2025

Voices of affluence

The first UHNWI survey on Greek luxury real estate

A first of its kind

For the first time, Ultra-HighNet-Worth Individuals share their views on Greece. A direct insight into how the world’s most affluent perceive luxury real estate.

A rare audience

Over 250 respondents participated, revealing the motivations, aspirations, and concerns that define global wealth’s relationship with Greece.

A truly global reach

Participants from more than 30 countries reflect the international scope of interest in Greece, positioning it firmly on the radar of the world’s elite investors.

From data to insight: A first-of-its-kind survey

Dear Partners, Clients, and Friends of Greece Sotheby’s International Realty,

When we began publishing our first reports back in 2022, our primary goal was clarity. To bring solid, reliable data to a market that was often clouded by assumptions and fragmented insights. Every edition since has been both proof of that aspiration and a testament to the hard work of our team in documenting the dynamics of Greek luxury real estate.

This report, however, represents something different. It showcases not only our commitment to clarity, but also the true power of Sotheby’s International Realty: the ability to reach and engage an audience like no other. For the first time in Greece, we asked high-networth and ultra-high-net-worth individuals, those who are already active or seriously interested in the Greek market, to share their views, their motivations, and their concerns.

Over the past 10 years, Greece's luxury and ultra-luxury real estate sector has evolved from a marginal niche into an increasingly important economic driver and a source of prestige for the country. Tourism growth, upgraded infrastructure, and Greece’s rising international profile as both an authentic and high-end destination have transformed the landscape. Yet, despite this transformation, there had never been a systematic, methodologically structured study asking UHNWIs themselves how they think, what they fear, and what they aspire to.

This gap is precisely what this survey fills. Between September 4 and 22, 2025, we gathered more than 250 completed responses, an unprecedented figure given the rarity of this audience. These participants were not random. They were drawn from a carefully built database of 14,300 qualified subscribers, developed over the course of a decade, each with proven interest as buyers or sellers in Greek luxury real estate. Among them, 10% reported a budget above €10 million, placing them firmly within the ranks of the world’s centi-millionaires.

The fact that so many from this rarefied group chose to share their views with us is in itself groundbreaking. It underlines not only the strength of Greece as a destination but also the unique power of Sotheby’s International Realty to reach, engage, and earn the trust of the world’s wealthiest.

Sincerely,

Savvas Savvaidis President & CEO, Greece Sotheby’s International Realty

Executive

Summary

Key Figures

Survey scope

• 250+ respondents from 30+ countries

• 33% Greek buyers | 67% international buyers

• Database size: 14,300 pre-qualified contacts

Purchase intention

• 63% very likely, likely, or definitely planning to purchase property in Greece.

• 52% of buyers also examine Italy (15%), France (10%), Spain (9%)

Market comparisons

• Annual Greek transaction volume: €800M–€1B

• Mediterranean luxury market: >€50B

Economic outlook

• 83% expect the Greek economy to remain stable or improve

• 44% expect property prices to rise

• 32% expect price stability

Top countries of origin

• USA 12%

• United Kingdom 10%

• France 8%

• Germany 7%

• Switzerland 6%

• GCC 4%

Preferred destinations

• Greeks: 42% Athens Riviera & northern suburbs, 28% Cyclades

• Foreigners: 40% Cyclades, 20% Ionian Islands

Buyer profile

• Median budget: €2.5M

• Main age groups: 45–54 (30%), 55–64 (34%)

• Emerging dominant archetype: the “Romantic Affluent”

Key points

• The Greek luxury residential market is entering a stable phase.

• Demand is strong and geographically diversified.

• Annual Greek transactions are estimated at €800M–€1B.

• This volume is less than 2% of the €50B+ Mediterranean luxury market. Greece remains a small player in transactional depth.

• Despite this, the country has entered the same comparison field as Italy, France, and Spain. Price convergence with mature Mediterranean destinations is already visible.

• Parallel searches confirm high competition: 52% of foreign buyers examine other countries.

• Economic sentiment is also positive. 83% expect the Greek economy to remain stable or improve.

• 73% forecast stable or rising property prices.

• Buyer origins confirm a dual domestic–international identity.

• Greeks prioritise proximity, practicality, and everyday usability.

• Foreign buyers focus on brand-driven island destinations.

• The Cyclades attract 40% of international demand. The Ionian Islands follow with 20%.

• The Athens Riviera is a shared point of interest for both groups.

• Americans, Swiss, and GCC buyers dominate upper-tier purchasing. These groups influence price benchmarks across prime destinations.

• Greece’s long-term position depends on qualitative supply expansion.

• Market development requires stable regulation and institutional clarity.

• Data transparency and consistent benchmarking are essential.

• Strengthening alternative destinations can reduce pressure on over-exposed islands.

• Greece has the fundamentals to advance further.

• The country must, however, align its institutional framework with its rising global profile.

Methodology and statistical base

The survey was conducted between September 4 and 22, 2025, gathering more than 250 completed responses from individuals belonging to the uppermost tier of wealth and purchasing power. With a margin of error of ±6%, the findings provide statistically reliable insights for strategic conclusions — particularly when considering the exceptionally high calibre of the respondents.

Composition of the sample

The composition of the sample reflects the truly international nature of Greece’s luxury property audience with Greek responders amounting to 33% of total sample, while foreign responders represent 67%.

A qualified audience

Unlike open public polls, this survey was conducted within a prequalified audience — individuals with a proven, prior engagement in Greek luxury real estate, either as buyers or sellers. All participants were drawn from a proprietary database of 14,300 subscribers, built by Greece Sotheby’s International Realty over the course of a decade. This database represents one of the most valuable assets in the field: a living network of highnet-worth individuals with verified interest and activity in the market.

Precision over volume

What makes this dataset truly unique is not its size, but its precision. This is not a random sample of the general population; it is the core of the target audience. Among respondents, 10% declared a purchase budget exceeding €10 million, meaning that

A first-of-its-kind access

This level of access and engagement is unprecedented in the Greek market. No other research to date has directly recorded the opinions and intentions of such an elite audience. Beyond its quantitative value, the survey serves as a qualitative breakthrough — providing first-hand insight into how the world’s most affluent individuals perceive Greece, what motivates their decisions, and what concerns shape their investment psychology.

More than data: a dialogue with influence

The methodological approach ensures that this report goes beyond numbers. It captures a state of mind. It is not merely a statistical exercise, but a direct dialogue with those who define the global luxury real estate landscape — a dialogue made possible only through the network, trust, and credibility of Sotheby’s International Realty.

millionaires — an extremely rare segment with immense influence on global property trends.

Source: Greece Sotheby’s International Realty

Anassa | Corfu

A unique set of participants

The 250+ respondents of this survey represent a truly global cross-section of wealth and influence. Greece’s luxury real estate market now attracts buyers from the world’s leading financial and lifestyle centres — a reflection of its growing international stature.

While Greek buyers remain a strong 33% of the total, demonstrating a maturing domestic market, the majority of respondents (67%) are international, led by the United States (12%), United Kingdom (10%), France (8%), Germany (7%), Switzerland (6%), and the Gulf Cooperation Council (GCC) countries (4%). Together, these six key international markets account for nearly half of total demand.

Beyond them, Italy and the Netherlands also appear among the extended group of origin markets, adding further depth to the Mediterranean and European profile of interest.

The psychology of buyers

Americans act emotionally, they seek experiences, images, and stories. Britons are deeply influenced by Brexit; this uncertainty makes them view Greece as a potential safe haven, but with caution. Germans are perhaps the most conservative, they will not buy unless they feel absolute stability and predictability. The French value prestige, but their domestic political climate keeps them hesitant. The Swiss are the kingmakers of the super-prime segment: few in number, but with purchasing power that shapes market balance. GCC buyers approach things differently, less concerned with price or taxation, more focused on prestige and efficiency of process.

• Greeks – Their responses indicate that they are life-driven buyers. They focus on areas close to urban centres (Athens Riviera, Northern Suburbs, Peloponnese) guided primarily by practicality.

• Americans – Represent the Romantic Affluent profile They view Greece as an experience. They have high budgets, personal optimism, and are driven more by lifestyle than by numerical investment logic.

• Britons – Safe haven seekers, though they carry “macro anxiety” due to Brexit. They seek stability but with a sense of caution.

• Germans – Conservative and risk-averse. They attach great importance to institutional stability and avoid risk.

• French – Prestige-driven, yet affected by the political uncertainty in their country.

• Swiss – Strategic and rational. They do not buy for lifestyle reasons but for asset value. They often define the super prime segment.

• GCC buyers – Ultra-wealthy, with budgets between €5–10M and above €10M. They focus on prestige and brand value rather than tax considerations.

Key countries of origin

Clarisse Meyer

Source: Greece Sotheby’s International Realty

A strong indicator of confidence

The intention to buy remains one of the most revealing indicators of this survey. Nearly two out of three respondents (63%) stated that they are either very likely, likely, or definitely planning to purchase property in Greece. Only 11% expressed a negative stance, while 6% confirmed that they will definitely buy.

A

life-driven, not speculative market

What makes this finding particularly significant is the nature of the intent. Even among respondents who anticipate a potential decline in property prices, a considerable portion still intend to proceed with a purchase. This indicates that demand in Greece’s luxury property sector is life-driven rather than speculative, motivated by lifestyle, emotional value, and the desire for permanence, rather than short-term financial gain.

The

disproportionate power of few

The 14 respondents who declared with certainty that they will purchase represent an extraordinary concentration of buying power. Though small in number, their combined wealth and capacity for high-value transactions have the potential to shift market dynamics disproportionately. In a relatively shallow market such as Greece’s, even a limited number of determined ultra-high-net-worth buyers can generate hundreds of millions of euros in transactions, influencing pricing, liquidity, and investor sentiment across key destinations.

The strength of purchase intention among such a high-income audience is both a validation of Greece’s current appeal and a signal of long-term resilience. The market is driven by conviction, lifestyle, and personal aspiration, not speculation, positioning Greece as a destination where luxury real estate reflects emotional and cultural value as much as financial opportunity.

Nearly two out of three respondents (63%) stated that they are either very likely, likely, or definitely planning to purchase property in Greece. “

Source: Greece Sotheby’s International Realty

GREECE IN THE FOREFRONT

Attitudes and regional outlook

A

cautiously optimistic mindset

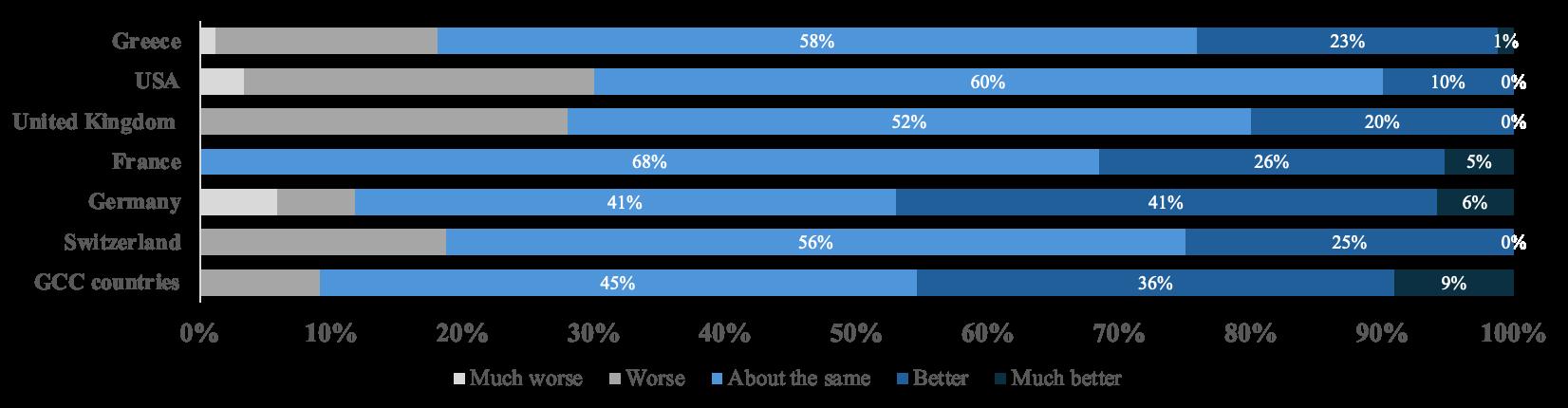

The findings in this section reveal a nuanced mindset among participants — one that balances personal confidence with broader economic caution. When asked about their personal financial situation, 39% reported an improvement over the past year, while an additional 46% expect further improvement ahead. This high level of individual optimism underscores the strong financial foundations of the survey’s participants, most of whom belong to the top tiers of global wealth.

Confidence

in Greece’s economic stability

Despite global uncertainties, confidence in the Greek economy remains robust. 83% of all respondents believe that Greece’s economy will either remain stable or improve over the coming year. This is a remarkable vote of confidence in the country’s trajectory, particularly when compared with lower optimism rates

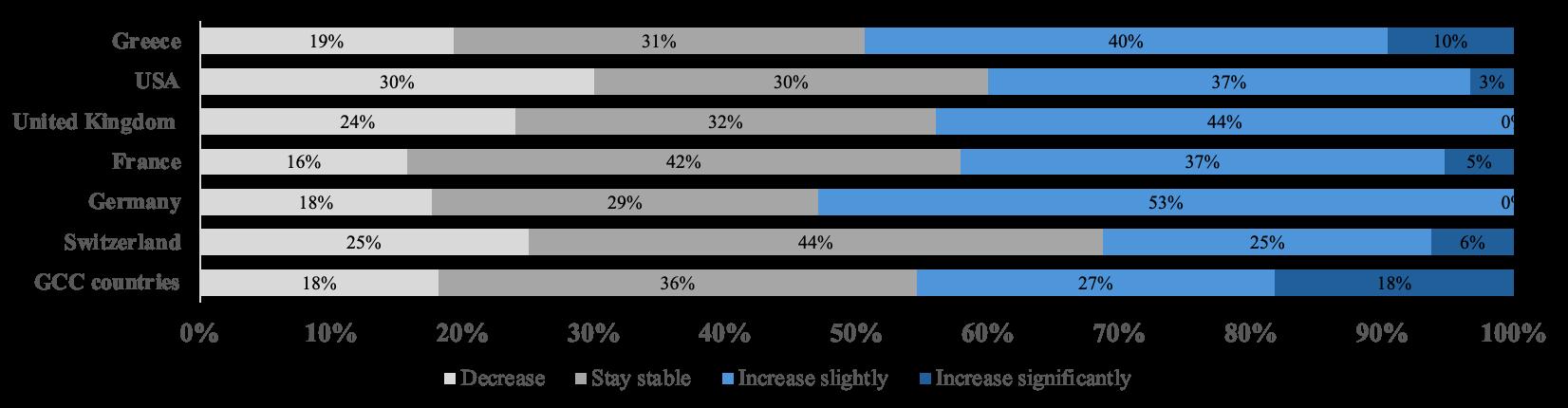

Do you expect luxury property prices in Greece to…

83% foresee the Greek economy remaining stable or improving in the year ahead “

for national economies such as the United Kingdom and France. Greece is increasingly perceived not as a volatile emerging market, but as a maturing investment environment with improved fundamentals and institutional resilience.

Market expectations: resilience over speculation

When it comes to property values, sentiment remains strongly positive. 44% of respondents expect prices in Greece to rise, while 32% anticipate stability — meaning that 73% overall foresee either steady or upward movement in the market. Only one in five (20%) predict a potential decline. What is particularly telling, however, is that even among those expecting a drop in prices, a significant share still declare themselves as likely buyers. This highlights a fundamental truth of the Greek luxury property market: transactions are lifestyle- and prestige-driven, not speculative.

How do you view the Greek economy over the next 12 months?

Source: Greece Sotheby’s International

Motivations & destinations

Drivers vs. Barriers

Every real estate decision is shaped by a balance of aspiration and restraint. In the case of high-net-worth and ultra-high-networth individuals, these drivers and barriers reveal much about their investment psychology.

Key motivations and obstacles

• Drivers: Lifestyle (57%), price expectations (47%).

• Barriers: Taxation (42%), geopolitical factors (23%), interest rates (20%).

By country:

• Greeks: Discouraged primarily by taxation.

• Americans: Focused on lifestyle, indifferent to geopolitical factors.

• Britons: Experience macro anxiety due to Brexit.

• Germans: Highly risk-averse, concerned about institutional and geopolitical stability.

• French: Motivated by prestige, but restrained by political uncertainty at home.

• Swiss: Strategic buyers focused on value preservation.

A mosaic of perspectives

The key takeaway is that, while lifestyle is the common denominator across all markets, the barriers differ dramatically. Americans view Greece as a place to experience life and remain largely unaffected by macroeconomic conditions. Britons continue to feel the lasting uncertainty of Brexit, which has left them cautious toward international markets. Germans will not act without a strong sense of institutional security. The French are drawn to prestige but weighed down by political instability at home. The Swiss buy only when they see clear guarantees that their investment will retain its value over time.

Areas of interest in Greece

The distribution of responses clearly shows two worlds:

• Greeks: 42% prefer the Athens Riviera and Northern Suburbs, 28% the Cyclades, 15% the Peloponnese, and 10% the Ionian Islands.

• Foreigners: 40% prefer the Cyclades, 20% the Ionian Islands, 15% the Athens Riviera, and 10% Crete and the Dodecanese. Greeks are oriented toward markets close to urban centres or regions with easy access, while foreigners prioritise the brand value and lifestyle appeal of the islands.

A dual market identity

Greece has a dual market identity. On one hand, Greeks act with a focus on everyday use and practicality. On the other hand, foreigners buy mainly for lifestyle and prestige. The Cyclades function as a global brand, attracting demand from Americans, Swiss, and GCC buyers, while the Peloponnese and Crete remain underdeveloped but with great potential. This highlights the need for a polycentric development strategy: if the country wishes to ease pressure on the Cyclades and avoid overvaluation phenomena, it must strengthen alternative destinations through infrastructure and international promotion.

INTENTION TO BUY

INTENTION TO BUY

Alternative destinations and Mediterranean competition

Greece among the Mediterranean elite

Greece’s rise as a global destination for luxury real estate is now beyond dispute, yet it unfolds within a highly competitive Mediterranean landscape. According to the survey, 52% of foreign buyers stated that they are also considering other countries alongside Greece. The leading alternatives are Italy (15%), France (10%), and Spain (9%), followed by Portugal (4%), Cyprus (3%), and Switzerland (2%).

Competing with heritage and maturity

Italy, France, and Spain remain the dominant benchmarks in Mediterranean luxury property. Their markets benefit from institutional maturity, deep liquidity, and long-established global branding built over decades. Greece, by contrast, has achieved something remarkable: it now stands beside these traditional leaders in perception among high-net-worth individuals, yet its market structure remains relatively young and shallow in comparison.

Prestige and imbalance

The fact that one in two international buyers compares Greece with Italy, France, or Spain confirms that the country is now playing in the “Champions League” of global luxury real estate. However, this elevated position also brings relentless comparison. Tuscany, the Côte d’Azur, and Mallorca offer regulatory stability and transactional depth; Greece offers uniqueness, authenticity, and brand allure, but not yet the same institutional framework.

Strategic insight

52% of international buyers compare Greece with Italy, France, and Spain — placing it firmly among the Mediterranean elite.

This creates a fundamental duality: Greece is both an opportunity and a challenge. In destinations such as the Cyclades and the Athens Riviera, property prices already rival, and in some cases exceed, those of more mature markets. For investors, this translates into high prestige but also higher perceived risk. The next chapter of Greece’s evolution will depend on its ability to combine its distinctive identity and emotional appeal with the institutional reliability that defines its Mediterranean peers.

Source: Greece Sotheby’s International Realty

DEEP DIVE

An analysis per country of origin for 7 of the most active buyer segments

Europe

United Kingdom

Switzerland

France

Germany

Greece

Middle East & Africa

GCC

North America

United States of America

United Kingdom

A market shaped by caution and legacy

British buyers continue to view Greece as a potential safe haven, yet their approach remains measured and cautious. The lingering psychological impact of Brexit has left a lasting mark on investor sentiment, instilling a sense of macroeconomic uncertainty that still influences purchasing behaviour.

The search for safety and predictability

British high-net-worth individuals are defined by their preference for stability, transparency, and institutional predictability. They are drawn to destinations where rules are clear, governance is consistent, and property rights are secure, areas where Greece’s steady progress toward maturity and reform plays a pivotal role in attracting their trust.

Preferred destinations and investment profile

The Cyclades, the Peloponnese, and the Athens Riviera emerge as their preferred regions, offering the right blend of lifestyle, accessibility, and perceived long-term value. Budgets for most British buyers fall in the €2–5 million range, positioning them within the upper mid-tier of the luxury segment, serious investors who balance emotional appeal with financial prudence.

Strategic insight

British buyers require clear signals of institutional stability. They are not speculative investors but discerning decisionmakers who will only proceed when they are confident that the environment is safe, transparent, and predictable. For Greece, maintaining this sense of reliability, through consistency in taxation, regulation, and property rights, is the key to unlocking sustained British investment in the luxury property market.

Source: Greece Sotheby’s International Realty

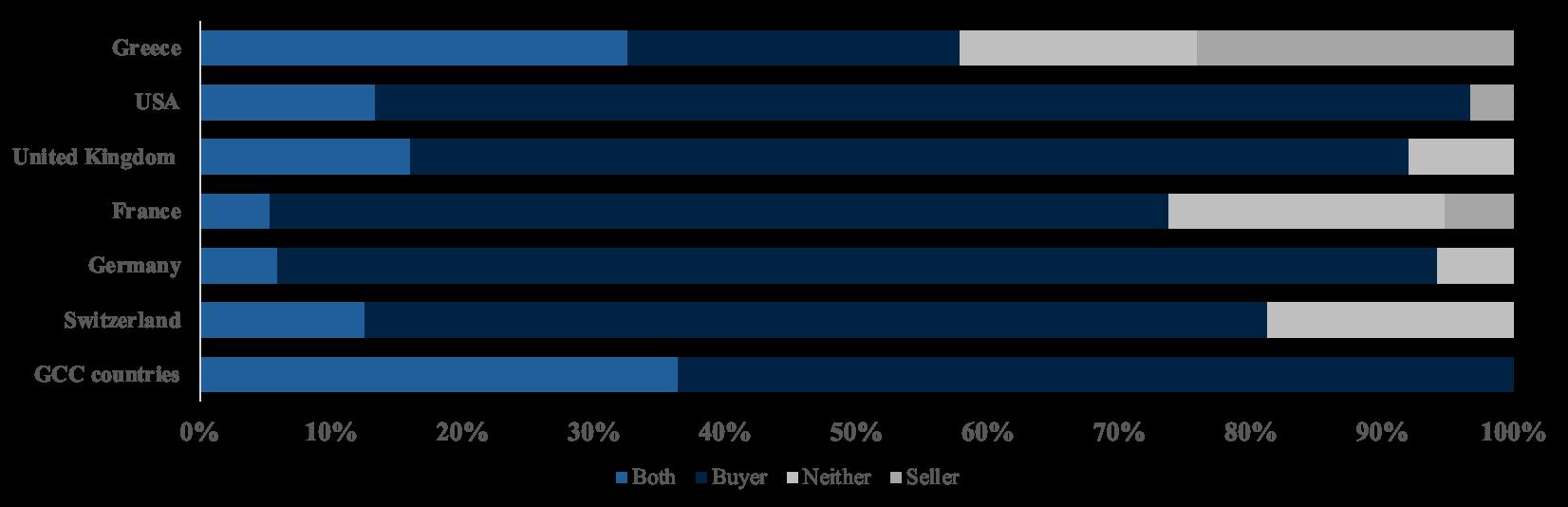

Active Role

Outlook of own real estate market

[buyer | seller | both | neither]

Strategic, analytical, and discreet

Swiss buyers represent one of the most sophisticated and calculated segments of Greece’s international demand. They approach real estate with a strategic and unemotional mindset, guided by long-term asset value rather than lifestyle aspirations. Their decisions are methodical, discreet, and deeply tied to considerations of wealth preservation and portfolio diversification.

The super-prime segment

Operating across all investment ranges, Swiss buyers’ presence is limited in numbers but disproportionate in influence: a single acquisition can redefine price benchmarks and shift perceptions of value within an entire destination.

Preferred destinations

Their interest is concentrated in Greece’s most prestigious locations, the Cyclades, led by Mykonos and Santorini, and the Athens Riviera. These areas combine architectural excellence, international recognition, and a level of privacy that aligns with Swiss expectations of discretion and exclusivity.

Strategic insight

Swiss investors are the kingmakers of the super-prime market. They do not buy for lifestyle or emotional reasons but for prestige, legacy, and capital preservation. Their participation signals credibility and maturity for the market itself. For Greece, attracting and retaining Swiss buyers requires a continued focus on transparency, long-term value stability, and exceptional quality, the very attributes that define their investment philosophy.

Source: Greece Sotheby’s International Realty

Active Role

Outlook of own real estate market

[buyer | seller | both | neither]

Drawn by prestige, tempered by caution

French buyers approach the Greek market with a mix of admiration and restraint. They are undeniably attracted by Greece’s prestige, history, and cultural depth, yet their investment sentiment is moderated by the lingering political and economic uncertainty in their own country. This duality shapes a profile of buyers who are inspired by emotion and aesthetics, but who ultimately act with deliberation.

Cultural affinity and emotional appeal

Greece’s timeless identity, a blend of heritage, beauty, and sophistication, resonates deeply with the French mindset. The nation evokes the same emotional connection that drives their appreciation for art, architecture, and authenticity. What they seek in Greece is not only a property, but a symbol of lifestyle and cultural belonging, an extension of the Mediterranean elegance they identify with.

Preferred destinations and purchasing profile

French buyers show a strong preference for the Cyclades and the Athens Riviera, destinations that reflect both natural splendour and cosmopolitan refinement. Their purchasing budgets typically range between €1–2 million, signalling a pursuit of high quality and aesthetic excellence rather than speculative return.

Strategic insight

For French buyers, narrative is everything. They respond to stories of heritage, craftsmanship, and prestige, to a Greece positioned as both authentic and elevated. While political unease at home tempers their confidence, the emotional and cultural resonance of Greece continues to draw them in. Strengthening this narrative, one that connects luxury with legacy, remains key to deepening France’s long-term engagement with the Greek property market.

Source: Greece Sotheby’s International Realty

Active Role

Outlook

Rational investors seeking security

German buyers represent the most risk-averse group among Greece’s international clientele. Their decisions are grounded in logic, prudence, and long-term value preservation rather than broad lifestyle aspirations.

Sensitivity to risk and volatility

Approximately 35% of German respondents anticipate a potential decline in Greek property prices, a perspective shaped by their conservative investment culture and sensitivity to geopolitical or institutional uncertainty. While such caution often slows their decision-making, once confidence is established, German investors demonstrate a remarkable degree of loyalty and long-term commitment to their chosen destinations.

Preferred destinations and purchasing profile

The Ionian Islands and Crete are the locations of choice for German buyers, regions perceived as authentic, environmentally appealing, and less volatile than more touristic hubs. Their typical budgets fall within the €2–5 million range, reflecting a balance between quality, sustainability, and value retention.

Strategic insight

German investors do not buy for prestige; they buy for preservation of value. Their approach is pragmatic, disciplined, and guided by an acute awareness of institutional stability. Once convinced that the environment is safe and predictable, they act decisively and with long-term perspective, becoming some of the most reliable and consistent participants in Greece’s luxury real estate landscape.

Active Role

Life-driven buyers shaping the domestic landscape

Greek buyers continue to play a defining role in the country’s luxury real estate market, representing one-third (33%) of total respondents. Their motivation is deeply personal rather than financial — they buy homes to live in, enjoy, and share with family, not for international capital placement or speculative gain.

A preference for proximity and practicality

The majority of Greek buyers, 42%, focus their interest on the Athens Riviera and the Northern Suburbs, areas that combine lifestyle appeal with year-round accessibility. Another 28% favour the Cyclades, drawn by their emotional and aesthetic resonance, while 15% express interest in the Peloponnese, reflecting a gradual diversification beyond the established hotspots.

Budget range and purchasing behaviour

Almost 94% of Greek buyers operate within the €1–5 million range. They tend to be decisive and pragmatic, often acting faster than foreign counterparts once they identify a property that aligns with their lifestyle needs.

Strategic insight

Greek buyers are life-driven, not speculative. Their decisions are guided by family, quality of life, and a long-term connection to place. While taxation remains the primary obstacle to domestic activity, their sustained engagement underlines a stable, resilient layer of demand, one that provides the Greek luxury market with both continuity and authenticity.

Source: Greece Sotheby’s International Realty

Active Role

Outlook of own real estate market

[buyer | seller | both | neither]

Powerful buyers driven by prestige and efficiency

Buyers from the United Arab Emirates, Saudi Arabia, Qatar, and Kuwait represent a small yet exceptionally influential group within Greece’s luxury property landscape. Their profile is defined by exceptional purchasing power, decisive action, and a preference for assets that combine prestige, exclusivity, and international visibility.

Focused on trust and process

Unlike other international buyers, GCC investors are largely unaffected by taxation or macroeconomic risks. Their primary concerns are transparency, credibility, and speed of execution. Once they trust the process and the counterparties involved, transactions tend to proceed swiftly and at scale. often setting new records in both value and visibility.

Preferred destinations and purchasing behaviour

Their attention is concentrated on the Cyclades and the Athens Riviera, destinations that embody Greece’s global appeal and align with their expectations of elegance, privacy, and brand recognition. While their budgets often exceed €5 million, what truly distinguishes them is not the amount spent but the impact of their confidence: when GCC buyers enter a market, they redefine its momentum.

Strategic insight

GCC buyers sit at the top tier of global purchasing power, and their engagement carries strategic significance far beyond individual transactions. For Greece, the key to deepening relationships with this audience lies in maintaining clarity, professionalism, and efficiency at every step of the buying journey. Once their trust is secured, their participation can serve as a catalyst for both prestige and market growth.

Source: Greece Sotheby’s International Realty

Active Role

Outlook of own real estate market

[buyer | seller | both | neither]

United States

Confident, active, and emotionally driven

American buyers stand out as the most optimistic and dynamic audience among all nationalities surveyed, representing 12% of total respondents. Their confidence is reflected both in their personal financial outlook and in their perception of Greece as a stable and rewarding destination. Almost 40% reported an improvement in their financial situation over the past year, and a further 43% expect continued growth ahead.

Strong belief in Greece’s potential

A notable 60% of American respondents believe that property prices in Greece will remain stable or rise in the near future — a level of optimism that underscores their long-term confidence in the country’s economic trajectory and real estate fundamentals. This sentiment aligns with a broader trend: the growing desire among affluent Americans to establish a “second home in Europe”, one that combines lifestyle, culture, and investment value.

Preferred destinations and investment profile

The Cyclades and the Athens Riviera remain the primary points of interest for American buyers, offering the blend of beauty, brand recognition, and sophistication that appeals to their sensibilities. Their budgets predominantly fall within the €2–5 million range, with a significant share extending well beyond that, placing them among the most influential buyers in terms of both scale and visibility.

Strategic insight

Americans represent the essence of the Romantic Affluent — buyers who seek experience, prestige, and legacy rather than short-term return. For them, Greece is more than an investment; it is a strategic extension of their lifestyle, a destination that connects aspiration with authenticity. Their enthusiasm and emotional engagement make them a cornerstone of the country’s high-end property demand and a powerful driver of its international appeal.

Investment range

Personal financial situation

Source: Greece Sotheby’s International Realty

Active Role

Outlook of own real estate market

[buyer | seller | both | neither]

Copyright ©

Voices of affluence is published by Greece Sotheby's International Realty. All rights reserved. Full or partial reproduction without written permission is strictly prohibited.

Disclaimer

Although every effort has been made to provide data that is current and verified, the author of this document does not guarantee or take responsibility for the accuracy of any information included in the report. The content is for informational purposes only and it should not be construed as investment advice.

Contact us

11 Voukourestiou st. Athens 10671. Greece

Tel. +30 210 968 1070

e-mail: enquiries@sothebysrealty.gr https://sothebysrealty.gr/

Cover Photo

Tosca, Corfu