3.

4.

5

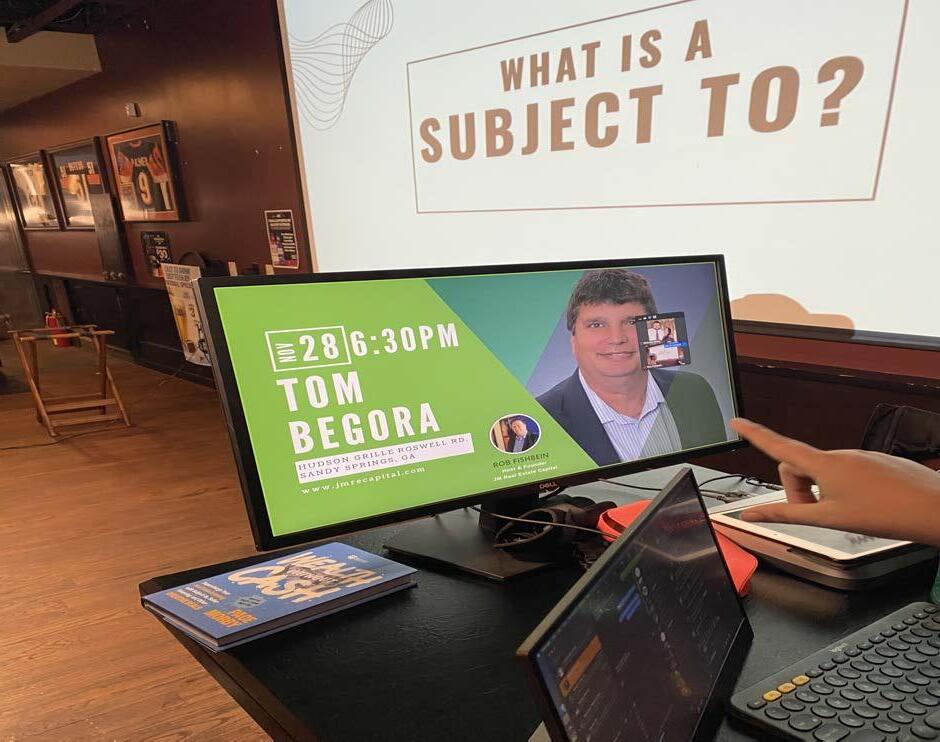

RE Journal Member Spotlight

Tom Begora

Tom Begora was born in Hammond, Indiana and grew up in the south suburbs of Chicago, Illinois. He went to Olivet Nazarene University in Kankakee and got his first job at AT&T in 1991. He ended up in Georgia at the age of 25 during a trip from Wisconsin to vacation in Fort Myers, Florida. He is an active member of the North Metro REIA in Marietta, GA.

Please tell us a little about who you are and what you did before getting into real estate investing.

Before getting into real estate investing, I worked for AT&T, owned a car lot, worked for UPS, was a property manager, and worked part— time in real estate. However, on our way to a vacation in Fort Meyers, Florida, my wife at the time and I stopped halfway in Acworth for the

Continued on Page 8

By Jason K. Powers

By Jason K. Powers

In the United States, a pervasive trend over decades has had individuals relinquishing control over their financial destinies in numerous ways, often without even realizing it. From depositing earnings into traditional banking institutions that offer minimal interest rates, to entrusting retirement savings to volatile market-driven plans, to unbridled amounts of debt accumulation, Americans are consistently ceding their financial autonomy. This systemic surrender not only hampers one’s ability to advance financially today but also significantly restricts the capacity to build for tomorrow and leave a lasting legacy for future generations.

The consequences of relinquishing financial control are far-reaching, affecting not just the individual but also the broader economic landscape in which they operate. By depending on external entities for financial growth and security, individuals miss out on opportunities to leverage their assets in ways that could yield far greater returns. This dependen-

Control the Banking Function: A Game-Changer for Investors How Inclusion Affects Your Rentals

cy on traditional financial systems and their associated instruments limits the ability to respond to financial challenges and capitalize on investment opportunities in alternative ways. Moreover, relinquishing financial control of one’s money constrains the capacity to create a sustainable generational wealth transfer, diminishing the potential to have an

impact on future generations.

“Regaining control over personal finances is not just about enhancing one’s wealth today; it’s about reshaping the financial future for oneself and those who follow.”

In this dynamic landscape of personal finance, the Infinite Banking Concept

Continued on Page 15

By David Pickron

If you’ve ever purchased a gift for someone, you’re familiar with the three dreaded words you have to be on the lookout for: “batteries not included.” For most of us, there has been that moment on a holiday morning or birthday when the excitement of receiving something new is dashed as the recipient realizes that without power, they just have an empty box and a lifeless gift.

Knowing what is and is not included in any transaction is critical to achieving the end goal of both parties; this is especially true for housing providers.

I recently had a potential tenant who

was going through some life challenges ask me if there was any way that I could include a washer and dryer as part of the rental. Questions like these set off all sorts of alarms in my head. I’ve been at this for more than 20 years and situations like this have rarely ended well for me… but I reluctantly gave in and provided the washer and dryer at move-in. Here’s why I entered into this agreement reluctantly; if they own the equipment and it breaks, they never call, but if I own the equipment and it breaks, I am the first call and end up playing repairman. Ideally, I avoid these situations, but under certain circumstances I do go that way and when I do, I always do two

Continued on Page 10

Rental Housing Journal, LLC 4500 S. Lakeshore Drive, Suite 300 Tempe, Arizona 85282 Circulated To Over 40,000 Real Estate Investors Nationwide Vol. 9 Issue 2 REAL ESTATE JOURNA L SPRING 2024 $4.95 Published In Conjunction With nationalreia.org rentalhousingjournal.com

Financial Independence for Real Estate Investors: The Role of Local Associations

2.

NREIA Legislative Update

The Corporate Transparency Act: What You Need to Know

. To Continue to Win, You Need to Continue to Learn

. How an IRA Investor Achieved a 255% ROI on a Real Estate Joint Venture

Navigating the Complexities of Retirement Planning

Why REIA Groups are a Must Today

Discover Mysterious Treasures in the Real Estate Landscape

6

10.

12.

14.

Financial Independence for Real Estate Investors: The Role of Local Associations

By Rebecca McLean, Executive Director, National REIA

For real estate investors, achieving financial independence is often the ultimate goal. However, the path to this form of wealth is not solely about accumulating properties or even a bigger bank account. It is about attaining a level of independence that allows you to make decisions based on your desires and goals rather than financial pressures. Valuing independence, leveraging the freedom it offers, and aiming for a fantastic life are key to real estate investors, and local real estate investor associations (an REIA) can play a significant role in supporting investors toward these goals.

1. Valuing Independence as a Real Estate Investor

For real estate investors, valuing independence means prioritizing autonomy over mere financial gain. It’s about building a portfolio that not only grows in value but also provides the freedom to pursue the life you envision. Independence in real estate investing is achieved through strategic acquisitions, diversification, and the smart management of assets to ensure a steady flow of passive income. This income stream enables investors to step back from the day-to-day grind and make choices that align with their personal and professional aspirations. Joining a local real estate investor association can be a pivotal step in this journey, offering access to resources, education, and a community of like-minded individuals who prioritize financial freedom.

2. The Liberty to Live on Your Own Terms through Real Estate

The most incredible freedom that real estate investment offers is the ability to live life on your own terms. Financial independence through real estate means not just the accumulation of assets but the liberation they provide. This includes the freedom to choose your projects, the flexibility to set your schedule, and the opportunity to work with individuals who share your vision and values. Local real estate investor associations play a crucial role in this aspect by providing networking opportunities, partnerships, and mentorship programs that open doors to new ventures and collaborations, making the goal of living on your own terms more attainable.

3. Achieving a Fantastic Life through Independent Investing

For independent real estate investors, living a fantas-

tic life is intrinsically linked to achieving financial independence. This entails creating a lifestyle where your investment portfolio supports your personal dreams, be it traveling, pursuing hobbies, or contributing to your community. A fantastic life is built on the foundation of independence, where your financial security is not tied to a single job or income source. Engaging with a local real estate investor association can significantly enhance this aspect by offering insights into market trends, investment strategies, and personal development opportunities that contribute to a well-rounded and fulfilling life as an investor.

Leveraging Local Associations for Independence

Embarking on the path to financial independence as a real estate investor involves more than savvy investments; it requires a supportive ecosystem that fosters growth, learning, and collaboration. Local real estate investor associations provide this ecosystem, offering a platform for education, networking, and advocacy that is invaluable for both novice and experienced investors. Through workshops, seminars, and events, investors can gain the knowledge and connections needed to navigate the complexities of the real estate market successfully. Moreover, associations advocate for the interests of investors, ensuring a favorable investment climate.

Financial independence for real estate investors tran-

scends the traditional metrics of success. It’s about achieving a level of independence that allows for a life lived on one’s own terms, supported by a business that provides both financial security and freedom.

Local real estate investor associations are instrumental in this journey, offering the resources, community, and support needed to realize this vision of independence. By valuing autonomy, embracing the freedom of investment, and striving for a fulfilling life, real estate investors can truly achieve the ultimate wealth: independence.

To find a National REIA-affiliated real estate investor association near you, please visit: nationalreia.org/find-a-reia.

Rebecca McLean is the Executive Director of National Real Estate Investors Association. With

Real Estate Journal Real Estate Journal · Spring 2024 2

National REIAU, we have

learning

of the best fast, easy and inexpensive. National REIAU delivers great low-cost, high-quality investor training on exactly the subject you want, exactly when you want it. Learn more by visiting nationalreiau.com

made

from some

NREIA Legislative Update

SCOTUS: Rent Control Remains for Now

The Supreme Court of the United States (SCOTUS) declined to hear a challenge to New York City’s rent control law, leaving it in place for now. Housing providers argued the law violates their property rights, but the court didn’t take the case. While the pleading focused on a Takings Argument, the court sought a more specific fact pattern necessary before taking up the issue. Evidently SCOTUS is comfortable with the government restricting owners from profitability as long as they still have “some” rights to their property. However, the court hinted at potential future interest in the issue, as Justice Clarence Thomas expressed concerns about the regulations’ constitutionality and requested more specific details about their impact. This decision maintains rent control while leaving the door open for future legal battles over the balance between tenant protections and property rights.

Election-Year Shenanigans?

The current Congress has been one of the least productive in U.S. history. With majorities resting on razor-thin margins, especially in the House of Representatives, very little is being accomplished. Key issues dominating the election scene range from budget deficits to illegal immigration to global unrest in Ukraine, Israel/Gaza, and numerous other regions. It will not get better until after November and likely well into January before things settle down. And, let’s not forget, this is also an election year for Congress along with a presidential contest that is shaping up to be a rematch of 2020.

Financial Impact

Divergent threats to the Suez and Panama canals are increasing shipping costs and adding to logistics snarls that may affect material supplies and cost! Just as the threat of inflation was supposedly decreasing, and the central banks of Australia and the UK are focused on lowering rates, the supply chain will likely increase the threat of inflation directly while the shortages will add to indirect cost pressures. If you are purchasing larger quantities of products from overseas, be prepared for delays.

Big Housing

Our political system has a series of checks and balances that include not only the usual executive/legislative/ judicial tensions, but also local, state and federal tensions. As noted above, with little being accomplished at the federal level, local and state elected officials are

moving to mitigate the concerns surrounding private equity funds investing in the single-family market.

At a time when the consumer, and more importantly the voter, is facing increased competition for housing, private equity groups are drawing the ire of local and state governments for further reducing single-family housing supplies as well as pushing housing costs due to the limited supply. There is more than a grain of truth to this in that private equity groups often don’t have “patient money” and are required to engage those funds in a timely fashion, often resulting in a willingness to pay top dollar. A few stories like that, and local electeds take note. When the numbers increase into the thousands in a region, the states begin to respond with efforts to transition single-family rentals to single-family home-ownership.

The obstacles with financial incentives are numerous and typically so slow to implement that it will be years before they go into effect. However, the punitive side can be achieved quickly. State and local officials are drafting (and sharing) those ideas with limits of group investments as low as 25 houses. Much like the argument made about firearm magazines—Why do you need so many rounds?—the same type of argument is being made about houses—Why does the investor need so many?

PLEASE stay engaged with local and state legislative bodies, or limits may be implemented that literally punish your business out of business. For example, one bill in Illinois limits the number of houses, and sets a punitive tax valued at the price of the fair market value of the house, for each house purchased above the limit, at the time of closing, with additional annual taxes charged as well. These bills are being shared…and may be coming to a neighborhood near you.

Corporate Transparency Act (CTA)

To allegedly combat financial crimes and enhance national security, the Corporate Transparency Act (CTA) was approved to pierce the veil of protection offered by LLCs and reveal more broadly the ownership of businesses operating in the United States. This legislation requires many companies, including corporations and limited liability companies (LLCs), to report detailed information about their “beneficial owners” – the individuals who ultimately own or control at least 25% of the company or who exercise significant influence. This information, including names, addresses, and dates of birth, is submitted to a secure database maintained by the Financial Crimes Enforcement Network (FinCEN).

Authorized law enforcement officials and, with customer consent, financial institutions can access this database to help investigate and prevent money laun-

dering, terrorism financing, and other financial crimes. While publicly traded companies and certain non-profits are exempt, most other businesses will need to comply with the CTA’s reporting requirements by the end of this year to avoid civil or even criminal penalties. As the CTA is still under implementation, details and specific regulations are being finalized by FinCEN.

Here’s a summary of the FinCEN Notice of Proposed Rulemaking, focused on enhancing transparency in the real estate sector, with the purpose to combat money laundering: The proposed rule seeks to prevent criminals from hiding illicit funds in U.S. residential real estate purchases, often using “all-cash” deals and shell companies to obscure the true owners. The rule specifically targets non-financed deals where cash purchases can help mask illegal activity. While it aims to complement existing anti-money laundering regulations, the government claims the rule will not burden the industry unduly. There are a number of groups being called upon to report the qualifying transactions, primarily attorneys, title insurance companies, and escrow agents.

Some of the key provisions include:

• Reporting requirements: Real estate professionals involved in non-financed (“all-cash”) sales or transfers of residential property to legal entities or trusts must report detailed information to FinCEN. This includes the beneficial ownership information of the entity or trust, property details, and transaction specifics.

• FinCEN Database: This reported information will enhance law enforcement investigations into financial crimes related to real estate.

• Exemptions: Transfers through traditional mortgages with regulated financial institutions are exempt, as the reporting is aimed at non-financed deals lacking standard scrutiny.

UPDATE 3/24: In early March, 2024 a federal judge in the Northern District of Alabama ruled that the Corporate Transparency Act (CTA), which became effective January 1, 2024, was unconstitutional. However, the devil is in the details. For the full update, please visit www.RealEstateInvestingToday.com/ctaupdate. For more information, please see Jeff Watson’s article on page 4 further detailing this issue as well as online at Real Estate Investing Today.

Stakeholder Groups

When it comes to addressing housing concerns or, in some areas, the housing crisis – especially during election season – politicians must show that they are doing

Continued on Page 6

Real Estate Journal · Spring 2024 3 Real Estate Journal

The Corporate Transparency Act: What You Need to Know

By Jeffery S. Watson

The Corporate Transparency Act (CTA) is here and is now in full force and effect. In 2021, Congress passed this legislation, which was signed into law by President Biden but did not become official and enforceable until January 1, 2024. This is the most broad, overreaching, and invasive federal reporting statute in the history of our government that squarely and directly affects every small business owner, entrepreneur, and real estate investor you know.

If you are a real estate investor, agent, broker, operator, or anyone else who owns a business, here is what you need to know.

• Which of your entities are considered “reporting entities” under the CTA?

• Who are the beneficial owners of each entity?

• What disclosure information is required?

Using that information, you are now required to timely file your disclosures with the Financial Crimes Enforcement Network (FinCEN). The regulators at FinCEN changed and expanded the time frame for a newly-formed 2024 company to report. It has 90 days. If a company formed in 2024 makes any changes to its ownership structure, such as adding or losing a member or someone different having substantial control, it is still a 30-day reporting window for that. Entities that existed before the January 1, 2024 effective date are required to report within one year of the effective date.

Let’s start with what entities are considered to be “reporting” companies under the CTA. The types of entities that must report include C-corporations, Sub-S corporations, LLCs taxed as corporations or partnerships, and LLCs treated as disregarded or pass-through entities.

There is a minimum threshold for the entity of owning, possessing, or controlling $1,000 or more in assets. This means if you have an entity, for example an LLC, that has only been filed with the secretary of state but does not yet have a tax ID number and does not yet own or control anything, that entity is not considered to be a reporting company yet. When that entity does get a tax ID number and has control or ownership of $1,000 or more of assets, whether directly or indirectly, that entity will then need to report.

What must be reported? Any person who has either substantial control of or an ownership interest of 25% or more in an entity must be disclosed. You do not report what is owned by the entity, you report who owns the entity. “Ownership interest” as defined under the CTA is incredibly broad and covers all sorts of arrangements, including, but not limited to, equity, certificates, interest in joint ventures, convertible interest, and bearer shares. Any individual who owns or controls an ownership interest through various means such as trusts, beneficiaries, grantors, intermediaries, or blocker MUST be reported.

Under the CTA, the definition of substantial control is distinct from other federal statutes defining that term, such as securities laws. Under the CTA, an individual is deemed to exercise substantial control if any of the following is true:

• They serve as a senior officer or manager of the entity that must report beneficial ownership information to FinCEN,

• They have authority over senior officer appointments,

• They have authority over a majority of the board of directors, or

• They influence important decisions, including those related to business operations, asset transactions, equity issuance, borrowing money, entering into contracts, and governance documents.

In the CTA, there is a non-exhaustive list of examples wherein an individual may exercise substantial control, but the foregoing list should give you an idea as to how wide open and subject to interpretation the term “sub-

CORPORATE TRANSPARENCY

stantial control” is as it relates to business operations, asset transactions and equity issuance.

I know what some of you are thinking: “Well, Jeff, I’ll never own more than 24%, and I’ll stay under that 25% threshold.” That’s fine, as long as you don’t have any substantial control. Without having substantial control, however, how are you going to be able to have that entity do what you want it to do? For example, in a small LLC that buys, fixes, and resells houses, those who make the decisions on what houses to buy, how much to spend, how to do the rehab, what contractors to hire, where to borrow the money, and when to sell the property and for how much, would all have substantial control.

Reporting is done through FinCEN’s website. I want to remind you of the importance of having good identity-theft insurance in place because it’s more likely than ever that your identity will now be exposed. You need to make sure that identity-theft insurance covers the family-owned businesses you may operate and control.

I understand that Congress set forth requirements regarding the cyber security for FinCEN’s website, and they are saying it has been given the highest non-classified cyber protection possible; but I also know that there is a history of even classified websites in our federal government being hacked by foreign operatives. That information will be stolen some way, somehow. I don’t know when or by whom or how, but I’m preparing for it now, and I recommend you do the same.

The CTA may also affect the way entities are formed. The CTA places a significant responsibility on the applicant to verify the accuracy and authenticity of the information being used to file a new entity. With the significant responsibilities and potential penalties being assessed on the person who actually goes online to submit the information with a Secretary of State office or tribal authority, individuals like attorneys or accountants will be less likely to want to take on that task on behalf of someone else.

The burden of determining what “substantial control” is, given the vague and broad language used in the statute and the uncertainties of the ever-changing rules and regulations, has caused certain advisory groups for accountants to say that accountants should not be doing this as a service to their clients going forward. I tend to agree. I anticipate that in the near future, and probably for some time to come, those who are very

careful about their craft are going to insist that any new LLC be established by either the actual owners themselves or by an actual lawyer (not a paralegal) advising or representing the owners and/or the new entity. The extra burdens and responsibilities will most certainly affect the cost of having an attorney assist with establishing an entity.

I suggest the following plan of action:

• Identify every LLC and corporation in which you have an ownership interest or with which you have an affiliation.

• Verify that each entity has its own taxpayer identification number.

• Every entity that has $1,000 or more of assets that it owns or controls must report in 2024.

• Make sure you have purchased identity-theft insurance.

UPDATE 3/24: In early March, 2024 small businesses across the United States were rejoicing upon hearing the news that a federal judge in the Northern District of Alabama, in a case brought by the National Small Business Association and Isaac Winkles, a member of the NSBA, had ruled that the Corporate Transparency Act (CTA), which became effective January 1, 2024, was unconstitutional. A few days later, the judge clarified his decision saying that his decision only applied to the parties in the case before him. If you were a member of the NSBA as of March 2024, then you were free from the burdens of filing under the CTA. If you were not a member of that organization at the time the lawsuit was filed, then it does not apply to you. Please visit www.RealEstateInvestingToday. com/ctaupdate for more information.

Jeffery S. Watson is an attorney who has had an active trial and hearing practice for more than 25 years. As a contingent-fee trial lawyer, he has a unique perspective on investing and wealth protection. He has tried more than 20 civil jury trials and has handled thousands of contested hearings. Jeff has changed the law in Ohio four times via litigation. You can read more of his viewpoints at WatsonInvested.com.

Real Estate Journal Real Estate Journal · Spring 2024 4

Published quarterly for chapters, associated real estate investor associations, their members and guests.

Editor Brad Beckett brad@nationalreia.org

For inquiries regarding Membership, Legislative, REIA organization information or to become a industry partner, call National REIA toll free at

888-762-7342

Fax: 859-422-4916

Hours of operation: 9:00a.m. to 6:00p.m. Eastern time zone Find us online at: info@nationalreia.org www.NationalREIA.org

RE

By M. Jane Garvey

By M. Jane Garvey

Real estate investing is a complex business. There are many different types of investments and strategies that fall under this broad banner. Rentals and rehabs are perhaps the most common that our members get involved in. To succeed in even these two seemingly basic investments you need to commit to continue to learn. The more you move out of the basics, the more knowledge is needed, and the more difficult it is to find reliable sources.

Publisher

The

As we learn about the business of real estate investing, we need to make sure that what we are learning is applicable where and when we are investing. This can be quite difficult, as things are continuously changing. No one is an up-to-date expert on everywhere and everything. We all need to learn how to investigate the reliability of what we are learning, and make sure that we are capable of updating the information we find.

There is nothing that makes the continuous quest for knowledge more necessary than dealing with ever-changing rules and laws. What is mandated by policymakers one year may be illegal the next year. One municipality may require that you de-convert a small multi-unit that started out life as a single-family home, while another incentivizes converting a larger home into several units. Building codes and many other applicable laws vary from community to community.

In Illinois, many municipalities enacted crime-free housing laws. Now that the state legislature is moving to outlaw discrimination based on arrests and even convictions, they are also trying to outlaw the crime-free housing ordinances. The pendulum swings from one extreme to the other – with the investor required to keep up with it or face expensive penalties.

Another of the basic areas that requires up-to-date knowledge is finding the value of a property. This has always been more of an art than a science. The

marketplace is imperfect, with many variables affecting values. It is rare to find two identical properties to compare, even when they are newly built by the same builder with the same floor plan. Yet, valuing property is one of the most basic skills required to succeed as an investor. After-repaired value, or market value (no repairs needed), is a key to every formula for determining what you can pay.

As investors, we need to become familiar with the things that are valued by buyers and renters. This can vary by the location of the property, the community that will buy or rent, and it can change with time. Getting it wrong can be expensive. Getting it right can allow you to dramatically change the value of a property by bringing it up to date with buyer preferences.

Anyone who has been in the business for very long can tell you that they have seen appraisals that were way off. Key neighborhood value-defining boundaries are often missed by out-of-area appraisers. They can also be easily missed by out-of-area investors and real estate agents. Even with the best advice and help, an estimate is an estimate and needs to be treated as such. A good rule from my perspective is to leave a cushion for error. The less experience you have, or the less reliable your information, the larger the cushion needs to be.

We all see news stories about prices rising by $X or Y% in our town. Those numbers are typically compiled averages. Actual numbers for your properties could be going down, sideways, or up even faster. All information needs to be drilled down to the point where it is relevant to your investment.

So, where do we find good, reliable information? The marketplace will provide the ultimate answer. When you hold your property out for rent or for sale you will get the answer. What are people willing to pay? This of course relies on it being a free market – something that is not always the case these days.

Short of waiting for the marketplace to provide you with the answer, you can

look to others that are familiar with the market. Having an active, reliable, and trustworthy real estate agent can help a lot. They need to have the vision to look past the as-is to the what-it-can-be in order to give you guidance on how the market will respond to your offering after you repair it.

Having friends who are also investing in the same area to run things by will help when you want to see if there are any holes in your knowledge and reasoning. Your local real estate investors association (REIA) is a great source of like-minded people who can often help you with that.

On the legislative front, you should get connected with a good source of up-todate information. You can look up the laws and regulations at the HOA, local, county, state, and federal level, if you know what you are looking for. You can also sign up for newsletters from your real estate attorney and real estate accountant. Looking at proposed legislation will allow you to adjust before you get caught by unexpected changes. In this arena, connecting with an association that works as an advocate for investors is important. Your legislators may also be good contacts to cultivate.

Occasionally the grass will look greener in a different pasture, but I suspect that when you examine other strategies or investments, you will find that they, too, have their own benefits and problems.

There is never a dull moment in this business. Knowledge is power, and the only way to tap into it is to keep learning. With the extra knowledge, you can continue to win.

M. Jane Garvey is President of the Chicago Creative Investors Association.

Real Estate Journal · Spring 2024 5 Real Estate Journal

publishers

Journal is published by Rental Housing Journal, LLC,

of Rental Housing Journal www.rentalhousingjournal.com

John

Linda

Advertising

Terry

Triplett john@rentalhousingjournal.com Editor

Wienandt linda@rentalhousingjournal.com Associate Editor Diane Porter

Manager

Hokenson terry@rentalhousingjournal.com

articles in RE Journal written by all authors are presented to you for educational purposes only. The authors and the National Real Estate Investors Association strongly recommend seeking the advice of your own attorney, CPA or other applicable professional before undertaking any of the advice or concepts discussed herein. The statements and representations made in advertising and news articles contained in this publication are those of the advertiser and authors and as such do not necessarily reflect the views or opinions of National REIA or Rental Housing Journal, LLC. The inclusion of advertising in this publications does not, in any way, comport an endorsement of or support for the products or services offered. To request a reprint or reprint rights contact Rental Housing Journal, LLC, 4500 S. Lakeshore Drive, Suite 300, Tempe, AZ 85282. (480) 454-2728 / (480) 720-4385 © 2024, all rights reserved.

Continue

Learn

To Continue to Win, You Need to

to

How an IRA Investor Achieved a 255% ROI on a Real Estate Joint Venture

By John Bowens, CISP

There is a misconception among aspiring real estate investors that you need substantial capital to get started. However, the journey of an Equity Trust IRA investor debunks this myth, instead showcasing the immense potential of leveraging a selfdirected Roth IRA for real estate investments. This investor embarked on a real estate joint venture with a mere $13,000 in their Roth IRA and strategically navigated the investment landscape to yield a staggering 255% return on investment.

Strategic Investment With Small-Balance IRAs

This strategy involves identifying potentially lucrative real estate opportunities, partnering with financial allies, and utilizing the advantages of self-directed IRAs. Here’s a real-life example that illustrates this strategy.

Investor A had about $13,000 in his Roth IRA. He needed about $105,000 for the purchase and rehab of an investment property he identified. Investor A brought that opportunity to a “financial friend” (Investor B). They then structured a real estate joint venture agreement that spelled out that 50% of the net profits upon the sale of the property would go back to Investor A’s Roth IRA, and 50% of the profit would go back to Investor B’s Roth and traditional IRAs.

Did investor B have to use an IRA? No. It could have been their non-IRA funds. The key here is Investor A found the opportunity and used his self-directed Roth IRA with only about $13,000, earning $68,000 in profit. And since Investor A negotiated with Investor B to receive 50% of that net profit, he made $34,000 tax-free through this real estate joint venture.

The investor’s journey involved finding a promising real estate deal, forming a joint venture agreement with a financial friend, and leveraging their Roth IRA for the investment. The result was a significant profit of $34,000 tax-free, catapulting the IRA’s value from approximately $13,000 to over $47,000.

By combining resources and expertise with a financial partner, investors with limited capital can access larger and more lucrative deals, maximizing their return on investment. The journey of this Equity Trust client serves as an example of the efficacy of strategic partnerships and the innovative use of self-directed IRAs in real estate investing.

Inspiration for Real Estate Investors

For real estate investors looking to maximize their investment potential, this example demonstrates that with the right strategy, partnerships, and investment vehicle, achieving substantial returns is not only possible but within reach, even with a small initial investment. When combined, these strategies could open doors to new investment opportunities.

By embracing the principles of strategic investment, leveraging self-directed IRAs, and forming beneficial partnerships, real estate investors can unlock new avenues for growth and potentially achieve remarkable returns on their investments.

Special Self-Directed IRA Offer for National REIA Members Only

Equity Trust Company is a national sponsor of the National Real Estate Investor Association (NREIA) and is offering NREIA members and its affiliated chapter members a special introductory self-directed account offer.

NREIA members can open an Equity Trust account for a discounted rate of $99 and receive bonuses worth $720 or more:

Legislative Update ... continued from Page 3

SOMETHING! Many municipalities are forming boards and commissions to address a range of housing issues. While eviction and affordability are often headline issues, there are plenty of process items that affect rehabbers and single-family rental housing providers. In several communities these groups have taken the form of rental commissions or eviction-avoidance task forces. The stakeholders invited to the table often represent several non-profits and legal representatives of low-income individuals. Representatives from the municipality and county are often involved, with occasional support from state and federal representatives. Some groups are designated by statute and specific individuals are delineated. In other communities, the group functions more like an interested-party meeting and is rather

casual on the participation. Both groups have their pros/cons.

With statutorily designated committees it is critical to be involved at the very beginning of the process, as mayors and councils do not like to come back and add stakeholders, nor do bureaucrats like to recommend them at a later time because it makes them look like they had included only those they wanted – which they do. So, they will often encourage “public participation,” which is qualitatively different than being a voting member in the committee records. Representation at this level requires ongoing participation by an organization and successful relationship-building that is solution-oriented – or loud enough that the organization cannot possibly be overlooked. In the latter case, prepare to be outnumbered, so the representative

• National REIA GOLD Level membership (includes priority processing and an experienced client service team dedicated to members) for one year

• Digital download of the No. 1 ranked book on Amazon: Self-Directed IRAs: Building Retirement Wealth Through Alternative Investing

• More exclusive wealth-building education Visit www.trustetc.com/nationalreia or call 844-7329404 to learn more.

John Bowens, CISP, is director and the head of education and investor success at Equity Trust Co., a leading custodian of self-directed IRAs. Visit www.TrustETC. com for more information.

Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional.

needs to be organizationally supported, persuasive and fully engaged for those last-minute agenda and venue changes that will inevitably occur.

Interested-party or task force meetings can suffer from a lack of facilitation, but that can be beneficial, allowing for deeper dives into the underlying problems and development of a universal list of concerns with a shorter list of action items. Participation is critical in those meetings, but while some of the members are paid by their organizations to attend – and are therefore quite content to have more meetings – the time demands can burden small business owners. Semi-retired participants can help by being engaged and keeping the broader group up to speed.

In both cases, the development of relationships and institutional knowledge

is critical to success. In a similar vein to poker, members must not just play the cards that are dealt but work the members, understanding their motives, needs, and goals. Attendance is critical. If your organization is allowed to be there and no one represents your interests, concerns raised later will often be dismissed. Remember: If you are not at the table, you are on it.

Stay Up-to-Date

Stay up to date with current industry news and updates by visiting RealEstateInvestingToday.com. Likewise, visit NationalREIA.org/advocacy to stay on top of current legislation and governmental actions.

Real Estate Journal Real Estate Journal · Spring 2024 6

Real Estate Journal · Spring 2024 7 Real Estate Journal ET-0039-80 © 2021 Equity Trust®. All Rights Reserved. Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Exclusive National REIA Member Benefits at Equity Trust Open a self-directed account at Equity Trust and receive: 844-732-9404 www.TrustETC.com/NationalREIA $99 SELF-DIRECTED IRA FOR 1-FULL YEAR* *$50 SETUP FEE APPLIES TWO FREE WEALTH BUILDING WORKSHOP TICKETS EDUCATIONAL MATERIALS COMPLIMENTARY GOLD LEVEL MEMBERSHIP TWO FREE EXPEDITED PROCESSING CERTIFICATES & TWO FREE WIRE TRANSFER CERTIFICATES $720 MINIMUM SAVINGS ET-0039-80 © 2021 Equity Trust®. All Rights Reserved. Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Exclusive National REIA Member Benefits at Equity Trust Open a self-directed account at Equity Trust and receive: 844-732-9404 www.TrustETC.com/NationalREIA $99 SELF-DIRECTED IRA FOR 1-FULL YEAR* *$50 SETUP FEE APPLIES TWO FREE WEALTH BUILDING WORKSHOP TICKETS EDUCATIONAL MATERIALS COMPLIMENTARY GOLD LEVEL MEMBERSHIP TWO FREE EXPEDITED PROCESSING CERTIFICATES & TWO FREE WIRE TRANSFER CERTIFICATES $720 MINIMUM SAVINGS ET-0039-80 © 2021 Equity Trust®. All Rights Reserved. Equity Trust Company is a directed custodian and does not provide tax, legal or investment advice. Any information communicated by Equity Trust Company is for educational purposes only, and should not be construed as tax, legal or investment advice. Whenever making an investment decision, please consult with your tax attorney or financial professional. Exclusive National REIA Member Benefits at Equity Trust Open a self-directed account at Equity Trust and receive: 844-732-9404 www.TrustETC.com/NationalREIA $99 SELF-DIRECTED IRA FOR 1-FULL YEAR* *$50 SETUP FEE APPLIES TWO FREE WEALTH BUILDING WORKSHOP TICKETS EDUCATIONAL MATERIALS COMPLIMENTARY GOLD LEVEL MEMBERSHIP TWO FREE EXPEDITED PROCESSING CERTIFICATES & TWO FREE WIRE TRANSFER CERTIFICATES $720 MINIMUM SAVINGS

night and unexpectantly found a house in Marietta during a drive after dinner. We called the Realtor and viewed the house that night. The next day, instead of finishing the drive to Fort Myers, we decided to make an offer — even though our lives were back in Wisconsin. The Realtor worked with us during the next few days, even reimbursing us for some of our expenses while working on the contract, inspection, and financing.

We finally had a binding agreement (I really had no idea what that was — but it sounded like we were buying a house!).

The Realtor always returned our pages quickly (phones were not as popular back then) and made us feel at ease.

We never made it to Florida and returned home where I advised my boss about the house and asked for a transfer.

My boss informed me of an opening in Atlanta. Because I did not know where Atlanta was in relation to Marietta, I remember pulling out the Rand McNally map, measuring the distance with a ruler, and thinking it did not seem that bad. The Realtor gave us recommendations of local hospitals for my wife, a nurse, and she got a job quickly. Twenty-eight days later, we were in Marietta, Georgia.

Where is your current market and what is your focus or area of expertise?

My current market is north of Atlanta in Bartow, Cherokee, and Cobb counties. Some of the cities I focus on are Acworth, Cartersville, Emerson, Marietta, Smyrna, and Woodstock.

How did you get started?

I got started through the Realtor who

helped me buy my first house. I was so impressed with the process that I wanted to get my real estate license and help people find their dream homes, like she did for me. After receiving my real estate license, I received a call six months later from my old boss in Wisconsin. AT&T was closing the office up there, and some of my old co-workers were moving to Atlanta. I got the business and referrals to sell their old homes and help them buy new homes.

Describe a typical work week for you as a real estate investor.

Typically, I try plan each day the night before. Every morning, I read and answer emails. As you would imagine, a lot of unplanned things come up throughout

“Subject

the day. However, my goal is to talk to 10 sellers or buyers every week.

How long have you been investing in real estate?

When I was a property manager, I was doing a lot of the accounting and looking at the rent each of my owners was receiving. I realized the difference between the payment and actual rent. I have been interested in investing ever since. My first investment deal was in 1995.

Tell us about your first deal.

My first deal was a NQ/NE loan. This means that you take over the payment and give the owner their equity. The owner wanted $1,850 to buy the house and take over the payment, and the house was rented for $850 a month with a payment of $462.09. I had maybe $50 at the time and did not want to borrow from family or friends. My boss even

said he would loan me the money, but I did not want to do that. Instead, I went to the bank and took out a cash advance on my credit card. Looking back, it was not the best choice with the cash advance fee, daily interest, and higher credit card payment. But I knew I could make it work. When repairs would come up, I had to use the credit card. When the tenant didn’t pay one month, I had to go deeper in the hole. Several years later, I sold the property and made a good profit even with all the interest we paid. If I had held the property, it would now be worth three times what I sold it for back then, and the rent today in that area is $2,800 per month. I should have listened to my old boss and kept that house.

How do you fund your investments?

Today, my favorite way to fund my investments is buying Subject-To — which reminds me a lot of the NQ/ NE loans. My second choice is owner financing, and my third is DSCR loans. DSCR loans are Debt Servicing Coverage Ratio loans. I like this type of loan due to the fact it has very little paperwork. On DSCR loans, 20 percent is needed for the down payment. The rent has to cover at least the payment, and the property has to appraise. You also have to have insurance on the property. Even though the rate is a little higher, if someone is making the payment and there is still positive cash flow, I am good.

Do you have your real estate license?

Yes, I’ve had my real estate license since 1992. ln addition I have owned a real estate brokerage since 2004.

Real Estate Journal Real Estate Journal · Spring 2024 8

Member Spotlight - Tom Begora ... continued from Page 1

Getting ready to teach about

To” deals in Sandy Springs, GA

Tom and his wife, Tammie

9

Exterior of Tom’s latest project that was part of an equity deal.

Continued on Page

Interior of Tom’s latest project that was part of an equity deal.

What projects are you currently working on?

This year, I have purchased three properties (Subject-to, DSCR, and an equity deal) as of mid-January. Currently, I am working on an equity deal and getting the property ready for the market. I am also working on expanding my team and teaching.

How much time do you put into your real estate education?

I put a lot of time into real estate education. I am usually on a Zoom class at least three times a week and attend as many meetings as I can regarding real estate. The meetings are so important, especially with my REIA. I strongly recommend finding one in your local area. The content, knowledge

Before and after photos of a mobile home rehab project in Florida that Tom’s parents now live in.

and networking are incredible. The business and relationships you create are irreplaceable and a great resource for deals and ideas.

Has coaching or mentoring played a part in your success?

Over the years, I have had many mentors who have brought me to the next level. Today, I am now mentoring and coaching. It is now my time to give back and teach others.

What are your current and future goals?

This year, I have a goal to purchase 10 homes. Three are under the belt already, and two are under contract (which should close by mid-February). I also have a goal to partner on at least five deals and teach at least 12 classes.

What has been your top struggle?

In this business, my top struggle is myself. I talk myself out of deals instead of presenting my best offer and letting the seller decide.

What do you like most about what you do?

It’s never the same day twice! I like that I get to make my own schedule. I am solving real estate problems as I travel and spend time with family and friends.

Do you have a tip or advice that you would pass along?

My advice is to talk to sellers. One of the easiest ways to do this is to go to garage or estate sales and ask if they are selling or know someone in the area that is selling. Find a Realtor in your area who works with investors. In addition,

have the mindset that I am not buying or selling homes; I am solving real estate problems.” If I cannot solve their problem, I give them alternate solutions.

How important is joining a local REIA to a new investor?

Joining a REIA should be one of the first things you do in your area. In almost every major city, there is a REIA. Sign up for the yearly membership. It saves you a few dollars and helps commit you to show up. Before and after each meeting, talk to the attendees. They could be the ones funding your next deal!

What is your favorite self— help book?

My favorite self-help books are from Tony Robbins. I’ve read a lot of his books and I listen to a lot of real estate podcasts.

Do you have any interesting hobbies or something unique that you like to do?

At home, my wife and I have a pony, pig, chickens and a dog — so that’s a lot of fun. I also like to watch my son play baseball at Young Harris College.

Do you have any social media accounts?

If I have social media accounts, then my kids set them up. Ha! I get most of my leads from phone calls, going to garage/estate sales and doorknocking. I also run Cartersville Real Estate Investors breakfast meeting in Cartersville, Georgia, every Tuesday at 8 a.m. at IHOP. If you are in the area, be sure to stop by and bring your real estate problem to our meeting.

Real Estate Journal · Spring 2024 9 Real Estate Journal

Member Spotlight - Tom Begora ... continued from Page 9

Tom and Tammie with their son Jeremy, who was Baseball Player of the Year at his college last year.

By Carl Fischer

RNavigating the Complexities of Retirement Planning

eaching retirement is an important milestone, and part of the journey often involves managing your retirement savings. If you’ve recently changed jobs or retired, you may be faced with the decision of what to do with your old 401(k) plan. It can be daunting or exhilarating. It can be similar to the past years or an opportunity to unlock your funds, take control, and invest in a different way. This article will explore various options available to individuals with old 401(k) plans and provide insights to help you make an informed decision.

1. Evaluate Your Current Plan

Before making any decisions, it’s crucial to assess your existing 401(k) plan. Consider the plan’s investment options, fees, and overall performance. If you’re satisfied with the plan and it meets your retirement goals, leaving your funds in the current 401(k) may be a viable option. This decision allows you to maintain the tax advantages and convenience of managing your retirement savings in one place.

2. Roll Over to Your New Employer’s 401(k) Plan

If you’ve started a new job that offers a 401(k) plan, you may have the opportunity to roll over your old 401(k) funds into the new plan. Assess the new plan’s investment options, fees, employer contributions, and other features to determine if it aligns with your retirement objectives. Rolling over funds into a new 401(k) plan can simplify your retirement savings strategy and keep your investments consolidated.

3. Consider an Individual Retirement Account (IRA)

Rolling over your old 401(k) into an Individual Retirement Account (IRA) is a popular choice that offers greater flexibility and control over your investments. IRAs provide a wider range of investment options compared to most employer-sponsored plans. A self-directed IRA provides true diversity and control, and the most asset options available, including alternatives such as real estate, notes, private placements, and precious metals, to name a few. Self-directing your investments is more work, but you are using your expertise and knowledge and investing in what you know and understand. You can choose between a traditional IRA or a Roth IRA based on your tax preferences. While a traditional IRA offers tax-deferred growth, a Roth IRA allows for tax-free withdrawals during retirement.

How Inclusion Affects Your Rentals

key things that will help to protect your investment.

Establish Your Ground Rules

When it comes to rental property, the number of items a tenant may ask for is unlimited. In your business, determine in advance what and what will not even be a possibility to include with the property. When it comes to appliances, those that are attached to the property are usually included. I’m talking about items like a dishwasher or oven. You might include a refrigerator depending on whether it is the built-in variety. Usually not included is anything related to laundry, microwaves, BBQ grills, etc. And speaking of grills, if you decide to provide one, make sure you establish that you are not responsible for providing fuel. I’ve taken the brunt of an angry phone call from a tenant whose dinner party plans were destroyed when the propane ran out halfway through cooking their meal. Same goes for things like yard equipment, such as if you decide to leave a lawn mower for the tenant who wants to maintain the yard. Each of these items present different challenges that require different rules, and it is best to lay out those rules in your lease.

Put it in the Lease

The lease is your first (and best) line of defense when it comes to items you have included in your property.

4. Weigh the Benefits of a Roth Conversion

If you’re considering rolling over your old 401(k) into a traditional IRA, it’s worth exploring the benefits of a Roth conversion. By converting your funds to a Roth IRA, you’ll pay taxes on the converted amount upfront, but future qualified withdrawals will be tax-free. This strategy can be advantageous if you anticipate being in a higher tax bracket during retirement or if you desire taxfree income in the future.

5. Evaluate Tax Implications and Penalties

When deciding what to do with your old 401(k) plan, it’s crucial to consider potential tax implications and penalties.

If you withdraw funds from the 401(k) before reaching the age of 59½, you may incur early withdrawal penalties and be subject to income taxes. However, rolling over your funds into another qual-

... continued from Page 1

I would recommend always using language that references the following categories:

• Ownership: Clearly state who owns the equipment that is included in the lease. This ensures that if something “walks” off at the end of the lease period, all parties know who it legally belongs to.

• Responsibility: If something breaks, it is critical to know who bears the financial and physical responsibility for its repair. For example, if I were to include laundry units in the property, I include language like, “If the laundry units become non-functional, you are responsible for all repair costs. If you do not want to cover those costs, the units will be removed from the property and you will be responsible for procuring your own units. If, when the lease is terminated, the units are in place and non-functioning, all repair costs will be covered by your security deposit.” Clear and concise, the tenant knows exactly what to expect and you can look back on this when these situations arise.

• Terms of Use: The final piece of protection is having them understand the terms by which you are providing any item in the property. This might include a term similar to this: “As the housing provider I am not responsible for any damages to your personal items created by using the laundry units provided.” Or this fun one, “Use of the

ified retirement account can help you avoid these penalties and maintain the tax-advantaged status of your savings.

6. Conclusion

Navigating the complexities of retirement planning and managing your old 401(k) plan can be challenging. You should consider personalized guidance based on your specific circumstances and analyze the pros and cons of each option, considering factors such as your age, retirement goals, risk tolerance, and tax situation.

Deciding what to do with your old 401(k) plan is an important step in securing your financial future. Evaluating your options, including leaving your funds in the existing plan, rolling over to a new employer’s plan, or transferring to an IRA, requires careful consideration. Take into account your investment preferences, fees, tax implications, and longterm retirement goals when making your decision.

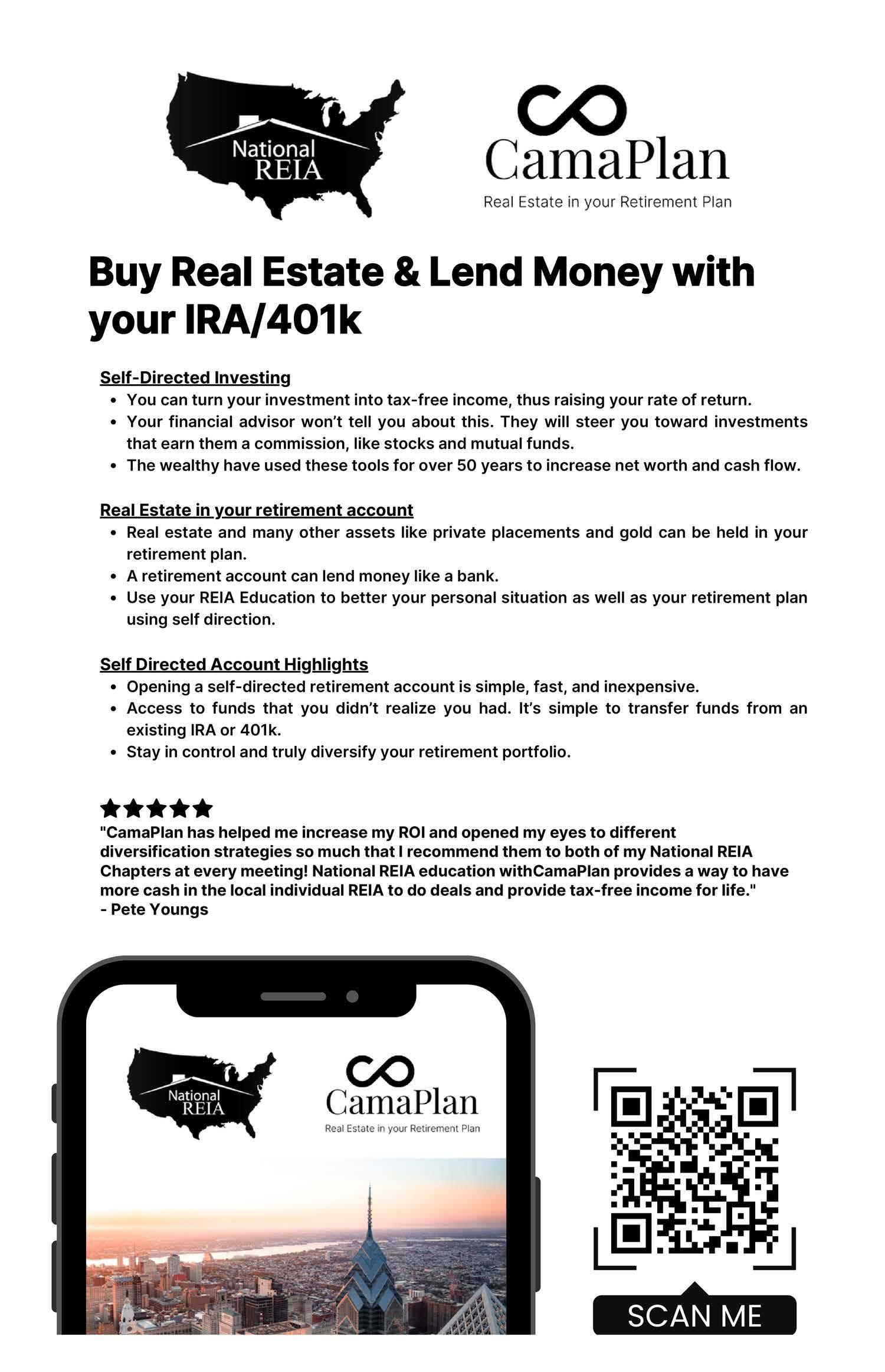

Members of National REIA can save up to $784, including a free consultation with the founder, one year of VIP customer service, and the opportunity to set up a new account for only $1. Plus, there are no annual fees until your first investment. You’ll also receive one free expedited transaction processing and two complimentary outgoing wires for your real estate deals. Visit https: www. iraasset.app/nationalreia for more info.

Carl Fischer is a founder and principal of CAMA Self-Directed IRA, LLC (dba CamaPlan). CamaPlan is a national, self-directed tax advantaged plan administrator company headquartered in Ambler, PA.

provided BBQ grill is at your own risk and expense. Housing provider is not responsible for providing fuel for grill and or for any damage or loss of food associated with use of the grill.” It sounds like overkill, but I’ve seen and heard it all.

Being in this industry is a gift. I can’t think of another place that would allow me the opportunity for challenge and growth as much as being a housing provider. Knowing if and what to include in a lease is paramount to finding success; but without fail, the satisfaction that comes from helping others is definitely “included” in every transaction.

David Pickron is president of Rent Perfect, a private investigator, and fellow landlord who manages several short- and long-term rentals. Subscribe to his weekly Rent Perfect Podcast (available on YouTube, Spotify, and Apple Podcasts) to stay up to date on the latest industry news and for expert tips on how to manage your properties.

Members of National REIA can take advantage of special pricing from Rent Perfect, the solution for rental property owners and managers for screening and managing tenants. Learn more at www.rentperfect.com or by calling 1-877-922-2547.

Real Estate Journal Real Estate Journal · Spring 2024 10

Real Estate Journal · Spring 2024 11 Real Estate Journal

Why REIA Groups are a Must Today

By Pete Youngs (aka Mr. Rehab)

Whether we like it or not, ever since COVID-19 came along, the business environment has caused extreme changes in how real estate investors (as well as other businesses) have had to operate and adapt. In my particular case, not only was I investing in property, but I have been a national speaker for my whole career, visiting anywhere from 100 to 200 cities a year in live training sessions. Then, suddenly, it seemed as if the world closed down. People were not able to gather in groups of any kind, venues were closed, meeting spaces were unavailable and, in all honesty, my business was completely shut down.

After all, the essence of my business was face-to-face networking. At a main

event, we could have anywhere from 75 to 300 people as well as field trainings with bus trips handling roughly 50 people. These weekend bus trips visited properties where I taught inspections, estimating, rehab costs and how to hire out contractors for about 50% off the regular general contractor rates. I was also stopped from doing my favorite and most popular things, such as my mold-certification training and my signature Home Depot nationwide store tours, which I originated over 20 years ago at corporate.

When live and in-person events were put on hold, and with no one really being able to predict how long the shutdown would last, changes had to be made. I consider myself to be old-school, and the people whom I had been speaking alongside of all these decades also needed to

adjust how they were to stay afloat.

Originally, I was brought into the business by my brother, Tony Youngs. He is an expert in finding distressed and hidden market properties, and I was the fix-up and rehab guy. Tony has set up coaching calls once a week and one-onone training for years — a smart move to have made. However, the pandemic opened up a whole new breed of people who took advantage of the limited faceto-face seminars and REIA meetings to those who were internet- and tech-savvy.

They opened up the world to online meetings — Zoom, etc. Sure, most people were already there, but not very many

of us “career investors” were using these tools. So, when everyone found out that they could sit at home in a pair of pajamas and watch seminars without making the trip to an in-person event, a lot of them loved that concept. Even some of the REIA groups fell for the idea that their overhead costs would go down if they went that direction — room rental, food & beverage, speakers’ travel costs, etc. However, many of the REIA groups who were not tech-savvy lost their businesses, failed or even sold.

Now, I will explain my reason for sharing all this background. Recently, I adjusted to the market by changing my business plan. My wife, Barb, and I used our IRA accounts with CamaPlan, and started using our tax-free and tax-deferred plans (CamaPlan is a National REIA-preferred vendor) to replace our incomes. We bought two REIA groups that I run personally: North Metro REIA in Atlanta, Ga., and Metrolina REIA in Charlotte, N.C. We did this because live and in-person training is getting back up to speed. While most REIAs are not back to full rooms, I can’t stress enough the huge advantage of the face-to-face and the in-person networking that goes on in REIAs all across the country.

Attending meetings and swapping business cards with buyers, sellers, and private-money lenders – as well as the education that is brought to you each month— is really unmatchable, anywhere.

In addition, know that if your REIA is a member of National REIA, the benefits also include 20% off almost every paint in Home Depot and a 2% biannual rebate, cabinet and appliance discounts, as well as many other money-saving benefits from other providers. You can see all of the member benefits on National REIA’s website (www.nationalREIA.org/ benefits).

But most of all, please remember this: There is no better investment than membership in your local REIA group (especially one affiliated with National REIA). Where else for the cost of a nice dinner out can you improve your future? There are opportunities out there every day. There are those who sit at home and hope that some clearinghouse or lottery is going to deliver a life-changing event to their mailbox, and then there are people who realize that if you do not move, you never go anywhere.

That being said, my last thought to leave you with is this: Don’t let someone who gave up their dreams convince you to give up on yours. Think about that for a moment and thank me later.

Pete Youngs, also known as “Mr. Rehab,” is a national speaker on rehabbing homes for up to 50% off. He does seminars and bus trips promoting his training system called SWAT (Simple Ways and Techniques). He has been a contractor/investor for more than 30 years. Learn more about him at PeteYoungs.com.

Real Estate Journal Real Estate Journal · Spring 2024 12

TEL: (877) 744-3660 WWW.NREIA.ARCANAINSURANCEHUB.COM UNIQUE COVERAGE, INTELLIGENTLY DESIGNED. Call us or visit our website for more information on our property and liability programs Investment Property Insurance Tenant Discrimination Program Landlord Supplemental Protection Tenant Renters Program

Real Estate Journal · Spring 2024 13 Real Estate Journal

Discover Mysterious Treasures in the Real Estate Landscape

By Gita Faust

We must adjust our business strategies to prepare for heavy market fluctuations because the real estate market is never steady. We have seen this during the 2008 real estate financial crisis and the COVID-19 pandemic. Hence, I am guessing that with the possibility of an upcoming recession, it is necessary to stay competitive. This is only possible when new strategies are implemented, such as finding properties that are the right price for you! There are hidden gems everywhere in the real estate market; we must know how to unearth them. We have a few tips and tricks up our sleeves for you to unearth these hidden gems in the best way possible.

Insider’s Guide to Off-Market Deals

Now, what exactly are off-market properties? These are the undiscovered treasures or the hidden gems in our real estate industry. Now, what makes them unique? They are properties not listed on the Multiple Listing Services (MLS). Still, they are available through word-of-mouth, networking, or direct marketing.

There are multiple advantages of off-market properties:

• They allow us to discover the exclusive, which assists us in finding unique and valuable properties.

• They give us plenty of time for inspection, saving on repair and maintenance expenses as there is less of a rush to buy the property.

• Lastly, off-market properties are heavily negotiable as they are sold by motivated sellers who wish to sell quickly and hassle-free.

Distressed Deals Don’t Distress Us

Properties experiencing financial or physical distress due to bankruptcy, neglect, or abandonment are referred to as distressed properties. These kinds of properties may be quite advantageous as they present unique opportunities for investors to buy assets below

the market value and turn them into successful enterprises while at the same time demanding that you be able to spot a financial and economic gap that requires correction.

Finding these distressed properties is relatively easy, and searching for hints such as overgrown lawns and “For Sale by Owner” signs can help you find these properties. You can also partner with real estate professionals specializing in searching for distressed properties, as they have the necessary experience and expertise in purchasing these properties.

Promising Neighbors

Multiple neighborhoods are undergoing extensive change, experiencing positive growth, and showing excellent investment potential where you can find those hidden gems that will help you decide to flip or hold the property.

How exactly does one find these neighborhoods? Well, these neighborhoods are easily identifiable by analyzing market trends and economic growth, i.e., through thorough market research, which assists in evaluating zoning changes, and local infrastructure projects, as these heavily affect the value of properties. There are various other indicators to explore such neighborhoods, such as increased employment, infrastructure upgrades, job creation, and new businesses and organizations.

Wheels of Wealth

This method involves driving through the specifically targeted neighborhoods to find properties that may be distressed or off-market. It is a tried and tested method for discovering hidden gems known as “driving for dollars.” It’s similar to the previous ways of finding distressed and off-market properties. Still, it’s different in its approach, wherein you spot an exciting property by driving around and then researching information surrounding the property through digital records and public records. We can easily use this strategy by utilizing technological apps/tools. Unlike the traditional

approaches, we will have many more opportunities to search for these hidden gems.

Hence, thinking outside the box is necessary to find these hidden gems in the real estate market. These hidden gems provide a competitive edge by allowing us to delve into the niche markets and explore the less popular localities. Thus, real estate is an ever-evolving field, and by thinking outside the box, we can generate quick revenue and explore multiple opportunities.

Embracing the Human Touch

Real estate is about finding suitable properties, caring for them, and making wise decisions. Tracking every penny will give you the adrenaline boost you need, and maintaining accrual-based books will help you manage your cash flow. This will help you close on a property in a split second. Your success hinges on selecting prime locations, maintaining them, and expanding one’s investments.

AI might be super smart, but it’s got nothing on us humans when it comes to uncovering hidden gems! Even if AI figures out how to dial a phone, there’s just something special about the personal touch of a human. It’s like trying to teach a robot to tell a joke - sure, it might get the punchline right, but it’s missing that genuine laugh that comes from a real person!

Gita Faust is the founder & CEO of HammerZen, which helps businesses save time and money by keeping track of The Home Depot purchases and efficiently importing receipts and statements into QuickBooks. National REIA members receive discounts on QuickBooks services and software. Learn more by visiting www.hammerzen.com/nreia.

Real Estate Journal Real Estate Journal · Spring 2024 14

Control the Banking Function ... continued

(IBC) shines as a beacon of hope and innovation, offering a radical departure from the conventional banking and investment paradigms. Conceived by R. Nelson Nash and outlined in the book, Becoming Your Own Banker, this strategy is more than just a financial maneuver; it is a transformative approach aimed at securing financial independence and sustainability.

At its heart, infinite banking revolves around leveraging the properly structured cash value of whole life insurance policies to create a personal banking system. This ingenious method allows individuals to borrow against their policy to fund real estate investments, repay the loans on flexible terms, and enjoy the benefits of cash-value growth concurrently. This harmonious combination of liquidity, safety, and growth affords real estate investors unparalleled flexibility and control, distinctly surpassing what traditional banks and investment firms can offer.

Empowering Real Estate Investors

For those vested in real estate, mastering the banking function is pivotal. Traditional financial institutions, with their own agendas, often impose restrictive terms and conditions that can misalign with an investor’s objectives. These institutions control loan terms, interest rates, and repayment schedules, leaving investors at the mercy of external influences. The infinite banking approach, on the other hand, empowers investors to finance their ventures on their terms, free from outside interference.

Imagine the profound impact of never having to pay interest to an external bank again. Consider the substantial savings over a lifetime without those higher interest payments, where instead, every dollar saved amplifies your investment potential. What if you could harness that power, becoming the bank yourself? This is not just a fantasy but a tangible reality with infinite banking. It offers an unparalleled opportunity to keep the wealth within your sphere, allowing you to reapply

from Page 1

every payment into growing your real estate portfolio or other investment ventures.

This autonomy is crucial in the fast-moving world of real estate investment, where timing and the ability to swiftly maneuver can be the difference between a profitable deal and a missed opportunity. The conventional financing route, fraught with protracted approval processes, can cause investors to lose out on prime investments. The infinite banking approach, with its near immediate access to funds, enables investors to seize opportunities with unmatched agility.

Challenging Financial Misconceptions

The debate around whole life insurance, particularly the views espoused by certain well-known financial commentators, often misrepresents the value and utility of these types of policies. Their critique of whole life insurance blatantly overlooks the strategic benefits of properly structured policies, which lie at the heart of infinite banking. Unlike term insurance or qualified plans, which carry their own risks and limitations, properly structured whole life insurance provides a stable, predictable foundation for financial growth.

Moreover, the perceived safety of qualified retirement plans is another area ripe for reevaluation. These plans, while popular, are not without their vulnerabilities, including market volatility and regulatory changes that can affect their value and accessibility. In contrast, a properly structured whole life insurance policy offers a robust alternative, providing dependable growth with guarantees, and access to capital that can be a bedrock for long-term financial strategy, far removed from the uncertainties of the market or government policies.

Expanding Horizons: Infinite Banking in Personal and Family Finance

The utility of infinite banking extends beyond real estate and into personal and family financial planning,

encompassing debt management, college savings, vehicle financing, mortgages, family savings, and even retirement planning. It evolves into a privatized family banking system, offering a structured approach to managing and growing wealth throughout one’s life. The concept also revitalizes the notion of generational wealth, ensuring that wealth accumulation and efficient transfer become cornerstones of family financial stability and growth across generations.

The Infinite Banking Concept is not merely a financial strategy but a journey towards financial autonomy. It confronts and challenges our traditional reliance on banks and financial institutions, presenting a blueprint for independent wealth management and growth. By adopting the infinite banking strategy in your life, you can unlock a new dimension of financial freedom, better positioning yourself to capitalize on opportunities with ease. In doing so, you don’t just achieve your immediate financial objectives but also lay the groundwork for a future where you are the masters of your financial destiny.

The journey towards financial independence through infinite banking is both intriguing and complex. It offers a new perspective on wealth management, investments, and personal finance. If you are a real estate investor seeking to break free from the constraints of traditional finance and pave a new path toward financial freedom, infinite banking could be the key.

Imagine a life without the bank.

Imagine a life where YOU could be your own bank.

Jason K. Powers is a multi-business owner, real estate investor and an authorized IBC practitioner. In an exclusive partnership with the National Real Estate Investor Association, Jason is the go-to expert for all aspects of infinite banking and life insurance. Connect with Jason today to explore how the Infinite Banking Concept can empower you to reach your financial goals. Visit www.1024wealth.com/NREIA for more information.

Real Estate Journal · Spring 2024 15 Real Estate Journal

Real Estate Journal Real Estate Journal · Spring 2024 16

Reach

*Participating members with semiannual net purchases of more than $5,000 receive a 2% rebate from The Home Depot based on spend on registered forms of payment in Pro Xtra and tied to the NREIA program. Rebate periods are January 1- June 30 and July 1 - December 31. Rebate checks are issued 60 days after the rebate period ends. Restrictions apply. Please call 1-866-333-3551 or homedepot.nationalreia.org for further details. Pro Xtra Paint Rewards is a sub-program of the Pro Xtra Program. Pro Xtra Paint Rewards Qualifying Purchases will be tracked during the Program Period and include select The Home Depot Paint department in-store purchases and online purchases from The Home Depot websites, see https://www.homedepot.com/c/ProXtra_TermsandConditions for details. Learn more at homedepot.com/c/Pro_Xtra. NREIA MEMBERS EARN 2% CASH BACK* ON EVERY PURCHASE HOW DOERS GET MORE DONE

The Home Depot has the tools to help you get more done faster. With convenient shopping, delivery how you need it, dedicated Pro support and a cash-back rebate program*, we help you reach your business goals. Plus, NREIA members receive Gold Tier Paint Rewards with 20% off paints, stains and primers every day.

out to NREIA or your local chapter to learn how you can start earning cash back today.