JANUARY 2025

Market Report.

04. Market CommentHeads Up, Eyes Front.

08. Mount Roskill Sales Statistics December 2024

06. Sandringham Sales Statistics December 2024

14.

Article – Tony Alexander: US punctures Kiwi hopes of cheaper mortgages in 2025

12. Case Study & Auction Update with Cameron Brain

16. Our month in Review Top Stories & Events from the City Realty Group

20. Article – Kelvin Davidson: Is NZ’s economy out of the hole yet?

22. LoanMarket Update

24. Marketing your home

26. Why choose us? Ray White Sandringham & Mount Roskill team

Heads Up, Eyes Front.

“With 2025 off to a strong start, the year is shaping up to be incredibly promising, highlighted by our highly anticipated Auction Day on 30 January,” says Daniel Horrobin, Director of City Realty Group.

“We’re gearing up for a huge Auction Day on 30 January, with what is building to be over 20 Auctions lined up at our central city office on the day. It’s shaping up to be an exceptional opportunity for sellers to beat the competition by getting ahead of the anticipated influx of listings expected in the first quarter 2025,” says Daniel.

The momentum started early with the Ray White exclusive Herald Homes publication on 4 January. “Those who worked through the holiday period have reported strong inquiry levels directly tied to this exposure,” Daniel adds.

The outlook for 2025 is further buoyed by the upcoming OCR announcement on 19 February.

“A widely expected cut to the OCR would provide a further confidence boost across the market, reinforcing the positive sentiment we’re already seeing,” he notes.

While media reports carry cautious optimism, there’s acknowledgment of positive market

activity. A NZ Herald OneRoof article on 2 January highlighted renewed interest from investors and traders in the auction room.

“Investors and traders have started to show their hands again in the auction room and while the resulting sale prices are nowhere near what they were at market peak, the bidding action has been on par. The end-of-year house price forecasts from the major banks have ranged from 5% to 10%-plus in 2025, although rising unemployment, a glut of stock on the market, debt-to-income ratio lending rules, and uncertainty in global politics may act as restraints.”

Reflecting on the bigger picture, Daniel concludes, “The central city is alive with activity—cruise ships arriving, spectacular yachting events, and back-to-back Eden Park concerts creating a vibrant backdrop for the real estate market. It’s a mood of vigilant optimism, and we’re thrilled to lead the charge into 2025. Bring it on, we can’t wait!”

The outlook for 2025 is further buoyed by the upcoming OCR announcement on 19 February. “A widely expected cut to the OCR would provide a further confidence boost across the market, reinforcing the positive sentiment we’re already seeing,” he notes.

Total Sales

December 2024

14

December 2023

7

There was a 50% increase in the total number of sales year on year.

Total Sales Value

December 2024

$18,938,489

December 2023

December 2024

$1,529,300

December 2023

$9,119,500 $1,260,000

There was a 107% increase in the total sales value year on year.

Source: REINZ

There was a 21% increase in the total median sale price year on year.

Median Sales Price Median Days On Market

December 2024

46

December 2023

52

There was a -11% decrease in the total median DOM year on year.

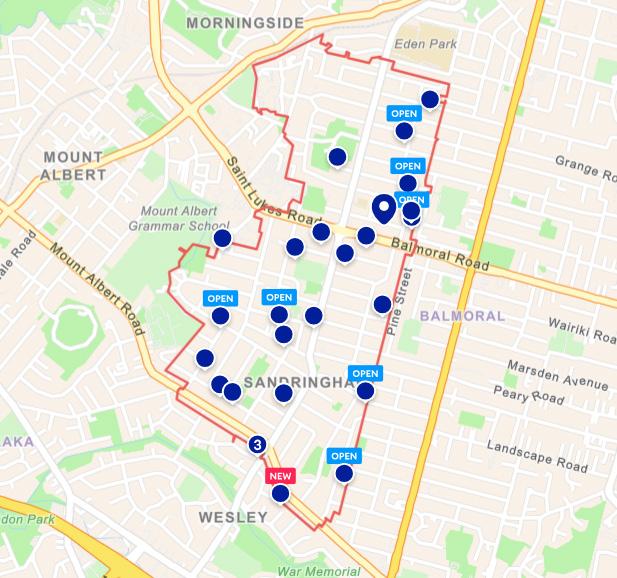

Sandringham Recent Sales.

Mount Roskill Market Statistics.

Total Sales

December 2024

28

December 2023

51

There was a -25% decrease in the total number of sales year on year.

Total Sales Value

December 2024

$28,895,888

December 2023

$51,926,556

There was a -44% decrease in the total sales value year on year.

Source: REINZ

December 2024

$906,000

December 2023

$860,000

There was a 5% increase in the total median sale price year on year.

Median Sales Price Median Days On Market

December 2024

30

December 2023

138

There was a -78% decrease in the total median DOM year on year.

Mount Roskill Recent Sales.

City Realty Group End of Year Auction Report.

As 2024 came to a close, City Realty Group concluded a successful year of Auctions, finishing on December 21st with an impressive total of 448 Auctions conducted.

Despite a challenging market environment, our team delivered a Clearance Rate of 66.22%, demonstrating resilience and expertise in the real estate auction sector. The total sales value for Auctions in 2024 reached $179,296,749, marking a remarkable 66% increase compared to the total Auction Sales value in 2023.

Among the notable results of the year, the lowest Auction Sale price was $2,000 for a leasehold apartment requiring remedial work in the Railway Campus on Te Taou Crescent, Auckland. On the other end of the spectrum, our most expensive Auction Sale achieved $8,630,000 for a luxurious penthouse apartment on St Heliers Bay Road, St Heliers. These results illustrate the diverse range of properties we successfully brought to market.

Throughout the year, we engaged with 790 registered bidders, averaging 1.7 bidders per Auction. This level of participation reflects the ongoing interest in auctions as a preferred method of buying and selling property, even in a shifting market.

Looking ahead to 2025, we are encouraged by a strong start to the year. On January 29th, our Ray White Sandringham and Ray White

Mt Roskill offices are hosting an Auction Event featuring 12 properties. Following closely, on January 30th, the Ray White Auckland Central and Ray White Wynyard Quarter offices will hold an Auction Event with 23 properties on offer. These early events indicate robust activity, fueled by a combination of growing market confidence and favorable interest rates, creating an attractive environment for buyers.

We anticipate 2025 to be a busy and dynamic year, and we remain committed to providing exceptional auction services to meet the needs of our clients. If you’re interested in learning more about Auctions or would like to discuss how we can assist with your property needs, please don’t hesitate to reach out. You can contact me directly at cameron.brain@ raywhite.com.

Here’s to another successful year of Auctions with City Realty Group!

Cameron Brain.

Auctioneer & Auction Manager 027 424 1782 cameron.brain@raywhite.com

Tony Alexander: US punctures Kiwi hopes of cheaper mortgages in 2025

The next OCR cut could be as low as 0.25%.

ANALYSIS: Happy 2025 and I hope everyone was able to get some semblance of a break over the Christmas-New Year period. At the end of my final column for 2024 written on December 17, I wrote “2025 is likely to be a year of mild economic recovery, mild declines in interest rates, and mild upward movement in prices and turnover in the real estate market.” In the past four weeks do things look any different? No.

Consider the outlook for interest rates. My warning for some months has been that underlying business pricing pressures (the need to rebuild margins) mean that as our economy improves slowly through 2025, businesses will seek to raise prices when they feel they can get away with it. Support for this view came just before Christmas

in the ANZ’s monthly Business Outlook Survey.

Whereas in June a net 35% of businesses said they plan to raise their prices in the coming 12 months, this rose to 42% in November, then 43% in December. Pricing plans are rising, not falling. This tendency was confirmed in the just-released Quarterly Survey of Business Opinion from NZIER. Whereas on average in the September quarter a net 7% of businesses said they plan to raise their selling prices, now a net 15% are planning to do so.

This is still below the average of 21% and tells us that scope exists for the Reserve Bank to cut the cash rate again come the next review on February 19. But at best the cut will be 0.5% and it may be just

There is a risk that fixed mortgage interest rates will not fall by all that much this year. Photo / Fiona Goodall

0.25%. Where might the Reserve Bank caution come from to justify just a 0.25% reduction? Developments offshore.

In the United States market expectations for easing monetary policy by the Fed this year have fallen away steadily in recent months then declined with a thud this week following far stronger than expected strength in the jobs market. The feeling amongst analysts increasingly is that the US monetary authority will be less and less feeling inflation risks lie on the downside and that extra job-creating stimulus needs to be applied to the US economy.

Some analysts in fact now think the first cut by the Fed last year of 0.5% was a mistake and one or two are now predicting that no further cuts will in fact occur this cycle. That seems unlikely but the main impact has been some sharp increases in US wholesale interest rates, which have boosted the US dollar and led to this week’s media headlines of the NZ dollar falling to just above US 55 cents from 62 cents in October.

Our central bank will surely be wondering if the new examination of a cyclical rise in inflationary pressures in the US means attention needs to shift to this development here as well. My view is that it does and hence the risk that fixed mortgage interest rates do not fall by all that much from current levels for terms of two years and beyond.

If I were borrowing currently, I’d probably still feel happy to fix only for a very short term. But there is a good chance I would jump to fixing for a three-year term before the middle of the year.

Having said that, it pays to note that there is considerable uncertainty regarding the growth, inflation, and interest rate impacts of the policies to be enacted by the incoming US president. For that reason, borrowers need to be careful not to get overly fixated on any particular view regarding where interest rates will head and how rapidly this year. Potential is high for all of us forecasters to be severely embarrassed.

- Tony Alexander is an independent economics commentator. Additional commentary from him can be found at www.tonyalexander.nz

@raywhiteaucklandcentral

@raywhitewynyardquarter

@raywhitesandringham

@raywhite.mtroskill

Party Season

What a night to remember!

Our City Realty Group crew from Auckland Central, Wynyard Quarter, Sandringham, and Mt Roskill came together at Parasol and Swing, and wow, did we party! Laughs, drinks, epic vibes— celebrating all the hard work we’ve smashed out this year.

Here’s to the best team and an even bigger 2025!

Exciting news ahead!

Our family is growing.

Congratulations to our Gabi for the safe arrival of Tyler over the Christmas and New Year Period!

More miracles are also on the way.

Congratulations to Ryan Bridgeman who is expecting twins, Jamie from LoanMarket is awaiting the arrival of his first child, also Tony Warren from our Wynyard Quarter branch who is expecting, and finally Dan & Claire who have the arrival of their second baby to look forward to!

So much family excitment this year!

Hello Yell w.

Available now for a limited time. SIZZLING SUMMER DEALS ARE HERE!

Summer is here, which means so are our seasonal property marketing specials.

Get in touch with your preferred sales agent today to find out more.

Kelvin Davidson: Is NZ’s economy out of the hole yet?

The five things you need to know about the housing market this week.

1. Consumer spending is looking better …. or worse

There were some slightly contradictory messages in the data early last week, with Stats NZ reporting that spending on electronic cards rose strongly in December (core retail +1.8% monthly), but then the BNZ-BusinessNZ Performance of Services Index remained in contractionary territory for the 10th month in a row. To be fair, I probably wouldn’t get too fixated on the different patterns; it’s more just a sign that our economy remains generally subdued/ patchy and without a clear upward trend yet. It really just adds further support to the case for another OCR cut on February 19.

2. Inflation well within target, as expected

On top of the patchy economic data, we also got further confirmation last week of subdued inflationary pressures. Headline consumer price inflation for Q4 came in at 2.2%, unchanged from the Q3 result. The non-tradable/domestic component (such as rents and council rates) eased to 4.5%, while the tradable component (e.g. petrol) was -1.1%. That split of the data wasn’t quite as anticipated, but the overall net result was still in line with expectations. As such, there was nothing here to radically alter the outlook for another 0.5% Official Cash Rate cut in February, as the Reserve Bank looks to kickstart the economy again and ward off the risk that inflation gets too low (or even negative) at some point down the track

The latest inflation figures point to another big cut in the Official Cash Rate when the Reserve Bank meets next month. Photo / Getty Images

3. Net migration remains subdued

Stats NZ reported last week that November’s net migration balance was 2200, which meant the annual running total dropped further, now sitting at around 30,600 – the lowest since December 2022. It’s difficult to know how much further it falls, and indeed may actually settle down at around that figure on a more sustained basis. But with the supply of available rental listings now high, the slowdown in migration and hence overall population is already seeing rental growth hold down at low levels.

4. Watching jobs and confidence

Coming up this week: Stats NZ will publish December’s filled jobs figures on Tuesday and ANZ will publish their business and consumer confidence surveys for January on Thursday and Friday respectively. It’ll be an interesting batch of data releases, given some hints in the November jobs data that labour market conditions aren’t collapsing, and that other sentiment indicators suggest a slow improvement in the economy. The year ahead may not be an economic boom, but it should at least fare better than 2024.

5. Back to the mortgage market again too

There’s been a lot of coverage of lending activity recently, and this week we’ll get another update of the figures from the Reserve Bank, relating to mortgage flows in December. It’d be no surprise to see a continuation of the recent upward trend for overall home lending activity, but my focus will be on the various cuts of the figures – e.g. split by loan-to-value ratio and debt-to-income ratio. The big picture lately is that high LVR (or low deposit) lending has been relatively muted, as has high DTI activity. But with internal servicing test rates at the banks having fallen, it’s going to be intriguing to see if/when high DTI lending starts to rise more appreciably again – and hence when the caps (six for owner-occupiers and seven for investors) potentially start to become a bigger factor.

CoreLogic chief economist Kelvin Davidson: “I anticipate house prices will rise in 2025, but perhaps by only 5-7%.” Photo / Peter Meecham

If history is any guide, this could lead to increased demand and rising property prices. While the past few years have been tough for many, the future looks bright, and I’m feeling optimistic about what 2025 will bring.

One major highlight will be the return of full interest deductibility – a gamechanger for investors.

Marketing your home.

A COMPREHENSIVE MARKETING STRATEGY TO REACH ACTIVE & PASSIVE BUYERS.

The marketing strategy is designed to reach the breadth of the active and passive buyer pool in the most effective manner, based on their Media consumption.

Our marketing strategy comprises of 3 key components; property portals, social and multi-channel digital strategy and print media.

Property Portals.

PRIMARILY ACTIVE & SOME PASSIVE BUYERS

There are 3 key portals, TradeMe Property, Realestate.co.nz and Oneroof.co.nz.

Property Portals generally attract active byers in the market, OneRoof has a unique position as it reaches both active and passive property buyers due to the diversity of information it has on the platform including property

Digital Marketing.

ACTIVE

& PASSIVE BUYERS

The Ray White City Realty Group has introduced a state-of-the-art digital solution that is powered by artificial intelligence to reach the breadth of the active and passive buyer pool across social media and multiple digital channels, including news and other high traffic websites. The programme is fully automated in the back end, it creates an audience

Print Media.

listings, estimated property values, market news and commentary. It is important to run campaigns across all 3 to effectively cover the breadth of the active buyer pool and a part of the massive buyer market. None of the property portals have complete market coverage and each of these portals have a set of unique audiences.

segment of active buyers specific to the property as well as reaching the passive buyer pool. The campaign is structured to deliver quality leads for the property, and it auto optimises spend across social media and multiple digital channels, skewing the spend towards channels that are performing the best.

PRIMARILY PASSIVE & SOME ACTIVE BUYERS

Print continues to play an important role to cover the breadth of the market reaching quality and highly engaged audiences. It takes criteriabased search out of the equation with respect to the active market and is the most effective medium to reach the all important passive buyer

market. This is clearly evidenced by the fact that the New Zealand herald has seen a massive 48% increase in its print readership over the last 18 months and average time spent reading the paper is over 50 minutes. The value of print is also well supported by agent feedback.

Why choose us?

City Realty Group is the largest Ray White franchise in New Zealand with offices throughout Auckland. It is the group with the ‘family factor’ - we’re family owned and we treat people like family. We’re all about open doors and open minds. We encourage a unifying atmosphere where opportunities are created, individuals are recognized and everyone grows - from our team to vendors, investors and tenants.

Our experienced and established team service the market Auckland wide -from Residential, Luxury Apartments, waterfront properties and rentals. With a dedicated property management team and marine brokerage teams. City Realty Group has a strategic partnership with Loan Market to provide clients with the best mortgage advice and rates through brokers.

+64 (9) 281 4707

www.rwsandringham.co.nz

+64 (9) 308 5551

www.rwmtroskill.co.nz

Leaders in the Auckland Residential market.

Ray White Sandringham

Ray White Mount Roskill

Meet the team.

SALES TEAM - SANDRINGHAM OFFICE

Pauline Bridgman

Amy Tsai

Kate Jiang

Diane Goer

Emily Hu

Ivan Koulin

Hugh Free

Daniel Chen

Lauren Indrisie

Alastair Hubbard

Ash Anandani

Jay Nair

Susan Woods -Markwick

Rosa Solano

Ren Agnew

Tracey Potter

Tim Cai

Yuhei Umezaki

Sammy Agnew

Claire Firmin

SALES TEAM - MOUNT ROSKILL OFFICE

OUR LOANMARKET MORTGAGE ADVISORS

WE CAN NEGOTIATE A LOWER RATE. WORK WITH A QUALIFIED AND COMPETENT MORTGAGE ADVISER

LoanMarket Mortgage Adviser

Mortgage Adviser

Damon Pooley Ethan Li

Jon Clark

Lisa Hui

Mark Li

Nana Li

May Ma

Eva Yin

Benjamin Liu

Pantea Wilson

Sara Wang

Tony Liu

Grant Harvey

Shubhrta Khanna

Ross Harvey

Maggie Liu

Anna Dong

LoanMarket

Jo Price

Davy Chen

Evie Gao

Jamie Maclennan

Ibrahim Khazi