Rates by Submarket

Source: Cushman & Wakefield

Midtown South’s overall vacancy inched up slightly to 22.5%, driven by an uptick of sublease supply coming onto the market. Class A office vacancies in Midtown South fell slightly to 22.5%, however, as 360 Park Avenue South was taken off the market due to renovations, and Class B office vacancy rose by 1.3% year-over-year to 24.4%.

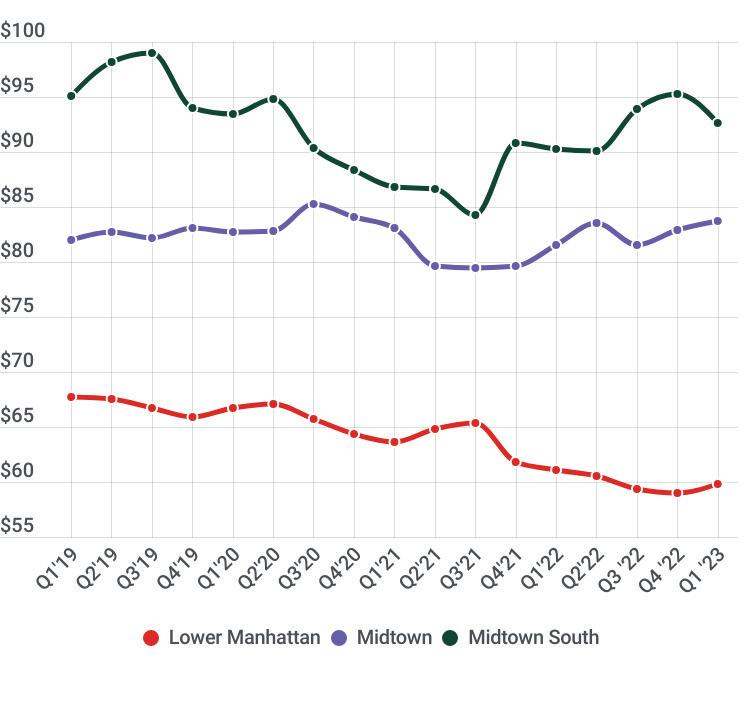

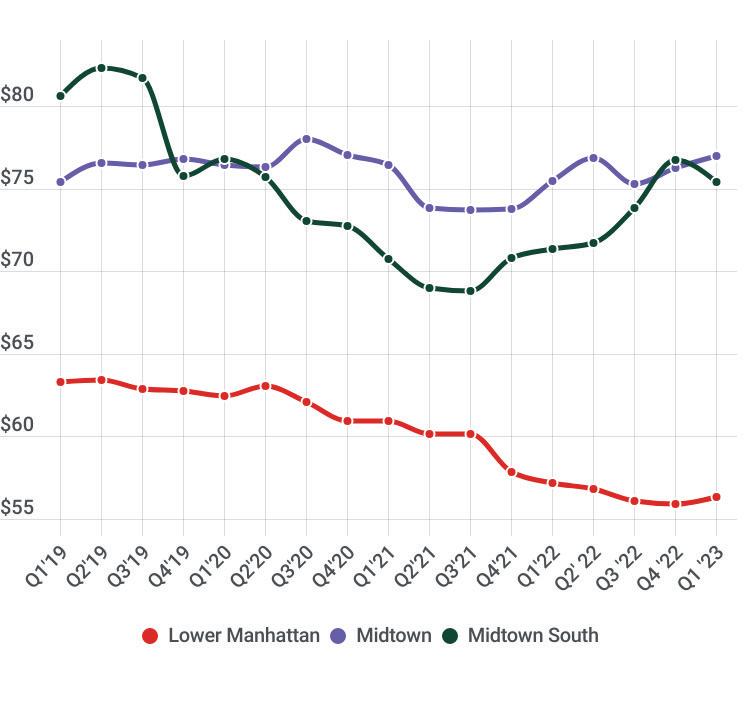

Office Asking Rents Grow Modestly

Lower Manhattan asking rents grew slightly in the first quarter after recording six consecutive quarters of falling rents, reflecting higher-priced space entering the market in the World Trade submarket. Though rents in Midtown and Midtown South grew over the past five quarters, diverging from patterns seen in Lower Manhattan, rents in Midtown South dipped for the first time since the third quarter of 2021. Meanwhile, both overall and Class A rents inched up modestly in Lower Manhattan and Midtown.

According to Cushman & Wakefield, Lower Manhattan’s overall average asking rent grew slightly over the previous quarter, but fell by 1.5% to $56.3 per sq. ft. over the past year — the sixth consecutive quarter below $60. Direct asking rents slid by 2.6 % over the past year to $59.65 per sq. ft.. Class A asking rents grew by 1.5% over the past quarter to $59.86 per sq. ft., but remain 2% lower than at the beginning of 2022. Class B average asking grew slightly over the previous quarter to $52.24, but fell 40 bps year-over-year.

Both overall and Class A office rents in Midtown increased over the past quarter to $76.95 and $83.77, respectively, due to higher-priced space entering the market at Five Manhattan West and 1440 Broadway. In Midtown South, overall asking rents dipped 1.7% over the quarter to $75.4 per sq. ft., driven by lower-priced space additions in the Hudson Square/West Village submarket, though they grew nearly six percent yearover-year. Class A rents in Midtown South rose 2.6% over the past year to $92.64.

$59.86

Lower Manhattan Class A Rent — Up 1.5% From The End Of 2022

Overall Asking Rents by Submarket

Source: Cushman & Wakefield

Class A Asking Rents by Submarket

Source: Cushman & Wakefield

First Quarter 2023 Property Sales

Development Site Sales

45 Broad Street: Madison Equities revealed it sold its interest in the development site at 45 Broad Street to development firm Gemdale for an undisclosed amount. Madison Equities purchased the site for $86 million in 2015 with plans to build a 226-unit condominium building, but foundation work stalled at the onset of the pandemic. Gemdale’s updated plans for the site call for a 60-story, 150 unit condominium development.

Hotel Sales

33 Peck Slip: Sono Hospitality, a South Korea-based hospitality group, closed on the purchase of the 66-room Mr. C Seaport hotel at 33 Peck Slip from the Ghassemieh family, who previously owned and operated the hotel in partnership with Cipriani. Sono purchased the hotel for $60 million, or just over $900,000 per room. Sono rebranded the property as the 33 Seaport Hotel

Recent Pending Sales Announcements

Historic Front Street: The portfolio of buildings at 213-217 Front Street, 214 Front Street and 236 Front Street/24 Peck Slip was listed for sale by owners The Durst Organization and Zuberry Associates for $87 million. The portfolio contains 95 rental apartments and 15 retail units across more than 140,000 sq. ft.

241 Water Street: The 32,000 sq. ft. building that housed the Blue School was listed for sale for $28 million. The Blue School, a private school operated by the founders of the Blue Man Group, has occupied the space since 2011. The Blue School is set to close at the end of the academic year.

2 West Street: A judge ordered an auction for the 298-room Wagner Hotel at 2 West Street with a reported opening bid of $60 million. Urban Commons, which owns the hotel, filed for Chapter 11 bankruptcy in November 2022 after reportedly defaulting on a $96 million loan. Urban Commons originally purchased the hotel for $151 million in 2018.

65 West Broadway: The construction site at 65 West Broadway was listed for sale by Cape Advisors. Plans for the site call for a 10-story, 68,000 sq. ft. residential building containing 23 condo units and ground floor retail space. Construction on the site began in 2017, but has been stalled since 2019. An asking price for the site has not yet been disclosed.

125 Maiden Lane: The United Nations International Children’s Emergency Fund (UNICEF) listed its 70,000 sq. ft., three-floor office condo for sale at 125 Maiden Lane. UNICEF is seeking to reduce its footprint as hybrid work has pushed the organization to reconsider its space needs. An asking price has not yet been disclosed. UNICEF originally purchased the condo in 2007 for $29.9 million.