CONNECT WITH US

Got a story or suggestion, or just want to find out some more information?

twitter.com/MPAMagazineAU

facebook.com/Mortgage ProfessionalAU

02 Editorial

Why brokers should look to commercial lending for growth

04 Statistics

The latest data on Australia’s booming property market

06 Opinion

Brokers play a key role in the success of SMEs, says COSBOA head

AUSUN Finance partner and co-founder Thomas Tang, who was named MPA’s Top Commercial Broker for 2024, talks about his career journey to date and why he is so dedicated to learning new skills and passing his knowledge on to others

MPA reveals Australia’s best-performing commercial finance brokers and they share their tips for success

Get to grips with what’s happening in the world of business finance

14 Commercial property

Demand for industrial space is on the rise in the sector

20 SMEs lending

Small businesses seek brokers’ expertise to navigate tough market

26 Asset and equipment finance

How non-major banks are working with brokers to build better partnerships FEATURES

A recovery is underway in the sector, providing opportunities for brokers

34 New app unlocks data

Aussie’s new mobile app provides instant access to property data

72 Other life

Broker Tom Uhlich looks back at the years he spent competing in triathlons

Cristian Fedrigo talks about what motivated him to set up Equipped

strategy, and what industry leaders have to say.

The latest broker market share figures released by the MFAA provide a compelling reason why mortgage brokers can’t a ord to ignore commercial lending.

Mortgage brokers wrote 71.8% of all new residential home loans between October and December 2023, breaking the quarterly record for market share. The previous highest figure was 71.7% in the September 2022 quarter.

The MFAA rightly points out that this record market share is due to brokers’ outstanding service to their customers, their commitment, professionalism and the trust clients place in them.

But it also reveals the highly competitive nature of the home loan space and how many brokers are competing with each other for lending business, rather than with the banks.

Conversely, the world of commercial finance, which covers loans for commercial property, small businesses, asset and equipment, has far less broker involvement.

There are no definitive figures on the total number of brokers writing commercial loans, although the MFAA Industry Intelligence Service 16th edition report, covering the six-month period from October 2022 to March 2023, showed that the proportion of mortgage brokers also writing commercial loans is less than 30%, or just under 6,000 brokers.

There’s still a massive gap in the market, with many potential commercial clients dealing directly with lenders

Clients are well served by highly specialised commercial brokers focusing solely on this sector but there’s still a massive gap in the market, with many potential commercial clients dealing directly with lenders.

This presents an enticing opportunity for mortgage brokers to expand and strengthen their customer base by o ering commercial lending. Brokers often say ‘‘if you don’t o er a service to your client, they’ll go elsewhere’’.

But taking a leap into the commercial sector requires patience, guidance and the need to acquire the necessary knowledge and skills. So how should brokers go about it?

MPA’s May edition takes an in-depth look at commercial finance, with features on commercial property, SME lending and asset and equipment finance.

We dissect how lenders and aggregators assist brokers to embrace opportunities in commercial lending and explain why diversification is so important.

In this issue, we also reveal the much-anticipated Top Commercial Brokers for 2024. In addition to a comprehensive report on the winners, our cover story features a fascinating interview with the No.1 commercial broker Thomas Tang, who has a passion for education and mentoring.

I hope you enjoy reading the May issue of Mortgage Professional Australia magazine.

ADVERTISING ENQUIRIES claire.tan@keymedia.com

www.keymedia.com

Australia, Canada, USA, UK, NZ and Asia

MortgageProfessionalAustralia is part of an international family of B2B publications and websites for the mortgage industry

AUSTRALIAN BROKER simon.kerslake@keymedia.com

T +61 2 8437 4786 NZ ADVISER

alex.knowles@keymedia.com

T +61 2 8437 4708

CANADIAN MORTGAGE PROFESSIONAL john.mackenzie@keymedia.com

T +1 416 644 8740

MORTGAGEBROKERNEWS.CA corey.bahadur@keymedia.com

T +1 416 644 8740

MORTGAGE PROFESSIONAL AMERICA katie.wolpa@keymedia.com

T +1 720 316 7423

MORTGAGE INTRODUCER (UK) matt.bond@keymedia.com

T +44 7525 456869

CoreLogic’s analysis revealed 88.4% of the national house and unit markets experienced value increases over the past year, a significant rise from 52.9% in July and 39.1% in February.

$10.4trn

New record high for residential real estate in February

1.3%

Quarterly rate of home value growth to February, from 1% in previous quarter

8.9%

Annual home value growth, highest since FY 2021-22 (10.8%)

Median days on market for properties in February

Dwelling approvals dropped 1% in January in seasonally adjusted terms

December, driven by a 9.9% decrease in private house approvals, ABS reported.

CoreLogic survey showed that 67.9% of Australians own homes, with women’s ownership slightly higher at 68.2%, compared with 67.4% for men.

The national vacancy rate fell to 1% in February, declining 0.1% from the previous month, with total vacancies at 30,161, down from 32,108.

GOT AN OPINION THAT COUNTS? Email antony.field@keymedia.com

Commercial and asset finance brokers help small businesses succeed, but government and banks must also play their part, says COSBOA CEO

IS the enabler of business growth and the ability for Australia’s 2.5 million small businesses to access finance has never been more important.

The work of commercial and asset finance brokers in providing solutions for small business plays a vital role in ensuring the engine room of our economy can access the equipment and productive capital that drives their success.

For many small businesses, 2024 will be a crunch year. Latest data from the Australian Small Business Ombudsman indicates that 43% of small business owners are not generating a profit, and most are paying themselves below-average weekly earnings.

The cost of doing business in Australia has become intolerably high, with small businesses facing a perfect storm of rising energy, rent and insurance costs.

Unfortunately, governments continue to increase the regulatory burden on small operators, particularly in areas like industrial relations where the impact on small businesses is often disproportionately high.

However, Australian enterprises remain resilient and continue to be the largest private employer in the country despite an increasingly complex environment.

When green shoots emerge, small businesses need to be able to execute quickly and with certainty.

The ability for time-poor small to medium enterprises to benefit from the services of brokers who bring expertise and market understanding cannot be understated, which is why over 75% of SMEs utilise a commercial broker to access the right facility.

Whether it is funding for new equipment, machinery or vehicles, these brokers are critical growth enablers.

There are at least two ways the federal government could better support brokers to support small business.

Firstly, the government should increase the instant asset write-o in this year’s federal

business is adhering to a serviceable payment plan with the ATO. It seems arbitrary and unfair, because it is.

Banks should update their lending practices to ensure that small businesses are not unfairly prevented from accessing muchneeded capital – which in many cases would be used to not only clear their tax debt but also open the door for future growth.

Financing of tax debt by banks, rather than the ATO, puts more money into the economy by making the ATO less reliant on funding its own debtors. This would be a win-win-win for taxpayers, small business and brokers alike.

As we move into 2024 the work of brokers will have an impact on small business success, for owners to not only survive but also thrive.

I have enjoyed engaging with the Commercial & Asset Finance Brokers Association of Australia (CAFBA) over the past year, including a productive day in Melbourne meeting with the board.

The ability of time-poor SMEs to benefit from the services of brokers who bring their expertise and understanding of the market cannot be understated

budget from its current dismal $20,000 to a more appropriate $150,000.

Australia’s projected productivity growth has declined from 1.5% to 1.2% per annum over the next 40 years, which means lower living standards for future generations.

Boosting the asset write-o threshold will help boost productivity and is a proven behavioural driver of businesses investing in their own productive capacity.

It is such an obvious thing to do; the Senate has already passed a motion in favour of lifting the threshold to $50,000, which is a good start.

Secondly, we are missing an opportunity to deal with the perverse e ects of tax debt.

The Australian Tax O ce (ATO) reminded small business that debt accumulated during COVID cannot be retained forever.

Yet many banks have indicated that they will simply not lend to small businesses that have an ATO liability. They will not lend even if the

As well as CAFBA being a staunch supporter of Australian small businesses, the work it does in promoting careers in broking and ensuring right-sized regulation such as the Professional Standards Scheme is vital.

As many residential mortgage brokers seek to diversify into commercial lending, I would highly recommend these practitioners join CAFBA as the national peak professional body and utilise its education and training platforms to increase their skill level so they can compete and provide the right outcomes.

enterprise and thank CAFBA for its ongoing

On behalf of COSBOA, I commend the commercial brokers that support Australian enterprise and thank CAFBA for its ongoing leadership and advocacy.

Luke Achterstraat is the CEO of COSBOA and has 15 years’ experience in advocacy. As CEO, he advocates on behalf of small businesses to ensure their voice is heard in Canberra.

Luke Achterstraat is the CEO of COSBOA and has 15 years’ experience in advocacy. As CEO, he advocates on behalf of small businesses to ensure their voice is heard in Canberra.

talks about the importance of great mentors and why he is so passionate about passing on his skills and knowledge to other brokers

KNOWLEDGE IS power, but for Thomas Tang, Australia’s Top Commercial Broker for 2024, sharing that knowledge with brokers and customers so they can flourish is where the real power resides.

The dynamic and highly successful broker, who settled more than $471 million of commercial loans to take the No.1 spot in MPA’s Top Commercial Brokers, is a partner at brokerage AUSUN Finance.

Tang has amassed an impressive set of skills

He started his career in finance in 2012, working as a marketing assistant for a big bank, and then moved into a personal banker role in the branch network.

After taking on the role of lending manager for just a few days, Tang left the bank in July 2015, deciding that it wasn’t for him and chose broking instead.

“I didn’t want to be put in a box in a big machine,” says Tang. “I want to find out what’s best for the customer, but as a residential

“In the past eight years, I have coached more than 20 brokers from non-industry experience to more experienced brokers”

during his career, including property development and investment and all aspects of commercial and residential lending. He also wrote a book, Retire on Rent, providing tips on how to achieve financial freedom through property investment.

He has shown his leadership capabilities as a lieutenant in the Australian Army Reserve, as co-founder of AUSUN Finance, and as a mentor to other brokers.

Tang is clearly passionate about mentoring and “paying it forward” after learning so much from others.

lending manager I can only offer one product.”

Tang praised his mentor Jun Sun, the managing director and founder of AUSUN Finance, who helped him become a successful broker and was ranked No.3 in Top Commercial Brokers 2019.

Tang says Sun assisted him immensely.

“When I was in uni I established two student societies – I was very good at networking, marketing and hosting events. Finding customers is for me never a struggle, but delivering a solution is a struggle for new brokers.”

Sun provided Tang with one-on-one coaching for the first few years. “He would sit down with me in the appointments and we would see customers together.”

While Tang would do the research and data entry, Sun would assist with compliance and risk management, checking files and negotiating loan deals.

With Sun as his mentor, Tang says he was able to leverage his experience to deliver high-quality solutions to clients and mitigate risk.

He describes Sun as being approachable 24/7, reliable and fair, with a strong commitment to grow the AUSUN team.

When AUSUN started in 2015, the brokerage consisted of Sun and two assistants, with Tang joining as a partner. Now the business has 30 licensed brokers, with two offices in Melbourne and locations in Sydney, Adelaide, Brisbane and Perth.

Tang says one of the big lessons he learnt from Sun was the difference between knowledge and experience.

“Knowledge you can learn quickly, but experience comes with time – this is why you need to leverage someone else’s experience to ensure that the client’s expectations are met.”

When it comes to his own ongoing professional development, Tang says he’s very willing to “pay and learn”. He has spent

Name: Thomas Tang

Title: Co-founder and partner

Company: AUSUN Finance

Years in the industry: 11

Career highlight: Going from a bank teller to No.1 commercial broker in 10 years, being an active army reservist, doing small property developments on the side and JVs with clients to grow together. Leveraging the team to provide success for many

Career challenge: There is a real scarcity of learning opportunities, including mentorships and partnerships. Putting systems in place and building your own community for long-term success

$300,000 in fees in the past 10 years to take part in mentorships and joint venture projects, learning “di erent things from di erent people”.

His mentors include business coach Mark Creedon, broker business coach Jason Back, former Telstra CEO Andrew Penn, Hotspotting founder Terry Ryder, Robert Kiyosaki, Michael Yardney and Tony Robbins.

Creedon has helped him to understand processes and his business ideas have led to fast growth that remains sustainable.

Tang has also studied short courses to learn how to manage property developments and commercial property investments.

He also mentors other brokers at AUSUN Finance through an MFAA accredited program.

“I have mentored others from day one,” Tang says. “As soon as I learned something, I would share it with others in a systematic way. In the past eight years, I have coached more than 20 brokers from non-industry experience to more experienced brokers.”

Four of Tang’s mentees have won trophies in MPA’s Rising Star awards, including Kiki Feng (2021), Lee Hao (2022), Christine Hong (2023), and Carl Hou (2024).

“And I will keep that track record,” says Tang.

Through his business consultancy service, Tang also teaches brokers about running their businesses like a branch or business centre, and about sta recruitment, training and retention.

Tang says it’s important that brokers know more than just lending policy. Knowledge of tax, legal issues, the commercial property market, valuation risk, technology and money psychology can all a ect lending outcomes.

To help answer new brokers’ basic questions, Tang is developing his own ChatGPT software called Ask Thomas 24/7.

On top of that, he runs an education program to teach people how to do small-scale developments, including a project manager and an architect.

Tang is proud of his involvement in the Army Reserve, now eight years and counting.

“I treat it as my free MBA degree – when I was in uni I didn’t have the money to do an MBA. I have learned a lot in the army’s leadership program – they teach you about how to manage stress, how to make quick decisions strategically, how to look after your people.”

These skills have been useful in his broking career and he encourages other brokers to consider joining the Army Reserve.

Tang says by the time an o cer in the army

“Knowledge you can learn quickly, but experience comes with time – this is why you need to leverage someone else’s experience to ensure that the client’s expectations are met”

Tang wants to help as many clients as possible but says his time is limited.

“So I want to coach other brokers to help them earn money, enjoy work life as a broker and enjoy their growing relationships with customers.”

Those brokers he mentors go on to mentor others.

graduates, it has invested about $1 million in taxpayers’ money into that person. “It’s very appealing and I have no regrets.”

He has also invested in software that generates feasibility studies for development projects.

“I’m keen to launch to the market for all commercial brokers and lenders in coming months.”

A solo broker has market information limits due to volume and bargaining power in front of multiple lenders. More brokers are grouping together to achieve sustainable growth

Partnership and system integration becomes the next challenge for a group of brokers, such as compliance standards, commission splits, marketing directions, culture value, and management style

Only consistent, growing sta can retain a client’s consistent growth. Creating a platform for the team is a higher priority than attracting clients. My success comes from the team behind me

Commercial lending is a big learning curve. Team up with an experienced accountant or nancial planner for business loans, and a good project manager, builder, architect, valuer, QS and property channel agent to make a project successful

Getting support from lenders can be a challenge. Channel con ict still exists. Demonstrate your experience and loyal client relationships, otherwise the lenders may provide their best e orts and compete with you on deals

Over 20 years supporting Australian businesses.

Partner with COG Aggregation’s 2024 Growth Financier of the Year.

Have you explored your opportunities in asset finance? As a trusted name in non-bank lending, we’re a fast-growing, fast-moving commercial lender that goes the extra mile to support brokers, with flexible solutions, attentive service, and reliable access to funding.

Contact us today to find out how we can help you grow your business with our competitive commercial rates for automobile and equipment finance. We keep you moving

Australia is a nation powered by small and medium businesses, so it makes sense that brokers should look to them to diversify their income streams, attract new customers and bolster existing client relationships. Unlike the home loan market, which is highly competitive, much of the commercial lending sector remains untapped by brokers. MPA’s Commercial Lending Guide provides valuable insights for brokers wanting a piece of the action

IN A competitive and constrained residential lending market, it’s a no-brainer that brokers should also o er commercial loans as part of their overall suite of services.

While the home loan refinance market has quietened down considerably since the record levels of 2023 when banks were ferocious in their pursuit of new clients, o ering cashbacks of up to $6,000, there’s still plenty of competition for residential mortgage customers.

More often than not mortgage brokers are now competing with each other for customers, rather than with lenders. The latest research from the MFAA, released in April, revealed that 71.8% of all new residential home loans were written by mortgage brokers, the highest result observed since the measure has been recorded.

While this is great news for the sector, there’s greater competition among brokers for a ‘smaller slice of the pie’ as the number of home loan applications falls on the back of 13 interest rate rises and stubbornly high inflation.

The Equifax Quarterly Consumer Credit Insights report for March 2024 showed that mortgage applications fell 4.5% for the quarter, compared to the March 2023 period.

The property market continues to break records across the nation, and this, combined with slow wages growth and higher interest rates, means lower borrowing capacity for mortgage holders.

In a tight residential mortgage market,

brokers can look to the commercial lending sector to boost their bottom line and strengthen their relationships with existing customers.

The 16th edition of MFAA’s Industry Intelligence Service report, covering the six months from October 2022 to March 2023, showed that less than 30% of mortgage brokers (28.8%) were also writing commercial loans, a drop of 4.1% compared to the previous six months.

This means there’s a big gap in the market – many SMEs are going directly to lenders for their finance requirements, without the help of a broker.

Brokers can gain a competitive edge by o ering commercial loans, becoming a ‘onestop shop’ for their clients’ finance needs.

To explain the advantages and opportunities of commercial finance, MPA is proud to present its 2024 Commercial Lending Guide.

In this comprehensive report, brokers can learn about market trends in three segments – commercial property, SME lending and asset and equipment finance.

Lenders and aggregators discuss the importance of diversification, how they ensure application and credit decisioning processes are fast and e cient for brokers, and how they work with brokers to provide the necessary training and skills to write commercial loans.

The guide also looks at predicted future growth in commercial lending when inflation improves and interest rates are reduced.

Despite various economic pressures, the outlook is improving in the commercial property finance sector as inflation eases and interest rates stabilise. Non-bank lenders say the sector remains strong, especially with SME demand for industrial property

THE CURRENT state of the commercial property finance sector is like looking out of the window – there’s a few grey clouds but clear blue skies are on the horizon.

Commercial property has suffered a variety of problems, including higher interest rates and inflation, rising building supply costs, and labour shortages.

This has made it difficult for businesses to “make the numbers work” and secure finance, but there are positive signs this is turning around.

The latest ABS business finance figures for February 2024 show loan commitments for construction finance rose 31.4%, after a rise of 5.9% in January.

Herron Todd White’s Month in Review March property report predicted another robust year for industrial property, a sector preferred by many investors.

To gain some insights into the sector and the opportunities for brokers and their clients, MPA spoke to Zeb Drummond, chief operating officer at Gateway Bank, David Smith, chief distribution officer at Liberty, Michelle Whateley, NAB’s specialised business bank executive commercial real estate, and Belinda Wright, head of partnerships and distribution at Thinktank.

Whateley says the commercial property market continues to go through a period of adjustment.

“We are still seeing good activity across the sector, but it is off its peak,” Whateley says. “There remains good demand for industrial property. Development activity is continuing and still seeing some rental growth, which has also resulted in owner-occupiers moving to purchase their premises.”

Whateley says activity in the retail property market has improved after a period of reset.

“Office is still in a period of readjustment. We see a flight to quality assets. There is leasing activity, but incentives are high.”

NAB has also seen a softening of yields across valuations for all sectors.

“Residential development activity has significantly decreased, with pressure on feasibilities and builder uncertainty. Sales have been impacted by interest rates and confidence in the delivery of projects.”

Smith says as inflation stabilises and the interest rate environment settles, Liberty

expects business confidence to improve.

“SMEs are well positioned to adapt quickly, creating more opportunities for brokers to provide support,” says Smith.

“At Liberty, we’re seeing both SMEs and investors looking for larger, modern spaces to help meet demand and allow for business growth. These commercial borrowers need trusted guidance, which presents an ideal occasion for brokers to expand their offering and their network.”

Drummond says given the ongoing interest rate environment, Gateway Bank is continuing to see strong demand and enquiry from borrowers looking for more favourable terms.

“Most often this is purely a simple rate decision, but we’re increasingly seeing enquiry from borrowers looking at our longer – up to 30-year – loan terms, which are helping ease financial burden and freeing up working capital for other areas,” he says.

“We see our commercial property lending offering being a fairly natural diversification option for brokers. Our experienced commercial banker can support brokers through the process step by step” Zeb Drummond, Gateway Bank

“Our portfolio is targeted at the smaller end of the market and we’re continuing to see enquiry related to industrial units and retail properties.”

Wright says the past year has been challenging due to inflation, rising interest rates and a changing economic environment, all of which have affected consumer sentiment and the business sector.

“However, despite these generally negative influences, we have continued to see solid commercial property lending activity across

different property asset classes.”

Thinktank remains conscious of numerous challenges facing the commercial office market and of the significant revaluations being revealed. Wright says Thinktank’s latest Monthly Market Focus report focuses on the industrial property space.

“Our view is that this sector remains strong, primarily driven by structurally supported demand leading to exceptionally low vacancy rates. While the prospect of lower interest rates may exert pressure on commercial property

yields, industrial properties have largely offset this through positive rental dynamics.”

Wright says vacancy rates have consistently fallen across all Australian states, with average net face rents experiencing quarterly increases in Q4 2023.

“The underlying supply-demand disparity, coupled with the ongoing demand for modern warehouse spaces, continues to support upward pressure on rents for the more sought after properties and areas.”

Drummond says it is pleasing to see increased demand from residential brokers wanting to become accredited to offer Gateway’s commercial products.

“We definitely see our commercial property lending offering being a fairly natural diversification option for brokers.”

Drummond says it opens up a new segment of the market for brokers with business owners, commercial property investors, be it individuals, companies or trusts. Often the

client’s residential mortgage tends to come with the commercial [loan], o ering brokers opportunities in both segments.

“We’ve had brokers provide feedback that they’ve avoided commercial because it can be too complex. While there can be more complexity than a vanilla home loan, on the whole once you’ve been through the process brokers tend to find that the basics of a commercial deal are very similar to that of a home loan.”

Drummond says an experienced commercial banker at Gateway can support brokers through the process step by step.

Gateway Bank, in keeping with its Pocket & Planet purpose, o ers a discounted green commercial property loan and a suite of fixed, variable, P&I and IO commercial property loans, up to $10 million for business owners

“SMEs are well positioned to adapt quickly, creating more opportunities for brokers to provide support. We’re seeing both SMEs and investors looking for larger, modern spaces to help meet demand” David Smith, Liberty

and investors for purchase and refinance with limited cashout.

Wright says brokers who o er a wide range of solutions to their client base will cultivate stronger and deeper relationships while creating new advocates.

“Expanding into commercial loans, and

SMSF loans which support a growing proportion of commercial property purchases, also unlocks potential new revenue streams.”

Thinktank was originally established nearly 20 years ago as a specialist commercial lender, and so it has deep commercial experience, says Wright. It o ers education sessions designed to

empower brokers to successfully diversify into commercial.

The property lending specialist’s product range is available exclusively through mortgage brokers. It includes full, mid and quick doc, SMSF and lease doc options with loan amounts up to $8 million, maximum LVR at 80% and loan terms up to 30 years with no annual reviews or regular covenant compliance requirements.

“We can provide finance solutions for investors, owner occupiers, PAYG, self-employed and SMSFs using retail, industrial, office space and professional suites along with specialised securities such as boarding houses… our loan terms and serviceability requirements are not restricted by a WAULT or WALE,” says Wright.

Whateley says there has never been a better opportunity for brokers to help business customers with their banking needs.

“Higher interest rates and a slowing economy presents both opportunities and challenges for SME owners,” she says. “Because of this they are increasingly choosing the broker channel as their pathway to a lender.”

This provides brokers with a huge opportunity to lend the assistance and advice that SME owners seek. However, Whateley says this comes with responsibility and brokers choosing to work with business customers must have the skills required.

“Mortgage brokers who are considering moving into the business lending space should invest in their own strategy to ensure that their firm has the capability to offer customers the most professional service possible.

“Support for brokers is available from their aggregator and/or industry body, who can provide the necessary guidance.”

Whateley says mortgage brokers should be open-minded about the options on the table, ranging from personally upskilling through to hiring the services of a former business banker.

“Regardless, the customer experience and the matching of the right advice is paramount.”

Smith says having an open mind to try new

Three out of six of Australia’s CBD markets recorded negative demand over Q4 2023 with Australia’s CBD net absorption totalling -58,700 sqm over the quarter

Negative demand and new office completions pushed the national CBD vacancy rate up from 14.2% in Q3 2023 to 14.9% in Q4 2023

Face rents continue to show resilient growth, although this growth was counterbalanced by an uplift in incentives in some CBD markets

There was an uplift in Q4 2023 office transaction volumes ($1.75bn) when compared to the previous quarter ($1.14bn), with signs that the bid ask spread for prime asset sales campaigns has narrowed over the course of 2023

“Higher interest rates and a slowing economy presents both opportunities and challenges for SME owners. Because of this they are increasingly choosing the broker channel as their pathway to a lender” Michelle Whateley, NAB

approaches and tools will prove vital for brokers looking to unlock options for business customers.

“By embracing the solutions offered by commercial lending, brokers can deepen relationships while expanding the range of customers they can serve,” he says.

As a specialist lender, Liberty has a broad range of commercial solutions which are straightforward and complementary for residential mortgage brokers.

Smith says Liberty’s commercial lending products are highly flexible, with prime, non-prime and low doc choices.

It also offers multiple income verification options and a streamlined application process,

making it easier to gather the required customer information.

“Even when customers have more complex scenarios, the Liberty has the widest credit capacity to provide creative solutions.”

Wright says Thinktank’s relationship manager team has extensive industry experience, and each member is available to provide guidance from workshop to settlement.

“We recommend establishing a partnership with your Thinktank relationship manager and reaching out to them in the first instance. Engaging with a trusted partner who can quickly workshop a loan application, then take

“We can provide finance solutions for investors, owner-occupiers, PAYG, self-employed and SMSFs using retail, industrial, office space and professional suites along with specialised securities such as boarding houses” Belinda Wright, Thinktank

that all the way through to settlement can make all the difference.”

The Thinktank team also understands the various nuances of structuring required for commercial loans, such as special purpose vehicles (SPVs), trust structures or SMSFs, and can help guide the collection of appropriate information required to support any loan application.

Drummond says Gateway prides itself on its collaborative approach to lending with brokers and maintaining responsive turnaround times.

“This approach is delivered in the commercial space through our broker team and our specialist commercial banker, who works through deals with brokers to help deliver great outcomes for brokers and their clients.”

The bank’s dedicated commercial banker has proved valuable for residential-focused brokers looking to diversify into commercial or those with a commercial opportunity coming across their desk for the first time.

“We’re able to assist with initial assessments and support brokers in delivering for their clients as they gain exposure and experience in the category,” says Drummond.

Gateway has also enabled commercial lending through Apply Online, giving brokers easy and convenient digital lodgement.

Smith says Liberty prides itself on working closely with brokers to quickly understand the needs of customers and any critical timelines.

“Recognising there is often more to a customer’s story than what is found in their credit file, we assess each application on a

case-by-case basis,” Smith notes.

“This ensures we are in a great position to support brokers to achieve better outcomes as the application progresses. Encouraging direct communication with our credit assessors and supported by our experienced sales team, this focus provides real comfort for our business partners.”

NAB is one of the largest commercial property lenders in the market, says Whateley.

“Our large team of BDMs are well versed in our appetite. We have the greatest number of business bankers and spread across all parts of the nation.

“Our bankers hold their own delegated lending authorities and are supported by an experienced specialised credit team who are available to workshop the larger transactions in a responsive manner.”

Whateley says that whether the project involves industrial land, an office complex or a medium-size multi-residential unit development, NAB is a staunch supporter of the broker channel and has appetite for lending to commercial property customers.

Smith says he’s confident more brokers will help more commercial customers than ever before in the coming year.

Brokers have continued building networks and referral channels into the business sector and it is up to lenders to “make sure we can support them with this positive momentum”.

“Liberty’s free-thinking approach and consistent performance positions us well to

meet borrowers’ changing needs and work with businesses throughout their growth cycles,” says Smith.

Whateley says ESG considerations will become more prevalent, particularly the carbon emissions of commercial real estate.

“This will be a focus for tenants, purchasers, investors, financiers and will impact valuations,” she says.

Given the housing shortage in Australia, and the recent Housing Australia Future Fund applications, affordable and social housing will also be an active sector.

Looking ahead, Whateley says confidence is expected to rebound when there is more certainty around interest rates, which will create further uplift in activity across the property sector.

Wright says Thinktank maintains the view that interest rates have reached the top of the cycle and momentum is positive for the cash rate to fall in the next 12 months.

“We expect to see stable to good performance in key sectors including industrial, and well supported segments such as childcare and student accommodation,” she says.

“However, due to the flow-on effects of tighter monetary policy, we anticipate some weakness in pockets of retail and strata office.”

Drummond says if the “last few years have taught us anything, it’s making predictions can be a thankless task”.

“That said, much will depend on the interest rate environment, if and when the RBA feels in a position to cut rates and how lenders respond to the predicted cuts will be key.”

If there are, as predicted, two to three cuts in the next 18 months, Drummond says optimism will rise among investors and owners.

“Lenders willing to pass on any rate cuts may be able to win share in this increasingly competitive space.

“If the current trend of growing commercial accreditation continues, more brokers will be able and willing to offer commercial lending to their client base, which will only support growth of the sector.”

Australia’s small businesses have shown their resilience during a difficult economic period. While overall credit demand is lower, SMEs are still reaching out to brokers and lenders to help them grow and navigate challenges

RESILIENCE AND adaptability – these are the traits small business owners must display as they grapple with a variety of pressures.

It’s tough for SMEs in the current economic environment.

Consumer spending is down and interest rates have risen considerably, while burdensome regulations and the higher costs of doing business have also taken their toll.

SMEs are also finding it difficult to secure finance from mainstream banks as their credit appetite for more complex lending wanes.

But in a nation dominated by small and medium businesses, owners have shown they can survive and adapt to new challenges – the recent COVID pandemic being a case in point.

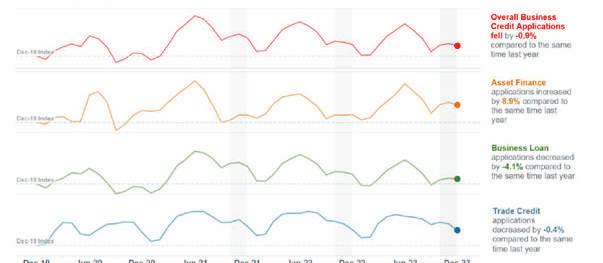

Equifax’s Quarterly Commercial Insights –December 2023 report revealed that overall business credit applications reduced by 0.9% in Q4 2023 when compared to the December quarter in 2022. Business loan applications fell by 4.1%, compared to the December 2022 quarter.

However, non-bank lenders are seeing a rise in SMEs which have adapted to rising interest rates, are wanting to grow and need a range of finance options to do so.

To gauge the SME lending market and the opportunities for brokers, MPA sought the views of two non-banks and an LMI provider:

Prospa director of sales and partnerships

Roberto Sanz, Dynamoney CEO David Verschoor and Helia chief commercial officer Greg McAweeney.

Prospa director of sales and partnerships

Roberto Sanz, Dynamoney CEO David Verschoor and Helia chief commercial officer Greg McAweeney.

Sanz says macro-economic factors, including rising operating costs and inflation, are continuing to place pressure on SMEs, which has forced lenders to re-evaluate their credit risk appetite.

“As a result, there has been a decrease in overall business credit applications,” says Sanz. “However, Prospa has seen significant growth in partner engagement, with the number of partners actively submitting leads up 22% year-on-year, which suggests that SME lending demand persists.”

Sanz says in direct response to the challenges contributing to the fall in credit applications, many small business owners may feel their eligibility for finances is

Overall business credit applications fell by -0.9% compared to the

increasingly complex to understand.

“As a result, SMEs have been actively seeking advice from brokers to navigate these challenges and secure the funding they still demand,” Sanz says.

McAweeney says the decline in business credit demand has predominantly been driven by the construction, retail and hospitality industries.

“This is largely due to the decline in business activity and consumer spending and the rising interest rate environment,” says McAweeney.

“While overall business lending has declined in NSW and Victoria, the recovery of the mining sector has led to an increase in the demand for business credit in Queensland, South and Western Australia, as identified in the recent Equifax Quarterly Commercial Insights (December 2023).”

Verschoor says 2023 was a tougher year for SMEs, with increasing interest rates and the high cost of doing business being major themes,

Asset nance applications increased by 8.9% compared to the same time last year

Business loan applications decreased by -4.1% compared to the same time last year

Trade credit applications decreased by -0.4% compared to the same time last year

“With business lending being the second largest lending market in Australia after residential lending, catering to SMEs presents an excellent opportunity for brokers to diversify and expand their business” Greg McAweeney, Helia

“but we’re seeing the sector adapt to these challenges”.

“Although the market may have seen falls, Dynamoney has experienced growth thanks to the launch of new products and securing additional funding for more loan capacity.”

SMEs usually maintain more direct relationships with their customers and suppliers, which allows them to work together on mutually beneficial solutions to challenging market conditions.

Verschoor says SME application volumes at Dynamoney have risen this year. “Asset finance solutions and business loans are the most sought after, showing a desire to invest in growing a business rather than refinancing previous loans.”

The non-bank lender has launched its Business Overdraft Mastercard Account, the first business overdraft account to come with an interest-only Mastercard credit card, giving SMEs maximum flexibility when accessing financing.

Verschoor says SMEs are adjusting to the new interest rate landscape and looking to grow again.

“We’re seeing increased application volume for a number of our products, and encouragingly, from a wide range of industry sectors spanning transport and renewable energy, through to IT and retail.”

The applications, strongest across business loans and equipment financing, signal that SMEs are investing in expansion and growth instead of refinancing.

Verschoor says SMEs still require simpler access to capital to guarantee free cash flow.

“Dynamoney’s asset finance solution means you can purchase almost any business asset imaginable.”

Sanz says as challenging market conditions persist, Prospa has identified an SME growth opportunity called the Established Small Business segment, for SMEs with at least two years trading and an average monthly turnover of $100,000 plus.

“These businesses are more likely to explore the value of alternative lending through a financial adviser and are generally able to service greater loan amounts,” he says.

“We have attributed an increase in the average loan value of 14.7% written by Prospa Partners, year-on-year, to this segment.

“On top of this, we’re continuing to see a lot of traction within the professional services, retail and hospitality industries.”

As a lenders mortgage insurance provider, Helia currently offers an SME residential product which is being assessed by lenders, says McAweeney. It enables SMEs to use their existing residential property to access funding.

“These offerings can be structured either as a single upfront payment or as a monthly premium, mirroring the approach taken with Helia’s traditional residential LMI.”

Opportunities, partnerships

McAweeney says Helia has engaged with a range of business brokers and lender

partners to assess the credit requirements of SMEs.

This identified a growing demand for enhanced access to credit, allowing banks to broaden their lending capacity by extending limits on LVRs and loan sizes.

“Helia’s collaboration with brokers in the

loans coming soon, just in time for EOFY.”

Verschoor says SME financing is built to fit the lives of SME decision-makers, meaning it is decentralised and easy to access, so it’s convenient for business people always on the move.

“Brokers are very accustomed to working

“Prospa has seen significant growth in partner engagement, with the number of partners actively submitting leads up 22% year-on-year, which suggests that SME lending demand persists”

Roberto Sanz, Prospa

SME lending space expands their market reach and allows them to offer innovative products and services to a wider audience of small to medium-sized businesses to support them in achieving their goals and drive economic growth,” says McAweeney.

Sanz says broker partners can tap into SME finance opportunities by building awareness, creating appetite, and providing access to funding solutions to their network of existing and new self-employed business clients.

“We have a dedicated team of BDMs that get to know your clients’ businesses and provide fast, tailored solutions, and offer resources to help partners find and win more business in the market.

“We understand the value of relationships in finance and the 22% growth in partner engagement, year-on-year, tells us the support we offer to our partners is working.”

Sanz says Prospa remains committed to empowering its partners to strategically engage with clients and grow their business.

“We are continuing to invest in the broker channel, with a new tool to improve and ease the experience of writing of business

with clients in an agile way, so Dynamoney has always invested in developing the most effective online lending platform in the market to fit both client and broker needs.”

Verschoor says the non-bank’s products are listed with most aggregators, and “we are always investing in education initiatives to help mortgage brokers expand into SME lending services”.

“Our lending platform is safe, convenient, fast, easy for brokers to use, and we’re constantly enhancing it, having just added new security and application processes that further reduce loan approval times.”

Loan approvals take a few minutes, and Dynamoney’s large BDM team can help brokers with their applications.

Sanz says SME lending offers brokers an easy path to understanding and writing business loans and building protection around their existing loan book.

He says many small business-owners feel their finances are complex and are more comfortable dealing with a broker than with a bank or finance company.

“Leading lenders, like Prospa, provide tailored support and experience-driven advice to help brokers tap into hidden value, creating stickier relationships, and building new revenue streams.”

McAweeney says given the dynamic nature of business lending, brokers can leverage their relationships with borrowers to o er holistic finance support.

He says diversifying into SME lending is compelling for brokers for a number of reasons, including:

• expanded market opportunities. There’s a growing demand for financing solutions tailored to suit unique SME needs, and brokers can tap into this large and under-served market segment;

• additional revenue streams;

• expanded existing client base – many SMEs already have established relationships with brokers for other financial services. By o ering SME lending, brokers can deepen these relationships and become a trusted partner for their client’s financial needs;

• providing value-added services to their clients beyond traditional mortgage brokerage services; and

“Our lending platform is safe, convenient, fast, easy for brokers to use, and we’re constantly enhancing it, having just added new security and application processes that further reduce loan approval times”

David Verschoor, Dynamoney

• competitive advantage – brokers who o er SME lending services can di erentiate themselves from other brokers solely focusing on residential.

“With business lending being the secondlargest lending market in Australia after residential lending, catering to SMEs presents an excellent opportunity for brokers to diversify and expand their business,” McAweeney says.

Verschoor says the 2.5 million SMEs in Australia are the lifeblood of the economy, making up more than 97% of registered businesses.

“They are looking for faster, easier, safer lending solutions and are seeking the support of finance professionals like brokers to help

them navigate the market,” he says.

Diversifying into SME lending can increase the value brokers can provide to their clients, helping enhance client retention and revenue per contact.

“With a large number of home and property buyers having a small to medium-sized business, the opportunity for brokers to build stronger pipelines into mortgage lending is very real.

“Additionally, successful SME loans maintain upfront brokerage and commission payments for brokers, a consistently strong revenue channel.”

Verschoor says that Dynamoney has a comprehensive suite of working capital and asset finance products for SMEs designed to be better for business, including its new Business Overdraft Mastercard Account.

He says the non-bank can help SMEs with all their financial challenges, from ensuring free cash flow, financing new equipment, covering the cost of overheads such as insurance and accessing capital for growth.

“Our system is built for SME lending, with an experienced team focused on ensuring brokers and customers secure financing as fast as possible.”

Sanz says Prospa has delivered more than $4 billion in funding, helping over 54,000 small businesses manage their cash flow and fund growth opportunities with business loans up to $500,000 and a business line of credit up to $150,000.

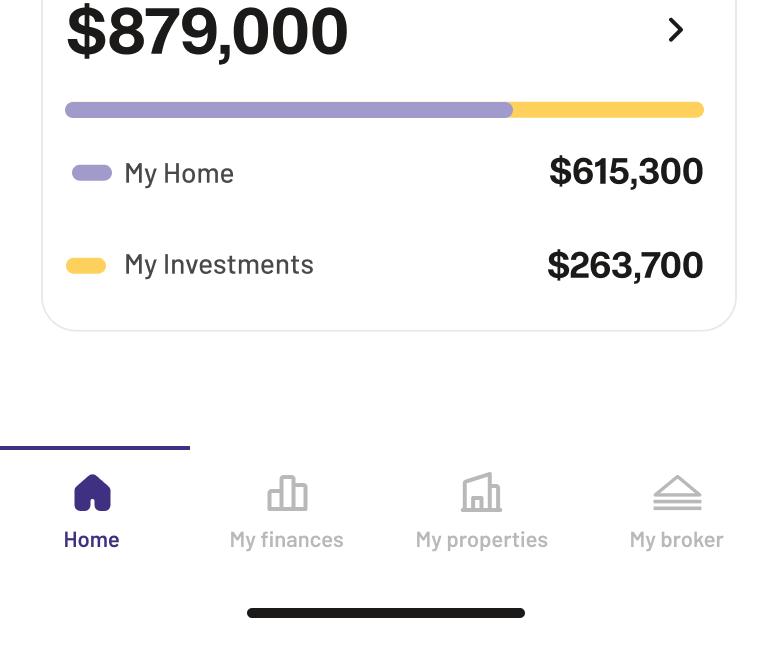

Unlock your property’s full potential with the new Aussie app

Get real-time property value estimates

Track your home loans and equity

Connect with your local Aussie Broker

SMEs are increasingly looking to brokers and their lender partners for assistance in accessing loans to fund asset and equipment. MPA sought the views of experts in this sector to learn more about the market

IT’S FAR too early to say when the asset and equipment finance sector will return to full health, but there are signs that a recovery is brewing and more opportunities await brokers and their customers.

Equifax’s Quarterly Commercial Insights Report showed that asset finance applications had risen 8.9% in the December 2023 quarter compared to the Q4 2022. That was a much better result than business loan applications, which fell -4.1% in Q4 2023, and trade credit applications, which were down 0.4% Business confidence rose one point to +1

in the NAB Monthly Business Survey for March 2024, with signs that supply and demand are coming into better balance with capacity utilisation continuing to ease. Businesses are still feeling the effects of higher costs and interest rate rises, but non-bank lenders and aggregators are reporting an increase in demand for asset and equipment finance, especially as supply chain problems ease.

To understand the market and how brokers can grow their business in this space, MPA spoke to Blake Buchanan, general manager of SFG; Tom Caesar,

group executive – asset finance at LMG; Ken Spellacy, general manager asset finance, Pepper Money; and Danny Tuttlebee, head of sales at Resimac Asset Finance.

While there was an uptick in demand for asset finance in Q4, Buchanan says over the longer term growth had been flat or declining for several years prior to the December 2023 quarter.

“So whilst the bump is great news, it is a modest improvement when averaged over a couple of years,” says Buchanan. “It is likely due to people that were holding off on new or replacement assets that had a wait-and-see mentality, with the higher cost of goods and lifting interest rates affecting their choices.

“Having more confidence with the higher cost peak nearly behind us and rate environments easing off usually spurs on activity, which is what we are seeing here.”

Caesar says the industry is experiencing a shift in demand.

“Our [LMG] asset finance brokers around Australia have reported that their SME clients are prioritising cash flow in the current environment, therefore relying more on their borrowing capabilities,” Caesar says.

Business owners have been seeking to de-risk their businesses from any negative economic impacts, such as the uncertainty around interest rates and the general economic outlook.

“They’re keen to strike a balance between cautious optimism and realistic expectations,” says Caesar.

“With recent improvements in the supply chain, access to both equipment and transport assets has been easier than in previous years, and that’s been reflected in healthy levels of enquiry and applications.”

Spellacy says despite the challenging market, Pepper Money is still seeing opportunity across various segments where there is robust demand for financing assets

such as equipment, vehicles, and machinery.

Several factors are contributing to this demand, including more favourable interest rates encouraging financing activity.

“Some segments of construction and manufacturing are still experiencing growth, and we are seeing general resilience in the mining, agriculture and logistics space,” Spellacy says. “There is also most likely some post-pandemic economic recovery still occurring, with business strategically buying assets to boost productivity and drive growth.”

Tuttlebee says Resimac’s data and feedback reveal that the strong end to 2023 was helped along by record truck sales, up 7.6% on 2022.

“The automotive industry also had record numbers in 2023, with sales surpassing 1.2 million new vehicle sales,” says Tuttlebee.

“This growth has been driven by several things. Continuous government spending in infrastructure is certainly a factor, as well as overseas migration increasing by a third from 2022 to 2023.”

Tuttlebee says early numbers this year already suggest a strong start for the automotive industry, with a continued increase in electric vehicle (EV) take-up, “and

Overall business credit applications reduced by -0.9% (vs December quarter 2022)

Business loan applications decreased by -4.1% (vs December quarter 2022)

Asset finance applications increased by +8.9% (vs December quarter 2022)

Money’s broker partners has always been: “make it easy for me to do business”.

“That feedback sits at the heart of everything we do. Because when our partners succeed, so do we.

“We are clear and consistent about our appetite and service levels, with the aim to provide certainty for our brokers. We offer a broad range of solutions for a wide range of

“SFG brokers experienced significant year-on-year growth and the demand for more asset and equipment accreditations has never been greater. Our brokers are seeing greater levels of enquiries from new and existing clients”

Blake Buchanan, SFG

we’re cautiously optimistic about the economic outlook for the remainder of 2024”.

Spellacy says constant feedback from Pepper

customers, allowing brokers to consider us as a one-stop shop.”

Spellacy says Pepper Money prioritises ease of doing business by implementing intuitive systems.

“Brokers find it straightforward to engage with us. We support the broker through the life cycle of the customer, providing retention opportunities to the introducing broker when a customer is considering buying a new asset, or at key milestones in the contract term.”

Resimac prides itself on its broker relationships, says Tuttlebee.

“We have come a long way in a short period of time and one of the key drivers for this success has been our willingness to listen to brokers.

“We regularly seek broker feedback on our products and services, enabling us to provide better solutions for Australian SMEs that are seeking funding to grow their business.”

Tuttlebee says Resimac made some major product changes late last year, one of which was an increase to funding limits on its Lite Doc product.

“The feedback we received was that trucks had become more difficult to fund. Inflation had driven up prices, and meeting the higher lending requirements meant brokers had to provide full financial analysis solutions through banks.”

The Lite Doc change gave businesses access to those greater loan limits through Resimac simply by using the two most recent activity statements and tax portal statements.

“This is one of many examples where Resimac Asset Finance has developed products off the back of broker needs. One of the benefits of being a lender our size is that we can move quickly when market conditions changes,” says Tuttlebee.

Supporting the growth of its brokers is at the forefront of LMG’s activities, says Caesar.

The aggregator’s extensive events calendar features LMG professional development days, as well as asset finance and commercialspecific PD days.

“We provide brokers with access to a range of online training courses and opportunities to network, upskill and educate themselves in the ever-changing finance industry,” Caesar says.

LMG also provides its brokers with leading technology solutions, including integration of MyCRM and Nodifi, allowing asset finance, commercial and residential deals to be written and housed in the one platform. This centralised platform enhances brokers’ productivity, freeing up their schedules to spend more time supporting their clients.

Caesar says LMG’s holistic marketing suite, including email communications, reviews and social media content, not only allows brokers to nurture relationships with clients, but also expand their reach and grow their business.

Buchanan says brokerages are becoming more sophisticated, scaled and diversified, allowing for deeper customer discussions around clients’ more wholistic financial needs.

“Our central learning and development platform, Brokerversity – exclusively available to LMG brokers – also educates brokers so they can diversify into asset finance and commercial finance, successfully”

Tom Caesar, LMG

“When consumers don’t think something can be done, they don’t do it. When a customer is given credit advice that would be of benefit to them, they will usually act on it.”

Buchanan says SFG brokers experienced significant year-on-year growth and the

demand for more asset and equipment accreditations has never been greater.

“Our brokers are also seeing greater levels of enquiries from new and existing clients. This points to both an increase in market share but also some consumers who have paused their property finance aspirations to pursue other investments and finance requirements for their business purposes.”

Tuttlebee highlights the value of diversifying for mortgage brokers, with the most obvious route being to provide customers with asset finance solutions, “whether they’re PAYG clients who need a car to get the kids to weekend sports, or it’s the $300,000 prime mover that their truck driver client needs to take on a new and more lucrative contract”.

Resimac, a well-known non-bank mortgage business, did exactly this three years ago when it diversified into asset finance.

“Our initial offering focused on lending solutions in commercial asset finance, but we’re growing our product offering quickly. We recently launched our mortgage securitybacked short-term business loan (SBL), and later this calendar year will see us launch our consumer product and then move into novated leasing,” says Tuttlebee.

Resimac’s asset finance team has grown nearly 10 times in three years, with several internal account managers and broker

support staff on hand to assist mortgage brokers with moving into commercial asset finance.

This support can include helping brokers with a quote for their clients, packaging together a Resimac deal, walking them through the simplified processes, and providing a deeper understanding of not only the products “but why we may be asking for certain information or paperwork”.

Spellacy says it’s a great time for brokers to consider how they diversify into asset finance and support customers seeking access to asset finance solutions.

“First port of call for a broker should be with their aggregator. Aggregators can provide a broad range of information, training and support to a broker looking to diversify. Many aggregators offer different customer application pathways like spotand-refer programs.”

Spellacy advises brokers to familiarise themselves “with the asset types that your customers will require”.

Many residential mortgage customers may be considering an EV, so brokers need to become experts in this fast-expanding segment.

“Commercial clients will often require equipment finance on a regular basis, so it’s worthwhile understanding how you can best support them across their changing needs,” says Spellacy.

“Gradually start to introduce asset finance into your business and build out strong customer processes and journeys to ensure your customer is getting a great experience.”

Buchanan says that when it comes to diversification, SFG “takes the approach of education, connections and strategy”.

“Education empowers brokers with what can be done and identifies the opportunities that are within their current model, along with the open market.

“Connections is about the right partnerships with the right people and providers. The strategy is about planning, implementing

and making sure you have the right structure to execute against that and steer you towards your goals.”

Buchanan says SFG operates a busy education program at specific commercial and asset PD days, conventions and other events such as webinars and content libraries.

“It is one thing to know about it, but how you implement it is equally as important. This is where we take an individual approach with our members to assist them with their plans and implementation around business growth, improvements and diversification.”

insights from LMG experts.

Integrations with MyCRM and Nodifi create a “single source of truth to give brokers a 360-degree view of their customers across residential, commercial and asset finance on the one platform”.

Caesar says any cash rate movements will affect borrowing costs and influence market sentiment.

“In the next 12 months, various factors will influence growth in asset and equipment

“We support the broker through the life cycle of the customer, providing retention opportunities to the introducing broker when a customer is considering buying a new asset or at key milestones in the contract” Ken Spellacy, Pepper Money

Caesar says LMG supports brokers to diversify into asset and commercial finance in multiple ways.

Its newly created Referrer to Writer program is an intensive course for residential brokers who are currently referring asset finance deals but want to transition to writing their own.

The program is facilitated by the knowledgeable business success managers (BSMs) of LMG Asset Finance, helping brokers to build the capacity to write those deals internally.

“Our central learning and development platform, Brokerversity – exclusively available to LMG brokers – also educates brokers so they can diversify into asset finance and commercial finance, successfully,” says Caesar.

The library of online courses and webinars provides demonstrations and best practice

finance and the impacts will be different across separate sectors. For instance, in agriculture, farm equipment financing could see growth due to advancements in technology, the need for modernisation and recent seasonal conditions,” he says.

In the mining sector, demand for equipment finance may rise with increased exploration and extraction activities.

“We’ve seen dealerships offering discounts on vehicles and that could stimulate growth in the automotive sector,” says Caesar.

“Government incentives for the purchase of electric vehicles could encourage increased financing demand.”

Buchanan says broker market share will continue to grow in this sector, as a direct result of brokers continuing to upskill and diversify.

He says the general easing of costs with inflation coming down, the costs of goods

Discover opportunities in SME lending by partnering with Australia’s #1 online small business lender.

Funding options up to $500K

Fast applications, quick decision and funding possible in hours for your clients

Attractive commissions, plus education & tools to help you find opportunities in your database

Get in touch

1300 964 808 prospa.com/partners

“We recently launched our mortgage security-backed short-term business loan, and later this calendar year will see us launch our consumer product and then move into novated leasing”

Danny Tuttlebee, Resimac Asset Finance

easing and more cash available due to tax reform will result in increased consumer confidence and capacity to purchase.

“This will of course result in higher activity and more financing of goods in the near term.”

The EOFY will also trigger activity as

businesses either fit new purchases into the current tax year or wait to acquire equipment in the new financial year.

“Brokers should be prepared for this and be proactive with their client communications to make sure they are at the forefront of their clients’ minds for these inevitable

purchases,” Buchanan says.

Tuttlebee says in the forthcoming year, asset and equipment finance are poised for growth in certain areas. Several factors will be instrumental in shaping this growth –most notably the focus on reducing carbon emissions.

“Electric vehicle sales have surged, nearly tripling in growth between 2022 and 2023. This emphasises a groundswell of interest in cleaner transportation solutions,” he says.

Tuttlebee says government spending on infrastructure projects is expected to remain robust. However, the asset finance industry is not completely out of the woods just yet, with larger construction companies – which previously drove a sizeable portion of sales in this market – still grappling with the repercussions of the pandemic, he says.

“The good news is that construction is going to pick up again soon. Housing shortages and a growing migrant population means the demand for property is only going to get stronger, and this will drive a steady flow of new construction projects.

“Businesses that win the tender for these upcoming projects are great candidates for asset finance solutions.”

Spellacy says new car sales serve as a strong barometer for the industry’s health.

“We continue to witness remarkable records being set for car sales. Nine of the last 12 months have been a record for new car sales, which is an indicator that the supply constraints the pandemic caused have gradually eased.”

EV and hybrid sales also outperform expectations, says Spellacy.

“As we fast approach the end-of-financialyear period, the impact of the tax write-o scheme will come into play.”

He says although the current tax write-o scheme is less favourable than in 2023, “we are seeing some significant improvement in other factors, such as interest rates easing, and inflation being at lower levels compared to the same period last year”.

Empowering you to achieve more for your clients.

Giving you more certainty on the outcome for your clients.

Easy access to responsive, experienced, dedicated support every step of the way.

Equipping you with the right tools, so you have access to accurate information for your clients.

Continuously adapting policies and processes, making it easier for you to do business.

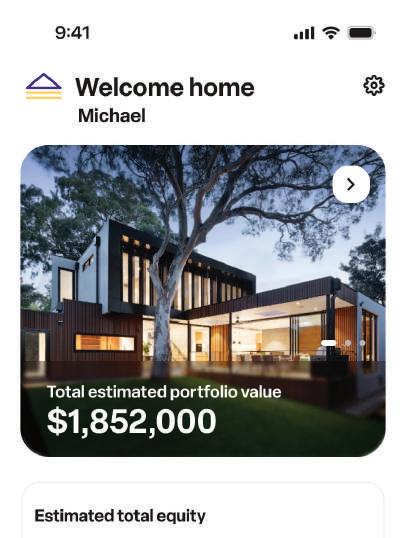

Aussie’s new mobile app provides customers with smart, easy access to property values, equity and loan details and drives engagement with brokers, says Lendi Group chief product officer Travis Tyler

IN A WORLD of smartphones, everyone wants instant access to services and information.

We do everything on our mobiles – banking, paying bills, booking travel, restaurants and tradespeople, as well as using them like modern day encyclopaedias for whatever we need to know.

In a nation obsessed with buying and selling homes, it’s no surprise that people want property data at their fingertips.

Aussie Home Loans, part of the Lendi Group, has now launched an Aussie mobile app that allows customers to keep track of

equity, their credit score, the value of their home, properties they are considering, as well as their loan finances.

Lendi Group chief product officer Travis Tyler explains to MPA the features and benefits of the Aussie mobile app for customers and brokers, the smart technology behind it, what brokers think of the app and what future enhancements are planned.

What drove the project

Tyler says Aussie realised there was no simple way for Australians to visualise the value of their home or investments.

“We know that over 95% of Australians use a smartphone, and we could see high visitation to our website and usage of our platform from mobile traffic,” says Tyler.

“This tells us that there was an opportunity to meet our customers where they are with an aesthetic, functional, mobile-optimised experience. So we set out to create a tool that allows first-time buyers, homeowners and tycoons alike to unlock their property potential.”

Tyler says Aussie is excited to be facilitating a new wave of digital engagement for brokers and customers, and putting property ownership within reach of more Australians.

He says previously there was no single experience that allowed homeowners and buyers to monitor the value of their property, or properties they’re interested in purchasing, or visualising the equity they’ve built.

“The Aussie mobile app allows customers to gain insights into the property landscape and e ortlessly manage their home value, equity and loan finances in one place.

“The app helps users to better understand their financial position, and then seamlessly connects them with their local Aussie broker to act on it.”

There’s a range of advantages that the app provides, says Tyler.

“New buyers can use the app to gain instant

lators, check the status of their loan application, track their credit score, and book an appointment directly into a broker’s diary with a choice of how they meet – phone, video call, or in-person,” says Tyler.

The app empowers customers to make smart financial decisions in a secure and convenient way. Featuring a clean interface and simplified mortgage terminology, the app is easy to use and navigate, Tyler says.

“Customers can also be assured that their personal information is safe, with secure two-factor authentication and face ID login.

“With the Aussie mobile app, our brokers businesses are now in the palms of their customers,” says Tyler. “The app presents our brokers with a

“The Aussie mobile app allows customers to gain insights into the property landscape and e ortlessly manage their home value, equity and loan finances in one place” Travis Tyler, Lendi Group

access to nearly 11 million properties, build a wish list and keep tabs on crucial property data during their search, including value estimates, rental yields and purchase history, which provides leverage for o ers and price negotiations.”

Investors can also track fluctuating property prices, which provides insights on the rental market and the financial health of and return on investments.

Tyler says property owners can discover the worth of all their properties in real time and enlist their broker to help unlock available equity to fund their next purchase or renovation.

Savvy customers can even take control of the home loan application process. The app also facilitates ease of broker-customer engagement “like never before”.

“Customers can now access home loan calcu-

new way to introduce customers into their world and build relationships in the digital age.”

Lendi Group’s multi-channel distribution model gives customers choice in how they engage their broker, and with the app “we’re expanding the breadth of choice and paving the way for even stronger, easier connection”.

Tyler says allowing customers to visualise their equity position opens additional business opportunities for brokers.

Features such as e-consent, document upload, and application tracking also minimise administration and follow-up, streamlining the appointment preparation and loan application processes.

“Reducing communication barriers and manual handling will add capacity into our brokers’ businesses so they can direct their attention to creating exceptional service experiences and driving revenue,” Tyler says.

The app allows customers to:

Build a property wish list

Access key data such as value estimates, rental yields and purchase history

Discover the worth of their properties in real time

Book a broker appointment to access support or unlock equity

Utilise home loan calculators

Check the status of their application

Tyler says following a soft launch in February, early signs point to the Aussie app being a winner for all involved.

“Our brokers have embraced the app with enthusiasm, embedding it into their sales processes, while strong review scores across Apple and Android indicate our customers are very receptive to the new value we’re delivering.”

One customer review says: “I have been keeping track of my property portfolio via a spreadsheet for the longest time, so I’m glad to find a tool to do this for me.”

Nathan Misell, franchisee at Aussie Blackwood, Mount Barker and Palmerston in the Adelaide Hills, says having direct broker input as the app evolved ensured the app would remain relevant.

“The app is going to provide our customers with a huge amount of benefit and allow us as brokers to ensure that our clients are in the best financial position that they can be in, not only now but into the future,” Misell says.

“I’m excited to see further enhancements and features that the app can provide to our current and future customers.”

Senior Aussie Mobile broker Samantha Harvey says she can see the app supporting her business “by delivering knowledge to my clients, keeping my services front of mind, facilitating more meaningful conversations, and saving me time by having more informed customers”.

“The exciting part is that this is just the beginning,” Harvey says. “As it is, the app o ers so many benefits, but with Aussie’s vision of continuous improvement and innovation, it’s going to be a game changer for brokers and customers.”

The core product development team for the app consisted of two engineers, one designer and one product manager, says Tyler.

“This small, tight-knit team allowed us to move with great agility, hypothesising, testing, and learning at lightning speed.”

Many other parts of the Lendi Group also supported the app’s development, including

“Our brokers’ businesses are now in the palms of their customers. The app presents our brokers with a new way to introduce customers into their world and build relationships”

Travis Tyler, Lendi Group

distribution, operations, risk and compliance, and legal teams.

Tyler says brokers, who are well attuned to customers’ needs, also played a core role in the development phase.

Top-performing brokers from the Signature Program were key consultation partners during the design and build.

“The app was piloted with 72 brokers across the country over a three-month period, where their valuable user insights supported us in optimising the product for launch,” says Tyler.

“The product discovery phase ran for six months, as we built, deployed, and validated our first concepts with brokers and prospective users.”

The first beta-app version was delivered in September 2023.

“Since then, we’ve continued to refine and iterate, evolving the Aussie mobile app into a customer-ready digital experience which went live on the Apple and Google Play app stores in February 2024.”

Tyler says there are plans to enhance the app, based on broker and customer feedback.

“We’ve already got exciting updates in development, including push notifications that will serve relevant updates at crucial touchpoints in the customer and homeownership life cycle, allowing brokers to connect with customers in a new way.

“In the future, we plan to add open banking for real-time loan balances and interest rates.”

The app is going to provide our customers with a huge amount of benefit and allow us as brokers to ensure that our clients are in the best financial position that they can be in, not only now but into the future