Auckland Central Market Report.

Part of the group with a family factor.

CITY REALTY GROUP CREATE RECOGNISE GROW

04. Market CommentSteady As She Goes Is Order Of The Day

08. Recent Sales June 2024

12.

Article – Tony Alexander: Reserve Bank drops the scary language - should borrowers get their hopes up?

18.

Article – Nikki Preston: Eight interest rate cuts in a row: Market turnaround on the cards, say experts

22. LoanMarket Update

06.

Auckland Central Statistics June 2024

10. Case Study & Auction Update with Cameron Brain

14. Our month in Review Top Stories & Events from the City Realty Group

20. Property Management Update

24. Our Awards & Accolades Ray White Auckland Central & Wynyard Quarter

Steady As She Goes Is Order Of The Day

July 1, 2024 – a big day for the housing market. The bright-line test has been scaled back from 10 years to two years, the loan-to-value ratio (LVR) rules have been loosened, and the debt-to-income ratio (DTI) caps came into force.

Director of City Realty Group, Daniel Horrobin comments: “What will probably be the most interesting for us is the influence the Brightline scale back to two years will have on investor intentions for their current portfolios. Will we see an increase in stock, which in the central city market is currently sitting comfortably into the 600’s after falling below 500 properties this time last year ? With so many other moving parts in the wider economic space it’s difficult to predict.”

Meanwhile back on interest rates, independent economist Tony Alexander has this to say: “At this stage, I struggle to find reasons for believing that price movement in the housing market will shift upward through winter and spring. But come summer, falling interest rates are likely to start turning things around.”

Daniels says: “This is in line with reports we are hearing which are that borrowers re-fixing interest rates right now are being advised to fix for only six to 12 months.”

This is further supported by CoreLogic reporting back in April this year that a record number of homeowners fixed on one-year terms in February, suggesting they are betting on possible interest rate falls in the near future.

Our very own Loan Market partner in our office, Jamie Maclennan adds: “Most of our clients are locking in for six,12 or 18 months at the moment with the view that we are hopefully past the peak for interest rates, and starting to make our way back down. With inflation seemingly trending in a better direction we are hoping the highest period is now behind us.”

On the auction floor this past month it’s been business as usual, reports Daniel. “Owners serious about selling are being presented with a genuine opportunity to do so with auction room activity through June producing 118 bids across 19 properties.”

“In fact,” adds Daniel, “the likelihood of selling your apartment within 90 days is far, far more likely by auction than non-auction methods, as shown by our last six months’ statistics.”

“In addition to that, our open home visitor numbers consistently demonstrate that auction properties attract significantly more interest from buyers. In the month of June alone, four auction properties were sold prior to their planned auction dates, indicating a strong willingness from buyers to engage with genuine sellers.”

“On that same topic,” continues Daniel, “over the month of June we met 271 open home visitors, a little down on May but still a healthy turnout.”

“In the rental space, rents have softened somewhat and properties are taking a little longer to move, so again, business as usual” reports Daniel.

“It’s steady as we go as the mid-winter months beckon,” concludes Daniel.

To finish on a bright note for the central city, policemen walking the beat were spotted at the foot of Queen St on Matariki holiday Friday, as police patrols on main streets increase. We say: “A very big welcome back.”

“What will probably be the most interesting for us is the influence the Brightline scale back to two years will have on investor intentions for their current portfolios”

Total Sales

June 2024

39

June 2023

There was a -64% decrease in the total number of sales year on year.

Total Sales Value Median Sales Price Median Days On Market

June 2024

$26,956,838

June 2023

June 2024

$300,000

June 2023

108 $49,644,140 $360,000 48.5

There was a -45% decrease in the total sales value year on year.

Source: REINZ

There was a -16% decrease in the total median sale price year on year.

June 2024

61

June 2023

There was a 25% increase in the total median days on market year on year.

Recent Sales.

AUCKLAND CENTRAL

Auction Case Study

274B Balmoral Road, Sandringham

28 Groups through Open Homes

4586

TradeMe.co.nz Listing Views

8 Online Enquires

15 Open Homes Conducted

8 Registered Bidders 90 Total number of Bids at Auction

7 Phone Enquires

2 Pre-Auction Offers

26 Days on Market “ It was a tough campaign in a tough market and the home was missing a CCC and a COA at the start and had a flood plain. Process. Follow it. That’s all you need for any sale. Don’t be a self-taught agent. A disaster. Get the best training from the best people as often as you can. Discipline. Stucture. Strategy. Method. Find it, learn it, practice it, just do it. Love it. Treat people around you like it’s your last day on earth.

DAMON POOLEY

The real estate landscape is experiencing a significant shift.

Positive media coverage and the banks’ decision to lower interest rates are driving increased buyer engagement across the board. This trend is particularly evident in the City Realty Group’s operations, encompassing Auckland Central, Wynyard Quarter, Sandringham, and Mt Roskill offices.

One of the most promising indicators of this revitalized market is the remarkable surge in open home attendance. Numbers have risen nearly 60% from June 2024, a clear sign that confidence is returning to both homeowners and prospective buyers. This increased activity suggests a healthier, more dynamic market environment as we approach the latter part of the year.

However, the key metric to watch remains the average days on market. Auctions continue to outperform other sales methods significantly, with properties selling in an average of 39 days. In contrast, other methods are seeing an increase in average days on market, now extending to 74 days. This stark difference highlights the efficiency and effectiveness of the auction process in the current climate.

Despite these positive signs, certain metrics have remained steady. The average number of bidders at auctions holds firm at two, and the auction clearance rate remains at 49%. These figures indicate a consistent level of

competition and a balanced market, with neither buyers nor sellers holding a definitive upper hand.

Looking ahead, the anticipated drop in the Official Cash Rate (OCR) is expected to further bolster market confidence. Lower borrowing costs will likely entice more buyers into the market, adding to the already busy landscape. The next six months are poised to be a period of heightened activity and opportunity for all market participants.

In summary, City Realty Group is witnessing a robust upturn in market engagement. The combination of positive media influence and reduced interest rates is fostering a more active and confident marketplace. As we continue through 2024, the real estate sector looks set for a bustling period, with auctions leading the charge in driving timely and competitive sales. Homeowners and buyers alike can look forward to a dynamic and promising market environment.

“One of the most promising indicators of this revitalized market is the remarkable surge in open home attendance.”

Tony Alexander: Reserve Bank drops the scary language - should borrowers get their hopes up?

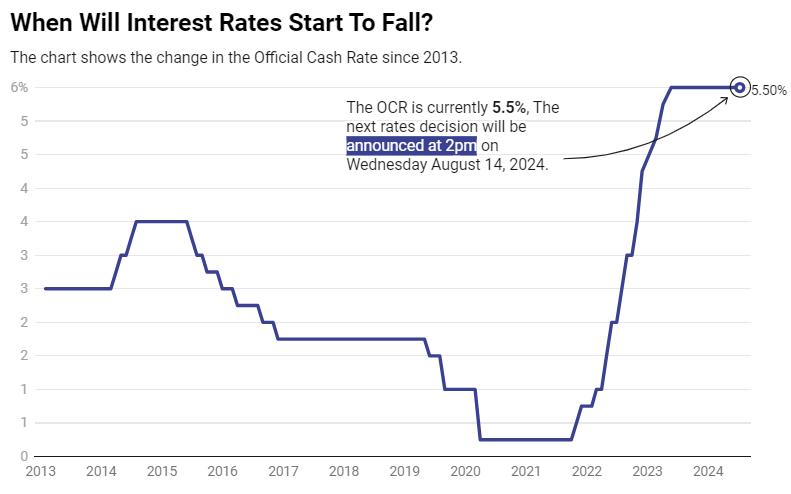

The RBNZ kept the Official Cash Rate on hold at 5.5%.

ANALYSIS: Most of the measures in the five monthly surveys I run took a turn for the worse around February this year as worries about employment lifted and people became aware of large hikes in insurance premiums and council rates. The deterioration in sentiment is now showing through in gauges of economic activity and this is prompting forecasters to shift their predictions for when the Official Cash Rate (OCR) gets cut from 2025 to the November timing I’ve sat at for some time.

Looking through my latest surveys of consumers, businesses, mortgage brokers and real estate agents I can see that

things remain at very depressed levels. But there does not appear to be any fresh deterioration underway. That is, sentiment and spending intentions have settled at recessionary levels but are not heading into territory which would prompt an immediate policy easing by the Reserve Bank.

That helps explain why this week the Reserve Bank today left the OCR unchanged at 5.5% – which was universally expected – and gave no direct message as yet that it is bringing its predicted timing of the first rate cut forward.

As discussed before, only now have we entered the period of the monetary

Chart: NZ HeraldSource: Reserve Bank of New ZealandGet the dataCreated with Datawrapper

policy tightening phase when businesses feel forced to change what they do and how they do it because passing on cost increases (for most) is no longer a viable option.

Now would be the worst time to ease monetary policy because of the risk that re-tightening would be needed in 12-18 months time. However, the Reserve Bank did what central banks do when they don’t change their cash rate, but they want to signal that their bias regarding what to do and when is shifting.

Whereas in May the Reserve Bank wrote about inflation reaching the 1-3% band by the December quarter, now committee members referred to “the second half of the year”. They did not repeat their May warning that additional policy tightening might be needed.

In reference to recent weak economic data they wrote: “Members discussed the risk that this may indicate that tight monetary

policy is feeding through to domestic demand more strongly than expected.” That is exactly what my surveys have been showing for four to five months now.

They also dropped their May comment regarding monetary policy needing to “remain at a restricted level for a sustained period” and instead wrote: “The Committee agreed that monetary policy will need to remain restrictive.”

The upshot of these changes is that wholesale borrowing costs have fallen to mild degrees in New Zealand this week and it is likely that more forecasters will bring forward their picks for when rates start falling. I am more confident of rate cuts in November.

But borrowers should not expect anything but minor rate tweaks by banks in the next few weeks – unless we get a downward surprise in the June quarter inflation number, which comes out on July 17.

www.tonyalexander.nz

- Tony Alexander is an independent economics commentator. Additional commentary from him can be found at

July in Review

Top Stories

&

Events from the City Realty Group

We celebrated Judi & Mahi’s birthday with a delicious morning tea spread.

Judi & Mahi have both been unwavering dedicated to Ray White Auckland Central for years. Here’s to many more years ahead.

Energy in our auction rooms despite gloomy news and weather.

Our busy Ray White Auckland Central Auction Rooms

Did You Say... Family First

Luke Crockford & the team Wynyard held another succesful Auction

Pictured:

July in Review

Top Stories & Events from the City Realty Group

Podcast Premiere: Tuning in with Dan, Cam & Sophie

Talking all things Real Estate with Cam, Dan and Sophie, on a podcast for Blank Canvas.

Who takes the cake?! We will.

We welcomed Stella King from her start up business “From Sugar” to talk to us about her delicious settlement gift options. Who doesn’t like cake!

Congratulations to Gabi & Ross who both achieved Premier Status recently! Celebrating Success

Casey Chen showed a tiny but important guest through her listings at the Proxima Residences.

Dan & his daughter joined the sales team to inspect this new development in Eden Terrace

It’s a... BABY!

Congratulations to Gabi on her exciting engagement and baby news! The Ray White Auckland Central & Wynyard Quarter teams celebrated with Gabi over a delicious spread following the Weekly Sales Meeting.

We recognised Casey, Habeeb, Ryan & Grant’s Premier status achievement.

Premier agents are in the top 11% in the Ray White network!

Well done to all of you!

Nikki Preston: Eight interest rate cuts in a row: Market turnaround on the cards, say experts

The week New Zealand got its mojo back.

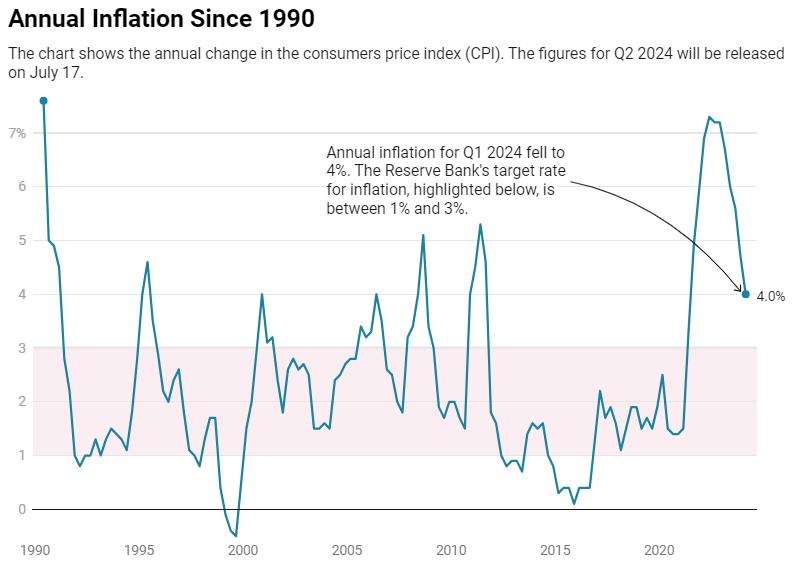

Some urgency may be returning to the housing market, with agents and mortgage brokers reporting lifts in buyer enquiry following last week’s better-than-expected inflation figures.

Anticipation of an early cut in the Official Cash Rate is building after annual inflation slowed to 3.3% in the second quarter of this year – its lowest point in three years. Banks are already primed to lower the cost of borrowing, with Westpac dropping its one-year fixed rate to 6.89% and ANZ, BNZ and Kiwibank dropping theirs to 6.85%.

Jared Cooksley, director of Ray White Mt Eden, in Auckland, told OneRoof that confidence had shifted following news of the drop in inflation.

“When buyers feel they don’t necessarily hold all the cards, you’ll see them acting a

little more swiftly,” he said.

One of Cooksley’s agents, Dean Tuffley, sold a four-bedroom home on Puriri Avenue, in Greenlane, under the hammer this week for $1.385 million, with 10 bidders registering for the auction. Another, Robyn Ellson, sold a house on Second Avenue, in Kingsland, this week after receiving multiple offers from buyers.

Harcourts salesperson Alex Dunn, who mostly sells in South Auckland, had noticed a bit FOMO in the market, with some buyers concerned prices will start to pick up again before the end of the year.

“Previously, it was like, ‘I can take my time, I’m not in an urgency to buy because possibly I can buy cheaper in two or three months’. Now, the thought is, ‘I better buy because it might be more expensive in two or three months’.”

A three-bedroom home on Second Avenue, in Kingsland, Auckland, sold after receiving multiple offers. Photo / Supplied

He had received two enquiries from firsthome buyers within an hour of one of his listings – a three-bedroom home at 1/10 Ranfurly Road, in Papatoetoe – hitting the market on Friday.

Another listing, a three-bedroom home at 1/7 Bunnythorpe Road, in Papakura, had received more interest this week than any other since it was listed three weeks ago.

First-home buyers continued to be active, he said, but there had also been a noticeable return of investors to the market, on the back of recent changes to the bright-line test and the return of interest rate deductibility.

The latest inflation figures, he said, had solidified people’s thinking that interest rates would drop soon.

Kiwibank chief economist Jarrod Kerr said buyers were right to feel optimistic. He is forecasting a cut to the OCR in November, and seven more successive cuts of 0.25 points next year.

“[Interest rates] will decline a little bit now and will decline a little bit further as the Reserve Bank cuts the OCR in November, but next year we will see some substantial declines in interest rates which will act as an accelerant for the housing market.”

Kerr said bank interest rates of 7% were restrictive and should be taken back to a more neutral setting of around 5%. “That’s a big move. They could do that quite quickly or they could take their time, depending on what inflation is doing.”

Once interest rates dropped, he expected a surge in investor activity. “I think if there’s any group going to bounce back, it will be investors and then, of course, owneroccupiers upgrading. Confidence for all in the market will improve.”

Kerr expects house prices to creep back up again, and is forecasting rises of between 4% and 7% next year.

He already had a client call him this week to talk about upgrading her house now interest rate decreases were on the cards. “There’s definitely a feeling that rates will reduce.”

Some banks were offering lower one-year rates of 6.72% down from 7% and that was before the OCR had even shifted, he said. Not all the rates were advertised, but there was wriggle room behind the scenes.

However, his advice to people was to fix for six months.

Kiwibank chief economist Jarrod Kerr says interest rate cuts will act as an accelerant for the housing market. Photo / Supplied

Interest Deductibility and why it matters for Property Investors

One key aspect of owning a rental property is understanding the intricacies of interest deductibility, a crucial concept that can significantly impact your financial outcomes as a property owner.

What is Interest Deductibility?

Interest deductibility refers to the ability of property owners to deduct the interest paid on their mortgage loans from their taxable income.

In simpler terms, the interest paid on the money borrowed to finance the purchase or improvement of a rental property can be subtracted from the property’s income, reducing the owner’s taxable income and potentially lowering their tax liability.

Two types of Deductible Interest:

1. Interest on Loans for Rental Property Purchase: If you took out a loan to purchase a rental property, the interest on that loan is typically deductible.

2. Interest on Loans for Property Improvement: If you borrow money to make improvements to your rental property, the interest on that loan is also usually deductible.

Benefits of Interest Deductibility

1. Tax Savings: By deducting the interest paid on your rental property loans, you can potentially reduce your taxable income, leading to lower tax liability.

2. Increased Cash Flow: Lowering your taxable income through interest deductibility can result in increased cash flow, providing you with more funds for property maintenance, improvements, or other investments.

Key Considerations

1. Keep Accurate Records: It is crucial to maintain detailed and accurate records of all transactions related to your rental property.

This includes invoices, receipts, and loan statements, which will be essential when claiming interest deductions.

2. Loan Allocation: If you have a mortgage that covers both your rental property and personal use, it’s essential to allocate the interest to the appropriate portion.

This ensures that you only claim deductions for the interest related to your rental property.

3. Changing Legislation: This is the big one. The previous Labour government began phasing out interest deductibility for property investors.

The new National led government intends to reverse those changes and gradually increase interest deductibility back to 100%.

As with all tax legislation the devil is in the detail and you should clarify your situation with an accountant or study the IRD rules.

“Lowering your taxable income through interest deductibility can result in increased cash flow.”

jamie.maclennan@loanmarket.co.nz

Finally some light at the end of the tunnel?

Although the Reserve Bank left the Official Cash Rate on hold at 5.50%, which is the 8th consecutive time it’s remained unchanged, in its latest announcement, it’s great to see some light at the end of the tunnel.

But the question on everyone’s mind is when will they start cutting?

The Reserve Bank has noted things such as, sticky nontradable inflation and the slow pace of disinflation in New Zealand, however they appear to be softening and although the Reserve Bank aren’t saying it, most economists have now moved their horizon for seeing a rate cut from 2025 to late 2024.

Although the window for a rate cut in 2024 is admittedly closing (there are only three scheduled OCR meetings left this year), I still think there is a plausible path for the RBNZ to start easing policy settings this year, especially if further cracks emerge in the labour market (which is a real risk).

However, irrespective of the timing of the first cut, it doesn’t alter the ultimate direction of policy. In fact, if cuts are delayed, all it does is mean a potentially more aggressive and deeper easing cycle when it does get underway.

With the market pricing in roughly one rate cut for this year and a further three to four cuts over 2025, we continue to think short term fixed rates are the way to go (6-12 months)

One of the major lenders has predicted a 12 month fixed rate will cost you 5.70% in 12 months time. Based on todays rates, thats over a 1% reduction in 12 months!

Let’s hope that is the way we go!

To discuss the competitive investment loan options available speak to Jamie today.

RAY WHITE AUCKLAND CENTRAL ARE PROUD TO BE ACKNOWLEDGED BY RATE MY AGENT FOR THE BELOW AWARDS

CURRENTLY PLACED

#1

Auckland Central

Agency of the Year 2025

#1

Grafton

Agency of the Year 2025

RateMyAgent is Australia’s leading real estate ratings and reviews website. It collects and verifies reviews from buyers, sellers, and landlords to provide an accurate and reliable assessment of real estate agencies.

RateMyAgent Awards are independently judged based on verified customer reviews and sales data.

Why choose us?

Based in the heart of Auckland City, Ray White Auckland Central & Wynyard Quarter are an awardwinning agency in Auckland City that specialise in apartment sales for investment, luxury waterfront and lifestyle.

Our 183+ dedicated professionals who understand this unique market, are all top performers who have contributed to our phenomenal results. As the Auckland central market continues to experience unprecedented growth, our Queen Street & Wynyard Quarter offices are well positioned to maintain its leadership in the market.

City Realty has a strategic partnership with LoanMarket, to provide clients with the best mortgage advice and rates with brokers throughout our offices that provide Home Loans, First Home Buyers Loans, Construction Loans, Refinance, Selfemployed Loans and Vehicle Finance – whatever the loan, LoanMarket can help.

Our office achieved the No.4 Ray White office in the world for 2018 and the No. 2 Ray White office in New Zealand for 2018 and we do the highest volume of sales across all agencies in New Zealand.

Meet the team.

TEAM - AUCKLAND CENTRAL OFFICE

Daniel Horrobin

Cameron Brain

Pauline Bridgman

Mike Richards

Ady Huang Aileen Wu

Ben Parkes

Craig Warburton

Dom Worthington

Dusan Valenta

Gillian Gibson

Habeeb Urrahman

Carl Russell Casey Chen

Chris Cairns

Grant Elliott

Kristine Liu

Cheryl Whiting

Leo Zhang

Judi Yurak

Keisha Gutierrez

Krister Samuel

Holly Cassidy Jeong Lee

Chris Guilford

Danika Ansley

Derek Yin

Manager

Wynyard Quarter, Sandringham & Mount Roskill

Belinda Henson

Leo Zhu Lisa Zhang

OUR SALES SPECIALISTS

Our strongest team yet. Selling right across Auckland Central & City fringe

SALES TEAM - WYNYARD QUARTER OFFICE

OUR LOANMARKET MORTGAGE ADVISOR

WE CAN NEGOTIATE A LOWER RATE. WORK WITH A QUALIFIED AND COMPETENT MORTGAGE ADVISER

Marco Sahar

Michelle Yurak Ryan Bridgman

Sam Huang

Steve King Steve Kirk

LoanMarket Mortgage Adviser

Jamie Maclennan

Louise Stephens

Ross Tierney

Luke Crockford

Gabriela Galateanu

Andrew Bond Ainsley Lewis

Max Beliak

Tony Warren

Tristan Young

Simon Lee