NARROWING NEW JERSEY’S RACIAL WEALTH GAP THROUGH HOMEOWNERSHIP Recommendations for the New Jersey Housing and Mortgage Finance Agency Princeton University School of Public and International Affairs December 2021

TABLE OF CONTENTS Executive Summary

4

Introduction

6

1. Outreach, Partnerships, and Community Collaboration

10

1.1. Employ a targeted home buyer strategy to prioritize outreach with underserved communities

11

1.2. Expand lender and real estate professional relationships with strong ties to communities of color and leverage their outreach capacity

13

1.3. Enhance community engagement and partnerships strategy to build trust with home buyers of color

15

2. Down Payment Assistance

18

2.1. Increase the base DPA amount to $14,000, and fix DPA to the maximum home purchase price

18

2.2. Leverage New Jersey Individual Development Accounts to increase available assistance to first-time home buyers

21

3. Foreclosure Prevention

23

3.1. Contract with one or more qualified CDFIs to purchase and service nonperforming loans

24

3.2. Target urban areas for bulk purchases of defaulted mortgages

25

4. New Programs and Innovations

27

4.1. Establish a statewide Homeowner Rehabilitation Assistance (HRA) program

27

4.2. Target first-generation professionals

31

4.3. Develop a comprehensive ‘northern county’ strategy to promote landlords of color

35

4.4. Improve access to community land trust (CLT) homeownership opportunities among low-income households

37

5. Agency Strategy and Process Improvement

40

5.1. Develop an annual NJHMFA strategy informed by racial equity and community input

40

5.2. Embed racial equity in goal setting and programs

42

5.3. Leverage digital platforms to improve efficiency and user experience

45

Conclusion

48

Acknowledgements

50

Endnotes

52

3

EXECUTIVE SUMMARY New Jersey has striking racial wealth inequality. While the Garden State’s median household net worth is the highest in the nation, its racial wealth gap is among the widest. The state’s legacy of slavery, racially restrictive covenants, redlining, predatory lending, and other forms of structural racism underlie the disparities in median net worth among white ($352,000), Black ($6,100), and Latino ($7,300) households.1 Inequitable access to homeownership is a primary driver of the racial wealth gap. The racial homeownership gap in New Jersey is wider than the national average with 76 percent of non-Latino white households owning a home compared to only 38 percent of Black households and 39 percent of Latino households.2 Low- and moderate-income New Jersey families face major barriers to purchasing their first home, including down payment, barriers to credit, a constricted supply of housing, and some of the highest housing prices in the country.3 This report provides the New Jersey Housing and Mortgage Finance Agency (“NJHMFA” or “Agency”) with recommendations to promote equity in access to homeownership across New Jersey. It addresses four principal goals set forth by the Agency: a) promote wealth creation, b) target neighborhoods for stabilization, c) support anti-gentrification efforts, and d) narrow the state’s racial wealth gap. The authors analyzed NJHMFA’s programs and internal data, conducted independent research, and met with housing stakeholders across the country to determine challenges, 4

innovations, and best practices around homeownership in New Jersey. Our recommendations fall into the following five categories:

1. OUTREACH, PARTNERSHIPS, AND COMMUNITY COLLABORATION

NJHMFA should look to community partners as sources of expertise, opportunities for collaboration, and forums for expanding access to underserved communities. We recommend a variety of new strategies to raise awareness of the Agency’s programs among home buyers of color and make the case that community collaboration should be a central part of the Agency’s strategies.

2. DOWN PAYMENT ASSISTANCE

NJHMFA should increase the baseline Down Payment Assistance (DPA) amount and respond to the wide variation in housing markets across the state. We offer a sliding scale framework for DPA and new ways that NJHMFA can partner with the state’s Department of Community Affairs to build pathways to homeownership through individual development accounts.

3. FORECLOSURE PREVENTION

NJHMFA should leverage its new authority under the New Jersey Foreclosure Prevention Act to stabilize neighborhoods and help prevent a wave of foreclosures across the state. We explain how the Agency can partner with qualified Community Development Financial Institutions (CDFIs) and target urban areas in order to maximize the reach and impact of its Residential Foreclosure Prevention Program.

4. NEW PROGRAMS AND INNOVATIONS NJHMFA should expand its suite of homeownership products to benefit more segments of the population, support antigentrification efforts, and promote climate resilience. We propose new programs and innovations that would provide home rehabilitation assistance to low-to-moderate income homeowners and buyers, mortgage assistance to first-generation professionals, financial support and counseling to potential landlords of color, and improved access to mortgages in community land trusts for lowto-moderate-income home buyers.

5. AGENCY STRATEGY AND PROCESS IMPROVEMENT

NJHMFA should clarify its own goals for promoting homeownership with an eye toward racial equity and maximizing the impact of the Agency’s programs. We outline the steps necessary to create a strategic plan, build a racial equity framework and update Agency practices to better position NJHMFA to serve more home buyers of color.

5

INTRODUCTION The New Jersey Housing Mortgage and Finance Agency is an independent state agency responsible for promoting affordable rental and homeownership opportunities for low-and-moderate-income New Jersey families.4 To meet this important mission, NJHMFA gives financial assistance and partners with mortgage lenders and community development stakeholders to fund mortgages for first-time home buyers, prevent foreclosures, and support housing construction.5 The NJHMFA Down Payment Assistance (“DPA”) Program is a statewide housing finance program that provides qualified firsttime home buyers with $10,000 to use toward down payment and closing costs.6 DPA is

designed to encourage homeownership and promote neighborhood stability by providing an interest-free, five-year forgivable second loan with no monthly payment.7 The program must be paired with a loan from the First-Time Homebuyer Mortgage Program.8 In recent years, the Agency has provided 1,300–1,400 DPA loans annually, and it expects to provide around 2,000 loans per year in future years. In March 2021, New Jersey Governor Phil Murphy signed into law the New Jersey Foreclosure Prevention Act. The Act created the Residential Foreclosure Prevention Program, which allows the Agency to purchase defaulted mortgage loans from banks and other financial institutions.9

FIGURE 1. NEW JERSEY HOMEOWNERSHIP RATE BY RACE AND ETHNICITY, 2019

Source: “2019 American Community Survey 1-Year Estimates,” Table S2502, U.S. Census Bureau, figure generated on November 15, 2021. Note: The households of color homeownership rate was calculated by dividing the sum of all nonwhite owner-occupied units by the sum of all non-white occupied units. “HH” stands for households. Each bar and demographic group is in units of households.

6

FIGURE 2. NEW JERSEY RACIAL HOMEOWNERSHIP GAP, 2009–2019

Source: “American Community Survey 1-Year Estimates,” Table S2502, U.S Census Bureau, 2010-2019, figure generated on November 15, 2021. Note: Projections of the homeownership rate were calculated using a depreciation rate of 0.32 percent per year, the average percentage point change in the racial homeownership gap between 2010 and 2019. Population projections after 2019 were calculated using the average percentage point change in number of households for each demographic group between 2009 and 2019.

The gap in homeownership between white households and households of color is 33 percentage points, as of 2019. These disparities exist in the context of a state with a history of anti-Black racism that includes slavery, racially restrictive covenants, redlining, and predatory financial practices.10 And they contribute to the state’s staggering Black– white wealth gap. The median household wealth among white families in the state is $352,000; for Black families, it is $6,100—a disparity of 58-to-1. The state’s racial wealth gap is also driven, in part, by disparities in property values. In cities with large Black populations such as Camden and Newark, median

home values are substantially lower than in predominantly white towns such as Cherry Hill and Millburn.11 In addition, predatory lending practices targeted Black and brown communities in the lead-up to the Great Recession, further suppressing home values and causing disproportionate rates of foreclosure in communities of color throughout the state.12 New Jersey’s racial homeownership gap has not significantly narrowed in 10 years despite the number of households of color growing by 18 percent within the same period. If these patterns persist, New Jersey’s racial homeownership gap will remain 24 percentage points in 100 years (see Figure

7

FIGURE 3. INCREASING THE HOUSEHOLD OF COLOR HOMEOWNERSHIP RATE TO 50 PERCENT BY 2030

Source: “American Community Survey 1-Year Estimates,” Tables S2502, U.S Census Bureau, 2010-2019, figure generated on November 15, 2021. Note: Projections of the homeownership rate were calculated using a depreciation rate of 0.32 percent per year, the average percentage point change in the racial homeownership gap between 2009 and 2019. Projections adjusted for population growth.

2). By 2030 the gap would narrow by only 1 percentage point while households of color grow by 22 percent.13 Notably, New Jersey will be a majority-minority state by 2030—households of color will outnumber white households.14 These trends suggest that an increasingly racially diverse New Jersey will not significantly narrow the racial homeownership gap. To reduce the gap by 7 percentage points by 2030 and achieve a 50 percent homeownership rate among households of color, roughly 100,000 additional households of color—net of secular trends in population growth—would need to become homeowners (see Figure 3). In response to these wealth disparities, NJHMFA seeks to use DPA, the First-Time Homebuyer Mortgage Program, and the Residential Foreclosure Prevention Program to advance several critical goals: (1) promote wealth creation, (2) target neighborhoods for 8

stabilization, (3) support anti-gentrification efforts, and (4) narrow the state’s racial wealth gap. To make progress towards these goals, NJHMFA should use an extensive network of partners, including housing advocacy groups, nonprofits, and community-based organizations. These stakeholders are vital because they have familiarity and trust with communities that have encountered barriers to homeownership and wealth accumulation. The policy workshop’s assignment was to analyze how NJHMFA should structure and target these programs to achieve these goals. In doing so, we analyzed the Agency’s programs and data. We also met with other Housing Finance Agencies (HFAs), nonprofits, lenders, community land trusts, and stakeholders from across the country to learn from their programs, best practices, innovations, and challenges. In total, we

interviewed more than 30 stakeholders.These entities are named in the acknowledgement section at the end of this report. We are grateful to everyone who provided their time, talent, and expertise. The topics covered in our meetings included outreach, partnerships, and community engagements; DPA; foreclosure prevention; HFA strategies and processes; and new and innovative programs. NJHMFA already approaches many of these areas in ways similar to other housing stakeholders, and we developed recommendations on how the Agency can improve its programs and processes to achieve its goals more successfully. Our report will make, and discuss, recommendations in the following categories: 1) Outreach, Partnerships, and Community Collaboration, 2) Down Payment Assistance, 3) Foreclosure Prevention, 4) New Programs and Innovations, and 5) Agency Strategy and Process Improvement. Recommendations with significant anticipated costs include cost estimates. While the total cost of all recommendations included here would require a significant financial commitment, we mean to provide a comprehensive set of options for NJHMFA to review and prioritize. Throughout the report, we acknowledge and address how our recommendations would advance racial equity. Our recommendations also address both the “supply side” and “demand side” of affordable homeownership. For example, we propose homeowner rehabilitation assistance to increase the state’s supply of affordable homeownership opportunities. Meanwhile, our recommendations concerning outreach and community collaboration aim to increase demand for NJHMFA products among underrepresented groups.

TERMINOLOGY Throughout the report, we use “low income” to refer to households with incomes below 50 percent of the area median income and “moderate income” for households with incomes between 50 and 80 percent of the area median income.15 The term “first-time home buyer” generally refers to someone who has never owned a home. In this report, we use the term in accordance with NJHMFA’s definition of a first-time home buyer, which is someone who has not had an ownership interest in their primary residence during the previous three years.16 We use “first-generation home buyer” for first-time home buyers whose parents do not currently own a home. In other contexts, we use the term “first-generation” to refer to individuals belonging to a category (e.g., professional, graduate) to which their parents do not belong. The term “Latino” is used throughout this report to refer to persons of Mexican, Puerto Rican, Cuban, Central American, Dominican, Spanish, and other Hispanic descent; they may be of any race. The analyses and recommendations offered in this report are the collective efforts of the student policy workshop, and do not necessarily reflect the views of the New Jersey Housing and Mortgage Finance Agency. We intend for NJHMFA to apply our recommendations in a manner that is in full accordance with all relevant federal and state laws and regulations. The policy workshop is committed to the full compliance of all federal, state, and local fair housing laws, which makes it illegal to advertise any preference, limitation, or discrimination based on a protected characteristic. This report and our recommendations should not be construed to suggest that NJHMFA either directly or indirectly discriminate against any prospective purchaser or lessee on the basis of race, color, religion, sex, disability, familial status, national origin, or other protected characteristic.

9

1. OUTREACH, PARTNERSHIPS, AND COMMUNITY COLLABORATION

NJHMFA’s outreach, partnership, and collaboration strategies have many notable strengths. The Agency should continue to innovate in these areas to promote homeownership, stabilize neighborhoods, and shrink New Jersey’s racial wealth gap. These recommendations aim to increase knowledge of the Agency’s products among New Jersey communities that have encountered historical barriers to homeownership and wealth accumulation.17,18

provides an unwieldy webpage to parties seeking to connect with a lender institution.

Through community events, online webinars, traditional media coverage, social media, advertising, and a newly redesigned website, NJHMFA has taken steps to make its programs more accessible. Despite this progress, we find that the Agency’s outreach efforts generally do not harness targeted and tailored strategies to reach underserved communities proactively. This gap has been especially detrimental for borrowers who are Black and Asian, groups that make up 17.8 percent and 10.2 percent of the state’s population but only 9.9 percent and 1.3 percent of 2020 DPA recipients, respectively.19

NJHMFA partners with New Jersey’s diverse network of nonprofit housing and community development organizations. Given these organizations’ trust and familiarity with New Jersey’s underserved communities, the Agency should prioritize the new partnerships to better address the state’s racial homeownership gap.

The Agency’s outdated technology infrastructure and insufficient staffing currently impedes its efforts to reach prospective borrowers of color and firstgeneration home buyers. So do its outmoded data collection systems, the barriers between the Agency and consumers, and the private lenders who often poach potential clients.20 The Agency lacks accurate demographic information about borrowers from private lenders, inefficiently tracks contact information for partner organizations, and

10

Beyond technological and staffing shortfalls, the Agency’s current outreach strategy relies on the institutional knowledge and expertise of a few staff members who oversee community engagement. This model limits the Agency’s ability to scale outreach to new audiences, and it risks major disruptions when those staff members leave the Agency.

The Agency’s meaningful steps to partner with outside organizations have, at times, been frustrated by inconsistent communication with affordable housing stakeholders. Our conversations revealed that many housing organizations lack certainty about the Agency’s key policy priorities, vision for state’s affordable housing landscape, and baseline expectations for the role these organizations should play. And many organizations say they are reacting to the Agency’s new programs, rather than receiving an opportunity to shape them. This dynamic tends to damage trust and frustrate the Agency’s mission.

1.1. Employ a targeted home buyer strategy to prioritize outreach with underserved communities

IMPROVE STAFFING PRACTICES TO ENHANCE TRUST WITH HISTORICALLY MARGINALIZED COMMUNITIES

NJHMFA should expand its community outreach and marketing staff with at least two additional full-time employees to ensure greater diversity and bilingualism. We estimate this would cost $160,000 per year.21

SPOTLIGHT: NJHMFA’s Hospital Partnership Subsidy Program In May 2019, NJHMFA announced its $12 million Hospital Partnership Subsidy Program. Under this program, the Agency matches funds from hospitals to develop affordable rental housing for low- and moderate-income families and to set aside units with wrap-around services for individuals who frequently use hospital emergency department services.22,23 One of the program’s first projects involved a partnership between NJHMFA, St. Joseph’s University Medical Center, and two nonprofits, New Jersey Community Development Corporation and New Jersey Community Capital.24 The partnership led to the construction of a 70-unit building on a vacant lot nearby St. Joe’s.25 Foreclosure and Eviction Prevention and Housing Counseling Through its Foreclosure Mediation Assistance Program, the Agency partners with HUDcertified housing counseling organizations to provide free, one-on-one foreclosure prevention counseling services.26 In March 2020, the program expanded to include New Jersey renters due to a potential surge in evictions after the COVID-19 eviction moratoriums expired.27 The Agency’s network of housing counselors extends to each county in the state and is comprised of trusted nonprofits, including NJ Citizen Action, Housing Partnership, Tri-City Peoples Corporation, Epic Community Development Corporation, and Consumer Budget and Credit Counseling.28 The Agency also oversees subgrant partnerships with several HUD-certified nonprofits across the state to provide pre-purchase counseling services.29 Bulk Purchases of Non-Performing Loans The Residential Foreclosure Prevention Program establishes NJHMFA’s authority to create public–private partnerships with nonprofits and community organizations for bulk purchases of residential properties or mortgage notes after a mortgage foreclosure judgment.30 The program is meant to curtail foreclosures by helping underwater homeowners modify their mortgages and to prevent the buildup of vacant properties.31 Due to the program’s recency, the Agency has not yet made a bulk purchase partnership.

11

Currently, one person runs community engagement for the entire state. To break into new markets and build trust in new communities, NJHMFA should invest in more staff of diverse backgrounds.

TARGET DIRECT OUTREACH TO “QUICK WIN” POPULATIONS “Quick Win” populations are groups with established internal communications mechanisms, high concentrations of people of color, and the financial conditions to be first-time home buyers. Examples include first-generation professionals, state and local government employees, union members, teachers, university staff, and large private employers. NJHMFA should hold information sessions with these groups or coordinate with their human resource departments to distribute pamphlets or emails. This strategy acknowledges the high cost—and potentially low return—of direct-to-consumer outreach, and it aims to targeting specific groups with greater potential to have true interest in the program.

CREATE A PROMINENT MARKETING CAMPAIGN TARGETING PROSPECTIVE HOME BUYERS OF COLOR

Following practices from other states, including California32 and Colorado,33 engagement with the target communities and representative partner organizations should directly inform this marketing campaign. The Agency should seek feedback, identify gaps in understanding and barriers to access, and tailor messaging to each group’s unique concerns and needs. The campaign’s main web page should be displayed prominently on njhousing.gov to signal that NJHMFA is an active player in this space and understands systemic racism.

12

EMPLOY MESSAGING STRATEGIES TO COMBAT PERSISTENT MYTHS AND MISCONCEPTIONS AMONG MORTGAGE-READY MILLENNIALS

National data from the Urban Institute indicate that a substantial portion of millennials, including millennials of color, are “mortgage ready.” Nevertheless, 39 percent of these potential homeowners mistakenly believe that they must have a down payment of more than 20 percent to purchase, and the majority are unfamiliar with down payment assistance programs.34 To promote awareness of its DPA program and dispel myths about down payment requirements, the Agency should adopt a statewide social media strategy. We recommend that the Agency advertise on Facebook, YouTube, and Instagram, the three platforms that Americans between the ages of 30 and 49 use the most.35 The campaign should use diverse representation in images and photos. The social media assets NJHMFA already has can be adapted with new messaging.36 This is a long-term strategy to raise awareness of the program, and it is not expected to have significant returns on originating new loans. Since this is not intended to be the central strategy for marketing, we recommend that the Agency spend no more than $10,000 per year on social media advertisements. Because NJHMFA does not have a presence on Instagram, the Agency should partner with prominent accounts of real estate professionals, associations, lenders and others across the state. For example, while there is a relevant news hook the Agency should partner with @NJGov to advertise to its 58,000 followers on Instagram and 399,000 followers on Twitter.

FINANCIAL READINESS AND HOMEOWNERSHIP TRAINING

NJHMFA should partner with a trusted nonprofit or a research lab at a state university to develop and administer a race-conscious financial readiness and homeownership education curriculum. The program should be developed, piloted, and evaluated by a nonprofit partner with established credibility in communities of color. By using data to target educational efforts in areas with low NJHMFA program take-up rates and in communities of color, this initiative will enhance awareness of the Agency’s homeownership programs and affirmatively address the racial homeownership gap. Following the model of many HFAs subsidizing nonprofit providers of home buyer counseling, the Agency should provide $50 in financial support for each student. We recommend NJHFMA either budget or request new appropriation of at least $60,000 for the initial pilot to cover subsidies, curriculum adaptation, program management, and evaluation.37 In developing a course, the Agency might consider elements of Getting Your House in Order, the Portland Housing Center’s raceconscious financial readiness community education course developed by Dr. Rhea Combs.38,39 Its curriculum acknowledges the historical and cultural context of financial practices in the African American community. Those who completed the course went on to have more savings, less debt, and improved credit scores. And while 54 percent of the program’s participants reported that they did not feel in control of their finances before they participated in the program, only 10 percent of graduates reported feeling the same way a year out from completion.40 Portland Housing Center developed a similar curriculum for the Latino Spanish-speaking community. This case study demonstrates that tailored outreach and policy design can create pathways

to homeownership among traditionally underserved communities.

AUDITING NJHMFA’S COMMUNITY OUTREACH AND EVENTS CALENDAR

NJHMFA should audit its current calendar of outreach events to identify, and address, gaps in its regional distribution, and reach to communities of color. The Agency should consult trusted housing stakeholder organizations—such as the Affordable Housing Alliance, Morris Habitat for Humanity, Urban League of Essex County, and Garden State Episcopal Community Development Corporation—to identify community events that do not have an NJHMFA presence.

1.2. Expand lender and real estate professional relationships with strong ties to communities of color and leverage their outreach capacity Because most client referrals come from lenders and real estate professionals, NJHMFA should ensure that this pipeline supplies a diverse population of potential home buyers. The Agency should proactively diversify and strengthen its relationships with lenders and real estate professionals. Some of the affinity groups the Agency already works with may be invaluable in these efforts including the New Jersey Association of Minority Real Estate Professionals, the New Jersey Chapter of the National Association of Hispanic Real Estate Professionals, and the Northern New Jersey Chapter of the Asian Association of Real Estate Professionals.41 Many communities of color distrust traditional banks and many rely on mortgage 13

brokers or mission-driven institutions like credit unions. Similarly, home buyers of color increasingly use online, algorithm-based lending platforms, which are not allowed access to NJHMFA programs under the Agency’s preferred lender list.42

AUDIT CURRENT LENDER AND REAL ESTATE PROFESSIONAL OUTREACH

NJHMFA should audit its internal data to identify which lenders originate the most loans among borrowers of colors and identify the geographic areas they serve. Then, the Agency should use this information to identify gaps in service and develop concrete goals to prioritize targeted outreach to lenders who work with home buyers of color and firstgeneration home buyers. These metrics should shape every step of the outreach strategy. NJHMFA should also survey lenders every six months to identify the challenges they face in navigating the Agency’s processes. For example, surveys might identify efficiency challenges, such as underwriting turnaround times, that could then be addressed.

PARTNER WITH NEW AND DIVERSE HOUSING PROFESSIONALS

NJHMFA should solicit feedback from community partners (discussed more below) to identify which lenders, real estate professionals, and mortgage brokers its clients are using. The Agency should leverage these relationships to build connections with new housing professionals and identify and address barriers to NJHMFA products. Meanwhile, NJHMFA should establish preferred lender relationships with credit unions and online mortgage service providers. In doing so, the Agency may choose to amend its requirement that preferred lenders have physical presences in the state. Consumers who use online mortgage services are digitally savvy, but they may lack the personalized 14

support offered by banks and traditional lenders. As a result, they will seek information about the Agency online. Once the Agency establishes a partnership with a provider—for example, Rocket Mortgage —it should create a “NJ First Time Homebuyer with Rocket Mortgage” page on its website and provide step-by-step instructions. These referral processes can be streamlined by creating tailored landing pages on the Agency’s website with direct referral links. That is, Rocket Mortgage would ideally embed a link from its website to link directly to the NJHMFA website. NJHMFA should also collect and understand information on each lender’s internal commission policies. Some lenders, like Prosperity Home Mortgage, LLC base commissions on the loan amount and do not consider the type of loan product at all, making them ideal candidates to partner with NJHMFA.

EDUCATE HOUSING PROFESSIONALS ACROSS THE STATE

NJHMFA already offers training for lenders, but these training efforts should expand to include tailored breakouts and networking opportunities for all housing professionals at conferences and events. These trainings should focus on increasing awareness of the programs NJHMFA offers, but importantly, they should emphasize the message we heard repeatedly from top lenders: First time home buyers will eventually want to buy a second home, and they will remember the lenders that helped them get free money. At each of these events, the Agency should survey housing professionals to learn about their needs and identify opportunities for new lending relationships.

LEVERAGE CO-BRANDING OPPORTUNITIES WITH LENDERS

NJHMFA already offers social media toolkits for lenders to co-brand, but these opportunities should expand to other media, including television, radio, print, and direct mail. NJHMFA should select one lending partner to pilot a co-branded marketing campaign, which should include both direct mail and a social media campaign with tracking links to measure the impact of the strategy. The Agency should also expand co-branding opportunities to real estate professionals by providing social media templates and sample copy for posts to Facebook, Twitter, and Instagram.

1.3. Enhance community engagement and partnerships strategy to build trust with home buyers of color ESTABLISH AN ANNUAL CONFERENCE FOR COMMUNITY PARTNERS ON COLLABORATION AND RACIAL EQUITY

NJHMFA should launch an annual conference focused on nonprofit, community development, and advocacy stakeholders. The conference should serve as a platform for Agency leadership and stakeholders to identify shared goals in areas such as affordable housing repair and construction, foreclosure mitigation, and homeownership expansion. The Agency should organize panel discussions and plenary sessions to highlight new collaborations between the Agency and organizations, review lessons from previous partnerships, identify opportunities to scale existing partnerships so that they reach underserved communities, and discuss how

the Agency and housing professionals can collaborate to close the state’s racial gaps in wealth and homeownership. Two conferences—the Governor’s Conference on Housing and Economic Development, and the Housing and Community Development Network of New Jersey’s annual conference— already center on affordable housing and community development. NJHMFA’s conference would uniquely focus on racial equity, partnerships, and collaboration. It will also help the Agency and stakeholders ensure that their efforts complement, rather than compete against, each other, a concern cited by several organizations throughout our field research. During the conference, NJHMFA should solicit feedback on its existing policies and programs to inform its annual strategic plan, as described in Recommendation 5.1, and refine its vision for racially equitable homeownership opportunities in New Jersey. Because no single state agency or housing organization has the perfect strategy for resolving New Jersey’s complex racial disparities in homeownership, the Agency will need to combine different ideas offered by various organizations to develop the necessary comprehensive approach for tackling these deep-rooted inequities.43

ANNUAL CONFERENCE COSPONSOR PARTNERSHIPS

To reduce costs associated with the annual conference, NJHMFA should host the conference in its own office space and create cosponsor partnerships with trusted nonprofit, advocacy, and community development organizations. Potential partner organizations include Fair Share Housing Center; New Jersey Institute for Social Justice; the Housing and Community Development Network of New Jersey; and Affordable Housing Alliance, New Jersey Policy Perspectives. Cosponsors’ 15

office spaces may serve as alternate conference venue options. Such partnerships would help the Agency build trust and legitimacy with influential housing professionals in these sectors. We estimate that the cosponsorship would cost the Agency $30,000 per year.44

DESIGNATE A NONPROFIT, COMMUNITY DEVELOPMENT, AND ADVOCACY STAKEHOLDER LIAISON

NJHMFA should designate a full-time, inhouse liaison who oversees partnerships with nonprofit, community development, and advocacy stakeholders. The liaison should report directly to the Agency’s Executive Director and understand the state’s pervasive racial discrepancies in homeownership rates and wealth accumulation. In addition, the liaison should have substantial experience working in the nonprofit, advocacy, or community development sectors such that she is familiar and credible to stakeholders. The liaison’s salary should be comparable to other Agency leadership positions in order to draw experienced candidates with high levels of trust among New Jersey’s nonprofit and advocacy stakeholders. As part of her responsibilities, the liaison should convene regular listening sessions with trusted representatives from partner organizations to solicit feedback on the strengths and weaknesses of NJHMFA’s policies and partnership practices, especially those that disproportionately affect communities of color. Her findings should be incorporated into NJHMFA’s regular internal process improvements discussed in Section 5. Finally, the liaison should prioritize communication with stakeholders in North and Central Jersey to help NJHMFA cultivate more robust networks in these regions.

16

DRAFT FORMALIZED MOUs WITH COMMUNITY PARTNERS SERVING HOME BUYERS OF COLOR

Memoranda of understanding can formalize the process by which the Agency shares information with partners, refers nonmortgage-ready borrowers to partners, and receives referrals for candidates to NJHMFA programs from partners. These memoranda should be simple and not impose any new administrative burdens on NJHMFA staff.

17

2. DOWN PAYMENT ASSISTANCE The barriers to homeownership are many, but one reigns supreme—the down payment. A 2018 Zillow Housing Aspirations Survey conducted with the Urban Institute found that down payment is the leading barrier consumers cite in their path to homeownership.45 While the fate of the current Build Back Better bill remains uncertain at the time of this writing, it includes DPA to firstgeneration home buyers, a testament to the momentum behind the use of DPA to expand homeownership.46 Even modest assistance can increase the number of low-income and minority households able to purchase homes.47 Down payment subsidies increase the number of qualified mortgage loan applicants without increasing the overall size of the loan.48 Programs that take the form of grants, rather than loans, transfer equity to the homeowner if conditions of the grant are met. After the Great Recession, most state HFAs added some form of DPA product to their loan portfolio. While DPA loan specifications vary widely by HFA, DPA is a central HFA product. NJHMFA offers a DPA program that provides a flat $10,000 to qualified first-time home buyers. The assistance is an interest-free loan, forgivable after five years if the homeowner stays in the residence. The DPA must be paired with an NJHMFA first-time mortgage loan. The following are simple yet effective recommendations to enhance the DPA loan program. Throughout the course of this research, the team investigated many of the county- and city-level DPA opportunities throughout the state of New Jersey. There are many 18

different opportunities that require extensive research by the potential home buyer and bear significant bureaucratic hurdles, including lengthy application review timelines and cumbersome application processes. Due to the barriers and administrative challenges associated with accessing these resources, we do not recommend pursuing a formal strategy of layering DPA with these local resources. This may, however, remain a point of consideration for the future if NJHMFA chooses to allocate staff bandwidth to this coordination challenge.

2.1 Increase the base DPA amount to $14,000, and fix DPA to the maximum home purchase price NJHMFA should increase the base DPA from $10,000 to $14,000 so home buyers can be more competitive in purchasing homes across a broader range of New Jersey counties. The loans should scale alongside the maximum purchase price limits and maximum income limits already set by NJHMFA.

DPA DESIGN AND GEOGRAPHIC CONCENTRATION

Over 75 percent of DPA loans originate in Camden, Gloucester, Burlington, and Atlantic Counties, where median home values are among the lowest in the state. This is not surprising—$10,000 goes further, as a percentage of home value, in counties with lower housing costs. Homes in these counties do not appreciate at the same rate as other higher-value counties in

FIGURE 4. DPA LOANS BY MUNICIPALITY data underscore a sentiment from Reverend Eric Dobson, Deputy Director of the Fair Share PER 1,000 PEOPLE, 2016-2020 Housing Center: “All this program is going to do,” he said, referring to the DPA program, “is push more segregation. You have a program that pushes homeownership in places that are rural and don’t have jobs.”50

Housing values have appreciated substantially since 2019. They appreciated the most in Ocean, Essex, and Monmouth Counties, where just 2.5 percent of the Agency’s loans originate. These disparities continue a trend that characterized the last decade: Values in the four counties that account for 75 percent of the Agency’s portfolio have appreciated on average 26 percent since 2010, compared with statewide appreciation of 38 percent, placing all in the bottom half of New Jersey counties for home value appreciation.51

Source: This map depicts the number of NJHMFA DPA loans per 1,000 residents within each New Jersey municipality. Population figures are drawn from the American Community Survey 2014-2019 5-year estimates.

the state. In Camden, the county with the most DPA loans, homes depreciated by 3 percent from 2014 to 2019. Homes in Gloucester, Burlington, and Atlantic Counties depreciated by 1 percent. Meanwhile, homes statewide appreciated by an average of 4 percent, buoyed by counties in North and Central New Jersey.49 For NJHMFA to narrow the racial wealth gap, its products must be used in communities where homes appreciate in value. But today, its loans are concentrated in counties where homes do not appreciate as quickly as in the rest of the state—if they appreciate at all. These

The Agency should increase its DPA to allow recipients to buy homes in communities more likely to see appreciation. Because a flat $10,000 goes further in some counties than in others, first-time home buyers are more competitive buyers in neighborhoods with lower value homes and lower likelihood of home appreciation.

DPA PRODUCT INNOVATIONS

NJHMFA should increase DPA for a second reason. Today, the value of DPA is outweighed by the cost of private mortgage insurance (PMI). Consider a $311,979 home, the maximum qualifying value set by NJHMFA for a single-family unit in Mercer County. PMI for the first year alone amounts to $8,111.45, almost the entire DPA. After closing costs are considered, the DPA covers approximately 37 percent of the initial purchase costs. It is worth underlining that the current maximum price set for Mercer County by NJHMFA is roughly 20% less than the 2021 median price for Mercer County.52

19

FIGURE 5. RECOMMENDED DPA BY COUNTY Counties

NJHMFA 1-Family Maximum Home Purchase Price Limit

NJHMFA 50% Target for DPA

Proposed New DPA Amounts

Atlantic, Cumberland, Mercer

$311,979

$13,649

$14,000

Warren

$326,195

$14,271

$14,000

Burlington, Camden, Cape May, Gloucester, Salem

$377,540

$16,515

$16,500

Bergen, Essex, $719,953 Hudson, Hunterdon, Middlesex, Monmouth, Morris, Ocean, Passaic, Somerset, Sussex, Union

$31,499

$25,000

Source: NJHMFA 1-Family Maximum Home Purchase Prices have been developed from NJHMFA. The proposed new DPA amounts were calculated by the authors of the report.

Given the barrier that the down payment and other upfront costs pose for the home buyer, we recommend that the Agency increase the base DPA to $14,000 and further increase it according to the geography, similar to the current county-specific income and home price limits. In our analysis, we aimed to cover 50 percent of the upfront costs to the homeowner. These costs consist of an estimated 3.5 percent down payment, 3.5 percent closing costs, and a 1.75 percent PMI fee. Closing costs and PMI are rough estimates and will vary somewhat by buyer. We chose $14,000 as the new base DPA because it covers 50 percent of the upfront costs in Atlantic, Cumberland, Mercer, and Warren Counties. Our recommendation to scale the assistance aligns with practices at other HFAs. 20

With clear messaging, NJHMFA can avoid confusion around the different tiers. Following the example of MassHousing, NJHMFA may choose to advertise “down payment assistance of as much as $25,000.”53

COSTS AND FUNDING

We estimate that NJHMFA committed $13,650,000 to the DPA program in 2020. If our proposed DPA amounts had been offered to the same 1,365 home buyers that year, the program would have cost $21,050,000, an increase of $7.4 million. This does not account for geographic changes to NJHMFA’s portfolio that may result from the expanded funding.

IMPACT ON NEW JERSEY’S RACIAL HOMEOWNERSHIP GAP The impact on DPA changes to the racial

homeownership gap is contingent on how the DPA loans are allocated. By increasing the amount of DPA funds available to each home buyer, NJHMFA enables home buyers to compete in higher appreciating neighborhoods and to combat the lack of generational wealth that many home buyers of color face. To fully leverage this recommendation toward reducing New Jersey’s racial homeownership gap, this must be paired with the targeting goals suggested elsewhere in this report.

2.2 Leverage New Jersey Individual Development Accounts to increase available assistance to first-time home buyers Individual development accounts (IDAs) are matched savings accounts that help households save for specific goals like homeownership. One study has found that IDAs can increase the homeownership rate among participants by 11 percentage points.54 New Jersey home buyers are eligible for two IDAs: the Temporary Aid for Needy Families (TANF) IDA55 and the New Jersey HOME IDA.56 Both are implemented by the Department of Community Affairs. Program eligibility is provided in Figure 6.

Department of Community Affairs and other organizations to promote IDAs, as other HFAs already do, and bundle them with DPA. For example, the Indiana HFA markets IDAs on its website and provides a list of administrators to supplement its support for first-time home buyers.57 The New York HFA previously provided an IDA program a different agency now administers.58,59 The NJHFMA should, at the least, promote the New Jersey HOME IDA as a supplemental option to DPA, given the programs’ similar eligibility criteria. This would provide firsttime home buyers with $7,000 in additional assistance. When bundling both programs, the Agency should allow its trainings to satisfy the homeownership education requirements of IDAs so that buyers can more easily participate in both programs. There is growing interest in IDAs as New Jersey recently passed a law in January 2020 to expand the benefits and eligibility requirements for the TANF IDA.60

IMPACT ON NEW JERSEY’S RACIAL HOMEOWNERSHIP GAP

Increasing the money available to home buyers of color for upfront homeownership costs increases the affordability of homeownership. This would increase the number of homeowners of color and narrow the racial homeownership gap.

NJHMFA should coordinate with the Department of Community Affairs to harmonize DPA and IDA programs for firsttime home buyers who qualify for both programs. In addition to the Agency’s DPA, for those who qualify for both IDAs, these programs could provide first-time home buyers up to $13,000 to cover a down payment, closing costs, and mortgage insurance.

OPPORTUNITIES FOR COORDINATION NJHFMA should coordinate with the

21

FIGURE 6. SUMMARY OF NEW JERSEY INDIVIDUAL DEVELOPMENT ACCOUNTS New Jersey HOME Individual Development Account

TANF Individual Development Account

Funding Entity

State

Federal

Matching Ratio

2:1

2:1

Maximum Contribution

$3,500

$3,000

Maximum Matching

$7,000

$6,000

Maximum years of account

2 years (5 with extension)

3 years (5 with extension)

Maximum contribution per year

$1,750

$1,000

Minimum length for fund withdrawal

6 months

6 months

Income Eligibility61

120% of County AMI First-time home buyer

250% of Federal Poverty Level

Examples of Qualifying Expenses

Down payment, settlement fees, financing or closing costs, title insurance, attorney fees, inspection fees, acquisition costs, construction or reconstruction, appraisal fees, mortgage insurance (as part of closing costs) and other customary prepaid expenses.

•First-home purchase (same as HOME IDA) •Education and job training •Small business support

Training Requirements

•10 hours of financial literacy •10 hours of basic financial •10 hours of homeownership literacy counseling •10 hours of homeownership counseling

Source: “The New Jersey Federal Individual Development Account Program, TANF IDA Program Manual,” New Jersey Department of Community Affairs; “The New Jersey Home Individual Development Account, HOME IDA Program Manual,” New Jersey Department of Community Affairs; New Jersey P.L. 2019, c. 460.

22

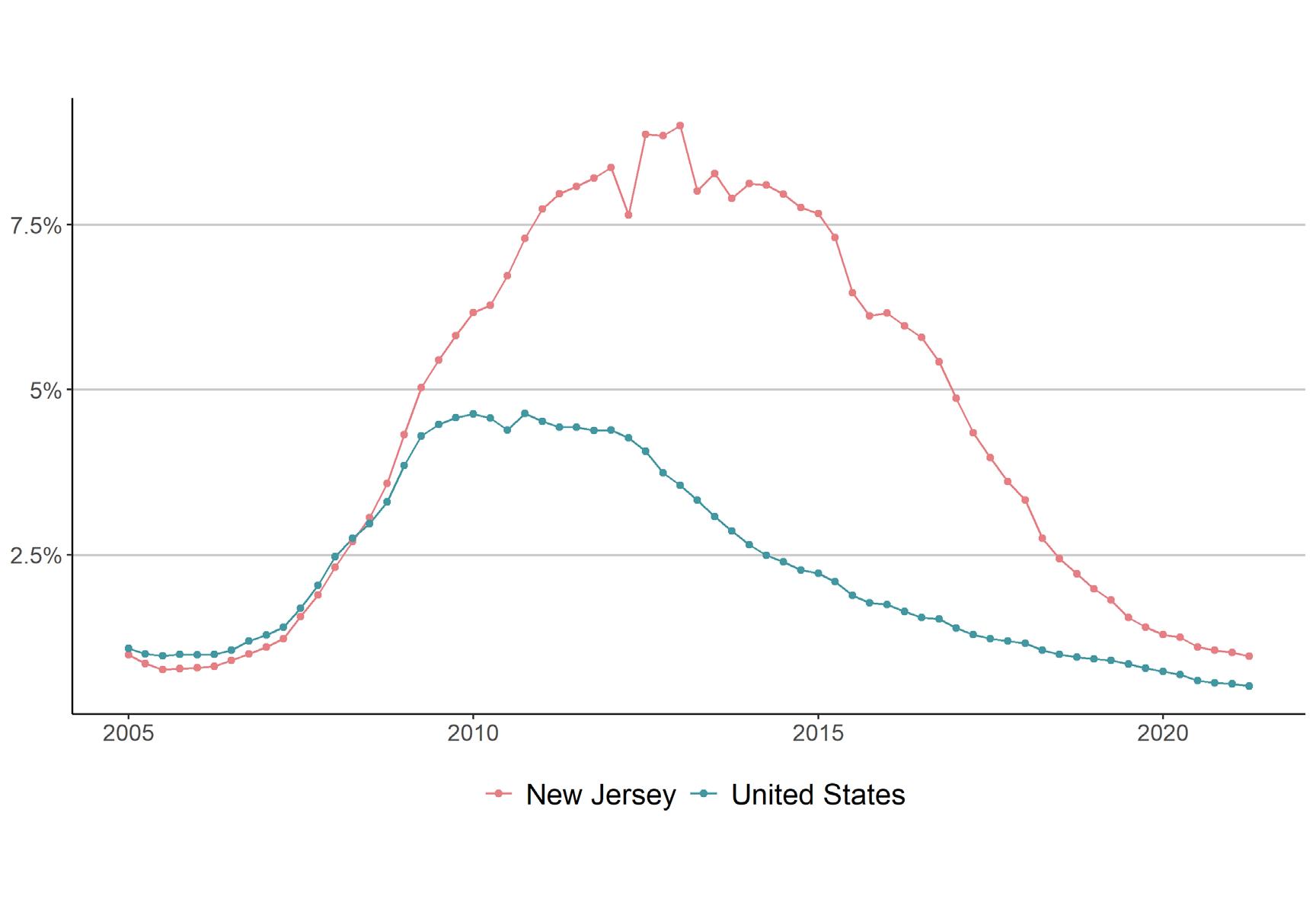

3. FORECLOSURE PREVENTION The Great Recession exacted an enormous, lasting toll on New Jersey homeowners. Foreclosures spiked, and they would not return to their pre-recession levels until more than a decade later in 2019.62 That year—as with every year since 2015—New Jersey’s foreclosure rate was the highest in the nation.63 And during 2020, as the COVID-19 pandemic caused unemployment to spike from 3 percent to as high as 16 percent, 64 the number of New Jersey households that deferred their mortgage payments exceeded 160,000 for five consecutive months.65 These trends motivated the passage of the Foreclosure Prevention Act.66 The Act authorizes NJHMFA to buy foreclosed properties and defaulted mortgages in bulk from mortgage lenders, investors, and loan

servicers.67 Most notably, Fannie Mae and Freddie Mac have “non-performing loan sale” programs in which they auction off pools of loans to private investors, non-profits, and governments.68 The Federal Housing Administration conducts a similar singlefamily loan sale program.69 Investors in these loan sale programs must meet specific requirements for servicing the loans and reporting on outcomes.70 The Agency should contract with community development finance institutions (“CFDI”) to purchase and service these loans. And where possible, it should seek to turn around vacant or foreclosed properties in urban areas, where the harm of foreclosure to surrounding homes is the greatest.

FIGURE 7. NEW JERSEY AND U.S. FORECLOSURE RATES BY QUARTER, 20052020

Source: Mortgage Bankers Association, 2021

23

3.1 Contract with one or more qualified CDFIs to purchase and service non-performing loans The loan purchase initiative and other activities under the Act will be funded through a $350 fee on sheriff’s sales collected in a Foreclosure Intervention Fund. NJHMFA projects sheriff sales revenues of around $6 million per year, and it will reserve 80 percent—or $4.8 million—for the bulk purchase of loans.71 The projection assumes that New Jersey’s baseline foreclosure activity going forward would be around 17,000 sheriff’s sales per year.

were mostly vacant—New York hoped to convert them to affordable housing. They were spread across 54 cities.74 And their partnership allowed for the participation of private investors in order to raise capital. Similarly, in 2017, SONYMA and NJCC partnered to purchase nearly 400 non-performing loans throughout New York state.75 Ultimately, they succeeded in leveraging SONYMA’s resources to acquire more loans.

The projected revenue would allow the Agency to purchase about 25 homes, and this estimate may be optimistic. If foreclosures return to their 2019 level—there were about 14,300 notices of foreclosure sales that year72—the revenue from sheriff’s sales would be $5 million, leaving only $4 million to purchase loans.

Our understanding is that NJHMFA plans to acquire mostly vacant homes at first, but that the full details of the Residential Foreclosure Prevention Program have not been finalized. Should the Agency begin acquiring occupied homes, it should work with the homeowner to reach the most favorable outcome. Generally, homeowners in default will see one of three outcomes. The homeowners might still face foreclosure, avoid foreclosure and keep the home, or avoid foreclosure but give up the home anyway—they might sell it in a short sale or provide the deed in lieu of foreclosure.76 On average, loans acquired through nonperforming or single family loan sales avoid foreclosure 30–40 percent of the time.77

CDFIs CAN HELP NJHMFA LEVERAGE ITS LIMITED RESOURCES

CDFIs HAVE EXPERIENCE WITH FORECLOSURE PREVENTION

The Agency should leverage its limited resources by contracting with a CDFI. The Act allows the Agency to contract with CDFIs that have at least $50 million in assets and two years of experience in financing affordable housing. One such institution is New Jersey Community Capital (“NJCC”), whose partnership with the State of New York Mortgage Agency (“SONYMA”) in April 2021 provides an instructive model. In April 2021, New York and NJCC partnered to purchase 70 loans from the U.S. Department of Housing and Urban Development, all located within the state of New York.73 The properties

24

CDFIs have a track record of success in helping homeowners avoid foreclosure. For example, as part of its ReStart program, NJCC partners with various private and nonprofit investors to pool resources for bidding on non-performing loans. Because of the different stakeholders involved, NJCC has specific requirements for participating in the investment partnership. Any properties foreclosed and sold must be made available first to owner-occupants, then to nonprofits and community land trusts, and only then to private investors.78 Further, NJCC has developed protocols for loan servicing, housing counseling, underwriting loan modifications, and reporting requirements

on progress and outcomes. NJCC has helped over 2,400 households avoid foreclosure since 2012.79 NJHMFA should partner with one or more CDFIs to acquire non-performing loans, service loans with the goal of helping borrowers avoid foreclosure, and manage foreclosed properties to be sold to new owneroccupants or be converted to affordable housing. By contracting with CDFIs, the Agency can leverage its limited program revenues to bring the program to scale. Further, some CDFIs have considerable experience in housing finance, bulk purchases of loans, and managing affordable housing. Finally, CDFIs are aligned with the Agency’s overall mission of helping low-income communities gain access to affordable housing.

3.2 Target urban areas for bulk purchases of defaulted mortgages Robust economic literature supports the existence of a foreclosure “contagion effect”: When a home is foreclosed, the values of neighboring homes fall.80,81 This downward price pressure can, in turn, put the owners of those homes at greater risk of foreclosure.82 The contagion effect is incredibly localized, affecting only those properties within 500 feet of the foreclosed home.83 Nevertheless, the size of the contagion effect is large. A single foreclosure reduces the value of nearby homes by about 1 percent84 and, on average, every 100 foreclosures will result in 30 to 60 more.85 Economists say these findings support the use of public funds to reduce the harm caused by foreclosures to neighboring properties.86 Because the foreclosure contagion effect is limited to properties within 500 feet of the

foreclosed property, foreclosures in urban areasf—where the density of surrounding homes is greatest—cause the greatest harm to their neighborhoods. Furthermore, each additional foreclosure within 500 feet of a property further reduces the property’s value and increases its own risk of foreclosure. Therefore, households within 500 feet of multiple foreclosed properties experience greater harm than households near a single foreclosed property. For these reasons, NJHMFA should concentrate its limited Foreclosure Intervention Fund revenues in urban neighborhoods with elevated foreclosure risk. To the extent that the Agency acquires its properties through bulk purchases, it will not have the luxury of creating, and consistently applying, criteria to guide it to identify homes whose neighborhoods would benefit the most from NJHMFA intervention. Instead, the Agency should use this knowledge as guiding principle. When choosing which properties, or pools of properties, to purchase, it should prefer the properties with the greatest number of other homes in a 500-foot radius. Matching these homes with new owners will help to stabilize their immediate neighborhoods. Finally, to the extent that NJHMFA acquires vacant homes, it should rehabilitate and resell them to new owners as quickly as possible. The longer a home sits vacant, the longer it depresses the value of surrounding properties. By moving to sell and have vacant homes be occupied quickly, NJHMFA will stabilize the surrounding neighborhood.

NJHMFA MAY NEED TO NEGOTIATE DIRECT PURCHASES OF TARGETED LOAN POOL

Our recommendations depend, in part, on the Agency having some level of discretion to acquire properties in urban areas. The “bulk”

25

nature of bulk purchases presents a challenge to this intentionality. Investors typically purchase non-performing loans through auctions held by Fannie Mae, Freddie Mac, or the Federal Housing Administration. The seller agencies pool together loans provided by their loan servicers, so investors do not generally choose which loans go into a pool or where the properties are located. Even pools designed with community impact in mind can have loans based across multiple states.87 There is precedent for nonprofits and governments negotiating with sellers to purchase a set of non-performing loans. For example, NJCC purchased underwater mortgages along the New Jersey coast after Superstorm Sandy. Unfortunately, this may come at a cost: NJCC paid a premium above the likely auction price.88 Depending on NJHMFA’s revenues, repeated direct purchases of loans may not be the most efficient or sustainable use of funds. By contrast, NJCC’s partnership with New York State resulted in a direct purchase of loans that were heavily discounted: $4.26 million sale price on a pool with $10.7 million in unpaid principal balance. 89 NJHMFA should work with sellers of nonperforming loans to negotiate targeted, direct purchases of non-performing loan pools. This will be made more feasible through contracting with CDFIs, as the Agency can leverage a broader pool of funds for purchasing loans. The Agency could also initially negotiate loan pools containing a higher proportion of vacant properties, which would cost less, as the Agency builds the program’s portfolio.

IMPACT ON NEW JERSEY’S RACIAL HOMEOWNERSHIP GAP

Contracting with CDFIs and targeting purchases of non-performing loans would allow NJHMFA to prevent a greater number of foreclosures. Preventing more foreclosures in a targeted manner would, at the least, help prevent the 26

racial homeownership gap from widening further. While vacant or foreclosed properties could be channeled into affordable housing opportunities, this would likely have little net impact on the homeownership gap over the long term given the Agency’s current budget for the program.

4. NEW PROGRAMS AND INNOVATIONS

The First-Time Homebuyer and Down Payment Assistance products promote affordable and stable homeownership in New Jersey. But not all communities have benefited from these products. We propose several new programs or adjustments to current programs to address this concern. Our proposed programs aim to reach the following groups: first-time home buyers who cannot afford a market-rate turnkey home, lower-income families at risk of losing their home due to substandard living conditions, first-generation professionals who are currently unable to access mortgage assistance, and potential landlords of color who would benefit from financial support and counseling. With the right supports in place, NJHMFA could expand homeownership opportunities among these populations and help narrow the state’s racial homeownership gap.

4.1. Establish a statewide Homeowner Rehabilitation Assistance (HRA) program NJHMFA should establish a homeowner rehabilitation assistance (HRA) program to rehabilitate homes for low- and moderateincome families. The program will complement HRA programs already offered by many New Jersey municipalities and counties. The Agency should direct part of its assistance to first-time home buyers, especially in areas with concentrated vacant, aged, or

substandard homes. It should also direct some funds to current homeowners in areas at risk of gentrification and in blighted neighborhoods. For the purposes of this recommendation, “gentrification” refers to the involuntary displacement of households in areas where housing costs are rapidly increasing. “Blight” refers to derelict or visibly substandard homes that depress surrounding property values.

A SURVEY OF HRAs

HRA programs provide financial assistance to low- and moderate-income homeowners for critical home rehabilitation, repair, or renovation needs. They can be categorized into two broad models. In the first model, a government offers loans or grants to current homeowner-occupants loans to improve their homes. The vast majority of state and local HRA programs operate this way. The second model reaches new home buyers. Under this model, a government will offer loans or grants to first-time home buyers to help cover the cost of rehabilitating a newlypurchased, substandard home. Few HRA programs currently operate on the purchase side. HRA programs improve both health and housing outcomes for those living in rehabilitated households. The health benefits include improved respiratory health and a reduction in exposure to lead paint, mold, pests, fire hazards, and other safety risks.90 Furthermore, renovation has been shown to appreciate home values in the surrounding area.91

27

HRA programs are also cost-effective. For example, Detroit’s small home repair grants— with a median grant of just $6,000—enabled homeowners to address one of every two major repair needs. In a survey, all participants said the program was important for their ability to stay in their home, and one-quarter said that, without the program, they would have left their home permanently.92

THE HRA LANDSCAPE IN NEW JERSEY

New Jersey has a patchwork of HRA programs administered by counties and municipalities. These programs are designed to meet the municipalities’ obligations under the Mount Laurel Doctrine, which requires that every municipality provide its fair share of affordable housing for people of low and moderate incomes.93 The programs are funded by local housing trust funds and by federal grants administered via HOME and the Community Development Block Grant Program. Few data exist on the extent to which rehabilitation under the Mount Laurel Doctrine meets the needs of New Jersey households. At the start of Mount Laurel’s “Third Round” in 2015, there existed at least 36,000 Present Need units requiring rehabilitation spread across over 200 municipalities.94 Meanwhile, the rate at which these homes are being repaired under county and municipal programs is inadequate. An administrator of a housing rehabilitation program informed us that three of the state’s largest HRA administrators each rehabilitate only several hundred homes annually.

TOWARD A STATEWIDE HRA PROGRAM

A statewide HRA program is critical for the expansion New Jersey’s stock of affordable, livable occupant-owned housing units. Today, low- and moderate-income households occupy tens of thousands of deficient units. And around 1.5 percent of units in the state are

28

vacant, many of which may not be habitable without rehabilitation.95 Without a comprehensive statewide HRA program, New Jersey is unlikely to meet its full housing rehabilitation needs. Existing home improvement programs at the municipal and county level are scattered, inconsistent, and not universally available. Meanwhile, many aging homes in the state will likely become deficient absent intervention. A state HRA program will promote streamlined, equitable access to rehabilitation assistance and allow NJHMFA to send rehabilitation funds to those areas with the greatest need. A statewide HRA program should not, however, replace local programs, which are legally mandated under Mount Laurel. Instead, eligible households should be able to combine state and local HRA loans.

TWO HALVES OF A STATEWIDE PROGRAM

NJHMFA’s HRA program should maintain two separate funds: one for existing low-tomoderate income homeowners and another for first-time low-to-moderate income home buyers. Both models have benefits, and each should be part of a comprehensive approach to expanding affordable, stable homeownership opportunities. The Agency should reserve at least half of state HRA loans for first-time home buyers. Today, only existing homeowners are eligible for county and municipal HRA programs. By reserving half of HRA loans for first-time buyers, the Agency will expand the stock of livable homes available to low- and moderateincome families, allowing these households to begin building wealth through home equity. NJHMFA should focus these loans in areas with the most vacant, aged, or substandard

housing units. Figure 8 shows New Jersey’s residential vacancy rate by county. Eight of the 10 counties with the highest residential vacancy rate are in southern New Jersey. Figure 9 shows the median age of housing units by county. Homes are oldest in the counties surrounding New Jersey’s oldest urban areas—Newark, Jersey City, Elizabeth, Paterson, Trenton, and Camden. HRA for first-time home buyers could expand the stock of livable homes in both New Jersey’s rural southern counties and its older urban areas.

The remainder of state HRA loans should assist existing homeowners, with the goal of preventing the displacement of households whose homes currently provide substandard or unsafe living conditions. The Agency should target these loans in areas where families are at risk of displacement due to rising housing costs or housing blight. In areas with rising housing costs, homeowners with distressed mortgages can use these funds to avoid foreclosure. Meanwhile, in areas with significant housing blight,

FIGURE 8. HOME VACANCY RATE BY COUNTY, 2019

FIGURE 9. MEDIAN HOME AGE BY COUNTY, 2019

Source: Craig McCarthy. “Here’s How Many Vacant Homes There Are in Each NJ County.” nj.com, January 16, 2019.

Source: 2019 American Community Survey 1-Year Estimate

29

rehabilitation assistance will not only help individual homeowners improve their home, but also buoy the value of other homes in the neighborhood. In either case, NJHMFA’s HRA program would work to promote neighborhood stability, and therefore support anti-gentrification efforts. Newark, Jersey City, Elizabeth, Paterson, Trenton, and Camden have been among the fastest-growing New Jersey municipalities over the past decade, indicating a potential for gentrification.96 Targeting homeowners in these counties for rehabilitation assistance is likely to go the furthest toward mitigating gentrification and blight. To target HRA loans to the desired communities and x, NJHMFA should follow the outreach and community collaboration guidelines outlined in Section 1. HRA loans to existing homeowners would also dovetail with NJHMFA’s foreclosure prevention efforts. For example, the Agency should offer HRA loans to first-time buyers and existing owners of properties acquired under the Foreclosure Prevention Program. NJHMFA should also use its HRA program to promote climate resilience for the state’s housing stock. Today, local housing rehabilitation programs across the state primarily cover health- and safety-related repairs. But repairs related to climate resilience are just as important in protecting future New Jersey families and their homes. By 2050, over 600,000 New Jersey properties are projected to have significant flood risk, due to both sea level rise and severe storms and hurricanes.97 Weatherization- and climate resilience-related repairs—including compliance with flood-resistance standards— should therefore be equally eligible for HRA loans as health- and safety-related repairs.

30

NJHMFA should leverage third-party HRA program administrators. Administering an HRA program is complicated and requires niche expertise. It requires the preparation of bid documents, comprehensive inspections, contractor review and outreach, applicant outreach and approval, unit certification, and legal documentation. Fortunately, several major private sector rehabilitation program administrators already operate in New Jersey. These include CGP&H, Rehabco, and Community Action Services, among others. Especially in the years leading up to and immediately after the launch of a statewide HRA program, NJHMFA should work with one or multiple such administrators to ease the program’s cost and personnel burden.

STRUCTURE OF HRA LOANS

The structure of HRA loans will be a critical decision point for NJHMFA. The Agency can either allow repayment to be deferred until the home is sold, or it can require regular interest payments similar to a conventional loan. Interest on the loan can be at market rate, below market rate, or zero. Most important, it may choose to forgive HRA loans after a certain number of years of occupancy. Forgivable loans are most beneficial to lowand moderate-income homeowners and home buyers. HRA loans should ideally be structured like DPA loans: zero-interest, no monthly payment, and forgivable after five years of occupancy. But non-forgivable, interest-free loans that defer repayment until resale offer a less costly alternative. These loans are still valuable in that they provide home buyers the upfront financing to move into and repair a home and begin to build wealth through home equity. If funds are insufficient to provide fullyforgivable HRA loans to both current

homeowners and first-time buyers, NJHMFA should prioritize forgivability for existing homeowners. Today, most low- and moderate-income first-time home buyers in New Jersey qualify for fully-forgivable DPA loans. But existing homeowners typically cannot access forgivable loans to rehabilitate their homes. By offering forgivable loans to existing homeowners, NJHMFA would even the playing field, thereby combatting displacement and gentrification.

COSTS AND FUNDING

NJHMFA should aim to scale its HRA program to a similar size as its DPA program: at least 1,000 unique loans per year. Based on our conversations with private sector HRA program administrators, we estimate that the average home rehabilitation project carries around $20,000, plus at least $4,000 in administrative costs. Considering the inflationary cost of materials and labor, we recommend that NJHMFA provide loans of up to $30,000. If NJHMFA were to provide 1,000 forgivable HRA loans of $30,000, the program would carry an annual cost of $30 million, plus administrative costs. We believe this is a cost-effective way to create or preserve 1,000 homeownership opportunities. When seeking funding from the State Legislature, NJHMFA should emphasize that HRA will create homeownership opportunities for low- and moderate-income households and expand the state’s stock of livable housing. If NJHMFA cannot obtain a full $30 million annual appropriation from the State Legislature, the Agency has a few options to reduce the cost of its HRA program. First, the program could be scaled down in terms of annual number of HRA loans. Second, the program could have a loan maximum of less than $30,000. Finally, the program could offer

interest-free, deferred payment loans instead of forgivable loans. As described above, if only some of the HRA program’s loans are to be fully forgivable, they should be prioritized toward existing homeowners.

IMPACT ON NEW JERSEY’S RACIAL HOMEOWNERSHIP GAP

While the state HRA program would not explicitly target households by race, we believe it would particularly benefit Black and Latino families, who are disproportionately low- and moderate-income. As described above, we recommend targeting many of the program’s loans toward areas at risk of gentrification, with widespread housing blight, or with an aged housing stock. These tend to be New Jersey’s older urban areas, which also have the state’s highest concentration of people of color.98 To ensure households of color can take advantage of the state’s HRA program, we recommend employing the outreach, partnership, and community collaboration strategies outlined in Section 1.

4.2. Target firstgeneration professionals Many factors contribute to the Black–white wealth gap, including policies and practices that have deprived Black Americans of equal access to higher education and homeownership. Today, Black Americans who attain a college degree carry an outsized share of student loan debt and earn a lower rate of return on their degrees compared to white graduates. For Black borrowers, many of whom are first-generation college graduates or professionals, student loan debt is a barrier to homeownership. Current mortgage underwriting practices unfairly penalize borrowers with high student loan debt burdens.

31

NJHMFA should partner with Rutgers Law School (RLS) to provide home buyer education to law students who are first-generation prospective home buyers and establish a pilot program to offset certain mortgage-related costs for RLS graduates.

NATIONAL IMPACTS OF STUDENT LOAN DEBTS ON BLACK COMMUNITIES Nationally, 37 percent of white adults have bachelor’s degrees, compared to just 22 percent of Black adults. Meanwhile, 13 percent of white adults and 8 percent of Black adults have graduate degrees.99 These disparities are partly explained by racial disparities in college graduation rates: 64 percent of white students graduate, compared to just 40 percent of Black students.100

Black students who do graduate see a lower return on their degrees than white graduates. For every dollar in wealth that the median Black household with a college degree accrues, the median white household accrues $11.49.101 This disparity explains, at least in part, why homeownership is less common among Black college graduates than for white high school dropouts.102 At graduation, Black students—who often lack access to family wealth—owe $7,400 more on average in student loans than do their white peers. Just four years later, that gap triples

to $25,000 due to interest accumulation.103 Typically, white borrowers reduce their student loan debt by 94 percent over 20 years. Black borrowers reduce their debt by just 5 percent in the same period, and half default. Although higher education is normally associated with wealth, an average collegeeducated Black family has just two-thirds of the wealth of an average white family headed by someone with less than a high school degree.104

IMPACTS OF STUDENT LOAN DEBT ON BLACK COMMUNITIES IN NEW JERSEY

New Jersey has the fifth highest student debt burden among the states. Two in three recent college graduates in the state have debt, and the average debt burden is $34,000. Since the Great Recession, funding per student at public universities in New Jersey has declined by 23 percent, shifting the cost of education to students. The average annual cost of public college in New Jersey is now $26,000, the third highest in the nation.

For Black and Latino students, these costs can be enormous. In 2017, the cost of public college to Black and Latino students in New Jersey was equivalent to 32 and 29 percent of their median household income, respectively.105 White families, meanwhile, needed only 17 percent of their household income to cover the cost of college. Student loans are therefore

FIGURE 10. STUDENT LOAN DEFAULT RATE BY COUNTY AND RACE Essex County Borrowers of Color

21%

White Borrowers 4%

Camden County

Mercer County

Atlantic County

24%

22%

28%

8%

4%

10%

Source: New Jersey Institute for Social Justice 2020 report - “Freed From Debt: A Racial Justice Approach to Student Loan Reform in New Jersey”

32

the only choice for many Black and brown students.106 And in the counties that surround New Jersey’s urban centers, default rates in communities of color are devastating.107 To mitigate the racial wealth gap among college graduates, NJHMFA should target students and graduates of color for its FirstTime Homebuyer Program. First-generation professionals and home buyers are typically trailblazers within their family. They may lack access to generational wealth and can, therefore, benefit greatly from NJHMFA’s guidance on homeownership.

BARRIERS TO HOMEOWNERSHIP AMONG RECENT PROFESSIONAL GRADUATES

To qualify for a conventional mortgage, borrowers must put 20 percent down and pay closing costs.108 Federal Housing Administration (FHA) loans allow borrowers to put as little as 3.5 percent down. To offset the risk of foreclosure, FHA loans require the borrower to carry PMI.109 This PMI is paid to FHA at an upfront rate of 1.75 percent, and at an annual rate of 0.45–1.05 percent, of the purchase price of the home.110 Lenders typically assess an applicant’s monthly debtto-income ratio. The greatest ratio allowed under NJHMFA’s First-Time Homebuyer Program is 45 percent.111 Many recent law school graduates have little savings, making a conventional mortgage unattainable. Because of their student debt, they also struggle to qualify for FHA mortgages despite job stability and modest income-based student loan payment obligations. Black lawyers are especially likely to find themselves unable to qualify for a mortgage—they graduate with nearly double the debt of their white counterparts.112 Federal student loans offer plans that cap monthly payments at 10 percent of an applicant’s discretionary income.113 Despite

this, historically FHA had for years required lenders to consider 1 percent of an applicant’s loan balance as their monthly debt. This policy harmed applicants with high student debt burdens by artificially inflating their debtto-income ratio.114 In 2021 FHA relaxed its terms by allowing lenders to use 0.5 percent of the total balance, or the actual student loan payment, when calculating debt-to-income ratio.115 But the requirement remains a hurdle. For some graduates, 0.5 percent of the total balance could still be higher than their actual income-based repayment. And the requirement fails to account for public sector loan forgiveness for which those who work in the public sector may qualify.

ESTABLISH A PROFESSIONAL MORTGAGE PILOT PROGRAM FOR FIRST-GENERATION HOME BUYER GRADUATES OF RUTGERS LAW SCHOOL

Recognizing that professionals pose a relatively low risk as borrowers, some lenders—like Cadence Bank, which does not operate in New Jersey—have created special mortgage products for select professionals, including attorneys, doctors, and dentists. These products offer up to $1.5 million, with no PMI requirements.116 The removal of PMI allows borrowers to enjoy lower closing costs and monthly payments. NJHMFA should fill the need for these products within New Jersey and establish a pilot program awarding grants to cover PMI for RLS graduates who use its First-Time Homebuyer Program. In year one of the pilot, NJHMFA should award such grants to 200 borrowers. After two years, the Agency should expand the pilot to include Rutgers School of Dental Medicine and Rutgers New Jersey Medical School. After three years, NJHMFA should assess risk of current grantees and, if 33

favorable, make it a permanent program. We are not aware of similar programs offered by HFAs, meaning the Agency has an opportunity to innovate. The program could have enormous benefits for professionals. In 2020 alone, New Jersey home values increased by 19 percent,117 creating enough equity for the average homeowner

to eliminate educational debt several times over. But the significant cost of PMI—nearly 10 percent of the home’s value over the first ten years of ownership—can wipe out much of these equity gains and dissuade recent graduates from becoming homeowners when they are already burdened with debt.

FIGURE 11. ILLUSTRATIVE PMI COSTS OVER TIME Atlantic County

Camden County

Essex County

Max Single Family Home Price

$311,979

$377,540