SEPTEMBER 2024

04. Market CommentWhen A Little Goes A Long Way.

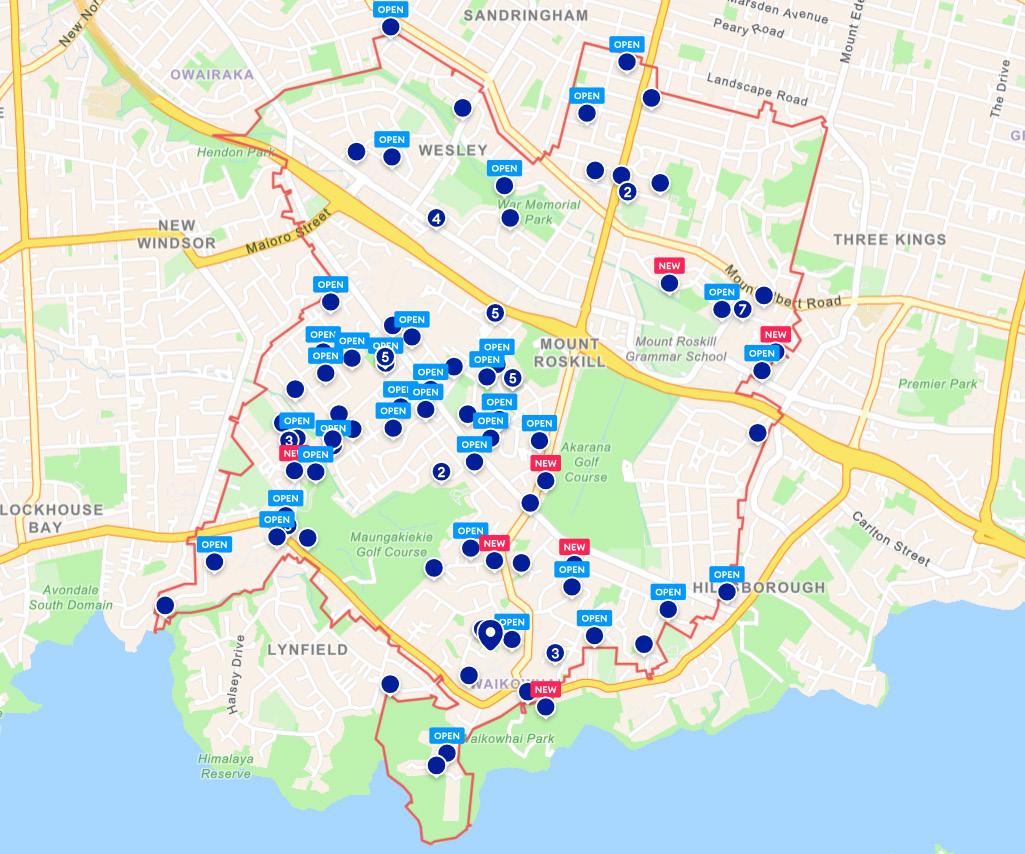

08. Mount Roskill Sales Statistics July 2024

14.

Article – Tony Alexander: Buyers are back but don’t expect a frenzy.

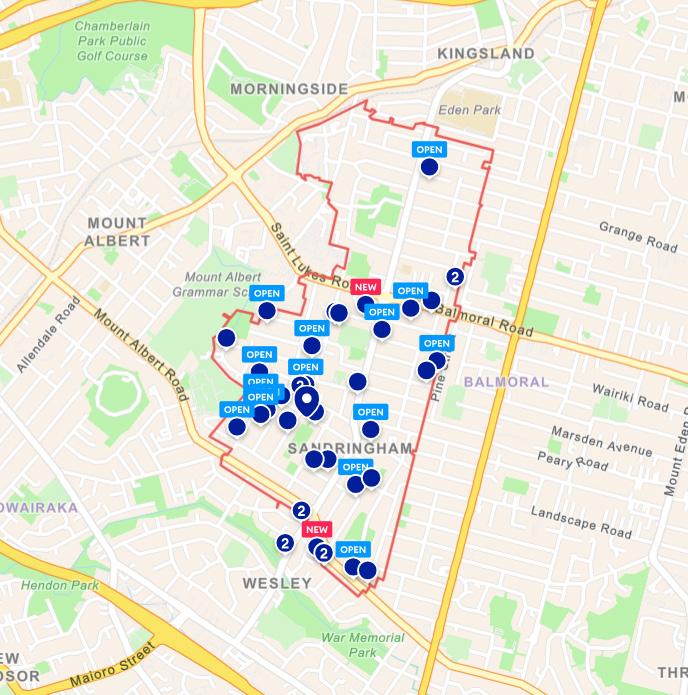

06. Sandringham Sales Statistics July 2024

12. Caset Study & Auction Update with Cameron Brain

16. Our month in Review Top Stories & Events from the City Realty Group

22. Article – Kelvin Davidson: Home loan shake-up - are property investors piling back into the market?

26. LoanMarket Update

30. Why choose us?

24. Property Management Update

28. Marketing your home

32. Ray White Sandringham & Mount Roskill team

What we are referring to is, of course, the 14 August announcement by the Reserve Bank that the Official Cash Rate was being trimmed by .25 basis points down to 5.25, the first cut since March 2020.

Director of City Realty Group, Daniel Horrobin says: “It wasn’t so much the size of the cut that mattered, it was more the message the announcement sent around the country. As well as a change in mood, an additional benefit was the flurry of bank activity as they jostled to attract customers.”

On 19 August the NZ Herald reported: “Homeowners are continuing to see the benefit of the Reserve Bank’s recent interest rate cut and outlook as banks scramble to offer competitive mortgage lending rates. ANZ today announced the largest cuts to its home loan rates so far this year.”

OneRoof goes on to report: “Mortgage brokers believe New Zealand’s one-year rate could drop to 5% before the end of the year as competition among the major banks intensifies.”

Also on Monday 19 August Ray White Head Office reported: “The New Zealand property market experienced an uptick last week in auction clearance results nationally, demonstrating a strong finish to winter and optimism ahead of spring.”

Then to close out the month on 30 August the NZ Herald quoted: “The ANZ-Roy Morgan consumer confidence index rose this month. The five-point lift was disclosed a day after the bank said business confidence rose to the highest level in a decade.”

REINZ Chief Executive Jen Baird reported in August that July brought a new wave of buyer activity not typically seen in late winter.

In their August update, Realestate.co.nz reported: “The latest New Zealand property report shows an increase in buyer activity following the recent OCR drop – the first in four years. In the two weeks after the announcement, there was a noticeable rise in listing enquiries, suggesting renewed interest from buyers.”

If ever those statements needed hard evidence, our City Realty Group Auctioneer Cameron Brain was delighted with the turnout at an early August auction conducted on-site at a suburban property by our Wynyard Quarter Team. “I counted 60 people in the lounge room, spilling out onto a backyard deck, nine registered bidders and the property sold under the hammer. I haven’t seen those numbers for three odd years.” he declared.

Daniel says: “Back on the Auckland Central sales floor, August was steady as we head into spring with considerable optimism for what the rest of the year will bring. As we indicated last month, stock is still a challenge with the total number of central city apartments for sale on Trade Me remaining stubbornly modest. Open home buyer visits were down in August compared to July, continues Daniel, “but there was a notable sting in the tail. Over the last weekend of August including Sunday 1 September, we met more than half the open home visitors we had encountered over the previous four weekends of the month. Hopefully another positive indicator of things to come.”

In the rental space, a wider view supports what we are seeing in the central city. As a result of a Tony Alexander survey in August: “This month a record net 21% of landlords reported that finding good tenants was difficult. Only five months ago a strong net 27% said finding good tenants was easy. The rental market has turned on a dime as the unusual migration boom rapidly fades.”

“Overall,” says Daniel, “there appears to be a general upswing in inquiry which augurs well for what lies in store for the warmer months ahead.”

Total Sales

August 2024

12

Up 6 from last month

August 2023

11

There was a 9% increase in the total number of sales year on year.

Total Sales Value Median Sales Price Median Days On Market

August 2024

$14,885,000

August 2023

August 2024

$1,301,000

August 2023

$16,737,111 $1,612,000

There was a -11% decrease in the total sales value year on year.

Source: REINZ

There was a -19% decrease in the total median sale price year on year.

August 2024

71

August 2023

52

There was a 36% increase in the total median DOM year on year.

Total Sales

August 2024

18

August 2023

42

There was a -57% decrease in the total number of sales year on year.

Total Sales Value

August 2024

$18,301,888

August 2023

$42,923,300

There was a -57% decrease in the total sales value year on year.

Source: REINZ

August 2024

August 2023

$947,000

Median Sales Price Median Days On Market

August 2024

$930,500 44.5

There was a -1% decrease in the total median sale price year on year.

August 2023

49

There was a -9% decrease in the total median DOM year on year.

300

503 Open Homes Conducted

City Realty Limited Licensed (REAA 2008) Properties Opened

759 People Met

Average Number of Buyers Through Open Homes Auction vs Private Treaty

6.22 Auction

1.62 Private Treaty VS AUCTION PROPERTIES SAW 3.84x THE AMOUNT OF BUYERS THROUGH THE OPEN HOMES COMPARED TO ALL OTHER SALE METHODS. (AUGUST 2024)

With spring now upon us and a recent easing of interest rates, the auction market is experiencing a noticeable surge.

Positive media coverage has further fueled this momentum, leading to a significant uptick in auction listings. September and October are fully booked with auctions, and we’ve even secured dates as far out as December.

Our open home numbers reflect this newfound energy, with 785 buyers visiting properties in the first three weeks of spring—a 29.75% increase from the 605 attendees during the same period in August 2024. Not only are more buyers attending, but the competition is heating up.

The average number of bidders per auction has risen from 1.6 to 2.2, a strong indicator of increased buyer confidence and engagement.

As media sentiment continues to shine a positive light on the real estate market, we are optimistic about a busy and successful final quarter of 2024. The City Realty Group team is prepared to meet the demand and help clients capitalize on this thriving market.

Our open home numbers reflect this newfound energy, with 785 buyers visiting properties in the first three weeks of spring—a 29.75% increase.

Auctioneer & Auction Manager 027 424 1782 cameron.brain@raywhite.com

Rate cuts have boosted confidence but house price growth likely to be modest.

ANALYSIS: Last week I wrote about the results of my monthly real estate agent survey showing a strong return of buyers to the market but without upward pressure on prices as yet. This week it is worth also noting the survey of mortgage brokers I undertake with mortgages.co.nz which shows similar strength.

A net 51% of brokers report that they are seeing more first-home buyers looking for advice while a net 33% say there are more investors in the market. Two months ago these results were -7% and +9%, which tells us that in response to the change in the interest rates outlook, it is young buyers who feel more greatly motivated to consider a home purchase.

For investors, the lowering of interest rates over time will clearly help. But we have

to remember that the heydays of easily growing wealth or even easily getting a good running yield from running a residential rental business have long gone. Credit is much harder to get from lenders, costs like rates and insurance are a lot higher, tenant legislation is much stronger, and property prices also are a lot higher.

When prices do start rising, we are certain to see more investors as that is the nature of all asset price cycles. But a repeat of one of the frenzies in place since credit rules were freed up in the mid-1980s is very unlikely. There is a structural shift underway in the role of investors in the housing market and that is both good and bad. It is good in that extra space will be provided for owner-occupiers and the ratio of average house prices to average

household incomes won’t climb as high this time around. It is bad in that when the rental market comes through its current period of temporary oversupply, the situation for renters will become quite difficult. But that is a story for perhaps a couple of years from now once developers who currently have placed unsold properties in the rental market have offloaded them to buyers.

Another element that will restrain price gains this cycle will be the rule changes allowing greater densification around the country and requiring the zoning of more residential land ready for development. These are good things. But given the hikes in construction costs, it is unlikely that we will ever see a serious decline in the ratio of house prices to incomes back remotely to the three ratio, which used to apply until the 1990s.

On another note, I’ve just had a look at how the NZ dollar moved once our economy went into recession in the three cycles before this one. Back in 1991 our economy shrank 1.3% but rebounded to 6.6% growth within two and a half years assisted by an 11-cent fall in the NZD. Back in 1997/98

the economy grew 0.4% at its weakest point (two quarters in a row GDP shrank so the technical recession definition was met) then rebounded to 6% within a year and a half helped by a 20-cent NZD decline.

After the 1.8% GFC shrinkage over 2008/09 growth did not exceed 4% until 2015. Although the NZD fell from 80 cents to below 51 cents it quickly jumped back up to 73 so the currency-induced bounces in the export sectors and the regions were muted.

This time around with the annual average growth measure looking like reaching -0.5% or so, has the NZD declined at all? No, we sit near US 62 cents from 59 cents a year ago and two years back. With interest rates falling offshore or set to fall, the chances of NZD depreciation against the US dollar this cycle look very low. In fact, since the August 14 easing of NZ monetary policy the Kiwi dollar has actually risen almost two cents.

The lack of a very strong cyclical surge in exporting will constrain the income-driven extent of average house price gains over the next few years.

@raywhiteaucklandcentral

@raywhitewynyardquarter

@raywhitesandringham

@raywhite.mtroskill

A Round of Applause for Our City Realty Group Auctioneer, Cameron Brain!

We are thrilled to announce that Cameron Brain has achieved remarkable success at the recent Ray White Auctioneer Championships, held at the Ray White Head Office in New Zealand. Cameron’s exceptional performance and unwavering dedication have truly set him apart.

Congratulations, Cam! Your talent and hard work have not only earned you this prestigious accolade but also made us incredibly proud. We are honored to have you as a leader within our team. Keep up the fantastic work!

Our Auckland Central office were awarded No.8 office at the recent Ray White New Zealand awards at held at Spark arena.

This isn’t just a number—it’s a reflection of the grit, passion, and unyielding commitment each team member brings every single day. I’m beyond proud to be part of such a dedicated group of professionals who constantly strive for excellence, support one another, and make our office a place where success is shared and celebrated. We are all family.

Three years running! Habeeb recognised again for exceptional customer service.

Habeeb once again demonstrated his unwavering commitment to our clients by winning the award for Excellence in Customer Service. We are incredibly proud of Habeeb’s continued dedication and the exceptional service he provides.

Some of our CRG team celebrating success at the annual Ray White New Zealand Awards.

A massive congratulations to our superstar agent Chris Cairns.

Chris & Valerie celebrated their beautiful wedding last month! You two make such an incredible couple, and we couldn’t be happier for you both! Here’s to a lifetime of love and happiness together!

Birthday wishes went to our fabulous ladies Diane, Rosa, Sue, and Jules!

Here’s to celebrating your special days and all the amazing work you do!

Congratulations go to our Dusan Valenta! They put a ring on it!

Dusan & Jessica have been enjoying a summer abroad, and they’ll come home with a little extra hardware. Congratulations Dusan & Jessica!

The five things you need to know about the housing market this week.

The Reserve Bank released its mortgage lending figures for July last week. There was $6.7 billion of new lending – up $1.7bn year-on-year. The numbers were bolstered by first-home buyers, who are taking advantage of the low deposit lending allowances, as well as increased activity by owner-occupiers and investors.

The figures reflected the July changes to the loan to value ratio (LVR) rules. Under the new rules, 20% (previously 15%) of bank loans to owner-occupiers can be done on deposits of less than 20% deposit, and up to 5% of loans to investors can be done on deposits of less than 30% (previously 35%). We always suspected this easing in the LVR rules might lead to a burst of investor purchases. The numbers for July show that the share of all lending to investors with deposits of less than 35% was 20%, up from less than 1% in June. But the share lending to investors with a deposit of less than 30% was a low 0.4%.

Meanwhile, the debt to income (DTI) ratio caps, also introduced in July, aren’t having much of an impact, which is to be expected. Less than 2% of first-home buyers took out a loan with a DTI of more than six, and less than 4% of investors took out a loan with a DTI of more than seven. This simply reflects the fact that mortgage rates are still high enough to be doing the job of naturally limiting how much debt people can service. However, as rates fall, DTIs will become more relevant, and a ballpark figure suggests that they could be much more significant at mortgage rates of around 5.5% or less. That figure could be reached mid-2025, or maybe earlier.

2. Return of “mum and dad” investors?

On a related note, the latest CoreLogic Buyer Classification data showed that mortgaged multiple property owners (MPOs, including investors) remain very keen on new-build properties, accounting for 31% of activity in that segment in July.

Meanwhile, although the overall share of buying activity going to mortgaged MPOs – across all property types and ages – remains stable at around 21%, the mix of that activity has shifted slightly more towards smaller investors and away from the larger players. With rental yields low and mortgage rates high (albeit falling), it’s still not straightforward for “mum and dad” investors to get the sums to stack up. But with the required cash top-ups now dropping alongside the fall in mortgage rates, some are seemingly dipping their toes again.

3. The labour market downturn is underway in earnest

The latest Stats NZ figures showed a 0.1% drop in filled jobs in July, the fourth in a row, with the total number of jobs down by around 25,000 from March (-1.1%). Clearly, this is a disappointing result and illustrates that even though mortgage rates will tend to boost the housing market, job losses will be working in the other direction. The weakening in the labour market took a while to get going – as it always does – but the downturn is much clearer now.

4. Dwelling consents close to a floor? Maybe?

The number of new dwelling consents approved in July (3352) was 10% higher than the same month last year, which at

face value looks pretty encouraging for a sector that has been falling steadily for about two years now. That said, June’s number was very weak, so the strength in July might just be a timing issue (e.g. “payback” for June’s weakness), while Stats NZ also noted that a large, one-off development in Queenstown with multiple consents played a role too. So I wouldn’t get carried away just yet, but there are nevertheless hints here that the floor for dwelling consents might be getting closer –consistent with the anecdotes I’m hearing. Certainly, with mortgage rates now falling, there seems a good chance that 2025 could look much better for construction.

Finally for the week, the Reserve Bank will publish more lending stats (Wednesday), which are likely to continue to show a strong preference for shorter-term fixed rates when people take out a new mortgage, switch banks, or increase their loan. In June, 71% of new lending was fixed for up to 18 months v 54% back in December. The latest figures will relate to July – i.e. before the OCR cut and the new rate wars amongst the banks – so they’ll be interesting in their own right, but August and beyond could be even more intriguing. That short end of the spectrum could get even more popular.

Please see below our latest, available properties for rent. If you have any friends or family looking for accommodation please pass this list on to them!

$2,100 per week

10 Summer Street, Ponsonby 3 Beds / 1 Bath

$600 per week

304C/130 Anzac Street, Takapuna 1 Bed / 1 Bath / 1 Car

L15X/1 Greys Ave, Auckland Central 3 Bed / 2 Bath / 2 Cars FOR RENT FOR

$650 per week

L4/10 Flower Street, Eden Terrace 4 Bed / 2 Bath

$1,500 per week

$950 per week

1207/1 Greys Ave, Auckland Central 2 Bed / 1 Bath / 1 Car

$850 per week

G07/250 Kepa Road, Mission Bay 1 Bed / 1 Bath / 1 Car

$600 per week

L4X/70 Sale Street, Auckland Central 1 Bed / 1 Bath / 1 Car FOR RENT FOR RENT FOR RENT FOR RENT FOR RENT FOR RENT

$750 per week

1206/1 Greys Ave, Auckland Central 1 Bed / 1 Bath / 1 Car

$2,000 per week

L16/6 Princes Street, Auckland Central 3 Bed / 2 Bath / 2 Cars

$1,100 per week

7c/14 Emily Place, Auckland Central 4 Beds / 3 Baths / 1 Car

To view a full list of available properties for rent follow this link or scan the QR Code on this page.

determine interest rates here in NZ, but also break costs for fixed rates.

Following this - in October, we have both the Inflation announcement (16th), and the OCR announcement (9th) - so next month will have a number of key milestones which will affect rates.

The majority of clients at the moment are fixing 6 & 12 month options. There is a big group of our clients at the moment who are looking at the 6 month option - as the rate of decrease in the last few months in rates has been

quick. However the 12 & 18 month options give a bit more stability if that is something you are looking for.

Every situation is different, so feel free to give us a call to discuss your options!

To discuss the competitive investment loan options available speak to Jamie today.

The marketing strategy is designed to reach the breadth of the active and passive buyer pool in the most effective manner, based on their Media consumption.

Our marketing strategy comprises of 3 key components; property portals, social and multi-channel digital strategy and print media.

There are 3 key portals, TradeMe Property, Realestate.co.nz and Oneroof.co.nz.

Property Portals generally attract active byers in the market, OneRoof has a unique position as it reaches both active and passive property buyers due to the diversity of information it has on the platform including property

& PASSIVE BUYERS

The Ray White City Realty Group has introduced a state-of-the-art digital solution that is powered by artificial intelligence to reach the breadth of the active and passive buyer pool across social media and multiple digital channels, including news and other high traffic websites. The programme is fully automated in the back end, it creates an audience

listings, estimated property values, market news and commentary. It is important to run campaigns across all 3 to effectively cover the breadth of the active buyer pool and a part of the massive buyer market. None of the property portals have complete market coverage and each of these portals have a set of unique audiences.

segment of active buyers specific to the property as well as reaching the passive buyer pool. The campaign is structured to deliver quality leads for the property, and it auto optimises spend across social media and multiple digital channels, skewing the spend towards channels that are performing the best.

PRIMARILY PASSIVE & SOME ACTIVE BUYERS

Print continues to play an important role to cover the breadth of the market reaching quality and highly engaged audiences. It takes criteriabased search out of the equation with respect to the active market and is the most effective medium to reach the all important passive buyer

market. This is clearly evidenced by the fact that the New Zealand herald has seen a massive 48% increase in its print readership over the last 18 months and average time spent reading the paper is over 50 minutes. The value of print is also well supported by agent feedback.

City Realty Group is the largest Ray White franchise in New Zealand with offices throughout Auckland. It is the group with the ‘family factor’ - we’re family owned and we treat people like family. We’re all about open doors and open minds. We encourage a unifying atmosphere where opportunities are created, individuals are recognized and everyone grows - from our team to vendors, investors and tenants.

Our experienced and established team service the market Auckland wide -from Residential, Luxury Apartments, waterfront properties and rentals. With a dedicated property management team and marine brokerage teams. City Realty Group has a strategic partnership with Loan Market to provide clients with the best mortgage advice and rates through brokers.

+64 (9) 281 4707

www.rwsandringham.co.nz

+64 (9) 308 5551

www.rwmtroskill.co.nz

OUR LOANMARKET MORTGAGE ADVISORS

WE CAN NEGOTIATE A LOWER RATE. WORK WITH A QUALIFIED AND COMPETENT MORTGAGE ADVISER

Mortgage Adviser